Asphalt Pavers Market Report Scope & Overview:

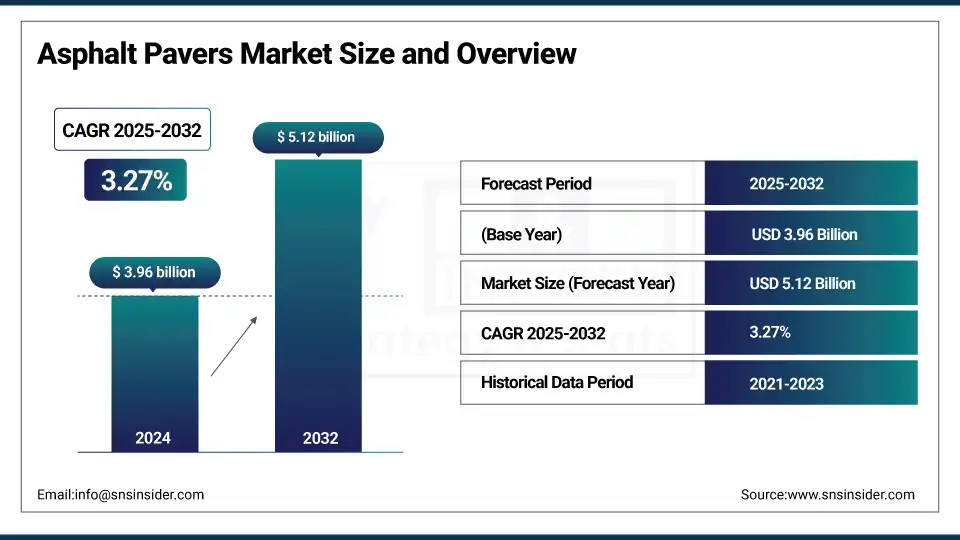

The Asphalt Pavers Market size was valued at USD 3.96 billion in 2024 and is expected to reach USD 5.12 billion by 2032, growing at a CAGR of 3.27% over the forecast period of 2025-2032.

The global asphalt pavers market is witnessing robust development, driven by increasing urbanization, infrastructure upgrades, and road construction activities worldwide. The asphalt pavers industry is significant in highway expansion, airport runways, and residential streets, among others, where speed and surface quality are critical. One of the significant trends influencing the market are smart technology which includes automated paving controls, telematics for equipment diagnostics, real-time monitoring, and performance optimization. To address sustainability objectives, manufacturers are adapting electric and hybrid pavers to help lower or eliminate emissions in the company of the worldwide demand for sustainable construction solutions.

To Get more information On Asphalt Pavers Market - Request Free Sample Report

Innovation is further accelerating through the development of screed technologies that ensure uniform compaction and smoother finishes. There is an increasing demand for track pavers instead, because these offer better stability and traction on uneven surfaces as compared to wheel pavers. Rising public infrastructure and smart city projects investments by governments are spurring demand for durable and high-performance paving equipment. In the last few years, some companies have also started using the Internet of Things and GPS sensor-based systems to work accurately and reduce downtime. Over the years, the asphalt pavers market has been experiencing a sea change driven by advanced engineering, digitalization, and the green mandate, forcing construction stakeholders to choose high-efficiency construction solutions.

In March 2025, at Bauma 2025, Vögele unveiled its Dash 5 series, including its first wheeled paver (SUPER 1803‑5 X‑Tier) and fully electric MINI 500e/502e models with up to 11 hours of zero-emission operation. Key innovations include the AutoTrac automatic steering, Smart Pave control system, and WPT Paving for digital jobsite tracking.

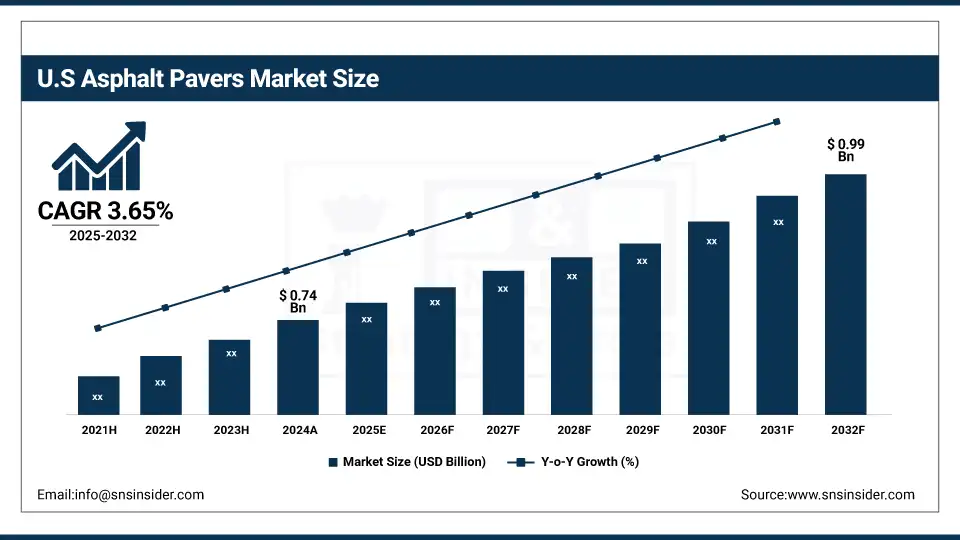

The U.S. asphalt pavers market is set to grow from USD 0.74 billion in 2024 to USD 0.99 billion by 2032, at a CAGR of 3.65%. The growth is attributed to continuous investment in infrastructure, road repairs, and new paving technologies. Market expansion is also aided by federally funded transportation modernization.

Asphalt Pavers Market Dynamics:

Drivers

-

Rapid Global Infrastructure Investment Is Significantly Boosting the Demand for Advanced Asphalt Pavers to Meet Large-Scale Road Construction Needs.

Rapid infrastructure investment is a major driver in the asphalt pavers market, propelled by global government initiatives to enhance transportation networks. Countries like the U.S, India, China, and all over Europe are investing heavily in road construction and upgrades. Worldwide, the U.S. Bipartisan Infrastructure Law sets aside USD 110 billion for roads and bridges, whereas India, under its Gati Shakti scheme, aims to build more than 25,000 km of highways. In much the same way, long-term infrastructure growth in Asia as well as Africa continues to be spurred on by China’s Belt and Road Initiative. Brazil and Mexico are still stepping up urban road and highway construction in Latin America. Such large-scale projects require high-capacity and efficient road paving machines which has a high intake of sophisticated asphalt pavers as they can meet the strict deadlines and also maintain the quality of the surface. Such a trend is one of the important points contributing to asphalt pavers market growth pertaining to performance, durability, and automation.

Restraint

-

High Capital and Operating Costs Hinder Adoption of Advanced Asphalt Pavers

One of the major restraints in the asphalt pavers market is the high capital and operating costs associated with these machines. High-tech pavers with GPS, telematics, and automation cost about twice as much as traditional paver models. This hefty, up-front investment represents a significant barrier for most small and mid-sized contractors. Additionally, maintenance, spare parts, and fuel costs continue to burden ownership costs. Industry experts say operating costs are more than 35% of the life cycle costs of a machine. Overhead is additionally raised by the requirement for skilled staff to run or service such high-tech equipment. This creates financial challenges that can postpone procurement decisions, particularly in areas where there is little public infrastructure budget. High Capital & Operating Costs

Asphalt Pavers Market Segmentation Analysis:

By Type

The wheel pavers segment dominated the market and accounted for 56% of the asphalt pavers market share. They're dominant because they have better mobility, so their ideal for urban areas, highways, and patchwork projects where you need to get quickly to where you need to go. For more productivity, wheel pavers feature better speed and handling on paved or semi-paved surfaces, thus reducing downtime. Plus, their lower operating and maintenance costs relative to tracked models make them more economical for contractors, particularly in regions needing frequent moves or softer substrates. This versatility and adaptability to different paving conditions keep them in demand across regions.

Screeds are the fastest-growing segment due to the rising demand for high-quality, smooth pavement surfaces in modern infrastructure. Advanced screed technologies, including variable vibration frequency, thermal control, and hydraulic extension, also contribute to improved surface uniformity, thickness control, and material consolidation. All of the enhancements minimize the requisite manual adjustment post pavement and facilitate greater construction quality. With the growing focus on new urban roads in terms of quality and longevity, more wheeled and tracked pavers are now adopting sophisticated screeds. The Global Market is growing rapidly due to the increasing role in maintaining the durable and uniform pavement.

By Pavement Width

The 2.5–5 meters pavement width segment dominated the asphalt pavers market due to its optimal balance between versatility and efficiency. This portion is best suited for a wide variety of paving projects, including municipal roads, city streets, and highways, or other small commercial projects. It provides enough coverage for quick progress, while life does not compromise on maneuverability in tight spaces. Most contractors choose this size for its ability to minimize the number of passes while still getting the job done accurately. That is due to its compatibility with medium and large-scale projects all around the world, both in developed and developing regions, thus making it very widespread and a market share leader.

The more than 5 meters segment is the fastest-growing due to surging demand from large-scale infrastructure projects such as expressways, airport runways, and major highways. Increased Paving Widths are Beneficial, as wider paving widths enable contractors to cover more area in fewer passes, operational efficiency is increased, project duration and labor cost are reduced. With governments and private sectors increasingly initiating mega infrastructure development projects to enhance connectivity and economic growth, the demand for high-capacity, wide-width asphalt pavers is witnessing a surge. Moreover, technological improvements regarding material handling, automated leveling systems also facilitate the growth of this segment.

By Screed Type

Hydrostatic screeds dominated the market as they provide enhanced control, consistent mat thickness, and superior compaction compared to mechanical variants. They operate on fluid pressure for smoother adjustment and more uniform asphalt distribution, and they are equipped with screeds. Hydrostatic screeds improve speed regulation and ease of use and are therefore suitable for high-precision or complex jobs, thus making it easier for the operator. As new technology develops, traditional paving rights give way to smart systems used in new modern paver systems that have integrated technologies that help avoid the need for operator corrections, each time the quality is enhanced. That is what makes them popular among professional contractors and large construction companies.

Hydrostatic screeds are also the fastest-growing segment due to their alignment with the ongoing shift toward digital and automated paving solutions. They are catching on in markets where construction equipment is becoming more modernized by an ability to provide high-performance output with minimal engagement. Adoption is driven by features like variable vibration settings, automatic slope control, and seamless extension support. Hydrostatic screed segment is growing at a fast pace across all developed and emerging markets on account of the increasing focus of road authorities on durability, surface smoothness, and long-term Performance.

By Operating Weight

The over 15,000 kg segment dominated the asphalt pavers market due to its ability to handle high-output applications like highways, airport runways, and large industrial roads. These industrial-grade machines are built to deliver higher stability, deeper compaction, and wider paving capability, which makes them ideal for tough, high-volume jobs. Having a sturdy design means they can work much longer without overheating or overheating, allowing major job sites to keep the workload up. This segment continues to be the leading segment, thanks to the consistently high demand for powerful and high-capacity pavers, driven by the rising global infrastructure spending, especially in transport and logistics corridors.

The 8000–12000 kg segment is the fastest-growing due to its perfect balance between size, power, and flexibility. These are best suited for medium to large-sized construction and rehabilitation projects due to their compact design without performance compromise. With multiple benefits, such as increased fuel economy, the ability to make tight turns in urban settings, and enough power for a range of paving widths. This weight category is getting popular due to the rise of urban development as well as the push from contractors to find economic solutions without compromising on the output. In addition, manufacturers are launching more sophisticated variants in this category, which is driving the adoption and expansion of this category in various regions.

Asphalt Pavers Market Regional Outlook:

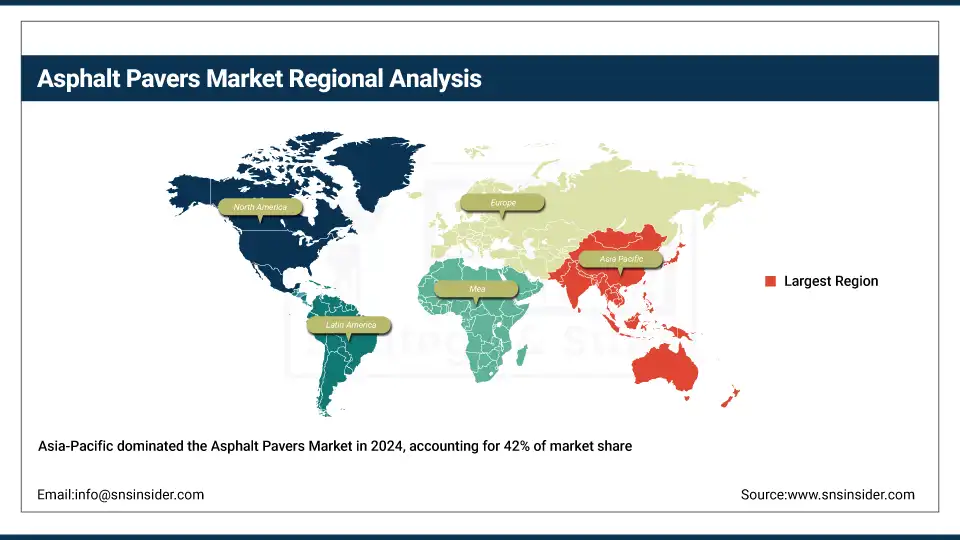

Asia-Pacific dominates the global asphalt pavers market, accounting for approximately 42.00% of the total share. This can be traced back to extensive infrastructure development projects, road expansion programs, and urbanization in the developing world (China, India, other Southeast Asian countries). Demand for equipment is mainly driven by Government Investments in National highways, Smart cities, and Road connectivity in rural areas. Moreover, the region is also projected to retain its market dominance owing to the presence of key manufacturers along with the penetration of advanced paving technologies in countries like China and Japan.

Get Customized Report as per Your Business Requirement - Enquiry Now

China dominates the Asia-Pacific asphalt pavers market due to its vast and continuous infrastructure development projects, including extensive highway construction and urban road expansions. Demand for paving machinery is also boosted by strong government initiatives such as the Belt and Road Initiative. Furthermore, the demand for advanced asphalt paving equipment is driven by China having a vast manufacturing base and the pace of rapid urbanization, which subsequently makes this country dominate the region.

North America is the fastest-growing region in the asphalt pavers market, driven by increased investments in infrastructure rehabilitation, highway upgrades, and smart paving technologies. The U.S. Bipartisan Infrastructure Law has unlocked billions for road construction, accelerating demand for technologically advanced pavers with telematics and automation. Growing adoption of eco-friendly and emission-compliant equipment, along with fleet modernization among contractors, continues to fuel regional growth at a rapid pace.

Europe holds a significant share in the global asphalt pavers market, backed by well-established road networks and ongoing maintenance projects. In Germany, France, and the UK, for example, sustainable transport infrastructure is being heavily invested in, and only high precision, low-emission paving machines can be used to meet tough environmental standards. Innovation-led demand backed by the continued push to minimize downtimes, the ability to provide high-quality roads, and the integration of digital technologies, such as 3D paving control systems, are a few of the sine qua non elements driving the European road construction equipment market.

Key Players in the Asphalt Pavers Market are:

Asphalt Pavers Companies are AB Volvo, Fayat Group, Caterpillar, Astec Industry, XCMG Construction Machinery Company, AMMANN GROUP, Zoomlion, AUNG HEIN MIN CO., LTD., SANY GROUP, Deere & Company, Dynapac, LeeBoy, BOMAG GmbH, Sumitomo Construction Machinery, Roadtec, VÖGELE - a Wirtgen Group brand, Sakai Heavy Industries, LiuGong Machinery, Mauldin Paving Products, Shantui Construction Machinery Co., Ltd.

Recent Development:

-

In February 2025, Dynapac announced its participation in bauma 2025, set for April in Munich, showcasing a new generation of highway pavers. The company emphasized digital solutions under the theme “Connect and Control,” aiming for smarter, more connected machines. It also highlighted its push toward sustainability with expanded electric equipment offerings and robust aftermarket support.

-

In March 2025, Caterpillar previewed its new AP600, AP655, AP1000, and AP1055 asphalt pavers ahead of the World of Asphalt 2025. These models offer improved fuel efficiency, easier operation, and enhanced mat quality using advanced Axenox screed plates. The design helps achieve better compaction and smoother finishes with fewer roller passes.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.96 Billion |

| Market Size by 2032 | USD 5.12 Billion |

| CAGR | CAGR of 3.27% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Track pavers, Wheel pavers, Screeds) • By Pavement Width (Less than 2.5 Meters, 2.5 – 5 Meters, More than 5 Meters) • By Screed Type (Hydrostatic, Mechanical) • By Operating Weight (5000–8000 Kgs, 8000–12000 Kgs, 12000–15000 Kgs, Over 15000 Kgs) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | AB Volvo, Fayat Group, Caterpillar, Astec Industry, XCMG Construction Machinery Company, AMMANN GROUP, Zoomlion, AUNG HEIN MIN CO., LTD., SANY GROUP, Deere & Company, Dynapac, LeeBoy, BOMAG GmbH, Sumitomo Construction Machinery, Roadtec, VÖGELE - a Wirtgen Group brand, Sakai Heavy Industries, LiuGong Machinery, Mauldin Paving Products, Shantui Construction Machinery Co., Ltd. |

Frequently Asked Questions

The Asia-Pacific region dominated the Asphalt Pavers Market in 2024.

The “wheel pavers” segment dominated the Asphalt Pavers Market.

Rapid Global Infrastructure Investment Is Significantly Boosting the Demand for Advanced Asphalt Pavers to Meet Large-Scale Road Construction Needs.

The Asphalt Pavers Market was USD 3.96 billion in 2024 and is expected to reach USD 5.12 billion by 2032.

The Asphalt Pavers Market is expected to grow at a CAGR of 3.27% from 2025-2032.

Get in Touch