Artificial Ventilation and Anesthesia Masks Market Report Scope & Overview:

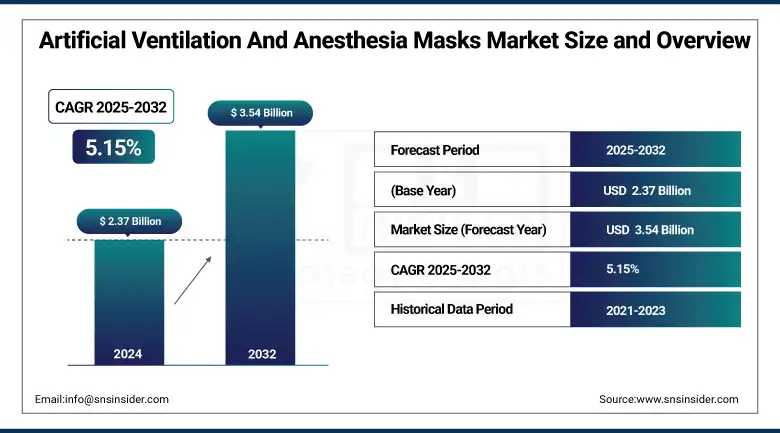

The artificial ventilation and anesthesia masks market size was valued at USD 2.37 billion in 2024 and is expected to reach USD 3.54 billion by 2032, growing at a CAGR of 5.15% over 2025-2032.

The artificial ventilation and anesthesia masks market is experiencing high demand in the surgical procedures for the chronic respiratory diseases industry. The WHO reported in 2023 that globally, 262 million people suffered from COPD, and that COPD was expected to persist as a leading cause of death globally. Over 300 million people globally are affected by asthma, further paving the way for ventilation solutions. Surgeries are booming, with the OECD projecting that surgery volumes will increase, on average, by 3.2% per year in developed countries. Meanwhile, the need for anesthesia masks during perioperative care has increased. On the supply side, companies that are also producing masks include Medtronic and Ambu A/S, which are ramping up production lines and introducing the next-gen masks featuring improved seal integrity and biocompatible materials. In 2024, healthcare infrastructure spending in the developing regions, such as Asia-Pacific, amounted to over USD 14 billion, contributing to a growth in ICU bed capacities at a rate of 5.8% YoY and encouraging the procurement of critical care equipment.

To Get more information On Artificial Ventilation And Anesthesia Masks Market - Request Free Sample Report

Regulatory agencies such as the US FDA issued numerous EUAs (Emergency Use Applications) for portable ventilators and associated airway management equipment in 2023–2024. The global respiratory devices exceeded USD 2.3 billion in 2024, and companies such as Philips Respironics and GE Healthcare are heavily funding the development of AI-based ventilation mechanisms, like automated oxygen titration. Moreover, favorable reimbursement scenarios in countries such as Germany, the U.S., and Japan for procedures such as mechanical ventilation and procedures related to anesthesia are reinforcing the hospital procurement trend, thereby increasing the global artificial ventilation and anesthesia masks market share.

In Aug 2024, CE Mark clearance was awarded to Ambu A/S for its next-gen single-use anesthesia mask, integrated with antimicrobial polymer coatings, in favour of infection control requirements, which have to be fulfilled in high-volume surgical centers in Europe.

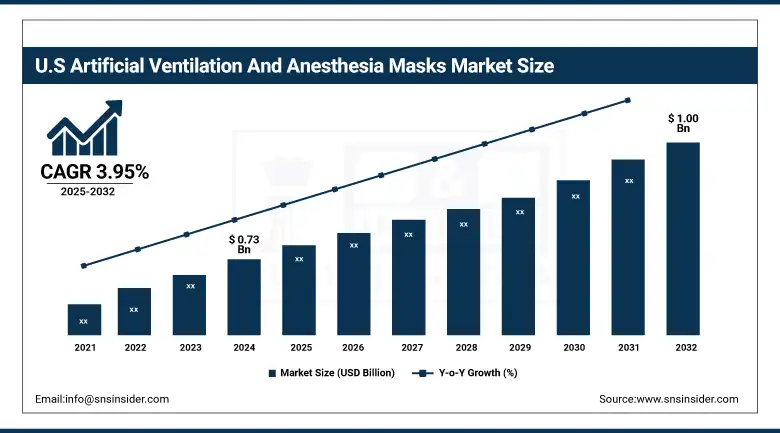

The U.S. artificial ventilation and anesthesia masks market size was valued at USD 0.73 billion in 2024 and is expected to reach USD 1.00 billion by 2032, growing at a CAGR of 3.95% over 2025-2032. The U.S. is the largest market in the region and is propelled by a high incidence of chronic respiratory diseases, around 25 million Americans have been diagnosed with asthma alone, coupled with growing numbers of surgeries. Supply-side strength has also been supported by government actions, such as BARDA investments to develop a respiratory device. There is also increasing use in Canada, specifically in tertiary care hospitals, with an emphasis on infection prevention. Mexico is developing with increased public health investment, particularly in urban hospitals. The area remains active with innovation pipelines as well, with U.S.-based companies such as Medtronic and GE Healthcare unveiling both new ventilators powered by AI and improved systems for anesthesia masks, and effectively establishing a position both in domestic and international markets.

Table: AI Integration in Artificial Ventilation and Anesthesia Masks Market (2023–2025)

|

Company |

AI-Enabled Feature |

Device/System |

Functionality |

Impact Area |

|

Philips |

AI-based oxygen titration algorithm |

Trilogy EV300 |

Auto-adjusts oxygen flow to patient needs using predictive analytics |

ICU & home ventilation |

|

Hamilton Medical |

Real-time patient breath synchronization |

IntelliSync+ Ventilation Mode |

AI anticipates patient breathing effort and synchronizes ventilator cycles. |

Mechanical ventilation accuracy |

|

Nihon Kohden |

Automated anesthesia depth control |

Prototype AI anesthesia system (2023) |

Controls anesthesia delivery based on vitals and predicted patient response |

Operating rooms & surgical procedures |

|

Drägerwerk AG |

Smart ventilation with decision support |

Evita Infinity V500 |

AI-driven algorithms support clinical decision-making for ventilation management. |

Emergency & critical care |

|

GE Healthcare |

AI for predictive ventilator maintenance |

Carestation Insights Platform |

Predicts component wear/failure using machine learning |

Hospital asset management & uptime |

|

ResMed |

Sleep data & respiratory pattern recognition |

AirSense 11 (adapted for hospital use) |

Tracks patient patterns for therapy adjustment |

Long-term ventilation & homecare |

|

Ambu A/S |

AI-enhanced visual analytics for airway navigation |

aScope 5 Cysto (2025 FDA-approved) |

AI supports navigation and monitoring during mask-guided endoscopy |

Procedural safety & diagnostics |

Market Dynamics:

Drivers:

-

Rising Respiratory Disease Burden, Technological Advancements, and Critical Care Expansion Fuel Market Growth

The increasing prevalence of respiratory support, advanced surgical care, and next-generation medical technologies is driving the artificial ventilation and anesthesia masks market growth. A rise in chronic and acute pulmonary diseases (amplified by long-COVID patients and increasing cases of respiratory distress syndromes) has led to demand for non-invasive ventilation and airway management devices.

From a 2024 Global Initiative for Chronic Obstructive Lung Disease report, respiratory diseases are now responsible for >7% of healthcare admissions globally, illustrating the clinical need. Accordingly, artificial ventilation and anesthetic guidance masks market players such as Teleflex, ResMed, and Smiths Medical are introducing masks that feature adjustable airflow and antimicrobial drive.

R&D spending was on the high side of USD 2.6 billion in 2024 for respiratory devices, thus heavily accelerating the artificial ventilation and anesthesia masks market size. Recent regulatory assistance in the form of the FDA’s Breakthrough Devices Designation has led to approvals for automated ventilators and ergonomically designed anesthesia masks, among others. An investment boom in surgical infrastructure and critical care units (especially in private hospitals and in specialized surgical centres) is building on the demand. These trends are creating a positive artificial ventilation and anesthesia masks market analysis, with continued innovation and uptake in both hospital and ambulatory settings in the global artificial ventilation and anesthesia masks market trends.

Restraints:

-

Cost Sensitivity, Limited Access in LMICs, and Regulatory Complexity Hinder Market Expansion

A major drawback is the cost-sensitive environment of the developing countries and under-equipped medical facilities. For instance, disposable anesthesia masks, which reduce the risk of infection, cost between 30 and 40% more than traditional reusable masks and have limited uptake in price-sensitive settings. Furthermore, the penetration rate of ventilators in low and middle-income countries is still insufficient at less than 2 units per 100,000 population based on the report of the World Bank (2024).

Supply chain inefficiencies, local factories that are unable to make all the parts, reliance on imports, even of essential components like pressure valves and medical-grade silicone, still hamper delivery and availability. In addition, regulatory compliance continues to create challenges for the artificial ventilation and anesthesia masks market, especially under the new regulatory acts such as the EU MDR and the standards of ISO 80601.

Product certification delays and piecemeal approval paths affect new firms’ time-to-market. Such constraints are deterring the growth of the artificial ventilation and anesthesia masks market, despite increasing demand. Inequalities in the insurance coverage of anesthetic drugs and supplies between countries also limit the adoption thereof. Together, these challenges are generating drag on the growth of the artificial ventilation and anesthesia masks market share, particularly across decentralized and rural facilities. However, policy reform and supply-side innovation may reduce such constraints down the road.

Segmentation Analysis:

By Mask

In 2024, the disposable masks segment contributed the highest revenue share of 71.03% to the global artificial ventilation and anesthesia masks market, as these are widely used in hospitals with the installation of infection control protocols. These types of masks are easy to use, have a lower cross-infection risk, and meet the stringent levels of cleanliness required in surgical and ICU practice. The growing trend toward disposable, one-time-use equipment, particularly in a post-COVID world, helped cement their grip on high-throughput clinical environments.

On the other hand, reusable masks are appearing as the fastest-growing category as they are more cost-effective over time, and also sustainable. Healthcare facilities seeking to decrease waste and manage procurement costs are transitioning to reusables, particularly for low-risk procedures or non-acute settings. Advancements in autoclavable materials and increased durability are also driving the use of reusable masks in both public and private hospitals.

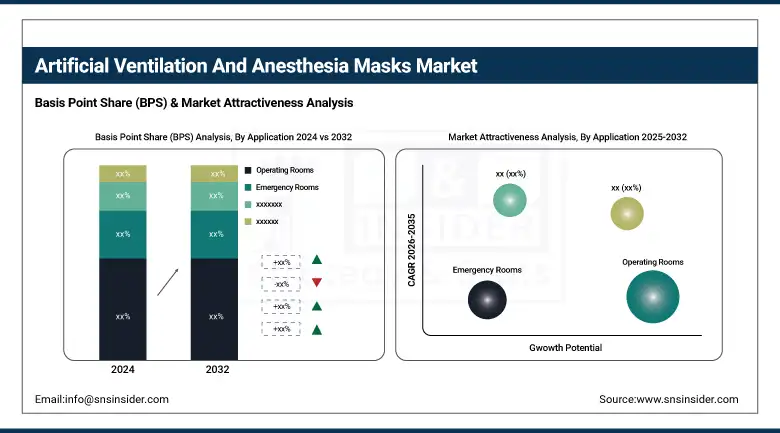

By Application

Operating rooms were the largest application in 2024, accounting for a market share of 38.02% as a result of the increasing number of surgeries that need accurate and consistent administration of anesthesia. Strict regulations regarding patient safety, standard utilization of general anesthesia, and high-quality airway management during surgeries are the most important factors in this dominance. Hospitals and surgery rooms, in addition, usually stock masks in the thousands for day-to-day operating, making their muscles stronger in the market.

ASCs are the fastest-growing application segment owing to increasing preference for outpatient procedures that offer cost and time savings. ASCSs are increasingly equipped with state-of-the-art anesthesia machines and are being granted additional procedure privileges. As patients increasingly opt for minimally invasive surgeries in non-traditional hospital facilities, the necessity for small-footprint, high-efficiency, and patient-friendly ventilation and anesthesia masks in such facilities puts a further boost to the segment growth.

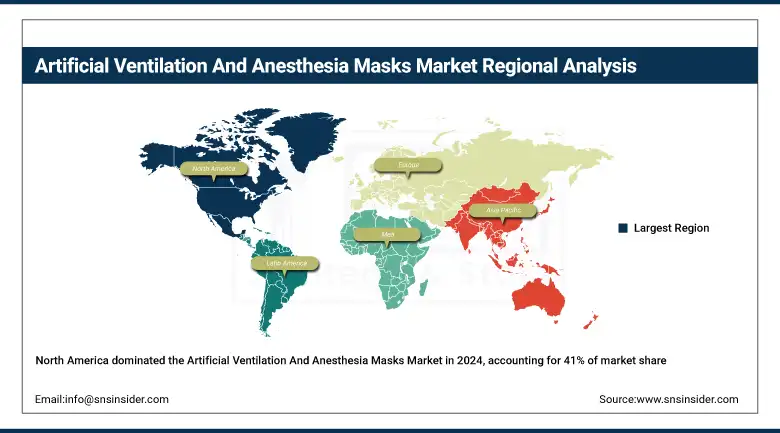

Regional Analysis:

The artificial ventilation and anesthesia masks market in North America held the largest revenue share of 41% in 2024, owing to well-advanced healthcare infrastructure, a larger number of surgical procedures in the region, and strong reimbursement policies.

Get Customized Report as per Your Business Requirement - Enquiry Now

The artificial ventilation and anesthesia masks market in Europe has a considerable market share, due to a well-established medical devices industry, along with a rising number of surgical and critical care admissions.

Germany is the major market of the region, owing to the presence of highly advanced surgical infrastructure and the highest per capita ICU beds in Europe, approximately 29.2 per 100,000 people. The market is being boosted by the EU's drive to promote hospital hygiene and infection prevention, which will encourage the use of single-use ventilation masks. France and the UK are spending on upgrading operating theaters and expanding day surgery, mainly at public hospitals, cranking up demand. Elderly populations rise, and the expansion of outpatient surgical facilities is driving the region’s growth, which is anticipated to remain strong. In Italy and Spain, the emphasis is on the post-COVID-19 ICU development, which indicates artificial ventilation and anesthesia masks market growth. Consistent regulations under MDR are attracting anesthesia and ventilation mask product manufacturers, driven by innovative makers.

Asia Pacific artificial ventilation and anesthesia masks market is anticipated to have a significant growth in the projected period, owing to increasing healthcare infrastructure, demand for surgeries, and a rise in infection control awareness.

China is the leading country in the region due to its larger patient base, growing government spending on health care, and rising number of inpatient surgeries. In 2024, China executed more than 20 million surgical operations, which was a main source of disposable mask usage. India is one of the fastest-growing nations, driven by growth in day-care surgeries, medical tourism, and public-private partnership in critical care. The availability has also increased due to local manufacturers producing low-cost ventilators. Japan and South Korea also make substantial investments in facilities for elderly care and high-tech operating rooms. Adoption of artificial ventilation and anesthesia masks in the region is on the rise, and is being used, indicating potential opportunities for foreign artificial ventilation and anesthesia masks companies looking to penetrate the market for the long term.

The artificial ventilation and anesthesia masks market in Latin America is expected to grow at the highest CAGR during the forecast period, due to advancements in the surgical and critical care infrastructure. Brazil is the powerhouse of the region, having the largest volume of surgery in Latin America and scaling up its public hospital capacity post-pandemic. Infection control directives have made purchasing single-use anesthesia devices a priority of the Brazilian government, increasing demand. The respiratory devices market is growing in Argentina with rising investment from the public and private sectors.

Table: Regulatory Approvals & Guidelines Impacting the Market (2023–2024)

|

Agency |

Approval/Guideline |

Impact Area |

Year |

|

U.S. FDA |

Emergency Use Authorization (EUA) update |

Portable ventilators, masks |

2023 |

|

EU MDR |

Compliance with reusable respiratory products |

Manufacturing, market entry |

2024 |

|

CDSCO (India) |

National policy on ventilator quality |

Domestic production standards |

2023 |

|

MHRA (UK) |

Guidelines for pediatric airway devices |

Pediatric mask design |

2024 |

Key Players:

Leading artificial ventilation and anesthesia masks companies operating in the market are Medtronic, Drägerwerk AG, Philips, ResMed, BD, Ambu A/S, Hamilton Medical, Air Liquide Medical Systems, Vyaire Medical, Nihon Kohden Corporation, Thermo Fisher Scientific, and GaleMed Corporation.

Recent Developments:

-

In June 2025, Ambu A/S received FDA approval in June 2025 for its aScope 5 Cysto HD, the first-ever single-use cysto-nephroscope, marking a strategic expansion into operating room respiratory and anesthesia support equipment.

-

In June 2024, GaleMed Corporation announced that it has achieved EU Medical Device Regulation (MDR) certification for more than 2,100 respiratory care items, including anesthesia and ventilation masks, ensuring enhanced compliance and access across European markets.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.37 billion |

| Market Size by 2032 | USD 3.54 billion |

| CAGR | CAGR of 5.15% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Mask (Disposable Masks, Reusable Masks) • By Application (Operating Rooms, ICU, Emergency Rooms, Homecare, ASCs) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Medtronic, Drägerwerk AG, Philips, ResMed, BD, Ambu A/S, Hamilton Medical, Air Liquide Medical Systems, Vyaire Medical, Nihon Kohden Corporation, Thermo Fisher Scientific, and GaleMed Corporation. |

Frequently Asked Questions

Ans: COVID-19 significantly accelerated demand for ventilators and disposable anesthesia masks, boosting innovation and regulatory fast-tracking.

Ans: Key artificial ventilation and anesthesia masks companies include Medtronic, Drägerwerk, Philips, ResMed, Ambu A/S, and Vyaire Medical.

Ans: Increasing prevalence of respiratory conditions, expanding ICU infrastructure, and rising demand for mechanical ventilators and oxygen masks are key growth drivers.

Ans: North America leads the global artificial ventilation and anesthesia masks market, followed by Europe, due to advanced healthcare infrastructure and high adoption rates.

Ans: The artificial ventilation and anesthesia masks market size reached a strong valuation in 2024, driven by rising surgical volumes and ICU admissions worldwide.

Get in Touch