Pressure Monitoring Market Report Scope & Overview:

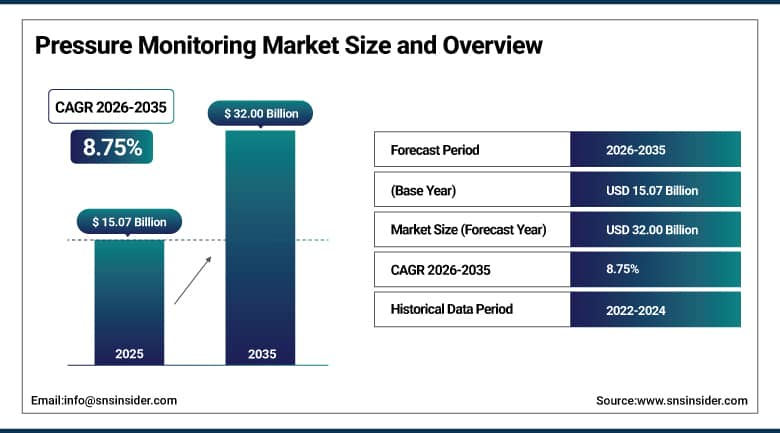

The Pressure Monitoring Market was valued at USD 15.07 Billion in 2025 and is expected to reach USD 32.00 Billion by 2035, growing at a CAGR of 8.75% from 2026 to 2035.

Globally, the trend in the pressure monitoring market is one that is recording a growth pattern, considering that the industry is experiencing a paradigm shift fuelled by increased awareness levels among people concerning their health status, increased incidence of cardiovascular diseases, and the trend towards personalized medical care. In this report, the increase in the incidence of both hypertension and cardiovascular disease are considered to be the major drivers, alongside regional trends in the adoption and usage of pressure monitors, especially amongst aging populations and those who are health conscious. This report seeks to differentiate the trend in the prescribing of blood pressure medication versus the need for self-monitoring through the use of pressure monitors.

In December 2024, Apple announced satellite texting capabilities in its Apple Watch Ultra 3, expanding the scope of emergency communication and underlining the brand's commitment to connected health safety. The capability extends Apple's health monitoring ecosystem beyond conventional pressure monitoring functionality, demonstrating the consumer electronics industry's progressive integration of health sensing capability into mainstream wearable devices whose accessibility creates expanded market reach for blood pressure and cardiovascular monitoring beyond traditional clinical and home healthcare device categories.

Market Size and Forecast

-

Market Size in 2026E: USD 16.39 Billion

-

Market Size by 2035: USD 32.00 Billion

-

CAGR: 8.75% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Pressure Monitoring Market - Request Free Sample Report

Pressure Monitoring Market Trends

-

AI integration in pressure monitoring devices is enabling predictive analytics, personalized health insights, and proactive patient management through intelligent monitoring systems

-

Rapid expansion of remote patient monitoring programs is increasing adoption of pressure monitoring solutions across home healthcare and chronic disease management applications

-

Growing use of wearable sensors and Bluetooth-enabled monitoring devices is improving patient compliance, data accuracy, and continuous health tracking capabilities

-

Integration of IoT connectivity and mobile health platforms is enhancing real-time data sharing, physician access, and telehealth-driven patient monitoring workflows

-

Development of cuffless and continuous pressure monitoring technologies is advancing non-invasive monitoring capabilities and expanding their use in both clinical and remote care settings

U.S. Pressure Monitoring Market Outlook

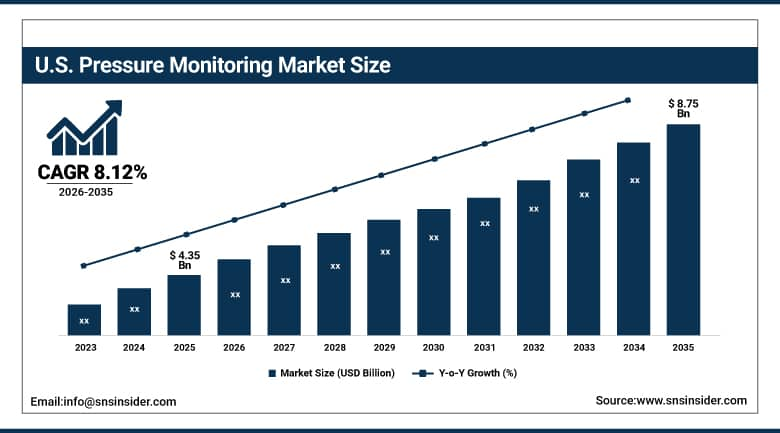

The U.S. Pressure Monitoring Market was valued at approximately USD 4.35 Billion in 2025 and is expected to reach approximately USD 8.75 Billion by 2035, growing at a CAGR of approximately 8.12%.

In the United States, market growth is driven by a high prevalence of hypertension, high consumer demand for remote monitoring, and positive reimbursement policies favouring digital health adoption among both urban and rural populations. Approximately 47 percent of adults suffer from hypertension according to CDC data, contributing to high clinical and homecare device demand. Favourable reimbursement models and robust telemedicine systems further solidify regional dominance. Welch Allyn, A&D Medical, SunTech Medical, Spacelabs Healthcare, and other major manufacturers collectively define the domestic commercial landscape serving hospital, ambulatory surgery centre, and home care settings across the country.

In November 2024, OMRON Healthcare disclosed that the U.S. Food and Drug Administration approved the firm's De Novo authorisation to market the latest home blood pressure monitors featuring cutting edge AI derived atrial fibrillation detection. The FDA clearance represents a significant regulatory milestone whose approval pathway demonstrates the growing acceptance of AI integrated health monitoring devices, enabling OMRON to expand its consumer cardiovascular monitoring portfolio with clinically validated screening capability that detects irregular heart rhythms during routine blood pressure measurement, creating differentiated value beyond conventional single function monitoring devices.

Pressure Monitoring Market Segment Analysis

-

By Product, the Pulmonary Pressure Monitors segment dominated the Pressure Monitoring Market with approximately 42.5% share in 2025, while the Blood Pressure Monitors segment is the fastest growing.

-

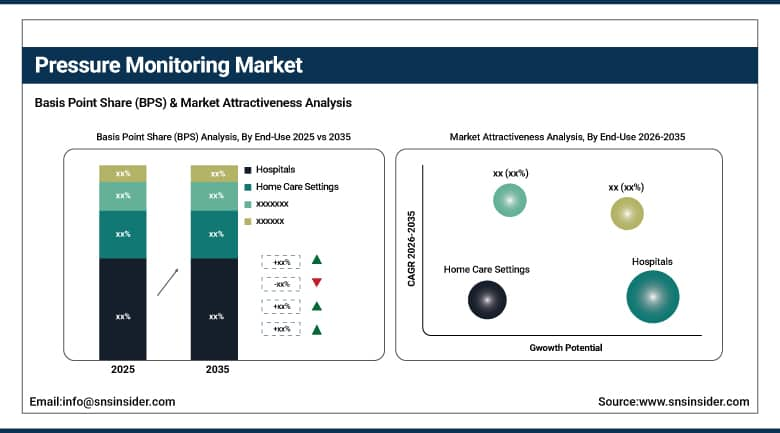

By End-Use, the Hospitals segment dominated the Pressure Monitoring Market in 2025, while the Home Care Settings segment is the fastest growing.

By End-Use, hospitals dominate, home care settings grow fastest

Hospitals retained the dominant end use position in the pressure monitoring market in 2025. Hospital based critical care, surgical, and inpatient monitoring requirements create the most commercially concentrated procurement of comprehensive pressure monitoring equipment across blood pressure, pulmonary, intraocular, and intracranial product categories. Each intensive care unit, operating theatre, and inpatient ward whose patient monitoring protocol requires continuous or intermittent pressure measurement creates hospital procurement whose breadth across multiple pressure monitoring product categories sustains the segment's commanding commercial position. The hospital setting's requirement for the most technically sophisticated monitoring equipment, including invasive intracranial pressure monitoring for neurosurgical and trauma patients, creates premium procurement that home care and ambulatory settings do not require at equivalent technical specification.

Home care settings are the fastest growing end use as the expansion of remote patient monitoring and consumer demand for convenient, real time health tracking create above average procurement growth outside traditional clinical environments. A study by the American Heart Association discovered that home blood pressure self-monitoring enhances patient compliance and treatment efficacy, demonstrating robust clinical justification for these devices. The growing trend toward home healthcare and personalised medicine provides substantial opportunity as patients increasingly choose home based care solutions that provide convenience, cost savings, and real time health tracking, with this need amplified by the rapid development of digital health technology and IoT connected monitoring devices.

By Product, pulmonary pressure monitors dominate, blood pressure monitors grow fastest

Pulmonary pressure monitors retained the dominant product position with approximately 42.5% of the pressure monitoring market in 2025. The large market share is ascribed to the growing prevalence of pulmonary hypertension and related respiratory disorders whose clinical severity creates non-discretionary continuous monitoring requirements in critical care, cardiology, and pulmonology settings. Each patient diagnosed with pulmonary arterial hypertension whose disease progression monitoring requires invasive or non-invasive pulmonary artery pressure measurement creates structured procurement whose per patient clinical value substantially exceeds conventional blood pressure monitoring equipment. The technology's integration into intensive care unit haemodynamic monitoring protocols, where continuous pulmonary artery pressure data informs fluid management and ventilator support decisions, sustains pulmonary pressure monitors' commanding position across the highest acuity clinical care environments.

Blood pressure monitors are the fastest growing product because the surging global incidence of hypertension, with approximately 1.28 billion adults aged between 30 and 79 years across the globe affected according to the World Health Organization, creates the highest unit volume procurement growth of any pressure monitoring category. Two thirds of hypertensive individuals reside in low- and middle-income nations, creating structured emerging market procurement growth as healthcare infrastructure investment expands monitoring access. The home based monitoring trend, where patients increasingly purchase personal blood pressure devices for self management, creates consumer market expansion that compounds with the clinical procurement base, sustaining blood pressure monitors' accelerating growth trajectory across both healthcare institution and direct consumer purchasing channels.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Pressure Monitoring Market Insights

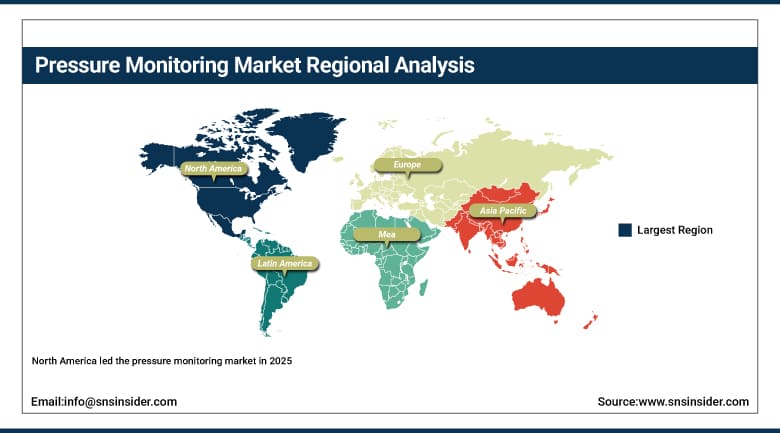

North America led the pressure monitoring market in 2025, driven by advanced healthcare infrastructure, high disease prevalence, and the early adoption of digital health tools. In the U.S., approximately 47 percent of adults suffer from hypertension, per CDC data, contributing to high clinical and homecare device demand. Favourable reimbursement models and robust telemedicine systems further solidify regional dominance. The United States accounts for approximately 87.4% of North American revenues through Welch Allyn, A&D Medical, SunTech Medical, and Spacelabs Healthcare's commercial operations.

Canada contributes complementary North American revenue through its publicly funded healthcare system's pressure monitoring equipment procurement and growing telehealth infrastructure investment supporting remote patient monitoring programmes across both urban and rural healthcare delivery networks.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Pressure Monitoring Market Insights

Europe is poised for substantial growth in the pressure monitoring market. Ageing demographics, government incentives for remote patient monitoring, and growing digital health awareness contribute to adoption. Countries such as Germany, France, and the United Kingdom are leading in home-based monitoring due to supportive chronic disease management programmes. Germany accounts for approximately 22.3% of European revenues through its strong hospital infrastructure and growing home healthcare device adoption.

The United Kingdom and France are significant secondary markets where NHS chronic disease management programmes and growing telemedicine infrastructure create consistent procurement. Dragerwerk's German headquarters and other European medical device manufacturers sustain regional commercial supply across the continent's pressure monitoring landscape.

Asia Pacific Pressure Monitoring Market Insights

Asia Pacific is the fastest growing regional pressure monitoring market, driven by accelerated funding by principal companies in advancing economies, China's vast population and rising hypertension rates impacting millions of people, and the region's focus on tech driven healthcare where smart monitoring equipment is gaining momentum, mainly in urban zones where digital health acceptance is at its peak. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary patient population scale and growing domestic medical device manufacturing capability.

India represents a particularly dynamic emerging market within Asia Pacific were increasing cardiovascular disease burden, expanding home healthcare, and rising penetration of affordable digital monitoring devices create above average regional procurement growth. Government health programmes and growing telehealth platforms drive uptake among hospitals, clinics, and individual consumers across the country's rapidly expanding healthcare infrastructure.

MEA & Latin America Pressure Monitoring Market Insights

Saudi Arabia leads MEA revenues through its growing hospital infrastructure investment under Vision 2030 healthcare modernisation programmes, supporting expanded access to advanced pressure monitoring equipment across Gulf medical centres and growing private hospital networks. The UAE's expanding specialty healthcare sector and growing medical tourism industry add complementary regional demand. Brazil leads Latin American revenues through its large hospital network and growing private healthcare sector's adoption of advanced cardiovascular monitoring solutions. Mexico's expanding healthcare infrastructure and Argentina's growing telehealth adoption collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Rising chronic disease prevalence and remote patient monitoring expansion

Growing worldwide incidence of chronic ailments such as high blood pressure, heart diseases, and breathing problems is the most significant growth factor in terms of commercial importance. According to the World Health Organization, there are 1.28 billion adults in the age group of 30 to 79 years who suffer from hypertension around the world, and two-thirds of them belong to the low and middle-income countries. This growing burden makes the need for continuous and dependable blood pressure monitoring necessary both at home and in the clinic. At the same time, advancements in the field of monitoring technology including wearable sensor technology, Bluetooth cuffs, and AI based monitoring systems are changing the game of vital signs monitoring.

Increased growth in remote patient monitoring and digital health platforms has opened up possibilities for wider access to pressure monitoring, particularly in response to the pandemic which fast tracked the move toward home care. The increased focus on preventive healthcare, along with increased patient awareness, is also driving market growth, compelling healthcare professionals and patients to embrace contemporary pressure monitoring solutions and providing a sound basis for long term market growth across both clinical and consumer market channels.

Restraints: High device costs and limited reimbursement policies

The costly aspect associated with the deployment of advanced pressure measurement instruments constitutes a significant barrier to growth in the market. The cost of instruments featuring smart sensors, wireless communication and cloud computing features is relatively high compared to the ability of the majority of the population to afford. Smart pressure monitoring instruments range between USD 50 and USD 150 each, an amount that could be too high for low income families or medical institutions in developing countries to purchase.

Unlike the case of insurance reimbursement of hospital monitoring equipment, out of pocket expenses for personal monitoring instruments are likely to discourage the adoption of the same by the patients for prolonged durations of time. Budgets allocated to public health care in poorer regions are focused on addressing the immediate clinical needs rather than preventative measures in terms of technology, with economic factors and inconsistent support continuing to hinder market penetration.

Opportunities: Home based monitoring expansion and AI powered predictive analytics

The growing trend toward home healthcare and personalised medicine provides substantial opportunity for the pressure monitoring market. With the expansion of chronic conditions and ageing populations, patients increasingly choose home based care solutions that provide convenience, cost savings, and real time health tracking. The intermingling of IoT, mobile health applications, and cloud connectivity facilitates remote monitoring and doctor access to current patient information, creating opportunity for diversification of products, innovation, and market outreach in unreached rural and semi urban regions where conventional care delivery is constrained.

Artificially intelligent pressure monitoring equipment can recognise signs of impending health decline, providing predictive feedback and tailored health alerts. AI based algorithms embedded in wearable monitors are now able to scan patterns and suggest lifestyle or medication changes, minimising hospitalisations. Governments and private entities alike are increasingly putting money into telehealth infrastructure, developing an enabling environment for smart pressure monitoring devices that creates substantial commercial opportunity for manufacturers capable of demonstrating measurable clinical outcome improvement.

Recent Developments:

-

2024: OMRON Healthcare disclosed in November 2024 that the U.S. FDA approved the firm's De Novo authorisation to market the latest home blood pressure monitors featuring cutting edge AI derived atrial fibrillation detection capability.

-

2024: Apple announced satellite texting capabilities in its Apple Watch Ultra 3 in December 2024, expanding the scope of emergency communication and underlining the brand's commitment to connected health safety within its broader health monitoring ecosystem.

-

2024: A&D Medical introduced a multi user blood pressure monitor with secure cloud access in November 2024 designed for assisted living and multi patient home settings, addressing institutional healthcare provider demand for shared monitoring infrastructure.

-

2024: Spacelabs Healthcare partnered with dabl in 2024, initially for the United Kingdom and Italy, enabling primary healthcare practitioners and local pharmacies to provide fast, reliable, and interpretive ambulatory blood pressure monitoring reports.

-

2024: Medicare expanded coverage for remote patient monitoring services in 2024, including reimbursement for blood pressure readings transmitted from a patient's home, encouraging primary care practices and cardiology groups to deploy Bluetooth enabled monitors as part of chronic disease management bundles.

Pressure Monitoring Market Key Players

-

OMRON Healthcare Inc.

-

Welch Allyn (Hillrom)

-

Dragerwerk AG & Co. KGaA

-

SunTech Medical Inc.

-

A&D Medical (A&D Company Limited)

-

Rossmax International Ltd.

-

Spacelabs Healthcare Inc. (OSI Systems)

-

Koninklijke Philips N.V.

-

GE HealthCare Technologies Inc.

-

Medtronic plc

-

Edwards Lifesciences Corporation

-

Natus Medical Incorporated

-

Integra LifeSciences Corporation

-

Vasamed Inc.

-

Mortara Instrument Inc.

-

American Diagnostic Corporation

-

Schiller AG

-

Microlife Corporation

-

Beurer GmbH

-

iHealth Labs Inc.

Pressure Monitoring Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.07 Billion |

| Market Size by 2035 | USD 32.00 Billion |

| CAGR | CAGR of 8.75% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Blood Pressure Monitors, Pulmonary Pressure Monitors, Intraocular Pressure Monitors, Intracranial Pressure Monitors) • by End-Use (Hospitals, Ambulatory Surgery Centers, Home Care Settings, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | OMRON Healthcare Inc., Welch Allyn (Hillrom), Dragerwerk AG & Co. KGaA, SunTech Medical Inc., A&D Medical (A&D Company Limited), Rossmax International Ltd., Spacelabs Healthcare Inc. (OSI Systems), Koninklijke Philips N.V., GE HealthCare Technologies Inc., Medtronic plc, Edwards, Lifesciences Corporation, Natus Medical Incorporated, Integra LifeSciences Corporation, Vasamed Inc., Mortara Instrument Inc., American Diagnostic Corporation, Schiller AG, Microlife Corporation, Beurer GmbH, iHealth Labs Inc. |

Frequently Asked Questions

North America dominated the Pressure Monitoring Market in 2025, while Asia Pacific is the fastest growing region driven by China's vast population and rising hypertension rates.

The increasing global prevalence of chronic conditions such as hypertension affecting approximately 1.28 billion adults worldwide, and increased growth in remote patient monitoring and digital health platforms that have opened up possibilities for wider access to pressure monitoring, particularly accelerated by the shift toward home based care.

Pulmonary Pressure Monitors dominated the Pressure Monitoring Market with approximately 42.5% share in 2025, while Blood Pressure Monitors is the fastest growing segment.

Get in Touch