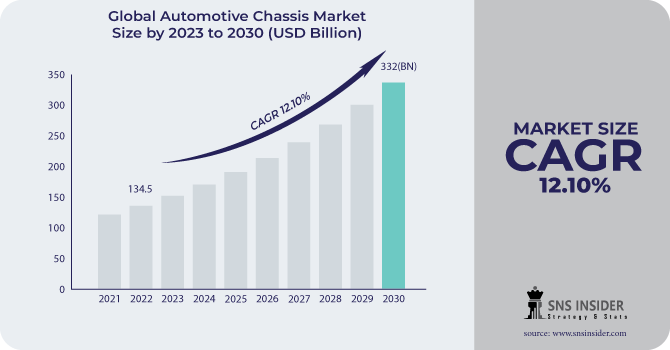

The Automotive Chassis Market size was valued at USD 145.6 Bn in 2023 and is expected to reach USD 365.68 Bn by 2031 and grow at a CAGR of 12.2% over the forecast period of 2024-2031.

Traditional body-on-frame construction uses a robust steel or other material frame as the chassis. The vehicle's weight is supported by this frame, which also serves as a mounting surface for other parts. Unibody construction is frequently used in contemporary automobiles, particularly in crossovers and passenger cars. The chassis and body are combined into a single component in this design, which reduces weight and increases rigidity. Most current autos frequently have this. The vehicle's suspension system is mounted to the chassis. These factors determine the vehicle's stability, handling, and ride comfort. The automotive industry growth rate is approximately matching up with 50% YoY growth compared to other industries which is increasing the demand.

The engine and gearbox can be mounted on the chassis. To lessen noise and increase overall driving comfort, these mounts aid in keeping the powertrain in place and absorbing vibrations. To enable steering and braking control, the steering column and brake components are normally fastened to the chassis. The chassis frequently provides spaces for the exhaust system and fuel tank mounting. Front and rear crumple zones are frequently used in contemporary chassis designs. These parts are made to distort during a collision in a regulated way, absorbing energy, and safeguarding occupants. The vehicle's safety cage, which is intended to safeguard passengers, is likewise built on the chassis.

The chassis layout affects how the vehicle's weight is distributed, which has an impact on how it handles and balances. In order to protect passengers in the event of an accident, chassis components must be constructed to meet safety standards and have sufficient structural integrity. Steel is a typical choice for chassis because of its strength and longevity. To minimise weight, some vehicles may use aluminium or composite materials.

Driver

The growth of automotive industry and the rising demand

A market size of 2.86 trillion dollars was generated by the automotive manufacturing industry in 2021, and in 2022 it is anticipated to increase. The sale of new automobiles is the main factor influencing chassis demand. The demand for chassis increases along with the growth of the automotive industry and rising customer demand for automobiles, trucks, and other vehicles. On the other hand, demand for chassis may fall during economic downturns or market contractions. Chassis demand may be impacted by changes in consumer tastes and market trends. For instance, the demand for varied types and numbers of chassis is influenced by the increased popularity of SUVs and crossover vehicles, which frequently require different chassis designs than conventional sedans.

Restrain

The global disruptions which are causing backlogs and volatility.

Opportunity

The rising trends in automotive industry and the rising sales percentage post global disruptions.

The need for automobiles in developing nations like China, India, and other regions of Southeast Asia has significantly boosted the market for chassis. The demand for cars is increasing as these economies expand and more people can afford them.

Challenge

The high cost and rising geopolitical pressures.

A recession's most immediate effects include a decline in consumer spending. The consumer’s spending is decreased by 6% people often put off large purchases like cars during economic downturns. Because chassis systems and components are essential to the 12% production of vehicles, lower production volumes caused by decreased demand for vehicles have an impact on the market for them. Automakers frequently undertake production cuts and plant closures as a response to declining demand. Suppliers and manufacturers in the chassis sector may experience reduced demand for chassis materials and components as a result. Recessions can cause supply chain disruptions the companies have experienced 30% loss because of backlogs which has disrupted their financial aspects in the automotive industry, which can delay the delivery of materials and chassis parts. Some suppliers may even have financial issues as they fight to sustain production levels.

Impact of Russia Ukraine War:

Steel, aluminium, and electrical components, among other raw materials and parts needed in the production of automobiles, are all significantly imported from Ukraine. Any interruptions in the flow of these materials from Ukraine could complicate the supply chains for the producers of chassis and autos and possibly postpone production. Supply chain interruptions, particularly those that influence raw materials, can lead to an increase in the cost of the components required to make chassis. Because of this, chassis makers may incur greater manufacturing expenses, which could result in increased vehicle prices. As a result, new automobile prices may rise for consumers. The cost has increase by 10% which has led to several pricing pressures on OEMs. Also, the transportation prices have got influenced by 25% because of the war.

By Chassis Type

Non-Conventional

Modular

Conventional

By Vehicle Type

Passenger Car

Commercial Car

Electric Vehicles

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Regional Analysis:

The automotive market in North America, and particularly the United States, is developed. Light vehicles, SUVs, and pickup trucks are in high demand in the US and frequently have distinctive chassis designs. These nations are important centres to produce car chassis for both local and international markets. Chassis design is influenced by the strict safety and emissions regulations in the North American market.

Europe will be the region with the second largest share, the automobile sector in this area is well-established, and safety and environmental requirements are highly prioritised. Efficiency and pollution reduction are frequently given priority in chassis designs. A few nations in this region, especially Slovakia and Hungary, have emerged as major hubs to produce automobile chassis. In certain areas, lower labour costs may be an advantage.

APAC is the region with the highest CAGR growth rate because, China is the largest automotive market in the world and a major producer of automobiles and chassis parts. From little vehicles to large trucks, a variety of vehicle types are available on the Chinese market. These two nations are renowned for their technological advances in the automotive industry i.e., Japan and South Korea. For their automobiles, Japanese and South Korean automakers frequently use cutting-edge materials and chassis designs. Small and tiny automobiles dominate the Indian automotive market. Designing a chassis frequently puts durability and cost effectiveness first.

The major key players are Schaeffler Technologies, Hyundai Motor, Aisin Seiki, Mahna International, Continental Ag, Tower International, CIE Automotive, REE automotive, Benteler International AG, ZF Friedrichshafen AG and others players.

Hyundai Motor; The company has stated investing heavily in U.S. for the inhouse production of parts, this will reduce the dependency factor.

Continental AG: The company is very much focused on improving the mobility services and aligning with the climate sustainability goals of government.

| Report Attributes | Details |

| Market Size in 2023 | US$ 145.6 Billion |

| Market Size by 2031 | US$ 365.68 Billion |

| CAGR | CAGR of 12.2% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chassis Type (Non-conventional, Modular, Conventional) • By Vehicle Type (Passenger Car, Commercial Car, Electric Vehicles) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Schaeffler Technologies, Hyundai Motor, Aisin Seiki, Mahna International, Continental Ag, Tower International, CIE Automotive, REE automotive, Benteler International AG, ZF Friedrichshafen AG |

| Key Drivers | • The growth of automotive industry and the rising demand |

| Market Opportunity | • The rising trends in automotive industry and the rising sales percentage post global disruptions. |

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact Of Russia Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Recreational Vehicle Market Segmentation, By Chassis Type

9.1 Introduction

9.2 Trend Analysis

9.3 Non-Conventional

9.4 Modular

9.5 Conventional

10. Recreational Vehicle Market Segmentation, By Vehicle Type

10.1 Introduction

10.2 Trend Analysis

10.3 Passenger Car

10.4 Commercial Vehicles

10.5 Electric Vehicles

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 Trend Analysis

11.2.2 North America Recreational Vehicle Market by Country

11.2.3 North America Recreational Vehicle Market By Chassis Type

11.2.4 North America Recreational Vehicle Market By Vehicle Type

11.2.5 USA

11.2.5.1 USA Recreational Vehicle Market By Chassis Type

11.2.5.2 USA Recreational Vehicle Market By Vehicle Type

11.2.6 Canada

11.2.6.1 Canada Recreational Vehicle Market By Chassis Type

11.2.6.2 Canada Recreational Vehicle Market By Vehicle Type

11.2.7 Mexico

11.2.7.1 Mexico Recreational Vehicle Market By Chassis Type

11.2.7.2 Mexico Recreational Vehicle Market By Vehicle Type

11.3 Europe

11.3.1 Trend Analysis

11.3.2 Eastern Europe

11.3.2.1 Eastern Europe Recreational Vehicle Market by Country

11.3.2.2 Eastern Europe Recreational Vehicle Market By Chassis Type

11.3.2.3 Eastern Europe Recreational Vehicle Market By Vehicle Type

11.3.2.4 Poland

11.3.2.4.1 Poland Recreational Vehicle Market By Chassis Type

11.3.2.4.2 Poland Recreational Vehicle Market By Vehicle Type

11.3.2.5 Romania

11.3.2.5.1 Romania Recreational Vehicle Market By Chassis Type

11.3.2.5.2 Romania Recreational Vehicle Market By Vehicle Type

11.3.2.6 Hungary

11.3.2.6.1 Hungary Recreational Vehicle Market By Chassis Type

11.3.2.6.2 Hungary Recreational Vehicle Market By Vehicle Type

11.3.2.7 Turkey

11.3.2.7.1 Turkey Recreational Vehicle Market By Chassis Type

11.3.2.7.2 Turkey Recreational Vehicle Market By Vehicle Type

11.3.2.8 Rest of Eastern Europe

11.3.2.8.1 Rest of Eastern Europe Recreational Vehicle Market By Chassis Type

11.3.2.8.2 Rest of Eastern Europe Recreational Vehicle Market By Vehicle Type

11.3.3 Western Europe

11.3.3.1 Western Europe Recreational Vehicle Market by Country

11.3.3.2 Western Europe Recreational Vehicle Market By Chassis Type

11.3.3.3 Western Europe Recreational Vehicle Market By Vehicle Type

11.3.3.4 Germany

11.3.3.4.1 Germany Recreational Vehicle Market By Chassis Type

11.3.3.4.2 Germany Recreational Vehicle Market By Vehicle Type

11.3.3.5 France

11.3.3.5.1 France Recreational Vehicle Market By Chassis Type

11.3.3.5.2 France Recreational Vehicle Market By Vehicle Type

11.3.3.6 UK

11.3.3.6.1 UK Recreational Vehicle Market By Chassis Type

11.3.3.6.2 UK Recreational Vehicle Market By Vehicle Type

11.3.3.7 Italy

11.3.3.7.1 Italy Recreational Vehicle Market By Chassis Type

11.3.3.7.2 Italy Recreational Vehicle Market By Vehicle Type

11.3.3.8 Spain

11.3.3.8.1 Spain Recreational Vehicle Market By Chassis Type

11.3.3.8.2 Spain Recreational Vehicle Market By Vehicle Type

11.3.3.9 Netherlands

11.3.3.9.1 Netherlands Recreational Vehicle Market By Chassis Type

11.3.3.9.2 Netherlands Recreational Vehicle Market By Vehicle Type

11.3.3.10 Switzerland

11.3.3.10.1 Switzerland Recreational Vehicle Market By Chassis Type

11.3.3.10.2 Switzerland Recreational Vehicle Market By Vehicle Type

11.3.3.11 Austria

11.3.3.11.1 Austria Recreational Vehicle Market By Chassis Type

11.3.3.11.2 Austria Recreational Vehicle Market By Vehicle Type

11.3.3.12 Rest of Western Europe

11.3.3.12.1 Rest of Western Europe Recreational Vehicle Market By Chassis Type

11.3.2.12.2 Rest of Western Europe Recreational Vehicle Market By Vehicle Type

11.4 Asia-Pacific

11.4.1 Trend Analysis

11.4.2 Asia Pacific Recreational Vehicle Market by Country

11.4.3 Asia Pacific Recreational Vehicle Market By Chassis Type

11.4.4 Asia Pacific Recreational Vehicle Market By Vehicle Type

11.4.5 China

11.4.5.1 China Recreational Vehicle Market By Chassis Type

11.4.5.2 China Recreational Vehicle Market By Vehicle Type

11.4.6 India

11.4.6.1 India Recreational Vehicle Market By Chassis Type

11.4.6.2 India Recreational Vehicle Market By Vehicle Type

11.4.7 Japan

11.4.7.1 Japan Recreational Vehicle Market By Chassis Type

11.4.7.2 Japan Recreational Vehicle Market By Vehicle Type

11.4.8 South Korea

11.4.8.1 South Korea Recreational Vehicle Market By Chassis Type

11.4.8.2 South Korea Recreational Vehicle Market By Vehicle Type

11.4.9 Vietnam

11.4.9.1 Vietnam Recreational Vehicle Market By Chassis Type

11.4.9.2 Vietnam Recreational Vehicle Market By Vehicle Type

11.4.10 Singapore

11.4.10.1 Singapore Recreational Vehicle Market By Chassis Type

11.4.10.2 Singapore Recreational Vehicle Market By Vehicle Type

11.4.11 Australia

11.4.11.1 Australia Recreational Vehicle Market By Chassis Type

11.4.11.2 Australia Recreational Vehicle Market By Vehicle Type

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Recreational Vehicle Market By Chassis Type

11.4.12.2 Rest of Asia-Pacific Recreational Vehicle Market By Vehicle Type

11.5 Middle East & Africa

11.5.1 Trend Analysis

11.5.2 Middle East

11.5.2.1 Middle East Recreational Vehicle Market by Country

11.5.2.2 Middle East Recreational Vehicle Market By Chassis Type

11.5.2.3 Middle East Recreational Vehicle Market By Vehicle Type

11.5.2.4 UAE

11.5.2.4.1 UAE Recreational Vehicle Market By Chassis Type

11.5.2.4.2 UAE Recreational Vehicle Market By Vehicle Type

11.5.2.5 Egypt

11.5.2.5.1 Egypt Recreational Vehicle Market By Chassis Type

11.5.2.5.2 Egypt Recreational Vehicle Market By Vehicle Type

11.5.2.6 Saudi Arabia

11.5.2.6.1 Saudi Arabia Recreational Vehicle Market By Chassis Type

11.5.2.6.2 Saudi Arabia Recreational Vehicle Market By Vehicle Type

11.5.2.7 Qatar

11.5.2.7.1 Qatar Recreational Vehicle Market By Chassis Type

11.5.2.7.2 Qatar Recreational Vehicle Market By Vehicle Type

11.5.2.8 Rest of Middle East

11.5.2.8.1 Rest of Middle East Recreational Vehicle Market By Chassis Type

11.5.2.8.2 Rest of Middle East Recreational Vehicle Market By Vehicle Type

11.5.3 Africa

11.5.3.1 Africa Recreational Vehicle Market by Country

11.5.3.2 Africa Recreational Vehicle Market By Chassis Type

11.5.3.3 Africa Recreational Vehicle Market By Vehicle Type

11.5.2.4 Nigeria

11.5.2.4.1 South Africa Recreational Vehicle Market By Chassis Type

11.5.2.4.2 South Africa Recreational Vehicle Market By Vehicle Type

11.5.2.5 South Africa

11.5.2.5.1 South Africa Recreational Vehicle Market By Chassis Type

11.5.2.5.2 South Africa Recreational Vehicle Market By Vehicle Type

11.5.2.6 Rest of Africa

11.5.2.6.1 Rest of Africa Recreational Vehicle Market By Chassis Type

11.5.2.6.2 Rest of Africa Recreational Vehicle Market By Vehicle Type

11.6 Latin America

11.6.1 Trend Analysis

11.6.2 Latin America Recreational Vehicle Market by Country

11.6.3 Latin America Recreational Vehicle Market By Chassis Type

11.6.4 Latin America Recreational Vehicle Market By Vehicle Type

11.6.5 Brazil

11.6.5.1 Brazil Recreational Vehicle Market By Chassis Type

11.6.5.2 Brazil Recreational Vehicle Market By Vehicle Type

11.6.6 Argentina

11.6.6.1 Argentina Recreational Vehicle Market By Chassis Type

11.6.6.2 Argentina Recreational Vehicle Market By Vehicle Type

11.6.7 Colombia

11.6.7.1 Colombia Recreational Vehicle Market By Chassis Type

11.6.7.2 Colombia Recreational Vehicle Market By Vehicle Type

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Recreational Vehicle Market By Chassis Type

11.6.8.2 Rest of Latin America Recreational Vehicle Market By Vehicle Type

12. Company Profiles

12.1 Schaeffler Technologies

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 Hyundai Motor

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 Aisin Seiki

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 Mahna International

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 Continental Ag

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 Tower International

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 CIE Automotive

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 REE automotive

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 Benteler International AG

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 ZF Friedrichshafen AG

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

12.10.5 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. USE Cases And Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Automotive Actuator Market size was valued at USD 27.77 Bn in 2022 and is expected to reach USD 47.01 Bn by 2030 and grow at a CAGR of 6.8% over the forecast period of 2023-2030.

The All-Wheel Drive Market Size grow at a CAGR of 8.0% over the forecast period 2024-2031.

The Automotive Biometric Market Size was valued at USD 7.30 billion in 2023 and is expected to reach USD 11.64 billion by 2031 and grow at a CAGR of 6% over the forecast period 2024-2031.

The Automotive Collision Avoidance System Market size was valued at USD 58.05 billion in 2023 and is expected to reach USD 115.67 billion by 2031 and grow at a CAGR of 9.22% over the forecast period 2024-2031.

The Automotive Electronics Sensor Aftermarket Market size was valued at USD 294.14 billion in 2023 and is expected to reach USD 502.79 billion by 2031 and grow at a CAGR of 7.09% over the forecast period 2024-2031.

The Self-Driving Car And Trucks Market had a worth of $1.52 billion in 2022 and is projected to attain $3.14 billion by 2030, experiencing a Compound Annual Growth Rate (CAGR) of 9.5% during the estimated timeframe from 2023 to 2030

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd