Airborne ISR Market report scope & overview:

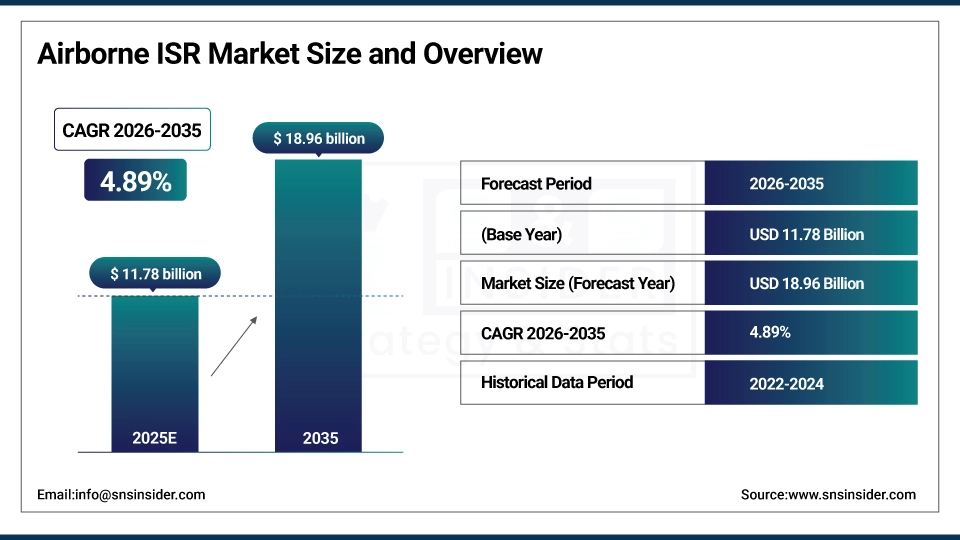

The Airborne ISR Market size is valued at USD 11.78 Billion in 2025 and is expected to reach USD 18.96 Billion by 2035 and grow at a CAGR of 4.89% over the forecast period 2026-2035.

Increasing border security needs and growing tensions amongst countries will have some positive impact on the Airborne ISR market. Increasing military spending on modernization programs and rising adoption of unmanned aerial systems are some of the other factors that spur demand for persistent surveillance and real-time intelligence. Sensor capability, AI (Artificial Intelligence), data fusion, secure communication and other advanced technology are enhancing mission effectiveness and operational efficiency. Moreover, rising efforts on the border protection, naval surveillance and advanced network centric operations would drive procurement and subsequent deployment rates ensuring the sustained growth of the market over 2026–2035.

According to industry studies, over 60% of Airborne ISR demand is driven by defense and homeland security applications, fueled by increasing geopolitical tensions, rising military modernization programs, and the growing adoption of unmanned aerial systems for real-time intelligence and surveillance operations.

Market Size and Forecast:

-

Market Size in 2025: USD 11.78 Billion

-

Market Size by 2035: USD 18.96 Billion

-

CAGR: 4.89% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Airborne ISR Market - Request Free Sample Report

Airborne ISR Market Trends:

-

UAV Adoption: Growing use of drones for cost-effective, persistent surveillance.

-

Advanced Sensors: Integration of EO/IR, radar, and SIGINT for enhanced intelligence.

-

AI & Analytics: Rapid data processing and predictive threat analysis using AI.

-

Network-Centric Operations: Real-time intelligence sharing across multiple domains.

-

Homeland Security Expansion: ISR deployment for borders, counter-terrorism, and disaster response.

U.S. Specialty Airborne ISR Market Insights:

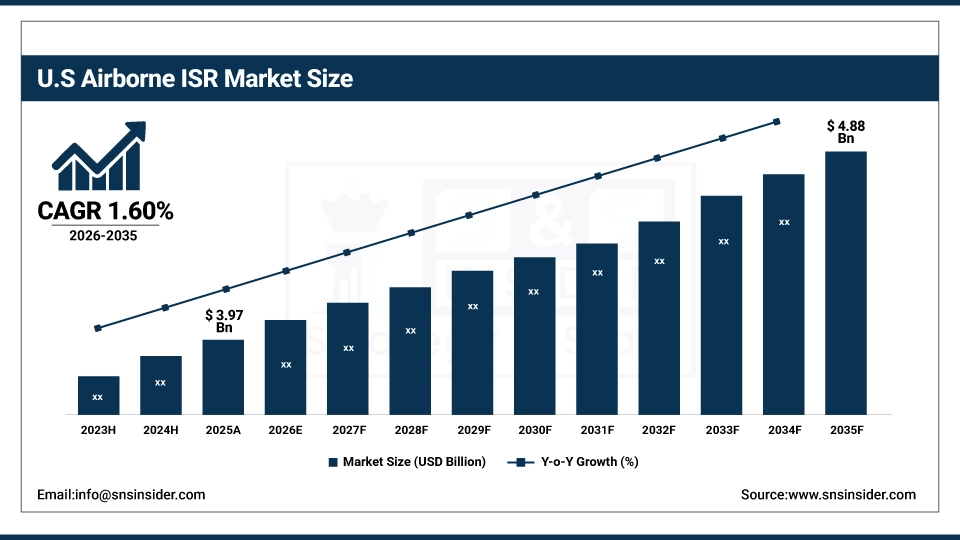

The U.S. Airborne ISR Market size is USD 3.97 Billion in 2025 and is expected to reach USD 4.88 Billion by 2035, growing at a CAGR of 1.60% over the forecast period of 2026-2035.

Increased defense and homeland security requirements, a large number of military modernization programs and proliferation in the use of unmanned aerial systems in real time intelligence are some of the factors boosting the demand for U.S. Airborne ISR systems. Developments in sensor technologies, artificial intelligence (AI), and secured communication systems improve operational capabilities and situational awareness; government programs, strategic defense investments, and collaborative network-centric warfare drive procurement at home.

Airborne ISR Market Growth Drivers:

-

Rising Defense and Homeland Security Needs

The Airborne ISR market is largely driven by rising defense and homeland security needs across the globe. Constant surveillance, quick intelligence and border vigilance are now part of government action for security. More than 60% of ISR need is for military and defense applications, indicating the supremacy in its market acceptance even according to industry research. Moreover, increasing demand for situational awareness, threat detection, and strategic reconnaissance is also driving the growth of market.

Airborne ISR Market Growth Restraints:

-

High System Costs and Complex Integration Challenges

Market expansion is limited by the high cost of acquisition and operation of airborne ISR platforms, and complexity in integrating advanced sensors, communication networks and AI-based analytics. It is estimated that almost 35% of purchasing programs are delayed through lack of funds and remote processing ability, and roll-out is hindered accordingly. In addition, the barrier against mass-adoption are constraints due to supply chain and maintenance dependencies.

Airborne ISR Market Growth Opportunities:

-

Technological Advancements and Autonomous ISR Expansion

Opportunities are great with the development of UAV, AI data analytics and multi-sensor fusion. Network-centric enabled, real-time command and control, predictive maintenance solutions ensure the most cost-effective actions are taken to enable mission effectiveness. Industry: It is reported that introduction rate of independent ISR satellites exceeds 15% annually, indicating a strong prospects for future development. Growing emphasis on smart defense programs, coalition operations and global partnership also offers potential growth for the long term in developed markets and emerging economies.

Airborne ISR Market Segment Analysis:

-

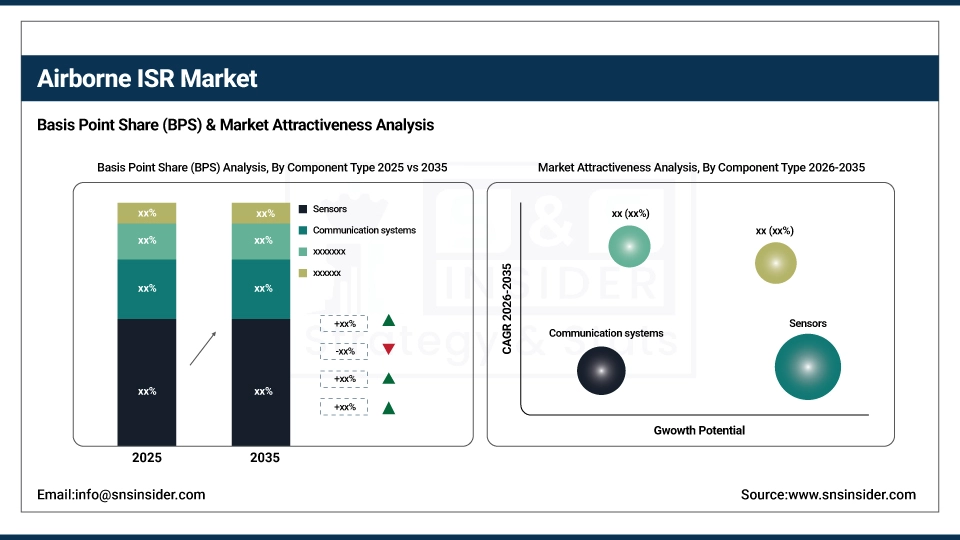

By Component Type: In 2025, sensors dominated with 50% share; communication systems are the fastest-growing segment during 2026–2035.

-

By Technology: In 2025, electro optical technology dominated with 45% share; signals intelligence technology is the fastest-growing segment during 2026–2035.

-

By Application: In 2025, military operations dominated with 55% share; disaster management is the fastest-growing segment during 2026–2035.

-

By End User: In 2025, defense forces dominated with 60% share; commercial and government agencies are the fastest-growing segment during 2026–2035.

By Component Type: Sensors Lead as Communication Systems Expand Rapidly

Sensors control the Airborne Intelligence, Surveillance & Reconnaissance (ISR) market based on their integral function of gathering real-time intelligence, monitoring borders and maintaining situational awareness in various military and homeland security operations counters. Sensors are ideal for strategic ISR because of their accuracy and long range as well as reliability.

Communication systems are rapidly increasing as secure data link and satellite, and networked C2 integration enhances the sharing of real-time intelligence. High demand from multi-domain operations for rapid decision-making and improved coordination coupled with growing deployment of advanced communication platforms, leading to strong demand for EO/IR systems.

By Technology: Electro Optical Leads as Signals Intelligence Technology Expands Rapidly

Dominance of electro optical technology is anticipated to endure, on account its demand in imaging and target tracking or high resolution surveillance for military and border security. Its reliable success in day and night operations will keep it in demand for years with wide spread usage.

SIGINT technology is advancing swiftly as governments and military agencies dedicate resources to intercept, monitor, and decode electronic communications with spying in mind. Recent advancements in AI-based signal processing combined with secure networks and multi-sensor fusion are increasing the use of SIGINT technologies in military applications as well as for homeland security.

By Application: Military Operations Lead as Disaster Management Expands Rapidly

ISR use is higher in the military for strategic reconnaissance, battlefield intelligence and mission planning. Military application is the largest segment as there is huge demand for real time situational awareness, target acquisition and operational efficiency.

There is a growing demand for real-time monitoring of natural disasters, emergency response and search-and-rescue operations and accordingly, the development of disaster management is becoming more effective. The rapid assessment of the situation, enhancement of the coordination among first responders and (by implication) subsequent deployment in time of relief bringing about marked market growth potential in humanitarian and civil applications.

By End User: Defense Forces Lead as Commercial and Government Agencies Expand Rapidly

Defense forces to account for highest market share over the forecast period, owing to use of ISR platforms for national security, border surveillance and intelligence operations in bulk. Given fixed budgets, strategic programs and a focus on sophisticated military technologies, defense is the biggest end-user sector.

Commercial and other government organizations are expanding which include such areas as the monitoring of critical infrastructure, environmental surveillance and smart city initiatives that have implemented ISR systems in greater numbers. Adoption is fuelled by: increasing requirement for real-time data gathering and analysis; as well as multi-use surveillance utilisation outside traditional defense scenarios.

Airborne ISR Market Regional Analysis:

North America Airborne ISR Market Insights:

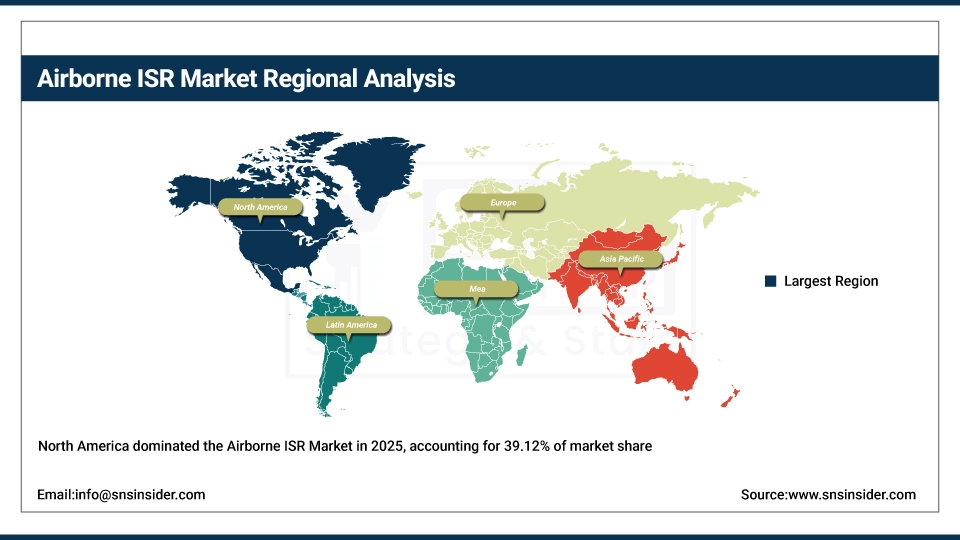

In 2025, North America’s Airborne ISR Market accounting for the highest regional revenue share of approximately 39.12% in 2025. North America homes to the highest defense and homeland security budgets consequently leading to substantial investments in advanced airborne ISR platforms. Strong aerospace and defense sectors, as well advanced sensor, AI, and communications capabilities provide the environment for widespread application of ISR systems. Moreover, the robust government policies along with the pursuance of military modernization programs and wide-scale deployment of unmanned aerial vehicles have also fueled growth in the market across this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Airborne ISR Market Insights:

Asia Pacific represents a high-growth region for the Airborne ISR market, registering a CAGR of 8.35% during 2026–2035. This robust growth is attributed to increasing defense and security spending, mounting military modernization initiatives, and rising deployment of UAVs across the region. Fast-moving geopolitical events and border protection and security needs are driving the need for instant intelligence and surveillance. Further, progress in sensor technologies, AI-enabled analytics and secure communications system in addition to favorable government projects and defense alliances, have helped expedite ISR operations thereby bolstering market expansion during the period 2026-2035.

Europe Airborne ISR Market Insights:

Airborne ISR market in Europe will be stimulated by growing defense modernization initiatives, increment of security and border surveillance and increasing utilization of unmanned aerial systems. New technologies like advanced sensors, AI-driven analytics, and secure communication systems can be used to improve real-time intelligence. Moreover, favorable government defense response and cross-border military partnerships along with strategic deployments in the NATO nations would further contribute towards stronger market growth across key European countries.

Latin America Airborne ISR Market Insights:

The demand for Airborne ISR systems in Latin American region along the three key segments of defense, security and safety will underpin market growth. Scarce infrastructure and a shift in focus to modernisation programs are driving governments to embrace low-cost ISR solutions. Furthermore, cross-border security missions, disaster relief and emergency services are spurring significant growth opportunities around Brazil, Mexico and other emerging regions.

Middle East and Africa Airborne ISR Market Insights:

The Middle East & Africa Airborne ISR (Intelligence, Surveillance and Reconnaissance) market has been on the rise owing to increasing defense requirements, challenges from terrorism, changing faces of modern warfare and growing interest for unmanned aerial vehicle systems concerning intelligence gathering. Innovations in advanced sensor systems, AI-based data analytics and networked command and control are speeding up operational efficiencies. Furthermore, strategic defense upgrade programs, cross border military collaboration and monitoring of urban areas are driving the overall market growth in the region.

Airborne ISR Market Competitive Landscape:

Northrop Grumman Corporation is a leading Airborne ISR company known for its advanced manned and unmanned ISR platforms, sensor systems, and mission integration solutions. Northrop Grumman provides comprehensive ISR capabilities for defense, homeland security, and strategic surveillance operations, focusing on long-endurance platforms and real-time intelligence gathering. The company is recognized for its advanced radar, electro-optical systems, and strong collaborations with U.S. and allied defense forces.

-

In 2025, Northrop Grumman successfully delivered the latest Global Hawk UAS upgrade with enhanced sensor fusion and AI-driven analytics for multiple U.S. Air Force ISR missions.

Lockheed Martin Corporation is a leading Airborne ISR company specializing in integrated ISR solutions, unmanned systems, and secure communication platforms. Lockheed Martin serves military and defense customers worldwide, offering high-performance airborne platforms, advanced sensor suites, and networked intelligence capabilities. The company is recognized for innovation in ISR integration, data analytics, and autonomous mission support.

-

In 2025, Lockheed Martin launched the upgraded F-35 ISR capabilities package, integrating advanced multi-sensor fusion and secure data links for enhanced battlefield awareness.

The Boeing Company is a leading Airborne ISR company known for its manned aircraft ISR platforms, unmanned systems, and maritime patrol solutions. Boeing delivers global ISR capabilities with advanced radar, electro-optical sensors, and mission control systems, focusing on defense, homeland security, and multi-domain surveillance. The company is recognized for high-endurance platforms, operational reliability, and strong partnerships with government defense agencies.

-

In 2025, Boeing introduced the new P-8A Poseidon ISR variant with enhanced maritime surveillance sensors and AI-enabled analytics for strategic missions across the Indo-Pacific region.

Airborne ISR Market Key Players:

-

Northrop Grumman Corporation

-

Lockheed Martin Corporation

-

The Boeing Company

-

BAE Systems plc

-

Raytheon Technologies Corporation

-

L3Harris Technologies Inc.

-

General Dynamics Corporation

-

Elbit Systems Ltd.

-

Airbus SE

-

Leonardo S.p.A.

-

Saab AB

-

Textron Inc.

-

Israel Aerospace Industries

-

Kratos Defense and Security Solutions Inc.

-

Sierra Nevada Corporation

-

Leidos Holdings Inc.

-

Hensoldt AG

-

Rheinmetall AG

-

General Atomics Aeronautical Systems Inc.

-

CACI International Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.78 Billion |

| Market Size by 2035 | USD 18.96 Billion |

| CAGR | CAGR of 4.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type (Sensors, Communication systems, Mission control) • By Technology (Electro optical, Radar technology, Signals intelligence technology) • By Application (Military operations, Homeland security, Disaster management) • By End User (Defense forces, Enforcement agencies, Commercial and government agencies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Northrop Grumman Corporation, Lockheed Martin Corporation, The Boeing Company, BAE Systems plc, Raytheon Technologies Corporation, L3Harris Technologies Inc., General Dynamics Corporation, Elbit Systems Ltd., Airbus SE, Leonardo S.p.A., Saab AB, Textron Inc., Israel Aerospace Industries, Kratos Defense and Security Solutions Inc., Sierra Nevada Corporation, Leidos Holdings Inc., Hensoldt AG, Rheinmetall AG, General Atomics Aeronautical Systems Inc., CACI International Inc. |

Get in Touch