Asset Management Market Report Scope & Overview:

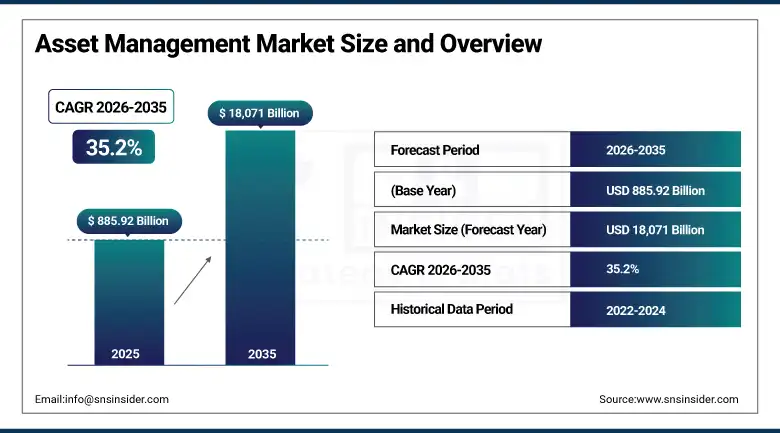

The Asset Management Market was valued at USD 885.92 Billion in 2025 and is expected to reach USD 18,071 Billion by 2035, growing at a CAGR of 35.2% from 2026–2035.

The asset management market encompasses the complete spectrum of technologies, platforms, and professional services that organisations deploy to systematically track, maintain, optimise, and derive maximum value from their physical, digital, financial, and infrastructure asset portfolios across the entire asset lifecycle from acquisition through operation to disposal. The market's extraordinary scale reflects the convergence of multiple asset management disciplines, including enterprise asset management whose IBM Maximo, Oracle EAM, and SAP PM platforms manage the physical equipment and facility assets of manufacturing, energy, and infrastructure organisations, asset performance management whose AI-powered predictive maintenance and condition monitoring platforms optimise asset reliability and operational efficiency. The financial asset management dimension whose technology platforms manage the investment portfolios, risk models, and regulatory compliance frameworks of institutional and retail asset managers globally.

In November 2023, ABB Ltd. launched ABB Ability SmartMaster, a condition-monitoring platform designed for critical assets in oil and gas and water treatment sectors, providing real-time equipment health monitoring through cloud-connected sensor data analysis that enables predictive maintenance scheduling before failures occur. The SmartMaster platform demonstrated ABB's strategy of embedding AI-powered asset intelligence into its industrial equipment ecosystem, creating a connected asset management layer whose continuous data collection and analysis generate operational insight that reactive maintenance programmes cannot achieve.

Market Size and Forecast

-

Market Size in 2026E: USD 1,197.77 Billion

-

Market Size by 2035: USD 18,071 Billion

-

CAGR: 35.2% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Asset Management Market - Request Free Sample Report

Asset Management Market Trends

-

AI and machine learning are enabling predictive maintenance, asset performance optimization, and failure forecasting across enterprise asset portfolios.

-

Cloud-based asset management platforms are gaining adoption due to scalability, mobility, and seamless integration with IoT ecosystems.

-

Digital twin technology is improving real-time asset monitoring, maintenance planning, and operational efficiency.

-

ESG-focused asset management solutions are supporting sustainability reporting, carbon tracking, and climate risk assessment requirements.

-

Blockchain technology is emerging for asset provenance, ownership verification, and secure lifecycle record management of high-value assets.

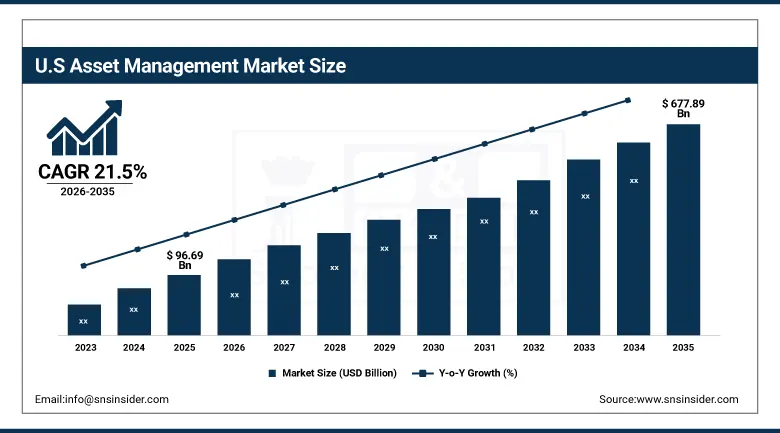

The U.S. Asset Management Market Outlook

The U.S. Asset Management Market was valued at approximately USD 96.69 Billion in 2025 and is projected to grow to approximately USD 677.89 Billion by 2035, growing at a CAGR of approximately 21.5%. The United States will witness tremendous growth owing to rising demand for complex investment solutions fueled by an expanding base of high-net-worth individuals and institutional investors, combined with the use of cutting-edge technologies such as AI and data analytics for optimizing investment strategies and portfolio management.

The United States asset management market is driven by the most extensive commercial and industrial asset base among major economies whose aggregate replacement value represents the largest national capital stock requiring systematic lifecycle management. Federal infrastructure investment under the Infrastructure Investment and Jobs Act whose USD 1.2 trillion commitment includes significant maintenance and lifecycle management requirements for highway, bridge, transit, and utility infrastructure creates government-funded demand for asset management technology and services. The world's largest institutional investment management industry, encompassing BlackRock, Vanguard, Fidelity, and State Street whose combined assets under management exceed USD 25 trillion, creates the most commercially significant financial asset management technology market globally whose platform investment, analytical software, and risk management system procurement sustains a premium commercial demand segment.

In January 2023, Schneider Electric finalized the acquisition of AVEVA to deliver a more integrated approach to industrial digital transformation and resource optimization. The acquisition combined Schneider Electric's energy management and automation expertise with AVEVA's industrial software capabilities, creating an integrated asset management platform that serves both the operational technology and the business intelligence requirements of industrial asset-intensive organizations whose management of complex physical asset portfolios benefits from unified data models spanning equipment condition, energy consumption, production performance, and maintenance cost.

Asset Management Market Segment Analysis

-

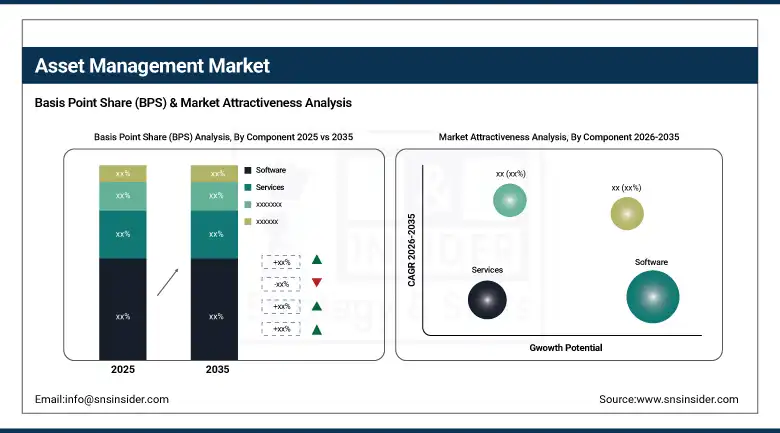

By Component, software segment dominated the asset management market with approximately 64% market share in 2025, while the services segment is projected to be the fastest growing, registering a CAGR of around 12.1% during 2026–2035.

-

By Deployment Mode, cloud-based segment dominated the asset management market in 2025, while on-premise deployment retains commercial importance in regulated and security-sensitive asset management environments.

-

By Asset Type, fixed assets segment dominated the asset management market with the largest share in 2025, while the digital assets segment is the fastest growing asset type driven by expanding cryptocurrency, tokenized asset, and digital infrastructure asset management requirements.

-

By End User, manufacturing segment dominated the asset management market with the largest share in 2025, while the IT & telecom segment is among the fastest growing end users driven by data centre asset management and network infrastructure lifecycle requirements.

By Component, software dominates, services grow fastest

Software retained the dominant component position with the largest share of the asset management market in 2025, reflecting the foundational role of asset management platforms whose operational functionality encompasses asset registry management, maintenance work order processing, preventive maintenance scheduling, spare parts inventory optimization, and compliance documentation whose combined software capability creates the information management infrastructure that all other asset management activities depend upon. The enterprise asset management software market encompasses both the established incumbent platforms including IBM Maximo Application Suite, Oracle EAM, SAP Plant Maintenance, and Infor EAM whose large installed bases generate recurring license and maintenance revenue.

Services are growing fastest as the gap between asset management platform capability and organizational capacity to deploy, configure, and optimize platform functionality creates sustained demand for implementation consulting, system integration, change management, and managed service operation that specialist asset management service providers deliver. Each asset management platform implementation project whose scope encompasses legacy data migration, IoT sensor integration, mobile application deployment, and business process reengineering creates substantial professional services engagement whose value frequently exceeds the platform software license cost, sustaining services revenue growth above platform software growth rates.

By End User, manufacturing dominates, IT & telecom grows fastest

Manufacturing retained the dominant end user position with the largest share of the asset management market in 2025, reflecting the foundational commercial relationship between manufacturing asset intensity and asset management investment motivation whose direct connection between equipment availability and production output creates the clearest and most financially quantifiable asset management ROI calculation of any end user sector. Manufacturing organisations whose production lines, process equipment, tooling, and facility infrastructure collectively represent capital investments of hundreds of millions to billions of dollars require systematic maintenance management, condition monitoring, and lifecycle planning whose asset management platform support enables the operational reliability and capital efficiency that competitive manufacturing requires.

IT and telecommunications is growing fastest as the explosive expansion of data centre infrastructure for AI workloads, the proliferation of distributed edge computing assets, and the complexity of multi-vendor telecommunications network asset portfolios create growing demand for asset lifecycle management, capacity planning, and infrastructure compliance documentation that traditional IT asset management tools extended with AI analytics and IoT connectivity enable. Each new hyperscale data centre whose server, storage, network, and power infrastructure spans tens of thousands of individual managed assets creates substantial EAM software deployment for asset tracking, maintenance management, and end-of-life planning that scales with the global data centre construction programme.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

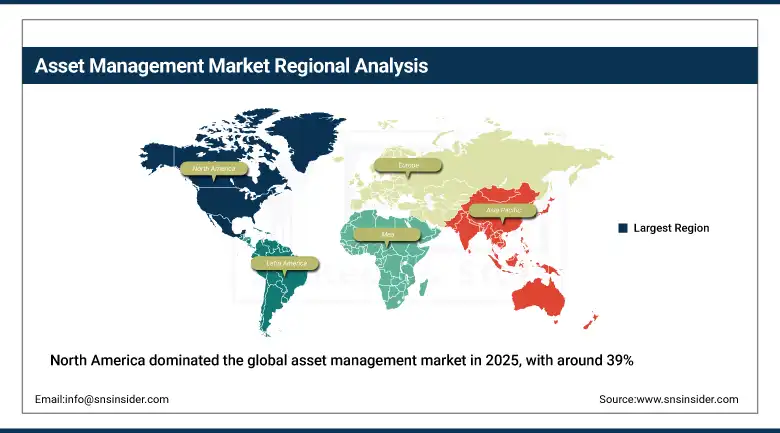

North America Asset Management Market Insights

North America dominated the global asset management market in 2025, with around 39% share and maintained its leadership in 2025 through the combination of the world's largest installed base of enterprise asset management software. The highest concentration of global investment management AUM in its financial services sector, and the most extensive industrial infrastructure requiring systematic lifecycle management. The United States accounts for approximately 82.5% of North American revenues through the commercial presence of IBM, Oracle, SAP, Honeywell, ABB, and Rockwell Automation whose enterprise asset management platform businesses define global market standards, and the world-leading financial asset management industry whose technology investment sustains a large and premium-priced asset management software and services market.

Canada contributes supplementary demand through its resource extraction industry's extensive physical asset management requirements in mining, oil sands, and forestry operations, the government infrastructure asset management obligations under public sector lifecycle management standards, and the growing financial services sector's investment management technology adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Asset Management Market Insights

Europe held a significant share of the global Asset Management Market in 2025. Germany, the United Kingdom, France, the Netherlands, and Switzerland are the leading national markets whose manufacturing, financial services, energy, and public infrastructure sectors create comprehensive and technically demanding asset management demand. Germany accounts for approximately 28.5% of European revenues through its world-leading manufacturing sector's asset management platform investment, the commercial presence of SAP and Siemens whose asset management technology businesses serve both European and global markets, and the energy sector's extensive infrastructure asset lifecycle management requirements.

Asia Pacific Asset Management Market Insights

Asia Pacific is the fastest-growing regional asset management market, driven by the rapid industrialization creating new physical asset portfolios requiring systematic management, the expanding financial services sector whose AUM growth creates investment management technology demand, and government infrastructure investment programmes whose asset lifecycle management requirements create public sector EAM platform adoption. China accounts for approximately 38.5% of Asia Pacific revenues through the manufacturing sector's extensive EAM platform deployment. The rapidly growing financial asset management industry whose domestic fund AUM has grown dramatically in recent years, and the smart infrastructure investment programme whose IoT-connected asset management creates new digital asset management demand.

Japan, South Korea, and Australia contribute premium regional demand through their advanced manufacturing sectors, sophisticated financial services industries, and well-developed enterprise technology adoption. India is growing fastest within the region where manufacturing sector expansion, infrastructure investment under the National Infrastructure Pipeline, and financial sector digitalization are collectively creating above-regional-average asset management market growth.

MEA & Latin America Asset Management Market Insights

The UAE leads MEA revenues of the regional total through its world-class infrastructure portfolio requiring systematic lifecycle management, the large sovereign wealth fund and investment management industry whose financial asset management technology investment sustains a premium commercial segment, and the government's smart city asset management programme whose IoT-connected public infrastructure creates digital asset management platform demand. Saudi Arabia's Vision 2030 industrial diversification programme and mega-project infrastructure portfolio create growing physical asset management requirements.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its extensive manufacturing, mining, and energy sector physical asset base requiring EAM platform management, the growing financial services sector's investment management technology adoption, and the public infrastructure asset management requirements of its large federal government portfolio. Mexico and Colombia are growing secondary markets whose manufacturing sector expansion and financial services modernization create above-regional-average asset management demand growth.

Market Dynamics

Growth Drivers: AI and IoT-driven predictive asset management transformation and the AI-enabled growth of financial assets under management are the primary structural growth drivers

The asset management market's extraordinary growth rate is powered by the convergence of two mutually reinforcing demand forces whose compounding momentum creates a market expansion trajectory unprecedented in the enterprise technology industry. The AI and IoT revolution in industrial asset management is transforming the value proposition of enterprise asset management platforms from administrative maintenance tracking to strategic operational intelligence whose predictive failure detection, autonomous maintenance scheduling, and asset lifecycle optimization deliver measurable operational reliability improvement and capital efficiency gain that justifies platform investment multiples above what legacy administrative EAM systems could sustain. Simultaneously, the global financial markets' continued growth, the democratization of investment access through robo-advisory and digital wealth management platforms.

Restraints: High implementation complexity of enterprise asset management systems and data quality requirements for AI-powered predictive analytics constraining deployment effectiveness in legacy industrial environments

Enterprise asset management system implementation in established industrial organizations whose asset registry data may be incomplete, inconsistently maintained, or stored in incompatible legacy systems creates data quality remediation requirements that extend implementation timelines, increase project costs, and delay the operational benefit realization that EAM investment is intended to deliver. The AI-powered predictive analytics capabilities that represent the most commercially compelling advanced EAM functionality require clean, complete, and historically continuous sensor and maintenance data whose availability at the quality needed for reliable machine learning model training is absent in many industrial environments whose instrumentation history predates systematic digital data collection.

Opportunities: Digital twin integration with enterprise asset management and ESG asset management platform development represent transformative market expansion frontiers

Digital twin technology whose virtual simulation of physical asset behavior provides a testing ground for operational decisions, maintenance interventions, and capital replacement scenarios. Whose impact can be evaluated in the digital environment before commitment in the physical creates an asset management capability whose integration with existing EAM platforms creates a premium product tier whose value proposition extends beyond historical data management into forward-looking operational intelligence. Each industrial asset whose digital twin model is calibrated from real-time sensor data enables operating teams to evaluate the consequence of maintenance decisions, process parameter changes, and operating condition variations on asset health and remaining useful life before implementation, creating a decision support capability whose operational and financial value is proportional to the capital intensity and consequence severity of the managed asset.

Recent Developments:

-

2025: ABB launched ABB Ability SmartMaster for critical asset condition monitoring in oil and gas and water treatment sectors, providing real-time equipment health assessment through cloud-connected sensor analysis enabling predictive maintenance scheduling and operational risk reduction.

-

2023: Schneider Electric finalized the acquisition of AVEVA to deliver an integrated approach to industrial digital transformation and resource optimization, combining energy management expertise with industrial asset management software in a unified platform for asset-intensive industries.

-

2023: IBM expanded its Maximo Application Suite with enhanced AI-powered visual inspection, predictive maintenance, and enterprise asset management capabilities integrated with AWS and Azure cloud infrastructure, enabling asset-intensive industries to deploy AI-driven asset intelligence across their operational technology and IT asset portfolios.

Asset Management Market Key Players are:

-

IBM Corporation

-

Oracle Corporation

-

SAP SE

-

Infor, Inc.

-

Hexagon AB

-

Bentley Systems, Incorporated

-

AVEVA Group plc

-

Siemens AG

-

Rockwell Automation, Inc.

-

ABB Ltd.

-

Microsoft Corporation

-

IFS AB

-

AssetWorks LLC

-

Aptean, Inc.

-

Ultimo Software Solutions BV

-

UpKeep Technologies, Inc.

-

eMaint Enterprises, LLC

-

MRI Software LLC

-

Accruent, LLC

-

IBM Maximo Application Suite

Asset Management Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 885.92 Billion |

| Market Size by 2035 | USD 18,071.01 Billion |

| CAGR | CAGR of 35.2% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Deployment Mode (Cloud-Based, On-Premise) • By Asset Type (Fixed Assets, Digital Assets, Financial Assets, Infrastructure Assets) • By End User (Manufacturing, Energy & Utilities, Oil & Gas, Transportation & Logistics, Healthcare, Government, IT & Telecom, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Oracle Corporation, SAP SE, Infor, Inc., Hexagon AB, Bentley Systems, Incorporated, AVEVA Group plc, Siemens AG, Rockwell Automation, Inc., ABB Ltd., Microsoft Corporation, IFS AB, AssetWorks LLC, Aptean, Inc., Ultimo Software Solutions BV, UpKeep Technologies, Inc., eMaint Enterprises, LLC, MRI Software LLC, Accruent, LLC, and IBM Maximo Application Suite |

Frequently Asked Questions

The Asset Management Market is expected to grow at a CAGR of 35.2% from 2026 to 2035.

The Asset Management Market was valued at USD 885.92 Billion in 2025.

Growing adoption of AI- and IoT-enabled predictive asset management, expanding global assets under management (AUM), increasing migration to cloud-based EAM platforms, rising integration of digital twin technologies, and evolving ESG compliance requirements are driving the Asset Management Market.

The Manufacturing segment dominated the Asset Management Market with the largest share in 2025.

North America dominated the Asset Management Market in 2025.

Get in Touch