Fitness Tracker Market Report Scope & Overview:

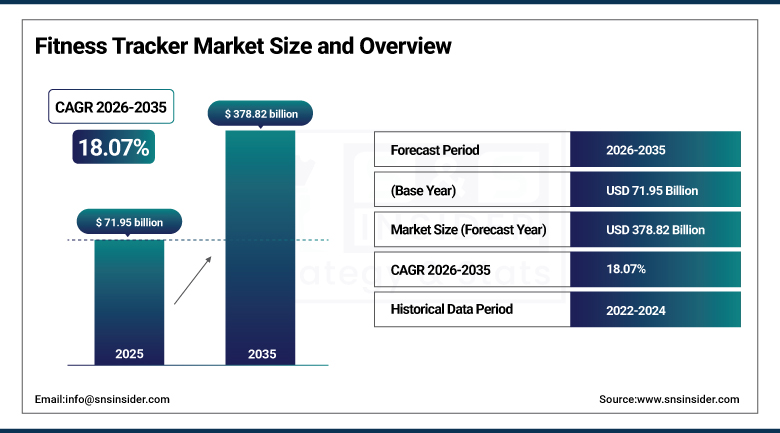

The Fitness Tracker Market was valued at USD 71.95 Billion in 2025 and is expected to reach USD 378.82 Billion by 2035, growing at a CAGR of 18.07% from 2026–2035.

Fitness trackers have moved well past their original role as simple step counters, and the pace of that evolution keeps accelerating. What started as basic activity monitors now routinely includes heart rate tracking, blood oxygen monitoring, sleep staging, and in the more advanced models, ECG functionality that used to require a visit to a cardiologist's office. Roughly 21% of Americans now use a smartwatch or fitness tracker, a meaningful adoption rate, though usage still lags noticeably among the groups who might benefit most, older adults and people managing chronic disease. Rising health consciousness, the growing prevalence of chronic conditions like diabetes and cardiovascular disease, and deepening integration between wearable devices and both AI analytics and the Internet of Things continue to push this market forward at a pace that's genuinely unusual for consumer electronics.

According to Heart.org data from 2020, fitness tracker adoption remains disproportionately low among high-risk groups, including elderly individuals and those managing chronic disease, precisely the populations that stand to gain the most from continuous health monitoring. The National Heart, Lung, and Blood Institute noted in 2023 that individuals with obesity or chronic disease continue to be underrepresented in fitness technology use, a gap that's increasingly framed as a target for public health intervention rather than simply a market inefficiency.

Market Size and Forecast

-

Market Size in 2026E: USD 84.95 Billion

-

Market Size by 2035: USD 378.82 Billion

-

CAGR: 18.07% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Fitness Tracker Market - Request Free Sample Report

Fitness Tracker Market Trends

-

Blood pressure and mental health monitoring capabilities are moving from research pilots into consumer-facing products, with both Apple and Samsung publicly signaling continued R&D investment in these areas throughout 2024.

-

Continuous glucose monitoring is emerging as one of the more closely watched frontiers in the category, with companies including Fitbit actively researching non-invasive blood sugar tracking as biosensor technology matures.

-

Regulatory clarity is slowly improving as programs like the FDA's Digital Health Software Precertification Program create clearer pathways for wearables that function closer to medical-grade devices than general wellness products.

-

Corporate wellness programs and insurer-backed activity incentives continue to expand the addressable market, effectively subsidizing device adoption for employees and policyholders who might not otherwise purchase one.

-

Interoperability between fitness tracking apps and electronic health records is improving steadily, giving clinicians a more complete picture of patient activity and physiological trends between office visits.

U.S. Fitness Tracker Market Outlook

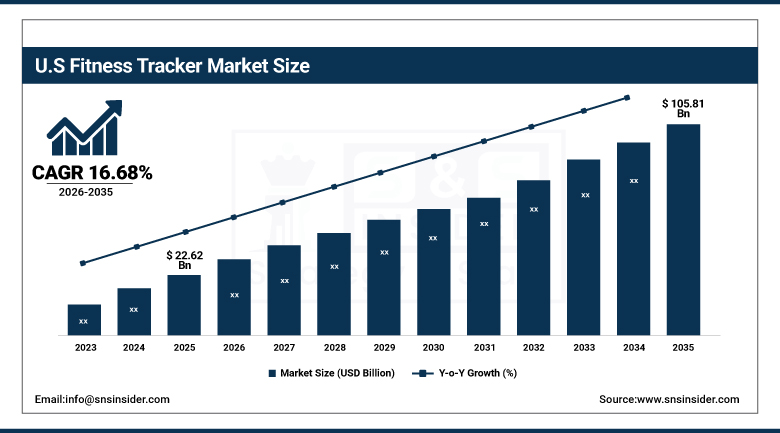

The U.S. Fitness Tracker Market was valued at approximately USD 22.62 Billion in 2025 and is expected to reach approximately USD 105.81 Billion by 2035, growing at a CAGR of approximately 16.68%.

The market within the U.S. is advantageous with regards to having a tech-savvy populace adopting new types of devices fast, considerable backing from FDA regulations in the form of their digital health programs concerning health monitors, and deepening integration of fitness monitor applications into clinical settings. According to NIH, about 30% of the adult population within America were using health trackers by 2023, a number which will only rise due to advancing capabilities in the devices and lowering of prices within affordable product segments. Fitness changes among consumers alongside government-led health drives continue to cement this trend, with the U.S. being the main R&D engine in the global fitness technology field.

In September 2024, WHOOP officially entered the Indian market, launching its advanced wearable fitness and health technology there for the first time. While the launch itself targeted India rather than the U.S. domestically, it reflects the kind of aggressive international expansion that American fitness technology companies are increasingly pursuing, extending the reach and brand recognition that fuels continued domestic investment and product development back home.

Fitness Tracker Market Segment Analysis

-

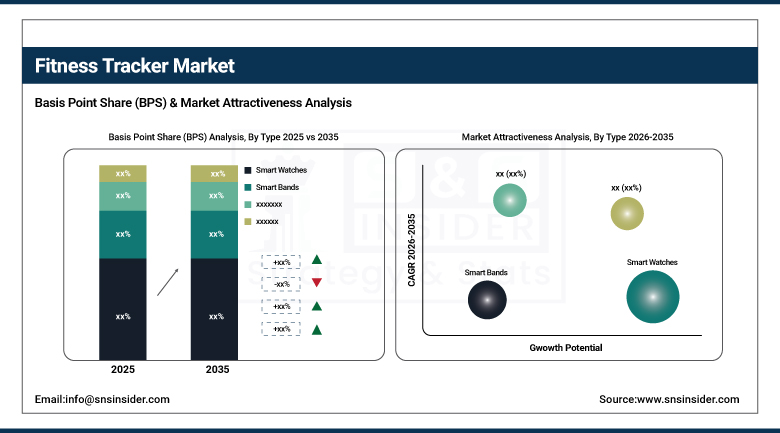

By Type, the Smart Watches segment dominated the Fitness Tracker Market with a 51.5% revenue share in 2025, while the Smart Bands segment is the fastest growing.

-

By Application, the Running Tracking segment dominated the Fitness Tracker Market with a 25.6% revenue share in 2025, while the Glucose Monitoring segment is the fastest growing.

-

By Wearing Type, the Handwear segment dominated the Fitness Tracker Market with a 76.2% revenue share in 2025, while the Legwear segment is the fastest growing.

-

By Distribution Channel, the Online segment dominated the Fitness Tracker Market with a 68.3% revenue share in 2025, while the Offline segment is expected to register the fastest growth in select markets.

By Type, smartwatches dominate, smart bands grow fastest

Smartwatch devices emerged as the top-selling product with a 51.5% market share in 2025 due to their wide array of features, integration with smartphones, ability to monitor ECG and SpO2 levels, as well as the presence of real-time notifications. The companies such as Apple, Garmin, and Samsung are still innovating the category with constant research and development and using AI technology, and their premium construction quality, as well as medical functionality, keeps on drawing customers from tech-savvy users and health-conscious individuals.

Smart bands were the fastest-growing product type due to their affordable price, light weight, and popularity with young consumers and first-time wearable users. Features such as step counting, heart rate monitoring, and sleep analytics can be purchased for significantly less than the full-fledged smartwatch devices, and due to rising healthcare consciousness in developing countries and growth of the e-commerce market penetration rates, this product type is growing very rapidly.

By Application, running tracking dominates, glucose monitoring grows fastest

Running tracking held the largest application share in 2025, at 25.6%, driven by the growing popularity of running clubs, marathons, and personalized training regimens, particularly among amateur athletes and urban professionals. Devices from Fitbit and Polar featuring integrated GPS, cadence sensors, and pace monitoring have become a standard part of many runners' training routines, and their ability to sync exercise data with companion fitness apps continues to enhance user engagement and sustain demand within this segment.

Glucose monitoring is the fastest-growing application, driven by rising diabetes incidence worldwide and growing interest in non-invasive blood glucose solutions that don't require finger pricks. Continued improvement in biosensor technology and device miniaturization is steadily opening a path for wearables to track blood sugar in real time, and as more medical-grade functionality gets built into consumer health wearables, this segment represents one of the more significant emerging growth opportunities in the category.

By Wearing Type, handwear dominates, legwear grows fastest

Handwear accounted for 76.2% of the market in 2025, the dominant wearing type, reflecting the success of wrist-worn fitness trackers that offer user convenience, clear screen visibility, and reliable sensor precision for heart rate monitoring, step tracking, and general activity tracking. Devices including the Apple Watch and Fitbit Charge have driven continuous advancement in this category through ongoing health monitoring, ECG functionality, and deeper app ecosystem integration, and their seamless everyday wearability continues to make them the recommended choice across a broad range of consumer segments.

Legwear is the fastest-growing wearing type, fueled by specialized athletic applications including gait analysis, cycling power measurement, and sport-specific performance feedback. Products from companies including Moov and Sensoria are gaining real traction among athletes and trainers seeking analytics that go beyond what traditional wrist-worn wearables can capture, reflecting a broader diversification in how consumers and professionals alike think about what a fitness tracker actually needs to measure.

By Distribution Channel, online dominates, offline grows in select markets

E-commerce was the dominant distribution channel at 68.3% of the market in 2025 owing to the increasing consumer preference for online channels, ease of comparison, rise of direct brand marketing by companies, and variety of products from around the world. Firms like Xiaomi, Fitbit, and Huawei have continued to rely on product launches through online channels, use of influencer marketing, and subscriptions in fitness platforms to expand their business, as well as product review sites and technology blogs to boost the confidence of consumers in their purchase of online wearable devices.

Offline retail is forecasted to witness robust demand in certain markets, especially in emerging economies and in older age groups who seek personal service and guidance. Offline retailers are partnering with retail partners, sports goods retailers, and medical product retailers to make products available in certain markets with developing consumer purchasing patterns.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

78.0% |

|

Europe |

Germany |

25.0% |

|

Asia Pacific |

China |

42.0% |

|

Latin America |

Brazil |

36.0% |

|

Middle East & Africa |

UAE |

28.0% |

North America Fitness Tracker Market Insights

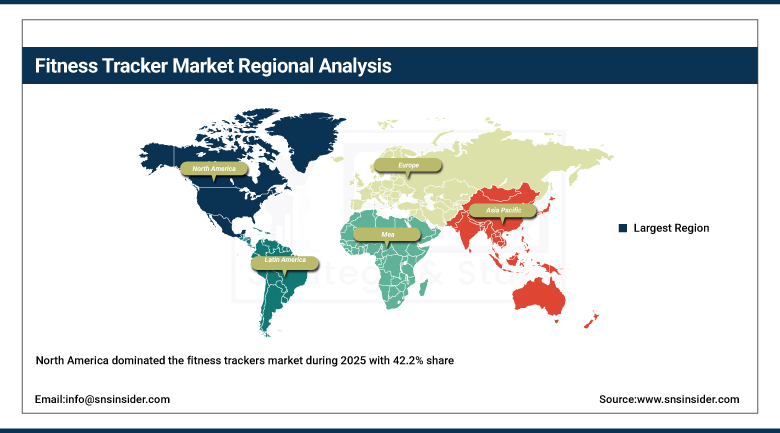

North America dominated the fitness trackers market during 2025 with 42.2% share because of its developed healthcare system, high consumer awareness, and prominent fitness trackers brand presence. Some of the key players are Apple, Fitbit, and Garmin. There is a high fitness tracker acceptance rate among health-conscious customers, athletes, and chronically ill individuals who are supervised by a doctor.

America is the key region within the region. It is driven by tech-savvy customers, FDA approval of health monitoring devices and their integration in clinical systems through the use of applications for tracking physical activity. According to the estimates of the National Institutes of Health, 30% of Americans already have some type of health-monitoring device.

Canada is characterized by a high fitness tracker adoption rate due to the implementation of government-sponsored wellness programs, and Mexico is experiencing market growth due to increased mobile phone penetration.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Fitness Tracker Market Insights

Asia Pacific is the leading growth region in the global fitness tracker market, fueled by rapid urbanization, rising disposable income, and a genuine boom in affordably priced smart bands and activity trackers. China dominates the region on the strength of its enormous consumer base, both local and international fitness tracker brands including Huawei and Xiaomi, and sustained government support for digital health initiatives, with more than 250 million Chinese consumers reportedly using fitness wearables as of 2023.

India is experiencing exponential growth as well, driven by rising health awareness and expanding smartphone penetration across tier-2 and tier-3 cities. The country's youth-oriented population and rapidly growing fitness app download numbers continue to meaningfully shape broader market trends across the region, positioning Asia Pacific as the growth engine most likely to define this market's next decade.

Europe Fitness Tracker Market Insights

Europe ranks second in the sales of fitness bands driven by awareness about preventative medicine, increased penetration of digital health solutions, and wellness programs initiated by governments in the major economies of Europe. Germany leads the European region owing to its sound economic performance, growing fitness culture, and popularity of smart fitness bands among consumers and for therapeutic use, with the German Federal Health Ministry promoting continuous health monitoring solutions on digital health platforms.

United Kingdom enjoys a good share of regional revenue due to the initiatives by the NHS promoting digital health adoption and sports and fitness gadgets among young people. France and Italy are other regions witnessing an increase in adoption owing to growing smartphone adoption and sports activities in both regions.

MEA & Latin America Fitness Tracker Market Insights

Latin America is seeing steady fitness tracker adoption, driven by rising health awareness, growing smartphone penetration, and expanding e-commerce infrastructure that's making global wearable brands more accessible across the region. Brazil leads regional demand, with Argentina and other markets contributing meaningful, if smaller, growth as digital literacy and disposable income continue rising across the region.

The Middle East and Africa region is experiencing similarly steady growth, driven by increasing health consciousness and government initiatives supporting digital health infrastructure across the Gulf states. The UAE leads regional adoption, supported by strong purchasing power and a young, tech-oriented population, while South Africa continues to anchor demand across the broader African market.

Market Dynamics

Growth Drivers: Technological advancement and preventive healthcare adoption fuel demand

Fitness tracker market growth can be attributed to the increasing pace of technological innovations, demand for preventive care solutions, and increased use of wearable devices for fitness tracking. The shift from reactive to proactive healthcare will continue to increase demand for health wearables such as smart fitness bands and heart rate monitors, with companies like Garmin and WHOOP having added the ability to monitor blood oxygen level, track recovery process and use artificial intelligence-based analytics specifically to help boost customer engagement and improve health results.

Approval by FDA of ECG smartwatches within its digital health program has substantially helped to boost innovation within the entire fitness technology industry, while R&D spending on intelligent fitness monitors globally is constantly growing, as Fitbit, Apple, and Huawei are making considerable investments in biometric sensing capacity. At the same time, demand for fitness trackers will also increase due to corporate wellness programs and incentives offered by insurance companies related to the active lifestyle tracking.

Restraints: Data privacy concerns and engagement fatigue limit sustained adoption

A 2023 JMIR study found that more than 35% of American wearable device users expressed concern about their health data being misused by third parties, including companies and insurers, a genuine trust gap that continues to shape purchasing decisions across the category. Inconsistent data governance frameworks around fitness wearable data exchange and protection continue to complicate this picture, and inconsistent user engagement or technology fatigue leads to meaningful disengagement over time, with roughly 30% of fitness tracking app users abandoning use within six months due to unmet expectations, data anomalies, or limited user experience design.

The absence of consistent global regulation adds a further layer of complexity. While the FDA has developed regulations for medical-grade devices, most consumer fitness trackers fall into wellness categories that create real regulatory ambiguity. Limited market penetration among disadvantaged populations and older demographics, driven by disparities in digital literacy and resources, along with ongoing semiconductor component shortages and rising component costs, continue to affect production schedules and constrain availability and scalability decisions across the industry.

Opportunities: Medical-grade functionality and emerging market expansion unlock substantial growth

"The steady evolution of fitness trackers from wellness-focused technology towards more clinically-oriented solutions such as blood pressure measurements, psychological monitoring, and even non-invasive glucose measurement are among the fields that both Apple and Samsung have promised to develop in 2024," constitutes a promising opportunity for businesses capable of making the leap towards becoming leaders in this field. As various regulatory processes, such as FDA's Digital Health Software Precertification Program, continue developing, businesses capable of delivering both consumer-grade and clinical-grade monitoring are likely to achieve premium pricing and deep integration into the healthcare system.

"Entry into demographics where adoption of the product is currently lagging behind," constitute another major opportunity, especially considering that fitness trackers' adoption among those who would benefit the most from their use, i.e., older patients and patients with chronic diseases, is currently rather low. While the costs of the devices continue decreasing, and awareness campaigns for these categories of users continue developing, along with the development of specialized markets, such as animal fitness trackers, businesses willing to develop products specifically for underserved categories of users have a lot to gain.

Recent Developments:

-

2023: In September 2023, Fitbit launched the Charge 6, combining advanced Google features including Maps and Wallet, improved heart rate monitoring, and seamless compatibility with various gym equipment.

-

2024: In September 2024, WHOOP officially entered the Indian market, launching its advanced wearable fitness and health technology with real-time insights into recovery, strain, stress, and sleep metrics.

-

2024: Throughout 2024, Apple and Samsung both reported continued research and development progress on advanced fitness tracker capabilities, including blood pressure measurement and mental health monitoring features.

Fitness Tracker Market Key Players

-

Apple Inc.

-

Google (Fitbit, Inc.)

-

Garmin Ltd.

-

Samsung Electronics

-

Huawei Technologies Co., Ltd.

-

Fossil Group, Inc.

-

Xiaomi Corporation

-

Amazfit (Zepp Health)

-

Polar Electro Oy

-

HYPE

-

WHOOP, Inc.

-

Suunto Oy

-

Withings SA

-

Coros Wearables Inc.

-

Oura Health Oy

-

Moov Inc.

-

Sensoria Inc.

-

Under Armour, Inc.

-

Nike, Inc.

-

Lenovo Group Limited

Fitness Tracker Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 71.95 Billion |

| Market Size by 2035 | USD 378.82 Billion |

| CAGR | CAGR of 18.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Smart Watches, Smart Bands, Smart Clothing, Others) • by Application (Heart Rate Tracking, Sleep Monitoring, Glucose Monitoring, Sports, Running Tracking, Cycling Tracking, Others) • by Wearing Type (Handwear, Legwear, Others) • by Distribution Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Apple Inc., Google (Fitbit, Inc.), Garmin Ltd., Samsung Electronics, Huawei Technologies Co., Ltd., Fossil Group, Inc., Xiaomi Corporation, Amazfit (Zepp Health), Polar Electro Oy HYPE, WHOOP, Inc., Suunto Oy, Withings SA, Coros Wearables Inc., Oura Health Oy, Moov Inc., Sensoria Inc., Under Armour, Inc., Nike, Inc., Lenovo Group Limited |

Frequently Asked Questions

North America dominated the Fitness Tracker Market in 2025 with a 42.2% market share, while Asia Pacific is the fastest-growing region.

The Fitness Tracker Market is expected to grow at a CAGR of 18.07% from 2026 to 2035.

The Fitness Tracker Market was valued at USD 71.95 Billion in 2025.

Technological innovation combined with growing demand for preventive healthcare solutions and rising adoption of wearable devices for personal health management.

Smart Watches dominated with a 51.5% revenue share in 2025, while Smart Bands is the fastest growing segment.

Get in Touch