Automotive Semiconductor Chip Market Report Scope & Overview:

Get more information on Automotive Semiconductor Chip Market - Request Sample Report

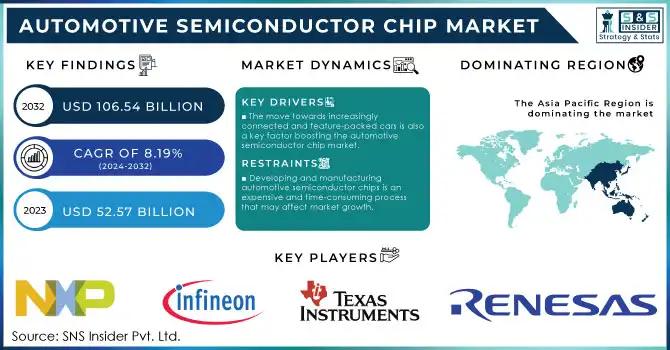

The Automotive Semiconductor Chip Market Size was valued at USD 52.57 billion in 2023 and is expected to reach USD 106.54 billion by 2032, growing at a CAGR of 8.19% over the forecast period 2024-2032.

The Automotive Semiconductor Chip Market plays a vital role in driving innovation and efficiency in the modern automotive industry, underpinned by trends like electrification, automation, and connectivity. A key factor fueling this market's growth is the rapid adoption of electric vehicles (EVs), hybrid vehicles, and battery electric vehicles (BEVs), whose combined U.S. sales rose from 17.8% of total light-duty vehicle sales in Q1 2024 to 18.7% in Q2 2024. These vehicles rely heavily on semiconductor chips for battery management systems, energy optimization, and power regulation. Power semiconductor chips, in particular, are crucial for managing energy flow in EVs, while microcontrollers and system-on-chips (SoCs) enable advanced driver-assistance systems (ADAS) functionalities like lane-keeping assistance and automatic emergency braking.

The increasing prevalence of connected vehicles further propels the demand for high-performance chips. In 2023 alone, approximately 50 million connected cars were sold worldwide, leveraging vehicle-to-everything (V2X) communication to enhance traffic management, boost safety, and enable real-time predictive maintenance. These functionalities depend on semiconductors capable of processing large datasets with minimal latency. Advanced automotive chips support the integration of cloud services, enabling seamless data sharing and real-time decision-making. Additionally, the rising need for autonomous vehicles and smart infrastructure reinforces the importance of chips optimized for reliability, scalability, and energy efficiency.

As automakers strive to meet the growing demand for sustainable, automated, and connected transportation, the automotive semiconductor chip market remains integral to innovation. From ADAS technology to EV energy systems, these chips form the backbone of cutting-edge automotive solutions, driving growth and revolutionizing the global automotive landscape.

Automotive Semiconductor Chip Market Dynamics

Drivers

-

The move towards increasingly connected and feature-packed cars is also a key factor boosting the automotive semiconductor chip market.

In-car infotainment systems, offering entertainment, navigation, communication, and other features, are now a crucial factor in setting car makers apart. These systems incorporate technologies such as touchscreens, voice recognition, connectivity features like Bluetooth, Wi-Fi, and 5G, and more advanced multimedia processing abilities. The efficient operation of all these features is dependent on semiconductor chips. Infotainment systems frequently consist of various components such as CPUs, GPUs, memory chips, and microcontrollers that all necessitate chips. With the growing desire from customers for enhanced connectivity features like easy smartphone integration, software updates via the internet, and online service accessibility, the automotive sector is incorporating more intricate and powerful semiconductor technologies. The increase in electric vehicles, which emphasize sustainable and energy-efficient technologies, is also connected to this trend, as it motivates manufacturers to create more advanced chip technologies to support these systems while maintaining vehicle range and performance.

-

The movement towards electrifying vehicles offers a significant growth potential for the automotive semiconductor chip market.

Electrification requires various semiconductor solutions, especially for power management, motor control, battery management systems (BMS), and onboard chargers. Electric cars, such as hybrid electric vehicles (HEVs), plug-in hybrid electric vehicles (PHEVs), and fully electric vehicles (EVs), need chips to control power distribution, improve performance, and optimize electric motor efficiency. MOSFETs and diodes are essential components in electrified vehicles, facilitating efficient power conversion among the battery, motor, and other parts of the powertrain. Furthermore, battery management systems need various semiconductor solutions to oversee voltage, temperature, and state of charge for the safe and effective functioning of batteries. Due to the growing emphasis on decreasing reliance on fossil fuels, manufacturers are heavily investing in semiconductor technologies to enhance vehicle electrification, leading to increased demand for automotive semiconductors.

Restraints

-

Developing and manufacturing automotive semiconductor chips is an expensive and time-consuming process that may affect market growth.

Automotive semiconductor chips require rigorous testing, certification, and validation to meet the stringent quality standards and safety requirements set by the automotive industry. These chips must be reliable, durable, and capable of functioning under extreme conditions such as high temperatures, humidity, and vibrations. Additionally, automotive manufacturers require chips that can operate over extended lifespans, as vehicles are expected to last for many years. The high development costs of these chips can pose a barrier to entry for new players in the market and can increase the overall cost of production for automotive manufacturers. Furthermore, the research and development (R&D) costs for creating cutting-edge chips for autonomous vehicles, EVs, and ADAS technologies can be prohibitively expensive, requiring substantial investment in design, simulation, and testing processes. For semiconductor manufacturers, the need to build and maintain specialized manufacturing facilities, which require high capital expenditure, also contributes to the overall cost structure. These high costs could hinder the widespread adoption of advanced automotive technologies, particularly for smaller manufacturers or in markets with lower vehicle production volumes.

Automotive Semiconductor Chip Market Segmentation Analysis

By Component

Discrete power segment dominated the market in 2023 with a 30% market share and it is expected to become the fastest-growing segment during 2024-2032, due to enhanced silicon carbide (SiC) and gallium nitride (GaN) technologies being increasingly adopted to improve efficiency and thermal performance. These chips are used in powertrain systems, battery management systems, and electric motor drives to ensure optimal performance and energy conservation. As EV adoption surges globally, the demand for discrete power components, such as MOSFETs and IGBTs, continues to dominate the market. Leading companies include Infineon Technologies, STMicroelectronics, and ON Semiconductor, which supply these components for EV applications like Tesla’s advanced powertrain systems and Toyota’s hybrid models. Similarly, Wolfspeed, Rohm Semiconductor, and Texas Instruments lead innovation in this segment, supplying chips for high-demand applications, including Lucid Motors’ electric drivetrains and BYD’s battery systems. This growth is further fueled by government incentives and investments in EV infrastructure.

By Vehicle Type

The passenger vehicle segment dominated with a 66% market share in the automotive semiconductor chip market in 2023, due to the increasing adoption of advanced driver-assistance systems (ADAS), infotainment solutions, and electrification in personal cars. With consumer demand for connectivity, safety, and enhanced driving experiences, semiconductors play a critical role in enabling features like real-time navigation, collision avoidance, and autonomous driving capabilities. For instance, Tesla relies heavily on semiconductor chips for its Autopilot system and energy management in Evs.

The LCV segment is projected to grow rapidly during 2024-2032, due to the expanding e-commerce industry and the surge in last-mile delivery services. These vehicles increasingly integrate semiconductor-enabled features such as telematics, fleet management systems, and electric drivetrains to improve efficiency and reduce emissions. Governments’ push for cleaner transportation solutions, especially electric LCVs, further accelerates semiconductor demand. For example, Ford’s Transit electric van integrates advanced semiconductors for battery performance and connectivity, catering to the growing demand in delivery fleets.

Automotive Semiconductor Chip Market Regional Overview

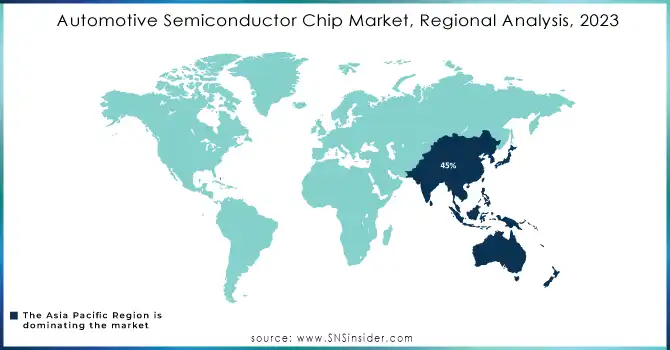

In 2023, APAC held a leading position in the automotive semiconductor chip market, with a market share of 45%. The presence of leading car manufacturers like Toyota, Hyundai, and Honda, together with the increasing use of electric vehicles (Evs) and advanced driver-assistance systems (ADAS), is responsible for this dominance. The strong semiconductor manufacturing ecosystem in the region, especially in places such as China, South Korea, and Taiwan, guarantees the presence of top-notch chips at affordable rates. APAC is a center for innovation in electric vehicle technology and intelligent transportation, as companies such as BYD and NIO drive the need for automotive chips.

North America is expected to experience the most rapid growth rate during 2024-2032, due to the quick progress in autonomous driving and connected vehicle technologies. Tesla, General Motors, and Ford are leading the way in incorporating artificial intelligence (AI) and machine learning (ML) into vehicles, boosting the need for advanced chips. Government incentives are helping to boost the demand for electric vehicles (Evs) by promoting the development of specialized semiconductor technology like battery management systems and silicon carbide (SiC) inverters.

Need any customization research on Automotive Semiconductor Chip Market - Enquiry Now

Key Players in Automotive Semiconductor Chip Market

The major key players in the Automotive Semiconductor Chip Market are:

-

NXP Semiconductors (i.MX 8QuadMax Processor, SAF5400 Radar Transceiver)

-

Infineon Technologies (AURIX Microcontrollers, TLE987x Motor Control Ics)

-

Texas Instruments (TPS543C20A DC-DC Converter, DRV8301 Motor Driver)

-

STMicroelectronics (SPC5 Automotive Microcontrollers, L9908 Battery Management IC)

-

Renesas Electronics (RH850 Microcontroller, R-Car V3H SoC for ADAS)

-

Analog Devices (LTC6811 Battery Monitor IC, ADSP-BF70x Blackfin Processors)

-

ON Semiconductor (FAM65V60DF Gate Driver, NCV7420 CAN Transceiver)

-

Broadcom Inc. (BCM89335 Wireless Chip, AFEM-8200 Automotive Front-End Module)

-

NVIDIA (NVIDIA Drive Orin, Jetson AGX Xavier)

-

Qualcomm (Snapdragon Ride SoC, Qualcomm C-V2X Module)

-

Intel Corporation (Mobileye EyeQ5 SoC, Intel Atom Processor A3900)

-

Rohm Semiconductor (BD9S402MUF-LA Buck Converter, IMZ120R045M1 IGBT)

-

Toshiba Corporation (TB9081FNG Motor Controller, TMPM4K Microcontroller)

-

Micron Technology (LPDDR4 Automotive Memory, NAND Flash for ADAS)

-

Samsung Electronics (Exynos Auto V9 SoC, GDDR6 Automotive Memory)

-

Sony Semiconductor (IMX490 Automotive CMOS Sensor, IMX324 Image Sensor)

-

Maxim Integrated (MAX9296 GMSL Serializer, MAX17320 Battery Fuel Gauge)

-

Marvell Technology (88Q2112 Automotive Ethernet PHY, OCTEON TX2 SoC)

-

MediaTek (Dimensity Auto 1050 SoC, MT8183 Processor for Infotainment)

-

Texas Instruments (LM53602-Q1 Buck Converter, ADS7128-Q1 Analog-to-Digital Converter)

Key Suppliers and Components for Automotive Semiconductor Chips:

-

Shin-Etsu Chemical (Silicon Wafers)

-

Sumco Corporation (Monocrystalline Silicon Wafers)

-

GlobalWafers Co., Ltd. (Epitaxial Wafers)

-

Dow Inc. (Epoxy Resins for Packaging)

-

3M (Thermal Interface Materials)

-

Nichia Corporation (LED Chips for Optoelectronics)

-

Honeywell International (Precious Metal Pastes)

-

Hemlock Semiconductor (Polysilicon)

-

Asahi Kasei Corporation (Photoresists and Specialty Chemicals)

-

Momentive Performance Materials (Semiconductor-Grade Sealants and Adhesives)

Recent Developments

-

September 2024: Renesas Electronics Corporation introduced its newest advancement in automotive semiconductor technology: the R-Car X5H SoC, the fifth generation of its kind. Crafted using 3nm process technology, the R-Car X5H is the first automotive multi-domain SoC in the industry to be developed on this cutting-edge node.

-

August 2024: Intel has introduced a new graphics processing unit (GPU) for vehicles in mainland China, as the US chip giant focuses more on the world's biggest electric vehicle market due to its slow growth and fierce competition in advanced semiconductors.

-

January 2024: Texas Instruments (TI) unveiled new chips created to enhance automotive safety and intelligence. The AWR2544 radar chip, operating at 77GHz in the mm-wave range, is the first of its kind for satellite radar structures, enhancing autonomy levels through better sensor fusion and decision-making in ADAS.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 52.57 Billion |

| Market Size by 2032 | USD 106.54 Billion |

| CAGR | CAGR of 8.19% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Processor, Discrete Power, Sensor, Memory, Others) • By Vehicle Type (Passenger Vehicle, Light Commercial Vehicle (LCV), Heavy Commercial Vehicle (HCV)) • By Fuel Type (Gasoline, Diesel, EV/HEV) • By Application (Chassis, Powertrain, Safety, Telematics & Infotainment, Body Electronics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | NXP Semiconductors, Infineon Technologies, Texas Instruments, STMicroelectronics, Renesas Electronics, Analog Devices, ON Semiconductor, Broadcom Inc., NVIDIA, Qualcomm, Intel Corporation, Rohm Semiconductor, Toshiba Corporation, Micron Technology, Samsung Electronics, Sony Semiconductor, Maxim Integrated, Marvell Technology, MediaTek, Texas Instruments |

| Key Drivers | • The move towards increasingly connected and feature-packed cars is also a key factor boosting the automotive semiconductor chip market. • The movement towards electrifying vehicles offers a significant growth potential for the automotive semiconductor chip market. |

| RESTRAINTS | • Developing and manufacturing automotive semiconductor chips is an expensive and time-consuming process that may affect market growth. |

Frequently Asked Questions

Ans: Miniaturization and integration, Electronic systems and features are becoming more prevalent, Demanding entertainment and comfort amenities.

Ans: Long development and production cycles, Compliance with regulations and safety standards.

Ans: Automotive Semiconductor Chip Market size was valued at USD 52.57 Billion in 2023

Ans: The Automotive Semiconductor Chip Market was USD 52.57 Billion in 2023 and is expected to Reach USD 106.54 Billion by 2032.

Ans: The Automotive Semiconductor Chip Market is expected to grow at a CAGR of 8.19% during 2024-2032.

Get in Touch