AI-Powered Content Creation Market Report Scope & Overview:

The AI-Powered Content Creation Market was valued at USD 2.65 billion in 2025 and is expected to reach USD 16.00 billion by 2035, growing at a CAGR of 19.69% from 2026-2035.

AI-Powered Content Creation Market growth is being driven by the increasing demand for real-time, personalized, and scalable content across digital platforms. AI tools are increasingly utilized by organizations to reduce writing, video creation, design, and SEO optimization time and operational costs. The explosion of generative AI technologies like large language models and AI art generators is paving the way for rapid innovation in marketing, media, and e-commerce. AI integration with content management systems and multilingual capabilities is taking global content reach to another level.

AI-Powered Content Creation Market Size and Forecast

-

Market Size in 2025: USD 2.65 Billion

-

Market Size by 2035: USD 16.00 Billion

-

CAGR: 19.69% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On AI-Powered Content Creation Market - Request Free Sample Report

AI-Powered Content Creation Market Trends

-

Rising demand for automated, high-quality content is driving the AI-powered content creation market.

-

Growing adoption across marketing, media, publishing, and e-commerce sectors is boosting market growth.

-

Expansion of AI-based text, image, video, and audio generation tools is fueling deployment.

-

Increasing focus on personalization, faster content production, and cost efficiency is shaping adoption trends.

-

Advancements in natural language processing, generative AI, and machine learning are enhancing creativity and accuracy.

-

Rising need for scalable content strategies and digital engagement is supporting market expansion.

-

Collaborations between AI tool providers, creative agencies, and enterprises are accelerating innovation and global adoption.

U.S. AI-Powered Content Creation Market was valued at USD 0.73 billion in 2025 and is expected to reach USD 4.26 billion by 2035, growing at a CAGR of 19.31% from 2026-2035.

The AI Powered Content Creation Market trend in the US is driven by growing computing and processing capability, leading towards the demand for content to be automated, personalized, and thereby developed in a scalable manner across marketing, media, and digital platforms.

AI-Powered Content Creation Market Growth Drivers:

-

The Surge in Personalized and High-Volume Content Needs Is Driving Widespread Adoption of AI-Powered Creation Tools.

A major factor driving the growth of the market is the rising demand for fast, affordable, and tailored content generation in many sectors. With the focus now shifted towards producing more content for everyone and everything, brands, publishers and agencies are feeling the heat. AI-powered tools automate the generation of texts, videos, and images, thereby streamlining this process by making it quicker, more uniform, and less dependent of human effort. Meanwhile, thanks to soaring consumer appetites for real-time, ultra-personalized experiences, businesses are turning to AI to meet those demands quickly. Additionally, AI as a deeper integration with CRM, CMS and digital marketing platforms means AI-driven, smarter content targeting which can enhance engagement and conversion rates, more prominently for the retail, media and e-commerce verticals.

70% of companies using AI for content creation report increased content output—demonstrating how AI meets high-volume demand

AI-Powered Content Creation Market Restraints:

-

Concerns Over Authenticity, Bias, and IP Misuse Are Restricting Full-Scale AI Deployment in Sensitive Sectors.

AI-generated content is efficient, but from a human-created perspective, it also raises heavy questions of authenticity, originality, and ethics. The possibility of misinformation, plagiarism, and biased outputs restricts the potential value of AI tools, particularly in sensitive fields such as journalism, healthcare, and legal services. Since generative AI models can imitate human-like text or visuals, it becomes hard to separate content created by the machine from that created by a human, which can be reputationally damaging and, in some cases, lead to litigation. Then there are concerns about IP if the AI has been trained using existing content. This is driving regulatory scrutiny and cautious adoption from many enterprises that cannot put their brand and content at risk.

In Hootsuite’s Social Media Consumer 2024 Survey, 62% of consumers said they would be less likely to engage or trust content on social media if they knew it was generated using AI

AI-Powered Content Creation Market Opportunities:

-

The Integration of Multilingual and Multimodal Capabilities Is Enabling AI to Scale Content Creation Across Global Markets.

Multimodal AI, that is, AI that can consume and generate text, video, image, and audio, is making some very interesting new use cases possible. When combined with multi-lingual capabilities, AI is not just able to shorten the time to production but also create region-specific content for global audiences at scale, taking a load off the localization teams. This opens up tremendous avenues in e-commerce, gaming, education, and entertainment, all of which rely on diverse and inclusive content. Additionally, the burgeoning demand for such interactive forms of content—such as AI avatars, virtual presenters, and synthetic voiceovers—fits right in with these advancements.

AI-Powered Content Creation Market Challenges:

-

Dependence on Biased or Low-Quality Training Data Hampers Content Accuracy and Relevance, Limiting User Trust

AI-powered content tools are efficient only if there is a good set of training data present — effective in terms of quality, quantity, and variety. It can skew output -meaning that you could suffer from output that does not even relate to what you mean or reputation that brings down your brand due to its relation to bad data, a very real consequence nowadays. Several AI models still face challenges of contextual understanding, sarcasm, or cultural nuances, producing inadvertently awkward or inappropriate content. Furthermore, training such large-scale models involves immense computational power and is economically feasible only for large-scale players, making it hard for startups and mid-size organisations to gain access. Keeping models up to date, being ethical about data sourcing, and being transparent about the way content is generated will continue to be an ongoing challenge.

AI-Powered Content Creation Market Segmentation Analysis:

By Component:

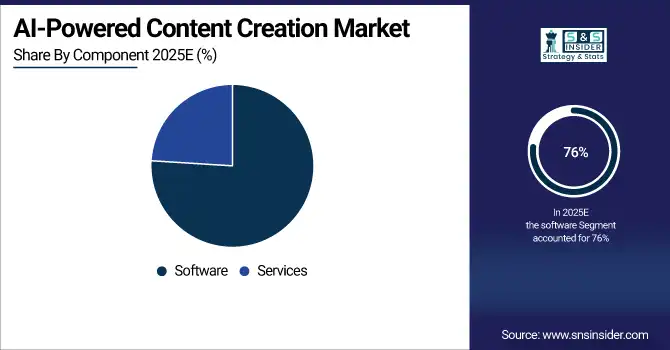

In 2025, the software segment dominated the market and accounted for 76% of the AI-powered content creation market share. Due to the growing popularity of AI-based applications such as text generation tools video editors as well as image enhancers that allow the automated and scalable creation of various types of content, the software segment is anticipated to hold the largest share. This growth is driven by continuous advancements in AI and the multiplying applications across media, retail, and e-commerce.

The services segment is expected to register the fastest CAGR in the AI-powered content creation market. This segment is receiving a boost as companies are looking for specialist assistance in deploying, customizing, and running the AI tools they are building. An increased number of SMEs and non-tech sectors are approaching us for consulting, writing training, and content strategy services. This development is a reflection of the need for quality output, compliance, and strategic alignment in AI-driven workflows.

By Creation Type:

In 2025, text segment dominated the AI-powered content creation market and accounted for a significant revenue share. The dominance of the text segment is owing to the extensive application of AI for automating blogs, social media posts, ad copy, and SEO content. Companies use AI writing tools to create volumes of quality, highly consistent content. The segment is an advantage played by generative language models and the increase in content consumption across digital marketing, publishing, and e-commerce.

The video segment is expected to register the fastest CAGR in the AI-powered content creation market. This trend is bouncing quickly with the ascent in short-structure video, forces to be reckoned with, and computerized narrating. Currently, marketers and creators are increasingly using AI tools that automatically help them with video editing, generating avatars, making voiceovers, and more. The origin for this growth is conceivably between consumers growing more partial to video content and the use of enticing, vibrant brand communication over assorted platforms.

By Deployment:

In 2025, the cloud-based segment dominated the AI-powered content creation market and accounted for 64% of revenue share. The cloud-based segment leads owing to vertical scalability, cost-efficiency, and accessibility from various devices. The cloud platforms are the go-to choice by organizations for collaboration in real time, updates at a flick of a second, and integration of AI models as a by-product. Driving factors in this segment include higher adoption among SMEs and remote teams and growing demand for SaaS-driven content tools.

On-premise segment is expected to register the fastest CAGR in the AI-powered content creation market. The rapid growth of the on-premise segment can be attributed to enterprises' need to ensure data security and regulatory compliance while retaining control over the AI-generated content. On-premise solutions are adopted by finance, healthcare, government, and similar high-risk industries to prevent the loss of intellectual property and sensitive data. On-premises adoption is further fueled by the need for customizable deployments and anxiety around cloud dependency.

By Application:

In 2025, the entertainment and media segment dominated the AI-powered content creation market and accounted for a significant revenue share. The entertainment and media segment holds a dominant position as the demand for an automated content generation solution is higher for video production, scriptwriting, and animation. AI is helping spark creativity, streamline production time, and tailor experiences to viewers. The transition to streaming platforms, digital narratives, and AR/VR formats further fuels AI implementation across media pipelines.

The marketing and advertising segment is expected to register the fastest CAGR in the AI-powered content creation market. With brands leveraging AI to quickly develop targeted content across scale, the marketing and advertising segment is rapidly growing. AI allows speedier turnarounds and customisation — whether this is in the form of ad copy, email campaigns, or social media creatives. This is driving rapid adoption of data-driven content strategies, real-time A/B testing, and cross-channel engagement.

AI-Powered Content Creation Market Regional Outlook:

North America AI-Powered Content Creation Market Insights

In 2025, the North America region dominated the AI-powered content creation market and accounted for a significant revenue share, owing to early adoption of generative AI technologies, the presence of several tech giants, and high consumption of digital content. Media, advertising, and e-commerce enterprises are integrating AI tools to automate content workflows. Benefitting from favourable regulatory frameworks, mature infrastructure providers, and substantial levels of investment in AI R&D, these regions maintain their lead.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific AI-Powered Content Creation Market Insights

According to the AI-powered content creation market analysis, the Asia-Pacific region is expected to register the fastest CAGR in the AI-powered content creation market. due to rising digitalization, growing penetration of social media, and mobile-first content strategies. AI is being used by startups and enterprises alike to satisfy content requests in varying languages and formats. Steered by government initiatives, the growing influencer economy, and the expanding reach of AI, the market is expected to proliferate in countries like China, India, Japan, and South Korea.

Europe AI-Powered Content Creation Market Insights

The Europe AI-Powered Content Creation Market is showing steady growth, and the growth in Europe is influenced by Government regulatory body for ethical AI, demand for multilingual content, and a strong media presence. Adoption is accelerating in marketing, publishing, and the government space, but continues to see more use cases in small to medium businesses and creative industries.

The United Kingdom dominated the European market with its mature digital economy, robust advertising market, and aggressive investment in AI, enabling the UK to capture European market share. The increasing use of AI in media/entertainment production, content localization, and branding is driving growth. Expansion is easily sustained by state-sponsored AI strategies and a healthy creative economy.

Middle East & Africa and Latin America AI-Powered Content Creation Market Insights

The AI-powered content creation market in the Middle East & Africa and Latin America is expanding rapidly, driven by rising digitalization, social media adoption, and demand for personalized marketing content. Businesses are increasingly leveraging AI tools for automated writing, video, and graphic generation to enhance efficiency and engagement. Supportive government initiatives, growing startup ecosystems, and investments in AI technologies further accelerate market growth across both regions.

AI-Powered Content Creation Market Competitive Landscape:

Adobe

Adobe continues to expand its generative AI ecosystem through Firefly and collaborative content platforms, enabling creators to generate, edit, and manage multimedia content across text, image, video, and design workflows. Adobe integrates third-party AI models to enhance creativity, streamline team collaboration, and provide enterprise-grade content solutions. Its platforms support ideation, production, and multi-modal outputs for professional designers, AI-Powered Content Creation Marketers, and creative teams.

-

2025: Adobe globally launched Firefly Boards, an AI-powered collaborative platform for brainstorming and content creation with integrated generative video/models from partners.

-

2025: Firefly expanded with third-party generative models (OpenAI, Google, others) to boost creative content workflows.

-

2023: Adobe released Firefly generative AI tools for text-to-image and video creation within Creative Cloud.

OpenAI

OpenAI develops multimodal generative AI solutions for content creation, enabling text, image, and video generation with advanced models. Its tools facilitate high-fidelity visual and interactive outputs for enterprises, creative professionals, and developers. By integrating image and video generation capabilities into its suite, OpenAI supports workflow automation, creative experimentation, and rapid multimedia content production across multiple channels.

-

2025: OpenAI released ChatGPT Images, an AI tool for image generation and editing, enhancing creative workflows.

-

2023: OpenAI previewed Sora, a text-to-video model enabling high-definition generative video from prompts.

Jasper AI

Jasper AI provides generative AI solutions for enterprise content creation, AI-Powered Content Creation Marketing, and workflow automation. Its platforms support multi-agent content pipelines, no-code application integration, and collaborative workspaces, enabling teams to scale content production efficiently. Jasper’s innovations embed AI into enterprise tools such as Slack and content management systems, streamlining ideation, creation, and review processes for AI-Powered Content Creation Marketers and content teams.

-

2025: Jasper introduced Jasper Grid, an intelligent interface for scaling AI-powered content pipelines.

-

2025: Jasper launched Jasper Agents and Canvas, multi-agent and workspace tools to transform AI content workflows.

-

2024: Jasper launched AI Studio with a no-code app builder and Slack integration for enterprise AI content creation.

Google LLC

Google’s AI content offerings focus on generative video, voiceovers, and creative tools integrated into Workspace. Leveraging Gemini and Veo models, Google enables cinematic AI content production, automated editing, and collaboration. Platforms such as Google Vids and Flow empower teams to create professional-quality video and multimedia content quickly, incorporating AI-generated visuals, audio, and workflows for enterprise and creative users.

-

2025: Google unveiled Flow, an AI video creation tool powered by Veo and Gemini models, supporting cinematic AI content.

-

2025: Google Vids added AI-generated voiceovers, enhancing full-content creation within Workspace.

-

2024: Google launched Google Vids, an AI-powered video creation app for collaborative content generation in Workspace.

Synthesia

Synthesia provides AI-driven video generation solutions, focusing on realistic avatar creation, automated voiceovers, and enterprise video content workflows. By licensing content from Shutterstock, Synthesia enhances AI avatar realism and fidelity, enabling scalable, high-quality video production for AI-Powered Content Creation Marketing, training, and communication. Its platform integrates with collaborative tools, supporting efficient content pipelines for corporate, creative, and educational applications.

-

2025: Synthesia signed a licensing deal with Shutterstock to train AI avatars using video content, improving realism in AI-generated video workflows.

Key Players

-

Adobe

-

Google LLC

-

Jasper AI

-

Colossyan

-

Anyword

-

Copy.ai

-

Writesonic

-

Frase

-

Rytr

-

Peppertype.ai

-

Lately.ai

-

PostGenie

-

Grok (xAI – Grok Imagine)

-

Google (Veo 3)

-

OpenAI (Sora)

-

Stability AI

-

ElevenLabs

-

Synthesia

|

Report Attributes |

Details |

|---|---|

|

Market Size in 2025 |

USD 2.65 Billion |

|

Market Size by 2035 |

USD 16.00 Billion |

|

CAGR |

CAGR of 19.69 % From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

•By Component (Software, Services) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, ASEAN Countries, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar,Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

|

Company Profiles |

OpenAI, Adobe, Google LLC, Jasper AI, Colossyan, Anyword, Copy.ai, Writesonic, Frase, Rytr, Wordform AI, Peppertype.ai, Lately.ai, PostGenie, Grok (xAI – Grok Imagine), Google (Veo 3), OpenAI (Sora), Stability AI, ElevenLabs, Synthesia, and others in the report |

Frequently Asked Questions

Ans- The North America region dominated the AI Powered Content Creation Market with 38% of revenue share in 2025.

Ans- In 2025, the software segment dominated the market and accounted for 76% of the AI-powered content creation market share.

Ans- The Surge in Personalized and High-Volume Content Needs Is Driving Widespread Adoption of AI-Powered Creation Tools.

Ans- The AI-Powered Content Creation Market was valued at USD 2.65 billion in 2025 and is expected to reach USD 16.00 billion by 2035.

Ans- The expected CAGR of the AI Powered Content Creation Market over 2026-2035 is 19.69%.

Get in Touch