Automotive Lubricants Market Report Scope & Overview:

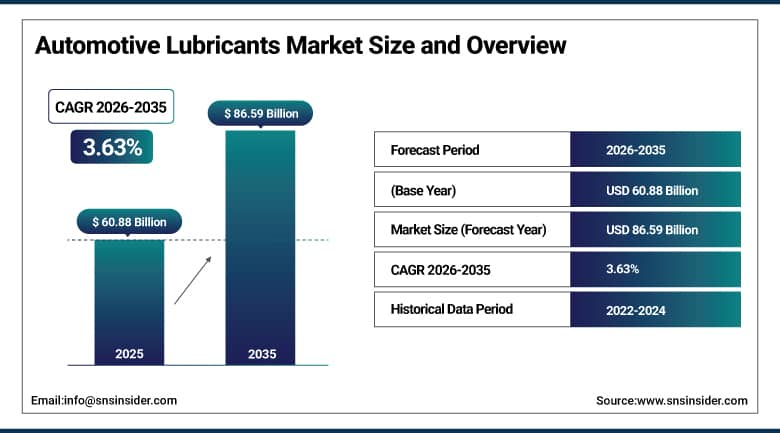

The Automotive Lubricants Market was valued at USD 60.88 billion in 2025 and is expected to reach USD 86.59 billion by 2035, growing at a CAGR of 3.63% from 2026 to 2035.

The demand for automotive lubricants remains stable across the globe, fueled by an increased number of operational vehicles, increasing industrial activities, and increasing awareness about maintenance of engines and improved fuel economy. Engine oil, transmission fluid, hydraulic oil, grease, and coolant are the key products in the automotive lubricants market. Passenger vehicles, commercial vehicles, two wheelers, and off highway machinery have been consuming the above mentioned products in all major regions across the world. There is gradual trend towards synthetic and semi-synthetic oils due to stringent performance requirements by automakers and evolving emission regulations. Growth in electric vehicles has forced automotive lubricant market manufacturers to develop specialized fluids like thermal management fluids and e-transmission oils for EVs.

Shell launched a new range of fully synthetic engine oils under the Helix Ultra brand in 2025, specifically formulated to meet the latest ACEA and API specifications for modern turbocharged and hybrid petrol engines. The formulations are designed to reduce oil consumption, support longer drain intervals, and improve cold-start performance in a wide range of climate conditions. Shell is continuing to expand its synthetic and EV-compatible lubricant portfolio as original equipment manufacturers shift toward tighter viscosity grades and lower-friction specifications across new vehicle platforms worldwide.

Market Size and Forecast:

-

Market Size 2026E: USD 62.82 Billion

-

Market Size 2035: USD 86.59 Billion

-

CAGR (2026 – 2035): 3.63%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Automotive Lubricants Market - Request Free Sample Report

Automotive Lubricants Market Trends:

-

Increasing adoption of fuel-efficient and low-viscosity engine oils is gaining pace as automakers push to meet stricter emission targets in North America, Europe, and Asia Pacific markets.

-

Synthetic and semi-synthetic lubricants are taking a growing share of the product mix as consumers and fleet operators look for longer drain intervals and better engine protection under demanding conditions.

-

Growth in the commercial vehicle segment, particularly heavy trucks and light commercial vehicles, is supporting stable demand for transmission oils, hydraulic fluids, and greases across major freight and construction markets.

-

The expansion of two-wheeler and off-highway vehicle fleets across developing markets in Southeast Asia, South Asia, and Latin America is creating sustained volume demand for entry-level and mid-range lubricant products.

-

EV-compatible lubricants, including e-fluids and dielectric coolants, are drawing increasing investment from major lubricant producers looking to address the needs of hybrid and battery-electric vehicle platforms as electrification gradually expands.

U.S. Automotive Lubricants Market Outlook:

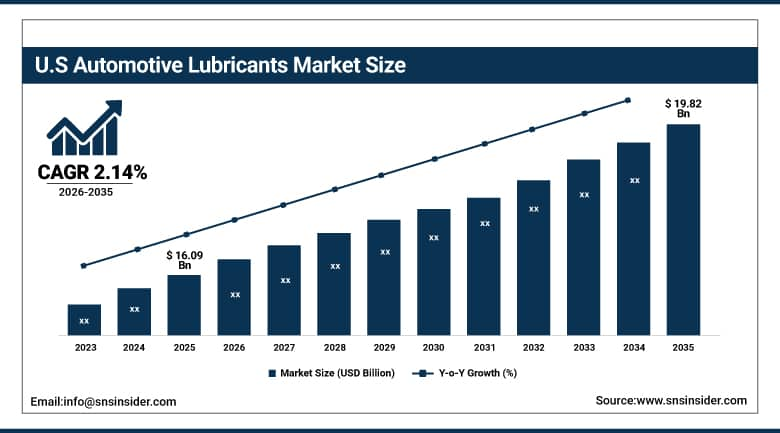

The U.S. Automotive Lubricants Market was valued at USD 16.09 billion in 2025 and is expected to reach USD 19.82 billion by 2035 at a CAGR of 2.14%.

The United States remains one of the largest individuals for automotive lubricants market in the world, underpinned by a massive installed vehicle base that spans passenger cars, pickup trucks, heavy commercial vehicles, and off-highway equipment. Engine oil accounts for the biggest share of sales, and the aftermarket channel dominates because of the sheer number of independent service workshops, quick-lube chains, and do-it-yourself consumers who purchase lubricants outside of dealerships. The continued popularity of larger displacement engines and towing-capable vehicles in the U.S. means that demand for high-performance and heavy-duty automotive lubricants market grades remains above the global average.

U.S. based lubricant producers are investing in next-generation additive technologies and re-refining capabilities to support both performance and sustainability goals. The growth of re-refined base oils is gaining regulatory and commercial support as corporations look to reduce their environmental footprint and as state governments introduce initiatives to promote used oil collection and recycling. This trend is expected to continue through the forecast period, with re-refined and bio-based oil products gradually capturing a larger portion of the U.S. market alongside conventional mineral and synthetic grades.

Market Segment Analysis:

-

By Product Type, Engine Oil dominated with approximately 41.26% revenue share in 2025; Transmission & Gear Oil is expected to be the fastest-growing product segment at approximately 4.42% CAGR from 2026 to 2035.

-

By Vehicle Type, Passenger Cars dominated with approximately 46.83% revenue share in 2025; Off-Highway Vehicles are expected to be the fastest-growing vehicle segment at approximately 6.17% CAGR from 2026 to 2035.

-

By Base Oil Type, Mineral Oil dominated with approximately 52.47% revenue share in 2025; Synthetic Oil is expected to be the fastest-growing base oil segment at approximately 6.32% CAGR from 2026 to 2035.

-

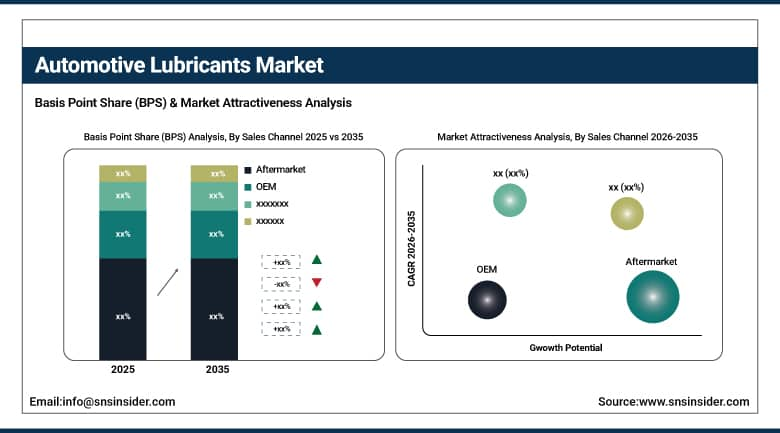

By Sales Channel, Aftermarket dominated with approximately 61.36% revenue share in 2025; OEM is expected to be the fastest-growing sales channel segment at approximately 4.31% CAGR from 2026 to 2035.

By Sales Channel, Aftermarket dominating while OEM emerging as the fastest-growing

The aftermarket channel generated approximately 61.36% of revenue in 2025, reflecting the large and diverse ecosystem of independent workshops, retail outlets, quick-lube chains, and fleet maintenance depots that serve vehicles throughout their operational life. Aftermarket sales are supported by strong brand loyalty among professional mechanics and a well-established distribution infrastructure in every major market.

The OEM channel is expected to post the highest CAGR of around 4.31% from 2026 to 2035 as automakers increasingly specify factory-fill and first-service lubricants through exclusive supply agreements. Vehicle complexity and the need for manufacturer-approved fluids in modern transmissions, cooling systems, and hybrid drivetrains are giving OEM channel partners a more durable foothold than in previous generations.

By Product Type, Engine Oil dominating while Transmission & Gear Oil emerging as the fastest-growing

Engine oil holds a share of 41.26% in the market revenue in 2025 as a result of its widespread applicability to safeguarding internal combustion engines in automobiles, trucks, motorcycles, and agricultural vehicles. Passenger vehicle motor oils and heavy-duty diesel engine oils form the majority of the engine oil market. The high potential of the segment arises from its replacement nature due to mandatory intervals for changing the oil, besides being invested in by various additive and base oil providers who compete based on performance criteria.

Transmission and gear oil is anticipated to register the highest CAGR of about 4.42% in the forecast period of 2026-2035 owing to the increased use of sophisticated technologies in modern automatic and dual-clutch transmission systems, which necessitate different types of oils than traditional gearboxes do. The increased penetration of automatic transmissions in Asia Pacific and Latin American regions, where manual transmissions had long been dominant, is a major factor that influences its relatively high CAGR.

By Vehicle Type, Passenger Cars dominating while Off-Highway Vehicles emerging as the fastest-growing

The passenger car category accounted for about 46.83% of the total market value in 2025 owing to the sheer number of passenger cars in the global market, despite their rising presence in developed nations. Demand for more oil changes, use of synthetic oil, and rise in consumer awareness about engine oils would result in healthy demand for engine oils among the segment.

The off-highway vehicles segment is anticipated to register the highest growth rate of around 6.17% from 2026 to 2035, owing to the advancements in the fields of construction, mining, and agriculture in developing economies. Vehicles used in tough conditions consume engine oil faster compared to road vehicles, thereby providing stable opportunities for growth.

By Base Oil Type, Mineral Oil dominating while Synthetic Oil emerging as the fastest-growing

Mineral oils were responsible for roughly 52.47% of the market in 2025, but their share is slowly dropping as synthetic lubricants continue to make more inroads, as they are currently the most economically efficient choice available in older vehicles. This notwithstanding, the volume is still going to be high considering that the products find application in economically driven markets.

The synthetic lubricants market is set to witness steady growth at a CAGR of about 6.32% between 2026 and 2035 on account of the rising contribution made by modern vehicles with tighter tolerances, turbocharging technology, and higher drain intervals. In North America and Europe, synthetic oil has already moved from a premium niche to a mainstream product in many categories. Its growth trajectory in Asia Pacific and Latin America will be an important driver of market premiumization over the forecast period.

Regional Insights:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

81% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

49% |

|

Middle East & Africa |

Saudi Arabia |

31% |

|

Latin America |

Brazil |

44% |

Asia Pacific Automotive Lubricants Market Growth Outlook

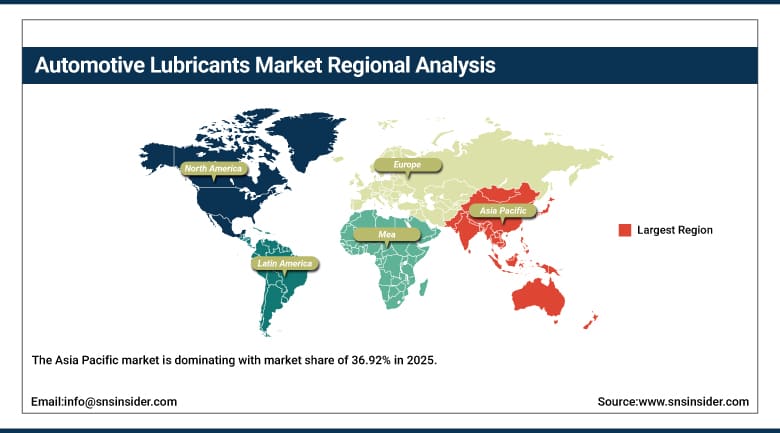

The Asia Pacific market is dominating with market share of 36.92% in 2025, whereas it is also likely to record the highest rate of growth with a CAGR of approximately 4.56% during 2026 to 2035 attributed to the rapid pace of urbanization, increased automotive manufacturing, and increasing car and truck ownership in China, India, Japan, South Korea, and other countries in Southeast Asia. China leads the market due to the presence of large number of commercial vehicles in the country, robust automotive manufacturing sector, and the trend among consumers towards premium synthetic lubricants. Growth in the number of two-wheelers in South and Southeast Asia, transportation activity, and use of performance-based engine oils are driving the market growth in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Automotive Lubricants Market Demand Analysis

The North America segment thereby being one of the two major regional segments along with the Asia-Pacific segment. The US dominates the demand from the region, whereas Canada is also a notable contributor to the market growth. It is pertinent to note that the vehicle population in North America is dominated by pickups, sports utility vehicles (SUVs), and commercial vehicles, all of which consume a larger quantity of lubricants than passenger cars. The North American region is notable for its robust aftermarket distribution, featuring a vast network of quick-lube centers and auto-parts stores.

Europe Automotive Lubricants Industry Trends

The automotive lubricants market in Europe is influenced by strict emission regulations and increasing demand for low-viscosity, long-life synthetic lubricant products across the automotive sector. European automakers and lubricant manufacturers are increasingly focusing on advanced lubricant technologies that improve engine efficiency, reduce emissions, and support hybrid vehicle performance. Germany continues to play a major role in regional growth because of its strong automotive manufacturing industry and high consumer spending on vehicle maintenance products. France, the United Kingdom, and Italy also contribute significantly to regional demand. Increasing adoption of plug-in hybrid vehicles across Western Europe is further driving demand for specialized lubricants designed for hybrid engines and electrified automotive systems.

Middle East & Africa and Latin America Automotive Lubricants Market Insights

There is consistent growth in the automotive lubricants market in the Middle East & Africa due to the extensive use of vehicles in high temperatures, where lubricants tend to deteriorate quickly, necessitating the need for more frequent replacements. Infrastructure development, commercial transportation growth, and industrial activities taking place in countries such as those in the Gulf region and Sub-Saharan Africa have been contributing significantly to the growth in demand in the market. In addition, Saudi Arabia has been one of the major contributors to the growth due to the high rate of automotive activity and industrial development. On the other hand, there is consistent growth in the automotive lubricants market in Latin America due to increased ownership of vehicles, commercial transportation, and branded lubricants.

Growth Drivers: Expanding global vehicle fleet and rising demand for high-performance lubricants supporting market growth

The most important driver of growth in auto lubricants is the continuous increase in the size of the world vehicle population especially in the Asia Pacific region, Latin America, and the Middle East. Due to higher disposable incomes in these regions, people are buying more cars which will need more frequent lubrication. With the rise in the number of cars being used and the longevity of existing ones, there will be increased demand for lubricants that will be used in the maintenance of these automobiles. Even though demand may not be increasing at a high pace, the trend towards synthetics and semi-synthetics is adding dollars to sales.

The major lubricant suppliers such as Shell, ExxonMobil, and Castrol have been putting emphasis on research and development of products that will be able to meet the ever-changing demands of the market from turbocharged engines to automatic transmissions as well as hybrids. The expansion in production capacity of these lubricants is currently being carried out in many parts of Asia and the Middle East with an aim to increase efficiency and reduce time. In addition, strategic collaborations with automakers for OEM supply and first fill have become an integral source of income.

Restraints: Gradual shift toward electric vehicles and rising price pressure on conventional lubricants

The longer-term shift towards electric vehicles, which do not utilize engine oil and need much lower volumes of lubricant than ICE-based vehicles, will present the biggest structural headwind for the automotive lubricants market. Though the trend is forecasted to develop gradually and in a non-uniform way across regions, it will negatively impact volume growth of lubricants in the passenger car subsegment mainly in Western Europe, North America, and some parts of East Asia, which have already shown high penetration of electric vehicles. In the shorter run, unfavorable margins caused by unstable pricing on base oils and growing competition from private labels in the automotive aftermarket channel affect certain categories of lubricants.

Opportunities: Growing demand for bio-based lubricants and EV-compatible fluid formulations

Commercialization of bio-lubricants and re-refining of lubricants continues to increase as regulations are tightened and companies make more stringent sustainability goals, which will encourage consumers to explore other options apart from mineral lubricants. Biodegradable hydraulic and gear oils have gained market traction in those regions with specific biodegradable requirements; examples include forestry, agricultural operations, and construction close to bodies of water. With increasing vehicle electrification, a new category of demand is developing for lubricants producers, namely, e-fluids for lubricating and cooling electric motors, thermal management fluids for batteries, and lubricating greases for electric drive components. Early adoption of this trend could be very profitable for those organizations that can adapt their product offering in time for the growth in sales of hybrid and electric vehicles.

Equipment makers and fleets in North America and Europe are demonstrating more interest in bio-degradable and bio-hydraulic fluids that adhere to performance and environmental standards. Bio-hydraulic fluid is gaining traction, leading to the willingness of specialty chemicals companies and lubricants manufacturers to invest in their production in order to earn higher margins in an area where prices are less sensitive and regulations are favorable.

Recent Developments:

-

May, 2026: Shell expanded its Helix Ultra synthetic engine oil range to cover the latest vehicle platforms entering production across Asian markets, with new formulations targeting hybrid-electric passenger cars and light commercial vehicles operating in high-temperature urban environments.

-

2026: ExxonMobil continued to expand its Mobil 1 product range for electric and hybrid vehicles while reinforcing supply agreements with major automotive OEMs in Europe and North America, focusing on delivering factory-fill lubricants aligned with the latest generation of turbocharged and electrified powertrain specifications.

-

June, 2025: TotalEnergies partnered with a leading European truck manufacturer to supply a dedicated range of heavy-duty engine and transmission fluids for the next generation of long-haul commercial vehicles, designed to support extended drain intervals and meet the latest European emission regulations.

Automotive Lubricants Market Key Players are:

-

Shell plc

-

ExxonMobil Corporation

-

TotalEnergies SE

-

BP plc (Castrol)

-

Chevron Corporation

-

Valvoline Inc.

-

Fuchs Petrolub SE

-

Idemitsu Kosan Co., Ltd.

-

Lukoil

-

Petro-Canada Lubricants Inc.

-

Repsol S.A.

-

Indian Oil Corporation Ltd.

-

China National Petroleum Corporation (CNPC)

-

Sinopec Limited

-

Motul S.A.

-

Liqui-Moly GmbH

-

Quaker Houghton

-

Petrobras Distribuidora

-

Kluber Lubrication

Automotive Lubricants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 60.88 Billion |

| Market Size by 2035 | USD 86.59 Billion |

| CAGR | CAGR of 3.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Engine Oil, Transmission & Gear Oil, Hydraulic Fluid, Grease, Coolants & Brake Fluids) • By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-Wheelers, Off-Highway Vehicles) • By Base Oil Type (Mineral Oil, Synthetic Oil, Semi-synthetic Oil, Bio-based Oil) • By Sales Channel (OEM, Aftermarket) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Shell plc, Exxon Mobil Corporation, BP p.l.c., Chevron Corporation, TotalEnergies SE, Valvoline Inc., FUCHS SE, Castrol Limited, Petroliam Nasional Berhad (PETRONAS), Idemitsu Kosan Co., Ltd., Phillips 66 Company, Indian Oil Corporation Ltd., Sinopec Corp., ENEOS Holdings, Inc., Motul S.A., Repsol S.A., Gulf Oil International Ltd., Amsoil Inc., SK Enmove Co., Ltd., Liqui Moly GmbH |

Frequently Asked Questions

The Automotive Lubricants Market is expected to grow at a CAGR of 3.63% from 2026 to 2035.

The Automotive Lubricants Market was valued at USD 60.88 billion in 2025.

Engine Oil dominated the market in 2025 with approximately 41.26% of revenues.

Passenger Cars dominated the market in 2025 with approximately 46.83% of revenues.

Asia Pacific dominated the Automotive Lubricants Market in 2025 with approximately 36.92% of global revenues.

Get in Touch