Attack Surface Management Market Report Scope & Overview:

The Attack Surface Management Market was valued at USD 858.97 million in 2023 and is expected to reach USD 8247.40 million by 2032, growing at a CAGR of 28.60% from 2024-2032.

To Get more information on Attack Surface Management Market - Request Free Sample Report

This report includes insights on Threat Exposure Metrics, Security Vulnerability Trends, Automation & AI Use, Compliance & Regulatory Insights, and Supply Chain & Third-Party Risk Management.

The trend is fueled by the sophistication of digital ecosystems, rising cyber threats, and regulatory requirements. Organizations are making real-time risk assessment and anticipatory security measures a priority to address vulnerabilities. AI-powered automation improves monitoring and response, and compliance frameworks influence investment decisions. Third-party risk and supply chain security are also emerging as critical issues, which are making businesses extend their security posture beyond corporate networks. As more cybersecurity incidents occur, the demand for attack surface management solutions is projected to grow across business sectors.

U.S. Attack Surface Management Market was valued at USD 257.97 million in 2023 and is expected to reach USD 2461.36 million by 2032, growing at a CAGR of 28.48% from 2024-2032

Growth is fueled by evolving cyber threats, strict regulatory controls, and advancing digital transformation among industries. Deployment of cloud computing, IoT, and remote working models has been increasing attack surfaces, necessitating continuous monitoring and risk analysis. AI and automation are improving the capabilities of detecting threats, whereas government programs and compliance regulations challenge organizations to secure their defenses stronger. Moreover, increasing fears related to supply chain vulnerabilities are making investments in preventive cybersecurity solutions boost at a fast pace.

Attack Surface Management Market Dynamics

Drivers

-

Rising Cyber Threat Complexity and Stricter Regulations Accelerate Adoption of Attack Surface Management for Compliance and Security Resilience.

The increasing sophistication of cyber attacks, driven by advanced persistent threats (APTs), ransomware, and supply chain attacks, is compelling organizations to rethink their security postures. Conventional security controls are found wanting, and therefore, there is a need for real-time visibility into external attack surfaces. Meanwhile, regulatory authorities across the globe are imposing strict compliance frameworks, such as GDPR, HIPAA, and NIST standards, which are forcing enterprises to implement proactive security controls. Non-compliance attracts hefty monetary fines and reputation loss, leading to a greater uptake of cutting-edge Attack Surface Management (ASM) solutions. Companies are investing more in real-time threat insight, ongoing vulnerability scanning, and automated security processes to achieve compliance requirements while averting emerging cyber threats. With increased regulatory supervision and the shifting nature of cyber threats, firms are spending money on ASM for guaranteeing security resilience and compliance.

Restraints

-

High Implementation Costs and Resource Demands Hinder Adoption of Attack Surface Management Solutions Among Smaller Enterprises.

The implementation of Attack Surface Management (ASM) solutions requires significant financial outlays, posing a limitation for organizations with limited budgets. The purchase of sophisticated ASM tools, the recruitment of experienced cybersecurity experts, and the facilitation of smooth integration with current security infrastructures necessitate high capital expenditure. Small and medium-sized businesses usually find it difficult to set aside resources for such high-cost security solutions and, therefore, end up depending on less feature-rich alternatives. Moreover, the complexity involved in deploying and managing ASM platforms contributes to operational costs, further discouraging extensive use. Most organizations are also challenged by the inability to prove the return on investment, particularly when handling dynamic and changing attack surfaces. As cybersecurity budgets remain tight for smaller businesses, the cost-intensive nature of ASM solutions continues to be a limiting factor in their market penetration.

Opportunities

-

Collaborating with Managed Security Service Providers (MSSPs) Expands the Reach of Attack Surface Management Solutions for Organizations.

The increasing complexity of cybersecurity challenges has created a significant gap in expertise, especially among organizations with limited in-house resources. Partnering with Managed Security Service Providers (MSSPs) provides a specialized opportunity to fill this gap. MSSPs have the ability to incorporate Attack Surface Management (ASM) solutions into their services and offer organizations end-to-end cybersecurity packages that incorporate continuous monitoring, vulnerability management, and proactively detection of threats. It provides a way for companies lacking specialized cybersecurity teams to leverage sophisticated ASM solutions while leveraging the MSSP's experience. As organizations look for more comprehensive and economical security solutions, the increasing need for MSSP-led services puts ASM in the spotlight as an integral part of the larger cybersecurity ecosystem, enabling ASM providers to gain wider visibility and customer reach.

Challenges

-

Data Privacy and Regulatory Compliance Concerns Challenge the Effective Deployment of Attack Surface Management Solutions.

The gathering and analysis of large quantities of data in order to map and track attack surfaces can raise serious issues around data privacy. As companies use Attack Surface Management (ASM) solutions, they need to take care that sensitive data is not leaked in the process. Combining data from various sources, including cloud providers and third-party vendors, elevates the chances of breaching privacy laws such as GDPR or CCPA. This brings about a necessity for strong data protection controls to prevent legal consequences. Moreover, making ASM solutions industry-specific regulations compliant makes them more complicated to deploy. As data privacy regulations change with the evolution of cybersecurity frameworks, organizations have to keep pace with emerging data privacy laws, and hence compliance becomes an ongoing challenge. The urgency to protect privacy without compromising effective ASM might discourage some companies from implementing these solutions fully.

Attack Surface Management Market Segment Analysis

By Component

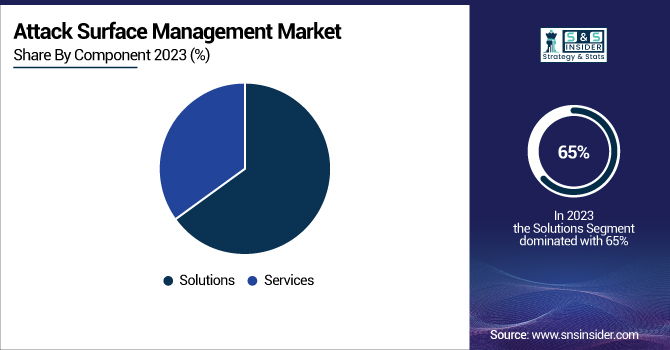

The Solutions segment held the largest share of Attack Surface Management (ASM) revenue at around 65% in 2023 owing to growing requirements for real-time and automated monitoring of digital assets. Solutions like vulnerability assessment, asset discovery, and risk management tools equip organizations with the requisite capabilities to continuously monitor and manage potential security threats on their growing attack surfaces. As companies focus more on anticipatory cybersecurity, ASM solutions have become a part of their security protocols, fueling revenue growth in this segment.

The Services segment is expected to expand at the fastest CAGR of approximately 30.09% during 2024-2032, fueled by the increasing need for expertise-based security services, including managed security, consulting, and incident response. As businesses are confronted with increasing cybersecurity threats and the complexity of attack surfaces, most are turning to third-party service providers to deploy and manage ASM solutions efficiently. This trend of outsourcing, along with the rising demand for customized security strategies, is driving the growth of the services segment.

By Enterprise Size

The Large Enterprises segment led the Attack Surface Management (ASM) market with the largest revenue share of approximately 69% in 2023 because of their vast digital infrastructure and more intricate attack surfaces. Larger organizations are exposed to increased cybersecurity threats because of their larger size, variability of operations, and greater susceptibility to advanced cyber attacks. Therefore, they are more inclined to spend on sophisticated ASM solutions to achieve thorough monitoring, risk management, and proactive threat detection throughout their large networks.

The SMEs segment is expected to grow at the fastest CAGR of approximately 30.07% during 2024-2032 due to growing awareness about the necessity for effective cybersecurity controls. As cyber threats evolve, small and medium enterprises are becoming more vulnerable and are realizing the importance of implementing ASM solutions to safeguard their digital assets. With the availability of cost-effective and scalable ASM options, SMEs are more inclined to adopt these solutions for enhanced security and compliance.

By End Use

The BFSI segment dominated the Attack Surface Management (ASM) market with the highest revenue share of about 30% in 2023 due to the critical importance of securing sensitive financial data. Banks, insurance firms, and other financial institutions manage vast amounts of personally identifiable information (PII) and financial transactions, making them prime targets for cyberattacks. As regulatory requirements and data protection laws become stricter, the BFSI sector invests heavily in ASM solutions to mitigate risks, comply with regulations, and ensure secure operations.

The Healthcare & Life Sciences segment is expected to grow at the fastest CAGR of about 31.48% from 2024-2032, fueled by the growing adoption of digital health technologies and the increasing volume of sensitive patient data. As healthcare organizations digitize their operations, the risk of cyberattacks escalates, making the need for comprehensive ASM solutions essential. The growing focus on safeguarding patient privacy, meeting compliance standards like HIPAA, and protecting critical healthcare infrastructure is driving rapid growth in this sector.

By Deployment

The Cloud segment dominated the Attack Surface Management (ASM) market with the highest revenue share of about 42% in 2023 and is expected to grow at the fastest CAGR of about 30.39% from 2024-2032, driven by the widespread adoption of cloud-based services across industries. As businesses increasingly migrate to the cloud to reduce infrastructure costs and enhance scalability, they face growing cybersecurity risks due to the expanding attack surface. Cloud environments require continuous monitoring and risk management, making ASM solutions crucial. The growing complexity of multi-cloud and hybrid cloud deployments, along with the rising need to secure sensitive data and comply with regulations, further fuels the demand for advanced ASM solutions. This trend is expected to accelerate as more organizations prioritize cloud security and adopt ASM to mitigate emerging threats.

Regional Analysis

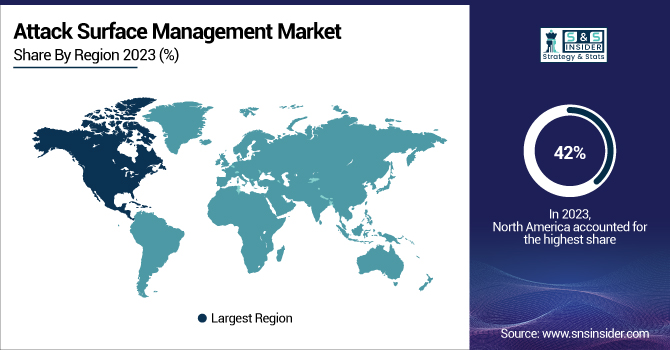

North America led the Attack Surface Management (ASM) market with the largest revenue share of approximately 42% in 2023 due to the region's high uptake of sophisticated technologies and robust regulatory environments. The presence of top cybersecurity vendors, combined with rising cyber threats against enterprises in various sectors, has prompted a greater emphasis on securing digital infrastructures. North American companies are at the forefront of embracing ASM solutions to meet stringent data protection regulations and reduce risks related to emerging cyber threats.

Asia Pacific is expected to grow at the fastest CAGR of approximately 30.39% during 2024-2032, led by swift digitalization and growing cybersecurity issues in developing economies. With the growth of e-commerce, cloud services, and IoT adoption, the region’s attack surfaces are expanding, making robust ASM solutions essential. Additionally, the increasing frequency of cyberattacks and the rising need for compliance with international cybersecurity standards are fueling the demand for ASM solutions in the Asia Pacific region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Cisco Systems, Inc. (Cisco Umbrella, Cisco SecureX)

-

CrowdStrike (Falcon Discover, Falcon Surface Optimization)

-

CyberArk Software Ltd. (CyberArk Privileged Access Security, CyberArk Application Access Manager)

-

International Business Machines Corporation (IBM QRadar, IBM Security Identity Governance and Administration)

-

Mandiant (Mandiant Advantage, Mandiant Threat Intelligence)

-

Microsoft (Microsoft Defender for Endpoint, Microsoft Sentinel)

-

Palo Alto Networks (Cortex XDR, Prisma Cloud)

-

Qualys, Inc. (Qualys Cloud Platform, Qualys Vulnerability Management)

-

Rapid7 (InsightVM, Metasploit)

-

Tenable, Inc. (Tenable.io, Tenable.sc)

-

JP Morgan (JPMorgan Cybersecurity, J.P. Morgan Intelligent Solutions)

-

Paypal (PayPal Fraud Protection, PayPal Advanced Fraud Tools)

-

Amazon (AWS Shield, Amazon GuardDuty)

-

Visa (Visa Advanced Authorization, Visa CyberSource)

-

Mastercard (Mastercard Identity Check, Mastercard Cybersecurity Solutions)

-

PhonPe (PhonePe Security, PhonePe Payment Gateway)

-

Razorpay (RazorpayX, Razorpay Payments)

-

Alibaba (Alibaba Cloud Anti-DDoS, Alibaba Cloud Web Application Firewall)

-

Stripe (Stripe Radar, Stripe Payments)

-

Adyen (Adyen Risk Management, Adyen Payments)

-

Block, Inc (Square Security, Cash App Protection)

-

FIS (FIS Fraud Detection, FIS Cybersecurity Solutions)

-

Global Payments (Global Payments Fraud Prevention, Global Payments Security Solutions)

-

Apple (Apple Pay Security, Apple ID Security)

-

Fiserv (Fiserv Fraud Risk Management, Fiserv Security Solutions)

-

Verifone (Verifone Cloud Security, Verifone Payments)

-

Paysafe (Paysafe Fraud Prevention, Paysafe Payment Gateway)

Recent Developments:

-

In 2024, Tenable Attack Surface Management introduces new filter options for the Last Metadata Change column, including date-based filters and integration with Azure Cloud Connector to add assets from Azure accounts.

-

Wallarm launched API Attack Surface Management (AASM) on August 22, 2024. This agentless technology helps organizations discover APIs, identify security gaps, and secure their entire API attack surface for enhanced protection.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 858.97 Million |

| Market Size by 2032 | US$ 8247.40 Million |

| CAGR | CAGR of 28.60% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (Cloud, On-premise) • By Enterprise Size (SMEs, Large Enterprises) • By End Use (BFSI, Healthcare & Life Sciences, Retail & E-commerce, IT & Telecommunications, Government & Public Sector, Manufacturing, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cisco Systems, Inc., CrowdStrike, CyberArk Software Ltd., International Business Machines Corporation, Mandiant, Microsoft, Palo Alto Networks, Qualys, Inc., Rapid7, Tenable, Inc., JP Morgan, Paypal, Amazon, Visa, Mastercard, PhonPe, Razorpay, Alibaba, Stripe, Adyen, Block, Inc, FIS, Global Payments, Apple, Fiserv, Verifone, Paysafe |

Frequently Asked Questions

Ans: North America dominated with a revenue share of about 42% in 2023.

Ans: The U.S. Attack Surface Management market was valued at USD 257.97 million in 2023.

Ans: The Services segment is expected to grow at the fastest CAGR of about 30.09% from 2024 to 2032.

Ans: The Solutions segment dominated with a revenue share of about 65% in 2023.

Ans: Attack Surface Management Market was valued at USD 858.97 million in 2023 and is expected to reach USD 8247.40 million by 2032, growing at a CAGR of 28.60% from 2024-2032

Get in Touch