Application Processor Market Report Scope & Overview:

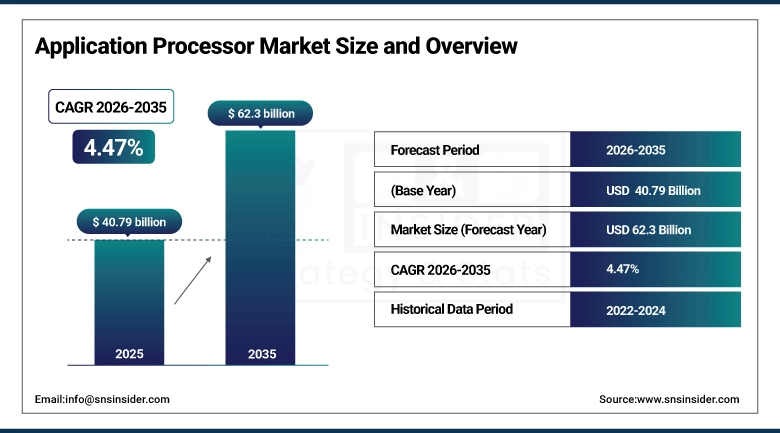

The Application Processor Market was valued at USD 40.79 billion in 2025 and is expected to reach USD 62.3 billion by 2035, growing at a CAGR of 4.47% from 2026–2035.

Application processors are the computing chips responsible for the execution of operating systems and application software on smartphones, tablets, smart watches, smart TVs, and in recent times automotive electronics and Industrial Internet of Things devices. They represent the intelligence of such modern gadgets performing functions ranging from graphical display to AI computations and networking among others. The market growth is fueled by the unrelenting quest for faster and efficient processors for enhanced device functionality. Cutting-edge process technology at 3nm and 5nm by TSMC and Samsung is helping produce desktop-quality processors for handheld form factors.

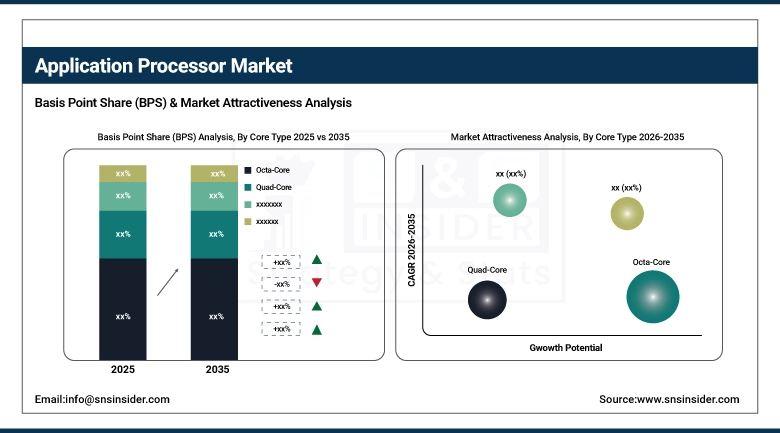

Currently, the octa-core CPU is seen as the most preferred design in the CPU segment with 48.1% of the market share in 2023. This design can perform complex calculations, multitasking and running background tasks with the use of energy-saving selective cores, which makes it the most suitable choice for diverse applications from low-budget smartphones to expensive smartwatches.

The automotive application processors segment is projected to be the fastest-growing CAGR segment due to the software-defined car concept that needs substantial computational power. A modern EV with assisted driving technology will go through terabytes of sensor information every hour, and an application processor previously reserved for high-performance computers will be used.

Market Size and Forecast:

-

Market Size in 2025: USD 40.79 Billion

-

Market Size by 2035: USD 62.3 Billion

-

CAGR: 4.47% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Application Processor Market - Request Free Sample Report

Application Processor Market Trends:

-

Advanced process node migration to 3nm and 2nm delivering significant performance and power efficiency gains in flagship smartphone processors.

-

Processing capabilities for AI being incorporated into application processors for on-device machine learning, voice recognition, and image enhancement.

-

RISC-V processors increasing in popularity as an open architecture alternative to ARM processors for IoT and embedded systems.

-

5G modems being incorporated into application processors, resulting in single chip devices that are lower in cost and power requirements for smartphones.

-

Application processors for the automotive industry expanding in growth to enable ADAS, autonomous driving, and software-defined cars.

-

Smart wearables causing a need for low-power processors with hardware accelerators for monitoring one’s health.

-

Edge AI inference becoming a standard differentiator in mid-to-high-end application processors.

U.S. Application Processor Market Size Outlook:

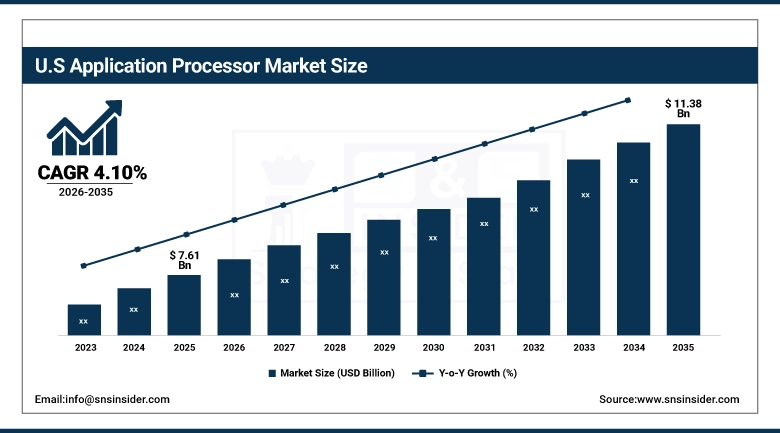

The U.S. Application Processor Market was valued at USD 7.61 billion in 2025 and is expected to reach USD 11.38 billion by 2035, at a CAGR of 4.10% from 2026 to 2035.

The market for application processors in the U.S. is influenced by Qualcomm, Apple, and Intel, who are major fabless semiconductor manufacturers for smartphones, wearables, and computing devices. The premium category of semiconductors is defined by Apple’s A-series chips, which power the iPhone, and M-series chips, which power the Mac computers. The CHIPS Act will influence the development of American semiconductor manufacturing, particularly the construction of fabs by companies such as Intel and TSMC’s Arizona facility. The adoption of ADAS systems and infotainment systems in American vehicles is an emerging application area for processors in the U.S.

Apple Silicon's success in replacing Intel processors in Mac computers with its own ARM-based M chips has reshaped the U.S. computing market and demonstrated that the ARM architecture can deliver superior performance-per-watt in even the most demanding computing applications, a finding that is now influencing data center and server processor designs globally.

Application Processor Market Segment Insights:

-

Based on Core Type, Octa-Core processors dominated with 48.1% share in 2025 and are projected to maintain the fastest CAGR above 22%.

-

Based on End-Use Device, Smartphones held the largest share; Smart Wearables is the fastest-growing device segment (CAGR).

-

Based on Architecture, ARM-Based processors dominate with approximately 90% market share; RISC-V is the emerging alternative architecture.

-

Based on Process Node, 5nm–10nm nodes led in 2025; Below 5nm (3nm, 2nm) is the fastest-growing process technology segment.

By Core Type: Octa-Core processors dominate and expected to grow fastest

The market is dominated by octa-core processors, with approximately 48.1% of market share due to their capability to combine performance-efficient cores together with power-efficient cores using big.LITTLE or DynamIQ technology. Octa-core processors help in efficient processing of games, videos, and even artificial intelligence computations, all the while keeping in mind the efficiency of battery usage. Octa-core processors are extensively used in premium smartphones, and some major players in the sector include Qualcomm and Apple; the reason behind this growth is because these processors are gaining traction within mid-range smartphones. However, quad-core processors serve the purpose of budget smartphones, tablets, and IoT devices, providing just enough computing capability to do simple tasks. Decacores and customized multicore processors have different uses within the industries of automobile and robotics.

By End-Use Device: Smartphones Market dominates, Smart Wearables grows fastest

The End-User Segment of Application Processor Market is dominated by Smartphones, with annual shipments of over 1.2 billion devices per year, all utilizing an application processor inside. High levels of competition between Qualcomm, Mediatek, and Samsung's Exynos processor range are ensuring constant progress in processing power and energy consumption of premium Android phones, with Apple's A-series chips serving the same purpose for their devices. Tablets are the second-largest end-user application, also using very similar application processors as smartphones. The Apple iPad Pro with M-series chipsets is pushing tablet computing performance towards that of laptops, with Samsung and Lenovo Android tablets using processors from Qualcomm and Mediatek.

The rapidly expanding sector involves smart wearables like smartwatches and activity trackers, which require processors that consume extremely low amounts of energy due to the requirement of performing continuous health monitoring, connectivity, and AI applications. The other rapidly expanding sector involves automotive solutions, used in advanced driver assistance systems (ADAS) and infotainment systems requiring real-time sensor fusion and AI capabilities. This involves technologies like the Snapdragon Digital Chassis by Qualcomm, the S32 by NXP Semiconductors, and NVIDIA Drive.

By Architecture: ARM-Based processors dominate, RISC-V grows fastest

ARM technology accounts for nearly 90% of Application Processors market share due to its higher energy efficiency, scalability, and ability to perform well in battery-powered devices. The ARM processor and Instruction Set Architecture (ISA) is licensed by Arm Holdings to be used by prominent companies like Apple, Qualcomm, Samsung, and MediaTek for various purposes including mobiles, tablets, wearable technology, and embedded systems. The new ARMv9 has many advantages with improved performance with respect to AI acceleration and new security features, which gives ARM processors greater competitiveness among other mobile processors as well as in edge computing environments. At the same time, ARM is now working on CPU development for server environments as well. RISC-V architecture has emerged recently as a promising option and gains popularity in the Internet of Things (IoT), embedded systems, and semiconductor ecosystems in China due to its licensing-free approach and flexibility of implementation in custom chips. Other architectures like MIPS and proprietary ISAs are mainly used in legacy embedded systems and AI accelerators.

By Process Node: 5nm–10nm nodes dominates, below 5nm (3nm, 2nm) grows fastest

Nodes under 5 nm form the most advanced part of the Application Processor Market that is dominated by companies such as TSMC and Samsung Electronics. For instance, Apple A17 Pro and M3 chipsets incorporate 3 nm technology provided by TSMC and deliver enhanced performance and power efficiency; in addition, 2 nm nodes are anticipated to increase transistor density and improve energy optimization starting from 2025-2026.

Nodes between 5 and 7 nm form the mainstream segment in terms of production and include processors with both low and high performances, as well as good cost efficiency. Qualcomm Snapdragon 8 chipset, Samsung Exynos, and MediaTek Dimensity processors are built on these technologies and are popular among smartphone manufacturers since they provide a good combination of performance and cost.

Application Processor Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

74% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

China |

50% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

49% |

Asia Pacific Application Processor Market Insights

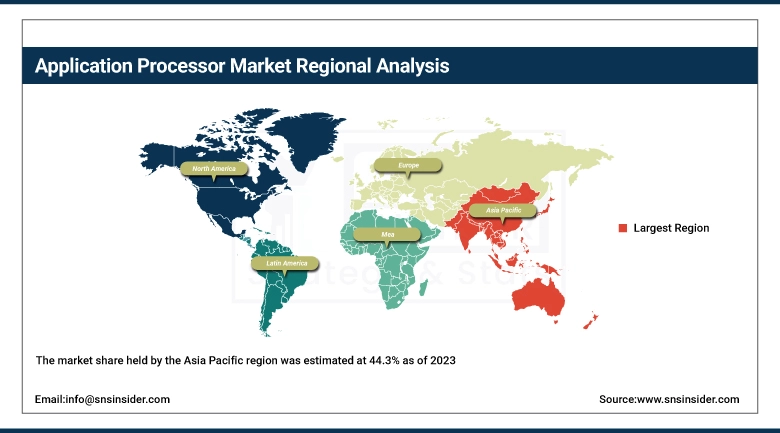

The market share held by the Asia Pacific region was estimated at 45.1% as of 2025. APAC will remain the dominant region throughout our forecast period till 2035. The main centers of manufacturing and consumption are located in Taiwan (TSMC), South Korea (Samsung), and China (MediaTek foundry, Qualcomm design for APAC). The huge and fast-growing market of consumer electronics in China, India, and Southeast Asia guarantees the continuous growth of demand. APAC is also projected to hold the fastest CAGR due to smartphone penetration in the developing markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Application Processor Market Insights

North America is the primary design hub for the global application processor market. Apple (Cupertino, CA), Qualcomm (San Diego, CA), and Intel (Santa Clara, CA) design the chips that dominate global device markets even though most manufacturing occurs in Asia. The CHIPS Act is funding new domestic manufacturing at Intel's Ohio and Arizona fabs and TSMC's Arizona fab, which will gradually build U.S. production capacity for advanced nodes.

Europe Application Processor Market Insights

Europe is a smaller consumer market for application processors but has important design centers for Arm Holdings (UK), NXP Semiconductors (Netherlands), and STMicroelectronics (France/Italy). European automotive OEMs are a major demand driver for automotive-grade application processors. The EU Chips Act is investing to build European semiconductor manufacturing capacity, particularly for automotive and industrial chips.

Middle East & Africa and Latin America Application Processor Market Insights

The Middle East is more of a consumer market for devices with application processors rather than a production center. However, countries like Saudi Arabia, the UAE, and Israel have been making investments in technologies that can incorporate chip design in the future. With its semiconductor engineering prowess (Intel's largest research and development center outside the United States), Israel is crucial in designing chips. African consumer electronics markets are relatively small but rapidly growing because of smartphone adoption.

In Latin America, the application processor market depends on the consumption of devices and not production. Brazil and Mexico are the biggest consumers of smartphones, tablets, and consumer electronics. In Latin America, there is high adoption of smartphones because of the mobile-first generation in the continent. Mexico's local electronics assembly for North American companies requires processor demand. There is increasing interest in IoT-specific chipsets for Brazil's emerging tech startups.

Market Growth Drivers: Smartphone proliferation and AI feature integration are the biggest market drivers

Over 1.2 billion smartphone shipments per year with application processors inside represent a substantial demand floor. Every new batch of smartphones needs a more advanced chip due to increased camera quality, AI functionality, 5G connectivity, and battery power efficiency. Incorporation of AI neural processing units (NPUs) as a standard feature of application processors is generating another level of competition and prompting more frequent replacements due to consumer demands for AI-enabled camera features and personal assistants.

Generative AI capabilities are emerging as an important component of smartphones, thus forming a whole new product lifecycle. With AI-powered photo editing, live translation, and even generation of new content by AI, smartphone companies are trying to persuade users to upgrade devices as quickly as possible in order to reverse the tendency of increasing replacement cycles seen in recent years.

Market Restraints: Market saturation in developed economies is slowing smartphone upgrade cycles

Consumers in developed nations such as the United States, Europe, and Japan have seen the replacement cycle of smartphones increase from two to three years to three to four years because the value of enhancements made from one model to the next has diminished. Consumers already have access to advanced smartphones to cater to their needs. Market saturation will act as a barrier for premium processors in developed nations, but emerging markets' growth will partly compensate for that.

Market Opportunities: Automotive processors and AI edge computing represent the highest-growth opportunities

The transition to software-defined vehicles is creating a new high-value market for automotive-grade application processors that could eventually rival the smartphone market in revenue. Every new EV platform and ADAS system requires orders of magnitude more processing power than previous generation vehicles, and this market is in its early innings. Edge AI inference, where devices process AI workloads locally rather than relying on cloud connectivity, is creating demand for processors with dedicated neural processing hardware in a wide range of device categories beyond smartphones.

Recent Developments:

-

2026: Rapid transition toward 2nm semiconductor manufacturing is underway, with TSMC and Samsung Electronics advancing Gate-All-Around (GAA) technology for next-generation application processors, expected to enter volume production in 2025–2026, significantly improving performance-per-watt efficiency and transistor density in the Application Processor Market.

-

2026: AI integration in application processors is accelerating, with companies such as Qualcomm, MediaTek, and NVIDIA embedding advanced NPUs and AI accelerators into SoCs to support on-device generative AI, real-time inference, and enhanced imaging workloads.

-

2026: The ARM ecosystem is expanding beyond smartphones as Arm Holdings strengthens its push into data center and PC-class processors, increasing competition with x86 architectures and enabling wider adoption of ARM-based AI PCs and servers.

Application Processor Companies are:

-

Qualcomm Technologies Inc

-

Apple Inc

-

Samsung Semiconductor

-

HiSilicon

-

NVIDIA Corporation

-

NXP Semiconductors

-

Intel Corporation

-

Texas Instruments Inc

-

Marvell Technology

-

Microchip Technology

-

STMicroelectronics

-

Advanced Micro Devices

-

Broadcom Inc

-

Rockchip Electronics Co. Ltd

-

Allwinner Technology Co. Ltd

-

Amlogic Inc

-

SiFive Inc

-

Unisoc

Application Processor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 40.79 Billion |

| Market Size by 2035 | USD 62.3 Billion |

| CAGR | CAGR of 4.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Core Type (Quad-Core, Octa-Core, Others) • By End-Use Device (Smartphones, Tablets, Smart Wearables, Automotive, Smart TVs, Industrial IoT, Others) • By Architecture (ARM-Based, x86-Based, RISC-V, Others) • By Process Node (Below 5nm, 5nm–10nm, Above 10nm) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Qualcomm Technologies Inc., Apple Inc., MediaTek Inc., Samsung Semiconductor, HiSilicon, NVIDIA Corporation, NXP Semiconductors, Intel Corporation, Texas Instruments Inc., Renesas Electronics, Marvell Technology, Microchip Technology, STMicroelectronics, Advanced Micro Devices, Broadcom Inc., Rockchip Electronics Co. Ltd., Allwinner Technology Co. Ltd., Amlogic Inc., SiFive Inc., Unisoc. |

Frequently Asked Questions

The Application Processor Market is expected to grow at a CAGR of 4.47% from 2026 to 2035.

The market was valued at USD 40.79 billion in 2025.

Octa-Core processors lead with 48.1% market share, dominating smartphones, tablets, and premium wearables.

Smart Wearables is the fastest-growing end-use device segment, followed closely by the Automotive segment.

Asia Pacific leads with 44.3% of global revenue, driven by TSMC's manufacturing leadership and the massive consumer electronics market.

Get in Touch