Anionic Flocculants Market Report Scope & Overview:

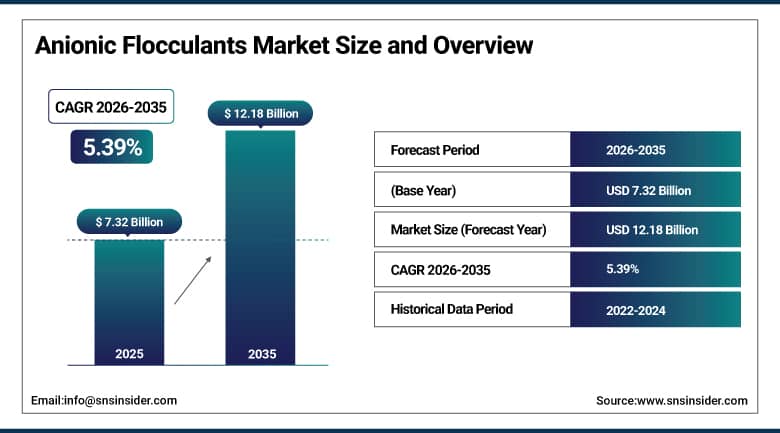

The Anionic Flocculants Market was valued at USD 7.32 billion in 2025 and is expected to reach USD 12.18 billion by 2035, growing at a CAGR of 5.39% from 2026–2035.

The anionic flocculants market is witnessing steady growth in the global market owing to the increasing demand for wastewater treatment solutions worldwide. The growing need for efficient solid-liquid separation and sludge management materials is promoting the usage of anionic flocculants across various industries. Investments made by organizations in water recycling infrastructure and environmental sustainability initiatives are contributing to market growth. Increasing developments in mining and mineral processing applications are playing a major role in driving the demand for anionic flocculants. Growth in paper manufacturing activities and stringent environmental discharge regulations are fueling the demand for anionic flocculants.

As per the WHO/UNICEF Joint Monitoring Program on water supply, sanitation, and hygiene, there are about 2.2 billion people without access to safely managed drinking water services and 3.5 billion people without access to safely managed sanitation services. According to UNEP, more than 80% of the world's wastewater is released without proper treatment.

Market Size and Forecast:

-

Market Size 2026E: USD 7.59 billion

-

Market Size 2035: USD 12.18 billion

-

CAGR (2026 - 2035): 5.39%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Anionic Flocculants Market - Request Free Sample Report

Anionic Flocculants Market Trends:

-

Rising wastewater treatment mandates drive anionic flocculants adoption, improving suspended solids removal efficiency up to 35% globally

-

Industrial sludge dewatering applications expand rapidly, with 28% increase in usage across mining and municipal sectors in 2025

-

Regulatory tightening on effluent discharge reduces chemical oxygen demand levels by 40%, accelerating advanced polymer deployment worldwide

-

Rising demand for high charge density polymers improves sedimentation rates by 30% in complex industrial wastewater streams

-

Sustainable water recycling investments increase 22%, boosting biodegradable anionic flocculant formulations in municipal treatment infrastructure

-

Technological advancements in polymer synthesis enhance flocculation efficiency up to 38%, reducing overall treatment cycle duration significantly

U.S. Anionic Flocculants Market Size Outlook:

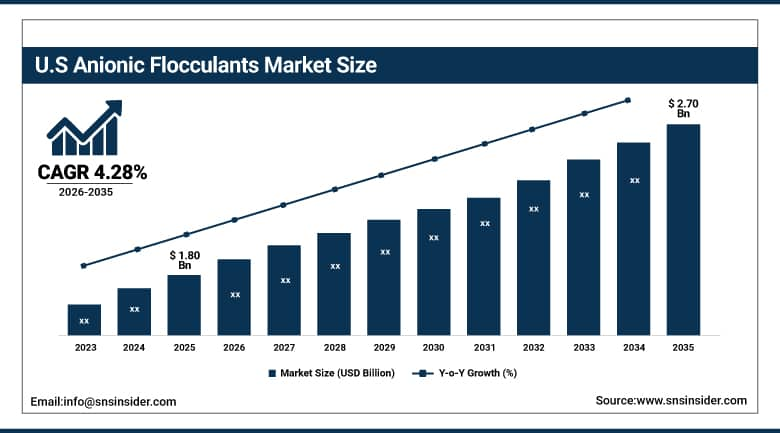

The U.S. Anionic Flocculants Market was valued at USD 1.80 billion in 2025 and is expected to reach around USD 2.70 billion by 2035, growing at a CAGR of 4.28% from 2026–2035.

The U.S. anionic flocculants market is growing consistently owing to increased demand in water treatment and wastewater management applications. The usage of anionic flocculants in solid-liquid separation, sludge dewatering, and industrial clarification processes has contributed to market growth in a consistent manner. Increased spending in the development of municipal wastewater treatment plants has generated an increase in demand for efficient flocculation chemicals. Development of mining operations, pulp and paper industries, and oil & gas facilities is further driving the demand for this product.

According to the U.S. Environmental Protection Agency, approximately 16,000 publicly owned treatment works operate across the United States, collectively treating about 34 billion gallons of wastewater daily. EPA biosolids management indicates that several million dry tons of sewage sludge are generated annually from municipal treatment processes. These measurable wastewater treatment outputs, combined with increasing regulatory compliance under the Clean Water Act, support sustained use of anionic flocculants in clarification, sedimentation, and sludge dewatering applications across U.S. municipal and industrial water treatment systems.

Anionic Flocculants Market Segment Analysis:

-

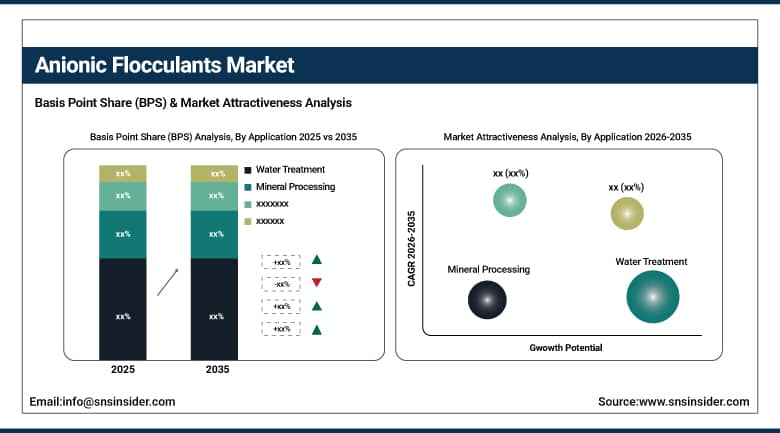

By Application, water treatment dominated the anionic flocculants market with 34.82% share in 2025; while mineral processing is the fastest growing segment with CAGR of 8.53% during 2026 to 2035.

-

By Form, powder dominated the anionic flocculants market with 34.82% share in 2025; while liquid is the fastest growing segment with CAGR of 8.53% during 2026 to 2035.

-

By End Use Industry, municipal dominated the anionic flocculants market with 34.82% share in 2025; while mining is the fastest growing segment with CAGR of 8.53% during 2026 to 2035.

-

By Functionality, coagulation dominated the anionic flocculants market with 34.82% share in 2025; while clarification is the fastest growing segment with CAGR of 8.53% during 2026 to 2035.

By Application, water treatment dominated the anionic flocculants market, while mineral processing is the fastest growing segment.

The Water Treatment segment had captured the dominated market revenue share in the anionic flocculants market in 2025. The reason behind this market dominance is the growing requirement for the treatment of municipal wastewater along with stringent requirements for discharge regulations. The increasing production of industrial wastewater and the rapid rise in the population have been fueling the demand for water purification products. Anionic flocculants have found their widespread applications in solid liquid separation, clarification, and sludge dewatering, which further adds up to its application.

Mineral Processing segment is estimated to register the fastest CAGR during the forecast period of 2026–2035 owing to the increasing activity in the mining industry along with the rising demands for ore separation. Anionic flocculants facilitate the solid-liquid separation and help in the management of tailings along with mineral extraction. Growth can also be attributed to the increase in mining activities in emerging countries, alongside the focus on efficiency.

By Form, powder dominated the anionic flocculants market, while liquid is the fastest growing segment.

Powder product type held the dominant position with the largest revenue market share in 2025. The dominance can be attributed to the longer shelf-life and easy storage factors associated with the product type. It is commonly used in large-scale industrial uses. The powder type provides cost-effectiveness in terms of transportation and handling. The high stability of the product type makes it highly efficient in water treatment procedures.

The liquid type is projected to register the fastest CAGR from 2026 to 2035 owing to the growing preference for ready-to-use formulations. The product type negates the necessity to blend, hence saving time during the treatment process. It provides high-efficiency in dispersion, which boosts its usage in automatic dosing systems.

By End Use Industry, municipal dominated the anionic flocculants market, while mining is the fastest growing segment.

Municipal was the dominated segment in the Anionic Flocculants Market, accounting for the largest revenue share in 2025. This was attributed to the high demand for wastewater treatment services from an increasing urban population. Growth in investments towards building municipal sewage treatment plants and stringent discharge standards also favor adoption. Increased requirement for effective sludge dewatering and recycling systems contributes towards higher adoption rates. Constant infrastructure upgrades in both developed and developing countries continue to stimulate adoption.

Mining was expected to be the fastest growing segment with regards to CAGR between 2026-2035. This growth would be mainly attributed to increased mining activities and increased ore processing in countries around the world. Growing mining, operations require effective methods for solid-liquid separation and tailing processing. Anionic flocculants help in improving efficiency in this regard. The increased focus on environmentally sustainable mining practices boosts growth within this application market segment.

By Functionality, coagulation dominated the anionic flocculants market, while clarification is the fastest growing segment.

Coagulation Segment led in the anionic flocculants market with the dominated revenue share in 2025. Its high share is attributed to widespread usage in primary water treatment processes and municipal sewage pre-treatment applications. The segment enables rapid solid-liquid separation through efficient destabilization of suspended solids. In addition to the rising volume of municipal sewage, increasingly stringent effluent discharge standards are driving higher demand. The low costs and broad industrial application scope of the coagulation segment in industries such as mining, pulp & paper, and chemical manufacturing are also major factors.

Clarification Segment is anticipated to witness the fastest CAGR during 2026-2035 owing to growing demand for quality treated water output. The segment finds applications in advanced filtration processes for removal of fine impurities. Stricter environmental standards and rising complexity in industrial wastewater are driving increased adoption. Investments in modern water treatment facilities and wastewater recycling infrastructure are further aiding segment demand. Pharmaceutical, food, and chemical industries are key contributors to segment growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.35% |

|

Europe |

Germany |

26.50% |

|

Asia Pacific |

China |

44.20% |

|

Middle East & Africa |

UAE |

18.50% |

|

Latin America |

Brazil |

45.60% |

North America Anionic Flocculants Market Insights.

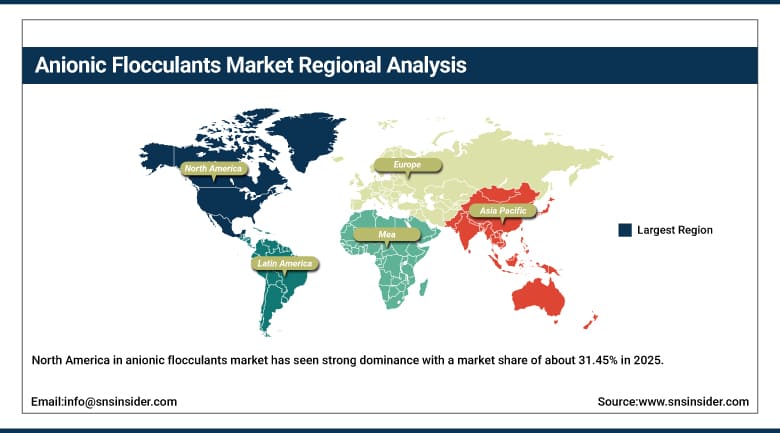

North America in anionic flocculants market has seen strong dominance with a market share of about 31.45% in 2025 due to advanced wastewater treatment infrastructure. The region benefits from strict environmental regulations and high industrial water reuse adoption. Increasing demand for municipal water treatment, mining, and paper processing applications is driving market expansion across the United States and Canada. Rising adoption in sludge dewatering and clarification processes is further supporting market leadership. Continuous government focus on clean water compliance is strengthening market dominance.

According to OECD Environmental Performance data and WHO/UNICEF Joint Monitoring Programme, over 99% of the population in the United States and Canada has access to at least basic drinking water services, while OECD countries report more than 80% of municipal wastewater receiving at least secondary treatment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Anionic Flocculants Market Insights.

The Europe anionic flocculants market shows strong presence in 2025 due to strict environmental sustainability and wastewater discharge regulations. Countries like Germany, France, United Kingdom, and Italy are key contributors to demand. High focus on industrial water treatment, pulp and paper production, and mining activities is supporting steady market growth across the region. Increasing adoption in advanced sludge management and recycling systems is further strengthening consumption. Expanding EU environmental directives are driving adoption of flocculation technologies.

According to WHO/UNICEF Joint Monitoring Programme, Europe and Northern America region has approximately 95% safely managed sanitation services coverage. As per the European Commission Urban Waste Water Treatment Directive, all agglomerations above 2,000 population equivalents require collection and secondary treatment, with reported compliance above 90% in many member states. These measurable wastewater treatment and sludge management standards drive consistent demand for anionic flocculants in solids-liquid separation and municipal effluent treatment processes across Europe.

Asia Pacific Anionic Flocculants Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the anionic flocculants market during the forecast period with a market share of about 7.19% in 2025. Rapid industrialization and urbanization are driving strong demand across China, India, Japan, South Korea, and Southeast Asia. Expanding water treatment infrastructure, mining operations, and paper manufacturing activities are significantly boosting adoption. Rising concerns over industrial wastewater discharge and river pollution are further accelerating market growth. Large scale infrastructure development supports strong regional demand.

According to UN-Water and UN DESA reporting on SDG 6, more than 80% of global wastewater is discharged without adequate treatment, highlighting widespread demand for water clarification systems.

As per FAO AQUASTAT, agriculture accounts for approximately 70% of global freshwater withdrawals, increasing reliance on efficient water recycling and reuse systems. As stated by UN DESA World Urbanization Prospects 2022, the Asia-Pacific region accounts for nearly 60% of the global population, significantly driving municipal and industrial wastewater generation and supporting adoption of anionic flocculants in treatment processes.

Middle East & Africa and Latin America Anionic Flocculants Market Insights.

The Middle East & Africa region along with Latin America is witnessing steady growth in the anionic flocculants market due to rising water scarcity challenges. Countries like UAE, Saudi Arabia, South Africa, Brazil, and Mexico are emerging as key demand centers. Increasing investments in desalination plants, mining operations, and oil and gas wastewater treatment are supporting market expansion. Growing need for clean water access and industrial effluent management is further boosting product adoption. Rising industrialization strengthens long term demand outlook.

As per UN DESA, urban population share is 81% in Latin America and 43% in Africa, with Middle East around 64%, indicating high wastewater treatment demand driving anionic flocculant usage in municipal and industrial effluent systems across regions globally.

Market Dynamics:

Growth Drivers: Increasing Demand for Efficient Wastewater Treatment Solutions Across Municipal and Industrial Sectors

Population growth and fast-paced industrialization have resulted in the rise in wastewater production across the world. This has created the need for the development of highly effective solutions for solid liquid separation processes in both municipal and industrial water treatment facilities. Anionic flocculants find widespread application in the removal of impurities from water. Higher investments and stringent regulations related to water recycling and discharge have been instrumental in boosting the adoption of anionic flocculants. Growth in the mining, paper, and chemical industry has augmented demand as well.

According to industry insights gained from recent developments, the trend of strict wastewater discharge regulations within the Asia-Pacific and North America is fostering the uptake of efficient anionic flocculants within municipal wastewater and mining wastewater treatment operations; SNF Floerger, Kemira, and Solenis have been making investments towards this end and will continue to do so in 2025. Improvements in water recycling and dosing technologies are enabling enhanced efficiency gains of 15%-25%.

Restraints: Environmental Concerns and Regulatory Restrictions on Chemical Based Water Treatment Usage

Environmental issues associated with chemicals used in treated water are posing constraints to market growth. There are stricter norms governing the release of wastage and use of chemicals in various geographical locations. The use of certain chemicals in the preparation of flocculants may pose problems in the disposal of sludge, creating environmental issues. Environmental agencies are promoting the use of environmentally friendly and biodegradable substances. This complicates the use of the product to a great extent.

Opportunities: Rising Adoption of Advanced Water Recycling and Zero Liquid Discharge Technologies

Implementation of the water recycling system and zero liquid discharge technology is generating significant business prospects. Industries are investing in water recycling efforts to minimize reliance on fresh water. Anionic flocculants are vital for achieving higher separation efficiencies and managing sludges. Industrial growth in developing nations will continue to stimulate demand for anionic flocculants. Government programs promoting sustainable use of water resources and water pollution control will provide impetus to the market development. Higher investments in intelligent water treatment facilities will offer future growth prospects.

As per the World Water Development Report 2024 by UN-Water and UNESCO, while estimates that almost 56% of the world's domestic wastewater is treated safely, according to the World Bank figures, the level of treatment of wastewater in urbanized areas exceeds 70% in developed nations, but the legal system, such as Central Pollution Control Board of India, has adopted Zero Liquid Discharge.

Recent Developments:

-

2026: SNF Group focuses on planned global capacity expansions and sustainability-driven polymer innovations for advanced wastewater treatment applications worldwide growth.

-

2025: Kemira Oyj advanced its water treatment chemicals strategy, emphasizing sustainable flocculant solutions and efficiency improvements across pulp, paper, and municipal water sectors.

-

2025: BASF SE progressed its strategic portfolio restructuring and low-emission production initiatives, strengthening focus on core chemicals and sustainability transformation programs globally.

-

2024: Ecolab Inc expanded digital water management solutions and sustainability programs improving industrial efficiency and reducing freshwater consumption globally initiatives.

Anionic Flocculants Market Key Players are:

-

SNF Group

-

BASF SE

-

Kemira Oyj

-

Solenis LLC

-

Ecolab Inc.

-

Nouryon

-

Ashland Inc.

-

Kurita Water Industries Ltd.

-

Solvay S.A.

-

Arkema S.A.

-

PetroChina Company Limited

-

China Petroleum & Chemical Corporation

-

Anhui Jucheng Fine Chemical Co., Ltd.

-

Beijing Hengju Group Co., Ltd.

-

Yixing Bluwat Chemicals Co., Ltd.

-

Yixing Cleanwater Chemicals Co., Ltd.

-

Shandong Polymer Biochemicals Co., Ltd.

-

Zhejiang Xinhai Petrochemical Co., Ltd.

-

Henan Tianrun Chemical Industry Co., Ltd.

-

Xitao Polymer Co., Ltd.

Anionic Flocculants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.32 Billion |

| Market Size by 2035 | USD 12.18 Billion |

| CAGR | CAGR of 5.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Water Treatment, Mineral Processing, Paper Production, Textile Industry, Oil and Gas, Chemicals and Materials) • By Form (Powder, Liquid, Emulsion, Chemicals and Materials) • By End Use Industry (Municipal, Mining, Pulp and Paper, Food and Beverage, Pharmaceutical, Chemicals and Materials) • By Functionality (Coagulation, Clarification, Sedimentation) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SNF Group, BASF SE, Kemira Oyj, Solenis LLC, Ecolab Inc., Nouryon, Ashland Inc., Kurita Water Industries Ltd., Solvay S.A., Arkema S.A., PetroChina Company Limited, China Petroleum & Chemical Corporation (Sinopec), Anhui Jucheng Fine Chemical Co., Ltd., Beijing Hengju Group Co., Ltd., Yixing Bluwat Chemicals Co., Ltd., Yixing Cleanwater Chemicals Co., Ltd., Shandong Polymer Biochemicals Co., Ltd., Zhejiang Xinhai Petrochemical Co., Ltd., Henan Tianrun Chemical Industry Co., Ltd., Xitao Polymer Co., Ltd. |

Frequently Asked Questions

The anionic flocculants market is expected to grow at a CAGR of 5.39% from 2026 to 2035.

The anionic flocculants market was valued at USD 7.32 billion in 2025.

Rising demand for wastewater treatment, strict environmental discharge regulations, and increasing industrial water recycling needs are driving global market growth.

The water treatment segment dominated the market in 2025 due to high demand for municipal and industrial wastewater treatment and sludge management.

North america dominated the anionic flocculants market due to advanced wastewater infrastructure, strict environmental regulations, and high industrial water reuse adoption.

Get in Touch