Artificial Spine Discs Market Report Scope & Overview:

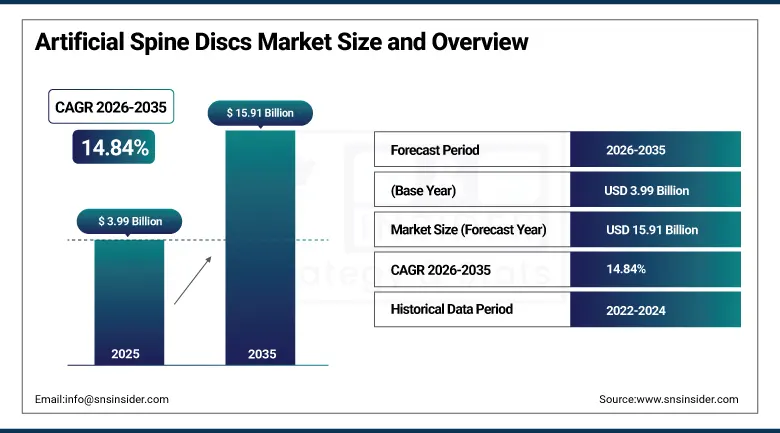

The Artificial Spine Discs Market was valued at USD 3.99 Billion in 2025 and is projected to reach USD 15.91 Billion by 2035, expanding at a CAGR of 14.84% during the forecast period 2026–2035.

The global artificial spine discs market is growing substantially driven by the rising incidence of degenerative spinal disorders, increasing preference for motion-preserving spinal procedures, and ongoing advancements in biomaterial engineering technologies. With improved mobility outcomes, less risk of adjacent segment degeneration and fast patient recovery, healthcare providers are increasingly opting for artificial disc replacement procedures as an alternative to spinal fusion. Increasing investments in minimally invasive spine surgery infrastructure, robotic-assisted surgical systems, advanced imaging platforms and next generation implant technologies continue to drive market growth across developed and emerging healthcare markets.

In 2025-2026, a few medical device manufacturers improved commercialization of advanced cervical and lumbar artificial disc systems that incorporated enhanced biomaterials, anatomical designs and long-term motion preservation capabilities.

Market Size and Forecast

-

Market Size 2026E: USD 4.58 Billion

-

Market Size 2035: USD 15.91 Billion

-

CAGR: 14.84% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Artificial Spine Discs Market - Request Free Sample Report

Artificial Spine Discs Market Trends

-

Growing adoption of motion-preserving spinal implant technologies.

-

Increasing utilization of titanium and advanced biomaterial disc replacement systems.

-

Rising deployment of robotic-assisted and navigation-guided spine surgeries.

-

Expansion of minimally invasive spinal reconstruction procedures.

-

Growing integration of smart hospital infrastructure, UDI compliance systems, and implant tracking technologies.

The U.S. Artificial Spine Discs Market Size Outlook

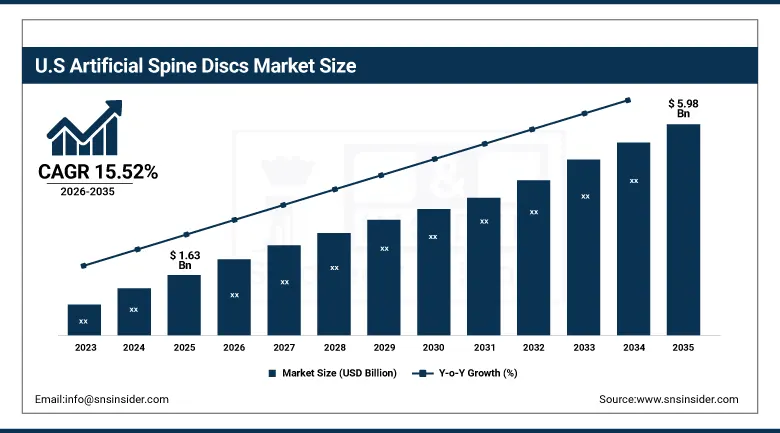

The U.S. Artificial Spine Discs Market was valued at USD 1.63 billion in 2025 and is expected to reach approximately USD 5.98 billion by 2035, expanding at a CAGR of 15.52% during 2026–2035.

The US dominates the artificial spine discs market owing to high adoption of advanced spinal surgery technologies, favorable reimbursement scenario, increasing prevalence of degenerative disc disorders and strong orthopedic care infrastructure. Hospitals and specialized spine centers are investing in advanced surgical navigation systems, robotic-assisted platforms, and next-generation artificial disc implants to improve procedural outcomes, shorten recovery times and boost patient mobility. The demand nationwide is also being driven by an increasing preference for motion-preserving procedures among active patient populations. The market leadership is still aided by the presence of leading spinal implant manufacturers, highly skilled orthopedic surgeons and well-established spine care facilities.

During 2025-2026, several U.S.-based spinal implant manufacturers accelerated clinical adoption initiatives and launched new artificial disc systems aimed at improving long-term biomechanical performance and patient outcomes.

Artificial Spine Discs Market Segment Analysis

-

By Material Type, titanium dominated the market with 31.00% share in 2025, while Ceramic is projected to witness the fastest growth with a 17.43% CAGR during the forecast period.

-

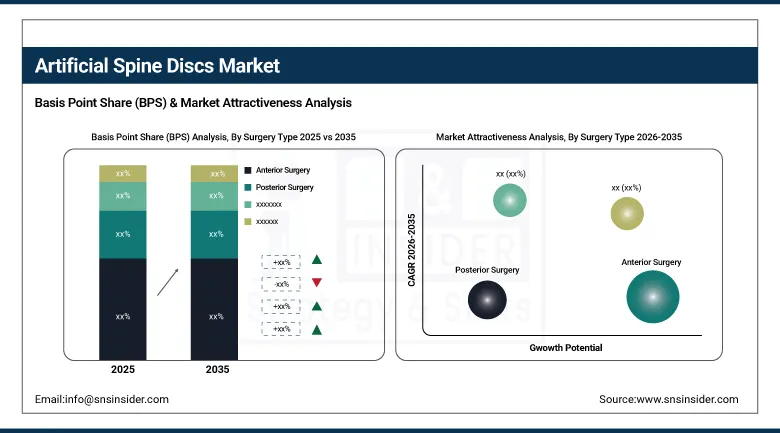

By Surgery Type, anterior surgery dominated the market with 71.00% share in 2025, while lateral Surgery is projected to witness the fastest growth with a 16.91% CAGR during the forecast period.

-

By Application, degenerative disc disease dominated the market with 52.00% share in 2025, while spinal stenosis is projected to witness the fastest growth with a 16.05% CAGR during the forecast period.

-

By End User, hospitals dominated the market with 63.00% share in 2025, while ambulatory surgical centers are projected to witness the fastest growth with a 17.76% CAGR during the forecast period.

By Surgery Type, anterior surgery dominated, while lateral surgery is fastest-growing.

The anterior surgery segment held the largest market share of 71.00% in 2025 owing to its widespread use in cervical and lumbar artificial disc replacement procedures. With the help of advanced navigation systems and intraoperative imaging technologies, surgeons are increasingly using anterior techniques to improve the efficiency of the procedure and the recovery of the patient. Many spine specialists still prefer this technique as a surgical approach because it allows for the best visualization of the affected disc space with the least disruption of posterior spinal structures.

The segment is expected to grow at the highest CAGR of 16.91% during the forecast period. The high growth of the lateral surgery segment is due to the rising adoption of minimally invasive spinal procedures. Lateral approaches permit less tissue dissection, shorter hospitalization and better postoperative recovery. Lateral access techniques are being adopted by spine surgeons around the world due to a growing emphasis on minimizing surgical trauma and improving patient recovery. Healthcare providers are progressively adopting advanced imaging guidance systems, robotic-assisted technologies, and minimally invasive surgical platforms in support of procedural precision and optimization of patient outcomes.

By Application, degenerative disc disease dominated, while spinal stenosis is fastest-growing.

In 2025, the degenerative disc disease segment contributed the largest share of revenue, accounting for 52.00% of the market, driven by the rising incidence of age-related spinal degeneration across the globe. Artificial disc replacement surgeries are being increasingly performed to avoid fusion surgeries and preserve spinal mobility. Strong procedural volumes across healthcare systems continue to be supported by rising ageing populations and increasing incidence of chronic spinal disorders. Degenerative disc disease continues to be a leading cause of chronic back and neck pain, underscoring a substantial unmet need for effective, long-term, and spine-preserving treatments. More and more healthcare providers are recommending artificial disc implants to suitable patients who want alternatives to traditional spinal fusion surgeries.

Spinal stenosis segment is expected to register the fastest CAGR of 16.05% during the forecast period. Growth of spinal stenosis segment is mainly due to increasing diagnosis rates, improved patient awareness and expanding access to advanced spinal care. Motion-preserving technologies are increasingly considered in the healthcare setting for selected stenosis patients. The increasing prevalence of spinal stenosis in the geriatric population and the increasing demand for minimally invasive treatment options are providing positive growth potential to artificial disc technologies in the patient population. Enhanced diagnostic imaging, early disease detection and specialized services for spine care are enabling healthcare providers to better identify suitable candidates for advanced surgical interventions.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

93.00% |

|

Europe |

Germany |

29.00% |

|

Asia Pacific |

China |

20.00% |

|

Middle East & Africa |

UAE |

4.00% |

|

Latin America |

Brazil |

3.00% |

North America Artificial Spine Discs Market Insights

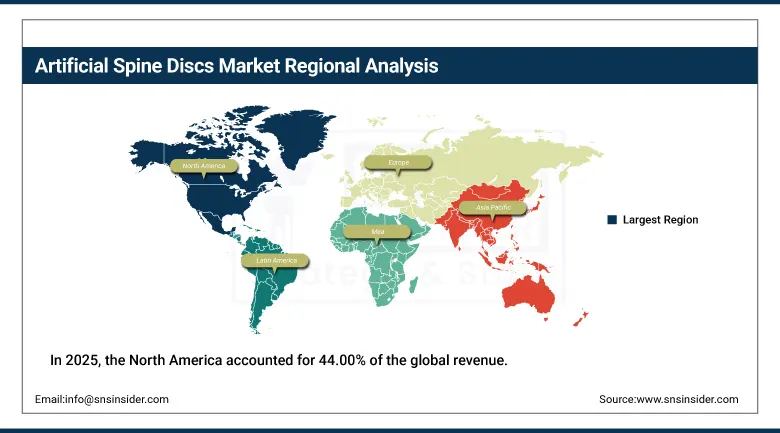

In 2025, the North America accounted for 44.00% of the global revenue. Market growth is supported by the presence of advanced orthopedic care infrastructure, high adoption of motion preservation spinal procedures, conducive reimbursement systems, and prevalent availability of robotic-assisted surgical technologies. “Healthcare providers continue to invest in next-gen spinal implant platforms and minimally invasive surgery capabilities. Further regional leadership is supported by growing procedural volumes for degenerative spinal disorders. The region has a well-developed network of specialized spine centers, experienced orthopedic surgeons, and a high level of patient awareness about advanced spinal treatment options.

In 2025-2026, some of the largest healthcare institutions in North America began to ramp up the use of advanced cervical and lumbar disc replacement systems integrated with navigation assisted surgical workflows.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Artificial Spine Discs Market Insights

Europe accounted for approximately 29.00 % of the overall global market in 2025. Increasing adoption of advanced spinal implants, expanding orthopedic surgical capacity, and rising demand for motion-preserving treatment options in Germany, France, the U.K., Italy and other major healthcare markets are driving growth. The healthcare systems are increasingly adopting advanced technological solutions in spinal reconstruction. The region is seeing procedural growth being supported by the presence of well-developed healthcare infrastructure, favorable clinical guidelines and growing access to specialized orthopedic care. Surgeons are increasingly utilizing advanced disc replacement technologies, minimally invasive surgical techniques and better imaging systems to improve treatment precision and speed up patient recovery.

A number of European health care providers have stepped up their investments in minimally invasive spine surgery programs and advanced disc replacement technologies in 2025-2026.

Asia Pacific Artificial Spine Discs Market Insights

The Asia Pacific region is expected to witness the highest CAGR of 17.89% during the forecast period due to increasing healthcare expenditure, increasing volumes of orthopedic procedures, expansion of medical infrastructure, and rising awareness about advanced spinal treatment options. Countries such as China, India, Japan, South Korea and Australia continue to invest heavily in the orthopedic and spinal care modernization programs. Rising number of specialized spine surgery centers also supports market growth. The region is experiencing a strong demand for advanced spinal treatment solutions, driven by rapid urbanization, ageing populations and increasing incidence of degenerative spinal conditions.

Several healthcare organizations in the Asia Pacific region adopted advanced spinal implant technologies and minimally invasive disc replacement procedures during 2025 – 2026.

Middle East & Africa and Latin America Artificial Spine Discs Market Insights

The Middle East & Africa market is experiencing steady growth due to the modernization of healthcare infrastructure, the growing capacity of orthopedic procedures, and the growing access to advanced surgical technologies. To improve treatment results, governments and healthcare providers are investing in specialized orthopedic care facilities and advanced implant technologies. Increasing awareness towards spinal health, increasing availability of skilled orthopedic specialists and rising healthcare expenditure are supporting the market growth in key regional countries.

Latin America accounted for a share of approximately 4.00% of the market in 2025 due to the increase in healthcare investments, improved access to specialized spinal care, and the growing awareness of artificial disc replacement procedures. The building out of private healthcare infrastructure and orthopedic specialty centers continues to underpin long term market development. Rising adoption of advanced spinal implants, rising diagnostic capabilities, and rising demand for motion-preserving surgical solutions are further boosting the regional growth. Furthermore, the healthcare modernization initiatives and investments in the orthopedic treatment technologies are still creating lucrative opportunities across both the regions.

Market Dynamics

Growth Drivers: Increasing prevalence of degenerative spinal disorders and growing preference for motion-preserving procedures.

Key drivers of demand for artificial spine discs across the world include increasing rates of degenerative disc disease, spinal stenosis and age-related spinal disorders. The adoption of disc replacement technologies as an alternative to spinal fusion to maintain natural spinal motion and to improve long-term clinical outcomes is increasing among healthcare providers. Developments in biomaterials, implant design, and surgical navigation technologies are further improving procedural success rates and broadening patient eligibility. The increasing ageing populations, sedentary lifestyles and rising prevalence of chronic musculoskeletal conditions are driving demand for effective spinal treatment solutions across healthcare systems.

Through 2025-2026, manufacturers expanded commercialization of advanced artificial disc systems that offer improved wear resistance, anatomical compatibility and long-term mobility preservation.

Restraints: High procedural costs and rigid regulatory requirements.

Despite strong growth potential, increased treatment costs, complex regulatory approval pathways and limited reimbursement coverage in some markets continue to limit wider adoption. The complexity of surgical techniques, sophisticated imaging infrastructure and premium implant technologies involved in artificial disc replacement procedures adds to the overall cost of healthcare. Longer commercialization timelines are also a result of long-term clinical validation requirements. Healthcare providers need to make substantial investments in advanced surgical navigation systems, robotic-assisted technologies, and surgeon training programs in order to successfully implement artificial disc procedures. Moreover, next generation spinal implants pricing may limit patient access for cost-sensitive healthcare markets.

In 2026, regulatory agencies continued to emphasize the need for post-market surveillance, UDI compliance, and long-term monitoring of clinical performance of spinal implant systems.

Opportunities: Technological advances in biomaterials and minimally invasive spinal surgery.

There is much room for further innovation in biomaterials, personalized design of implants, robotic assisted surgery, and minimally invasive spinal procedures. Medical providers are investing more money into high-tech surgical platforms that can make surgeries more precise and speed recovery. Further market expansion is supported by growing integration of digital surgical planning, implant tracking systems, and smart hospital infrastructure. Manufacturers are working on next-generation artificial discs using advanced polymers, metal alloys and bioengineered materials to target durability, biomechanical performance and compatibility with the patient’s anatomy. Robotic-assisted spine surgery and computer-assisted navigation technologies are being increasingly used to improve the accuracy of implant placement and variability in surgery.

In 2025–2026, multiple medical device companies released next-generation spinal implant technologies with superior biomechanical performance and enhanced long-term durability.

Recent Developments

-

2026: Multiple spinal implant manufacturers expanded commercialization of next-generation cervical artificial disc systems with enhanced motion-preservation capabilities.

-

2026: Hospitals increased adoption of robotic-assisted spinal surgery platforms supporting improved implant placement accuracy.

-

2025: Medical device companies introduced advanced titanium-based artificial disc designs focused on long-term durability and biocompatibility.

-

2025: Healthcare providers expanded minimally invasive spinal surgery programs utilizing advanced navigation and imaging technologies.

Artificial Spine Discs Market Key Players are:

-

Medtronic plc

-

Johnson & Johnson (DePuy Synthes)

-

Zimmer Biomet Holdings Inc.

-

Globus Medical Inc.

-

NuVasive Inc.

-

Orthofix Medical Inc.

-

RTI Surgical Holdings Inc.

-

B. Braun SE

-

Centinel Spine LLC

-

Spineart SA

-

Aesculap Implant Systems LLC

-

AxioMed LLC

-

Simplify Medical Inc.

-

FH Orthopedics

-

Synergy Disc Replacement Inc.

-

Aurora Spine Corporation

-

Spinal Kinetics Inc.

-

SeaSpine Holdings Corporation

-

Stryker Corporation

-

Alphatec Holdings Inc

Artificial Spine Discs Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.99 Billion |

| Market Size by 2035 | USD 15.91 Billion |

| CAGR | CAGR of 14.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Polyethylene, Titanium, Cobalt Chrome, Ceramic, Composite) • By Surgery Type (Anterior Surgery, Posterior Surgery, Lateral Surgery) • By Application (Degenerative Disc Disease, Spinal Stenosis, Trauma, Herniated Discs) • By End User (Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic plc, Johnson & Johnson (DePuy Synthes), Zimmer Biomet Holdings Inc., Globus Medical Inc., NuVasive Inc., Orthofix Medical Inc., RTI Surgical Holdings Inc., B. Braun SE, Centinel Spine LLC, Spineart SA, Aesculap Implant Systems LLC, AxioMed LLC, Simplify Medical Inc., FH Orthopedics, Synergy Disc Replacement Inc., Aurora Spine Corporation, Spinal Kinetics Inc., SeaSpine Holdings Corporation, Stryker Corporation, Alphatec Holdings Inc. |

Frequently Asked Questions

North America dominated the global market owing to advanced spinal care infrastructure and high adoption of motion-preserving spinal implant technologies.

The market is projected to reach USD 15.91 billion by 2035.

The market is expected to expand at a CAGR of 14.84% during the forecast period.

The Artificial Spine Discs Market was valued at USD 3.99 billion in 2025.

Titanium accounted for the largest revenue share of 31.00% in 2025.

Get in Touch