Automotive PCB Market Report Scope & Overview:

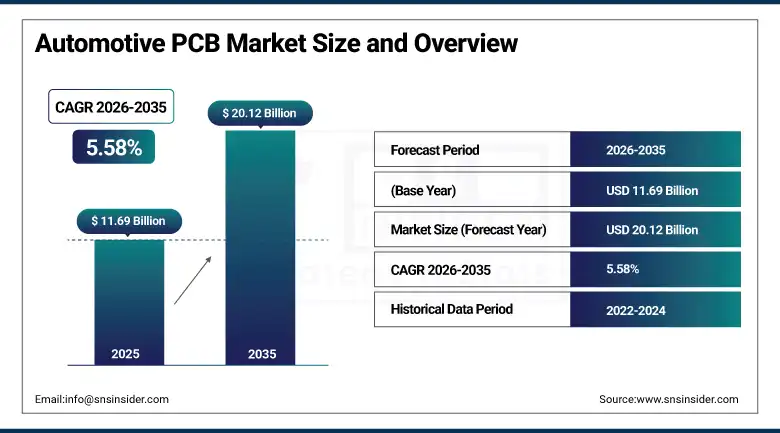

The Automotive PCB Market size was valued at USD 11.69 Billion in 2025 and is expected to reach USD 20.12 Billion by 2035, growing at a CAGR of 5.58% from 2026–2035.

The global automotive PCB market is undergoing a transformational shift driven by vehicle electrification, autonomous driving technology integration, and advanced connectivity. Automotive printed circuit boards are complex circuit systems used to control most electronic operations in modern vehicles including engine management, ADAS, infotainment, body electronics, and EV battery management. Rising penetration of EVs, ADAS, and advanced infotainment systems is boosting demand for high-density and multi-layer PCBs that can withstand the automotive environment’s extreme temperature, vibration, and electromagnetic compatibility requirements.

In June 2023, Meiko Electronics revealed that the company will invest USD 200 million in the development of a new factory in Hoa Binh, Vietnam, to expand automotive PCB manufacturing capacity for ADAS and EV power electronics applications. The investment reflects the commercial recognition that automotive PCB demand growth, particularly for high-layer-count and thermal management PCBs in EV and ADAS applications, requires dedicated capacity whose proximity to automotive OEM assembly facilities in Southeast Asia creates supply chain efficiency advantages.

Market Size and Forecast

-

Market Size in 2026E: USD 12.34 Billion

-

Market Size by 2035: USD 20.12 Billion

-

CAGR: 5.58% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Automotive PCB Market - Request Free Sample Report

Automotive PCB Market Trends

-

EV battery management system (BMS) PCB complexity is increasing as electric vehicles require advanced voltage monitoring, thermal sensing, and communication capabilities.

-

ADAS domain controller consolidation is boosting demand for high-performance automotive PCBs. These boards must process data from multiple sensors simultaneously while supporting greater computing power and thermal loads.

-

Advanced thermal management technologies, including metal-core substrates and high-conductivity laminates, are gaining adoption in automotive PCBs. These solutions help address the heat dissipation requirements of EV power electronics.

-

Vehicle-to-everything (V2X) connectivity is creating demand for high-frequency automotive PCBs and RF substrates. Reliable signal transmission at millimeter-wave frequencies requires advanced low-loss PCB materials.

-

Automotive manufacturers and suppliers are increasingly diversifying and regionalizing PCB supply chains. This strategy aims to improve supply security and reduce risks associated with geographic concentration and global disruptions.

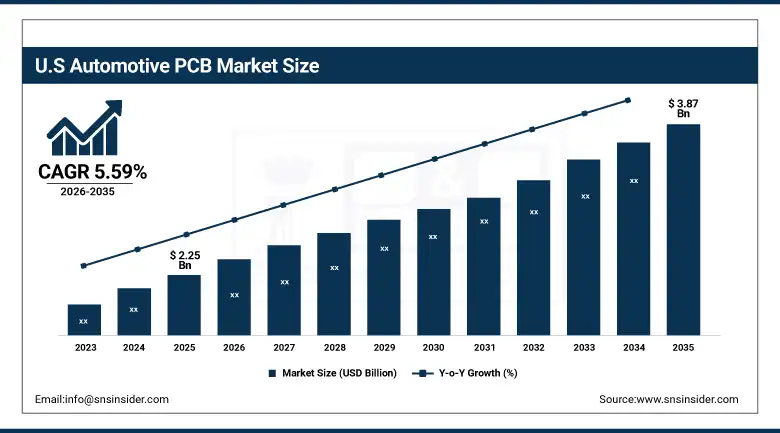

U.S. Automotive PCB Market Size Outlook:

The U.S. Automotive PCB Market was valued at approximately USD 2.25 Billion in 2025 and is expected to reach approximately USD 3.87 Billion by 2035, growing at a CAGR of approximately 5.59%. The U.S. is a significant automotive PCB consuming market whose domestic production capacity is growing with IRA domestic content requirements and CHIPS Act investment that creates incentives for automotive electronics supply chain localisation. TTM Technologies, Jabil Circuit, and Benchmark Electronics serve the domestic automotive PCB industry alongside imported boards from Asian manufacturers.

Samsung Electro-Mechanics announced the expansion of its automotive PCB portfolio in 2024 with new high-density interconnect PCBs for ADAS and autonomous driving applications, featuring enhanced signal integrity at radar and LiDAR operating frequencies. The product development reflects the commercial recognition that ADAS sensor fusion processing requires substrate materials and manufacturing precision beyond conventional automotive PCB standards whose performance specification creates premium procurement opportunities for technically qualified manufacturers.

Automotive PCB Market Segment Analysis

-

By PCB Type, the Double-Sided PCB segment dominated the Automotive PCB Market with approximately 39.80% share in 2025, while the Multi-Layer PCB segment is the fastest growing.

-

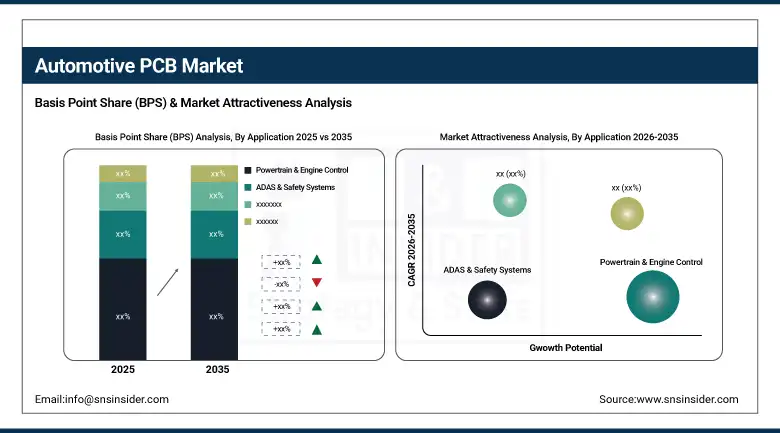

By Application, the Powertrain & Engine Control segment dominated the Automotive PCB Market with approximately 33.40% share in 2025, while the ADAS & Safety Systems segment is the fastest growing.

-

By Vehicle Type, the Passenger Cars segment dominated the Automotive PCB Market with approximately 61.50% share in 2025, while the Commercial Vehicles segment is the fastest growing.

By Type, double-sided dominates, multi-layer grows fastest

Double-sided PCBs retained the dominant type position in the automotive PCB market in 2025. Their commercial primacy reflects the established manufacturing infrastructure and competitive cost economics that double-sided PCB production provides for the majority of automotive body electronics, lighting control, infotainment interface, and engine control unit applications whose circuit complexity is achievable within two copper layers. Each vehicle’s instrument cluster, door control module, and lighting system PCB requirement creates consistent double-sided PCB procurement whose aggregate across global vehicle production creates the market’s highest-volume PCB type category.

Multi-layer PCBs are the fastest-growing type because the automotive electronics systems whose PCB requirements are growing fastest—EV battery management systems, ADAS domain controllers, V2X communication modules, and high-power inverter gate driver circuits universally require the signal density, controlled impedance routing, and power-ground plane shielding that multi-layer architecture enables. Each new EV platform that specifies a centralised BMS architecture creates multi-layer PCB procurement whose layer count, copper weight, and thermal performance requirements substantially exceed conventional vehicle electronics.

By Application, powertrain dominates, ADAS grows fastest

Powertrain and engine control retained the dominant application position in the automotive PCB industry in 2025. The powertrain ECU’s role as the vehicle’s most critical electronic control system creates PCB procurement whose reliability specification, operating temperature range, and vibration resistance requirements define the automotive PCB quality standard. Conventional ICE engine management systems have created decades of established powertrain PCB procurement infrastructure.

ADAS and safety systems is the fastest-growing application because regulatory mandates and consumer safety demand are creating systematic ADAS feature adoption across vehicle segments from premium to mainstream. Euro NCAP’s safety rating requirements, U.S. NHTSA’s automatic emergency braking mandate, and China’s ADAS-inclusive safety standards collectively create mandatory ADAS electronic content adoption whose radar, camera, ultrasonic sensor, and control unit PCBs must be supplied for every compliant vehicle.

By Vehicle Type, passenger cars dominate, commercial vehicles grow fastest

Passenger cars retained the dominant vehicle type position with 61.5% of the automotive PCB market in 2025. The passenger car segment’s commercial primacy reflects its extraordinary production volume, estimated at over 70 million units annually globally, whose per-vehicle PCB content creates aggregate procurement that no other vehicle category can approach. The passenger car market’s progressive adoption of ADAS, advanced infotainment, digital cockpit, and electrification technologies is simultaneously increasing per-vehicle PCB content while sustaining production volume, creating a compounding revenue growth dynamic that sustains the segment’s commercial dominance.

Commercial vehicles are the fastest-growing vehicle type because fleet telematics regulatory mandates, ADAS safety requirements for heavy trucks, and commercial vehicle electrification are creating above-average per-vehicle electronic content growth. Each new heavy truck EV platform creates battery management, powertrain control, and charging system PCBs whose combined content per vehicle substantially exceeds passenger car PCB economics. Fleet management telematics mandates in the U.S., Europe, and China create connectivity module PCB procurement across the entire commercial vehicle fleet whose regulatory adoption creates a defined procurement timeline.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

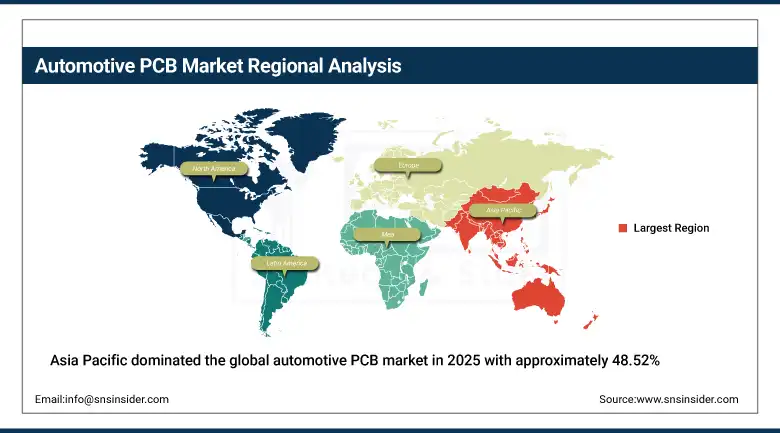

Asia Pacific Automotive PCB Market Insights

Asia Pacific dominated the global automotive PCB market in 2025 with approximately 48.52% of global revenues. China accounts for approximately 48.6% of Asia Pacific revenues through its position as the world’s largest automotive production market whose EV leadership creates the most commercially dynamic automotive PCB demand environment globally. Japan and South Korea represent technically sophisticated secondary markets where Nippon Mektron, Samsung Electro-Mechanics, Meiko Electronics, and CMK Corporation define the global automotive PCB technology frontier whose product development creates the high-performance specifications adopted by automotive OEMs worldwide.

India and Southeast Asia are the most commercially dynamic emerging markets within Asia Pacific where automotive production growth, EV adoption acceleration, and manufacturing capacity expansion—demonstrated by Meiko Electronics’ USD 200 million Vietnam factory investment—create above-average automotive PCB demand and supply chain development.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Automotive PCB Market Insights

North America is a commercially significant automotive PCB market whose domestic production is growing with IRA incentives and CHIPS Act investment creating supply chain localisation motivation. The United States accounts for approximately 87.4% of North American revenues through its EV manufacturing expansion at Tesla, GM, Ford, and Rivian facilities whose battery and powertrain PCB procurement creates structured domestic demand. TTM Technologies and Jabil Circuit serve domestic automotive PCB requirements alongside imported boards whose domestic content requirements are creating procurement localisation motivation.

Canada and Mexico are significant secondary markets whose automotive manufacturing infrastructure creates consistent automotive PCB procurement. Mexico’s automotive assembly facilities for both ICE and EV platforms create import procurement whose proximity to U.S. manufacturing creates North American supply chain integration opportunities.

Europe Automotive PCB Market Insights

Europe is a technically sophisticated automotive PCB industry where AT&S’s Austrian operations, the automotive OEM sector’s premium electronic content specification, and EU safety regulation’s mandatory ADAS feature requirements create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive OEM sector’s electronic content investment, the premium vehicle segment’s above-average ADAS and digital cockpit specification, and the EV platform transition’s BMS and power electronics PCB procurement.

The United Kingdom and France are significant secondary markets where Stellantis, Jaguar Land Rover, and Renault’s EV platform transitions create growing automotive PCB procurement. European PCB manufacturers’ investment in automotive-qualified HDI and rigid-flex production is progressively creating domestic supply alternatives to Asian imports for premium European OEM specification.

MEA & Latin America Automotive PCB Market Insights

The Middle East and Africa and Latin America are growing automotive PCB markets where vehicle production growth and increasing electronic content adoption create structured demand. UAE leads MEA at approximately 38.4% through its premium vehicle import market’s electronic content, the growing automotive electronics aftermarket, and technology park manufacturing investment. Brazil leads Latin American revenues at approximately 44.2% through its large vehicle production base, Volkswagen, GM, and Stellantis’ Brazilian operations, and the growing domestic EV market’s electronics procurement.

Morocco’s automotive manufacturing sector, anchored by Renault and Stellantis assembly facilities, and South Africa’s vehicle assembly industry create MEA automotive PCB procurement that complements the Gulf region’s vehicle import and aftermarket electronics demand.

Market Dynamics

Growth Drivers: Vehicle electrification increasing per-vehicle PCB content and ADAS mandates creating systematic procurement

Vehicle electrification is the automotive PCB market’s most commercially transformative structural growth driver. Each vehicle that transitions from ICE to battery electric creates a per-vehicle PCB content increase of 2-4 times whose aggregate across global EV market penetration growth creates substantial market revenue expansion beyond overall vehicle production volume growth. EV battery management system PCBs, power inverter control boards, thermal management controller PCBs, and DC-DC converter boards collectively represent electronic content per EV that substantially exceeds conventional vehicle counterparts whose replacement creates revenue growth from content per vehicle rather than production volume.

ADAS regulatory mandates are creating systematic automotive PCB procurement whose compliance-driven character sustains demand through economic and consumer preference cycles. Euro NCAP’s 5-star safety rating requirements, NHTSA’s automatic emergency braking mandate, and China’s vehicle safety standard evolution collectively create defined adoption timelines whose vehicle production volumes create predictable PCB procurement growth that automotive PCB manufacturers can plan production capacity investment around.

Restraints: Automotive qualification lead time and PCB price erosion from commoditisation

Automotive PCB qualification requirements create new product introduction timelines of 2-4 years from design specification through validation testing, supplier qualification, and production start-up approval whose duration creates commercialisation lag that limits the pace of new automotive PCB technology adoption. Each new PCB laminate material, via technology, or surface finish change requires qualification revalidation that extends the timeline for technology adoption in production vehicles.

Price erosion from PCB commoditisation in established automotive application categories creates margin compression for PCB manufacturers whose volume growth in standard applications does not create proportional revenue growth. Each year of production volume growth in established automotive PCB categories creates competitive pricing pressure whose impact on manufacturer economics requires migration toward higher-value HDI, rigid-flex, and multi-layer products to sustain revenue growth rates.

Opportunities: EV BMS PCB complexity growth and autonomous vehicle domain controller consolidation

EV battery management system PCB complexity growth represents the most commercially premium near-term automotive PCB opportunity. Next-generation BMS architectures that integrate cell-level voltage and temperature monitoring at higher cell counts create PCB layer count, feature density, and reliability requirements whose technical complexity creates commercial value substantially exceeding conventional BMS PCB economics. Each successive EV generation that increases battery capacity and management sophistication creates BMS PCB upgrade procurement whose premium pricing sustains above-market revenue growth for qualified suppliers.

Autonomous vehicle domain controller consolidation is creating high-performance computing PCB opportunities whose technical complexity and commercial value represent the most premium automotive PCB application category. Each centralised autonomous driving domain controller that consolidates multiple ADAS compute functions onto a single high-performance board creates multi-layer, high-speed differential routing, and advanced thermal management PCB procurement whose per-unit commercial value substantially exceeds distributed ADAS architecture alternatives.

Recent Developments:

-

2023: Meiko Electronics announced a USD 200 million factory investment in Hoa Binh, Vietnam in June 2023 to expand automotive PCB manufacturing capacity for ADAS and EV power electronics applications, targeting Southeast Asian supply chain proximity to automotive OEM assembly facilities.

-

2024: Samsung Electro-Mechanics expanded its automotive PCB portfolio in 2024 with new high-density interconnect PCBs for ADAS and autonomous driving applications featuring enhanced signal integrity at radar and LiDAR operating frequencies, targeting the premium automotive electronics specification market.

-

2024: AT&S announced the expansion of its automotive-qualified HDI PCB production capacity in 2024, targeting European automotive OEM EV platform and ADAS domain controller PCB procurement whose technical complexity requires the advanced manufacturing capability that AT&S’s Austrian and Asian facilities provide.

Automotive PCB Companies are:

-

Nippon Mektron Ltd.

-

Meiko Electronics Co., Ltd.

-

Tripod Technology Corporation

-

CMK Corporation

-

KCE Electronics PCL

-

Unimicron Technology Corporation

-

Chin Poon Industrial Co., Ltd.

-

TTM Technologies

-

Multek (Flex Ltd.)

-

AT&S Austria Technologie

-

Jabil Circuit Inc.

-

Benchmark Electronics

-

Foxconn Electronics

-

Ibiden Co., Ltd.

-

Sumitomo Electric Industries

-

Compeq Manufacturing

-

Elna Co., Ltd.

-

Dynamic Electronics Co., Ltd.

Automotive PCB Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.69 Billion |

| Market Size by 2035 | USD 20.12 Billion |

| CAGR | CAGR of 5.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Single-Sided PCB, Double-Sided PCB, Multi-Layer PCB, HDI PCB, Flexible/Rigid-Flex PCB) • by Application (Powertrain & Engine Control, ADAS & Safety Systems, Infotainment & Connectivity, Body Electronics, Lighting, EV Battery Management, Others) • by Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles, Hybrid Vehicles) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Nippon Mektron Ltd., Samsung Electro-Mechanics, Meiko Electronics Co., Ltd., Tripod Technology Corporation, CMK Corporation, KCE Electronics PCL, Unimicron Technology Corporation, Daeduck Electronics, Chin Poon Industrial Co., Ltd., TTM Technologies, Multek (Flex Ltd.), AT&S Austria Technologie, Jabil Circuit Inc., Benchmark Electronics, Foxconn Electronics, Ibiden Co., Ltd., Sumitomo Electric Industries, Compeq Manufacturing, Elna Co., Ltd., Dynamic Electronics Co., Ltd. |

Frequently Asked Questions

The Automotive PCB Market is expected to grow at a CAGR of 5.58% from 2026 to 2035.

The Automotive PCB Market was valued at USD 11.69 Billion in 2025.

Vehicle electrification increasing per-vehicle PCB content 2-4 times compared to conventional ICE vehicles through BMS, powertrain control, and charging system PCBs.

Passenger Cars dominated the Automotive PCB Market with 61.5% share in 2025, while Commercial Vehicles is the fastest growing segment.

Asia Pacific dominated the Automotive PCB Market in 2025 with approximately 48.52% of global revenues, with China accounting for approximately 48.6% of Asia Pacific revenues.

Get in Touch