Automotive Semiconductor Market Report Scope & Overview:

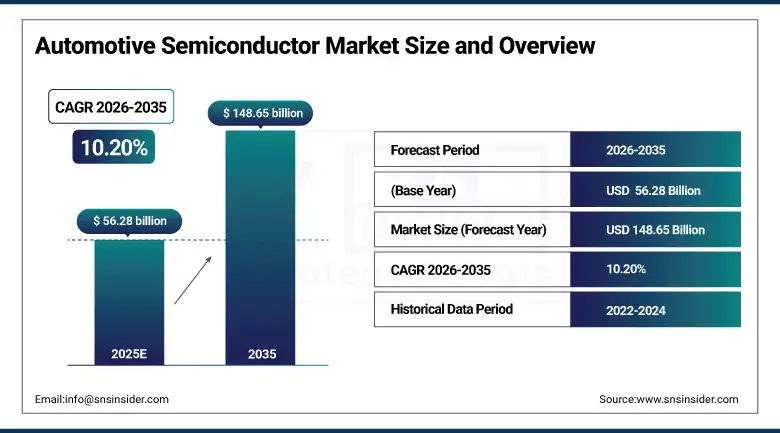

The Automotive Semiconductor Market size was valued at USD 56.28 Billion in 2025 and is projected to reach USD 148.65 Billion by 2035, growing at a CAGR of 10.20% during 2026–2035.

The Automotive Semiconductor Market is growing at an impressive rate, driven by the rising need for technologically advanced electronics in modern vehicles. The increased adoption of electric vehicles, the incorporation of advanced driver assistance systems, and the move towards autonomous driving are the primary growth drivers for the Automotive Semiconductor Market. Furthermore, the rise in consumer demand for connected vehicles and safety features also adds to the growth of the Automotive Semiconductor Market. Technological advancements, along with government regulations promoting the safety and electrification of vehicles, are also contributing to the growth of the Automotive Semiconductor Market during the forecast period.

Automotive Semiconductor Market Size and Growth:

-

Market Size in 2025: USD 56.28 Billion

-

Market Size by 2035: USD 148.65 Billion

-

CAGR: 10.20% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Automotive Semiconductor Market - Request Free Sample Report

Automotive Semiconductor Market Key Trends:

-

Rising adoption of electric vehicles (EVs) is significantly increasing demand for power semiconductors, battery management systems, and energy-efficient chips.

-

Advanced driver-assistance systems (ADAS) and autonomous driving technologies are driving the need for high-performance processors, sensors, and AI-enabled semiconductor solutions.

-

Growing integration of infotainment systems, connectivity features, and vehicle-to-everything (V2X) communication is boosting semiconductor content per vehicle.

-

Miniaturization of electronic components and advancements in chip design are enhancing performance, efficiency, and thermal management in automotive applications.

-

Increasing focus on vehicle safety, supported by stringent government regulations, is accelerating the adoption of semiconductor-based safety systems.

-

Supply chain diversification, localization of semiconductor manufacturing, and strategic partnerships between automakers and chip manufacturers are shaping the market landscape.

US Automotive Semiconductor Market Size Outlook:

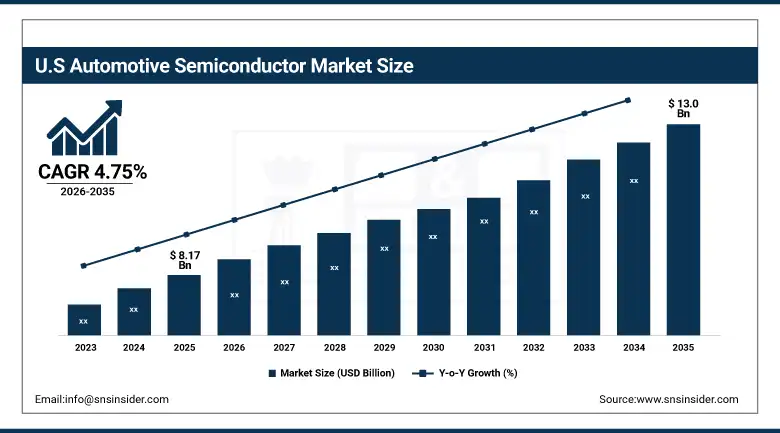

The United States Automotive Semiconductor Market size was valued at USD 8.17 Billion in 2025 and is projected to reach USD 13.0 Billion by 2035, growing at a CAGR of 4.75% during 2025–2035, Growth of the U.S. Automotive Semiconductor Market is driven by increasing demand for advanced driver-assistance systems (ADAS), rapid adoption of electric vehicles (EVs), rising integration of semiconductor content in modern vehicles, and continuous advancements in autonomous driving and in-vehicle connectivity technologies.

Automotive Semiconductor Market Key Drivers:

-

Rising Adoption of Electric Vehicles (EVs) and Advanced Driver-Assistance Systems (ADAS) Drives Market Growth

The increasing demand for electric vehicles and advanced driver-assistance systems is another significant factor that is boosting the automotive semiconductor market. Nowadays, vehicles are becoming more dependent on various kinds of semiconductor devices. For example, in 2025, more than 40% of new electric vehicle models were equipped with advanced battery management ICs as well as AI-based ADAS processor chips. The growing demand for connected as well as autonomous vehicles is another factor that is boosting the automotive semiconductor market.

Automotive Semiconductor Market Key Restraints:

-

High Manufacturing Costs and Supply Chain Constraints Limit Market Growth

In spite of the demand, the production cost of advanced semiconductors and supply chain disruptions are major factors acting as roadblocks in the growth of the global semiconductors in the automotive sector. The production of semiconductors for the automotive sector demands special chips, sensors, and processors, which are often required to be of top-notch quality and safety. Developing countries are facing greater challenges in terms of manufacturing capabilities and dependencies on imports.

Automotive Semiconductor Market Key Opportunities:

-

Integration of Autonomous Driving, Connected Cars, and V2X Technologies Creates New Opportunities

The trend towards autonomous driving, connected vehicles, and vehicle-to-everything (V2X) communication creates growth opportunities for the industry. Advanced processors, AI-enabled chipsets, and sensors are in greater demand for real-time data processing, safety, and predictive maintenance. For example, automobile manufacturers such as Tesla and Ford are adding semiconductors in vehicles for autonomous driving and infotainment systems. The development of smart cities and charging infrastructure for electric vehicles creates opportunities for semiconductor companies to launch innovative products in the automotive space.

Automotive Semiconductor Market Segments:

-

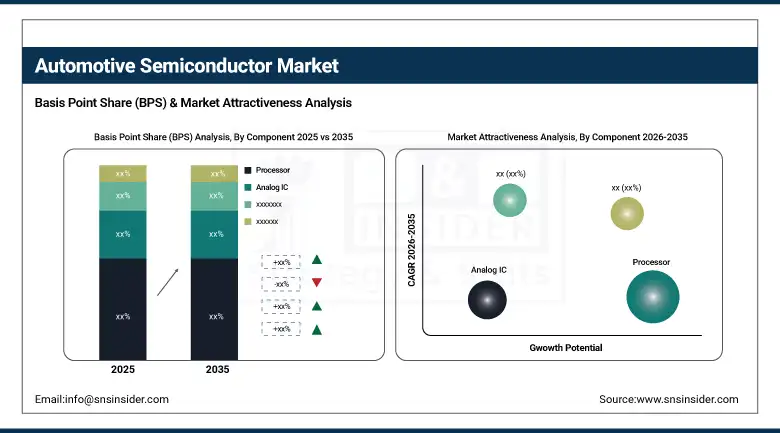

By Component, Processors held the largest market share of 28.45% in 2025, while Sensors are expected to grow at the fastest CAGR of 11.12% during 2026–2035.

-

By Vehicle Type, Passenger Cars dominated with 54.32% market share in 2025, whereas Electric Vehicles/Hybrid Electric Vehicles (EV/HEV) are projected to record the fastest CAGR of 12.05% through 2026–2035.

-

By Fuel Type, Gasoline vehicles accounted for the highest market share of 45.87% in 2025, while EV/HEV is expected to grow at the fastest CAGR of 12.18% during the forecast period.

-

By Application, Powertrain held the largest market share of 31.76% in 2025, while Safety and ADAS applications are anticipated to expand at the fastest CAGR of 11.89% through 2026–2035.

By Component, Processors Dominate the Market:

The Processors segment held the largest market share in the Automotive Semiconductor Market. This is because of the increased use of advanced driver-assistance systems, autonomous driving, and infotainment systems, all of which are processor-intensive. Even as other automotive semiconductor devices like sensors, memory devices, and individual power devices are gaining popularity, the growing need for computing power and artificial intelligence-based processing is sustaining this segment’s dominance.

By Vehicle Type, Passenger Cars Dominate the Market:

The market share of the passenger car segment was the highest in 2025, followed by the LCV segment, and the HCV segment lagged behind these two segments in the market share race. The reason is the high production volumes of passenger cars, coupled with the increasing trend of integrating electronic components into these vehicles. Though the trend of integrating semiconductors is catching up in the LCV and HCV segments, the trend of adopting electric and hybrid vehicles is keeping the passenger car segment at the top of the market share race.

By Fuel Type, Gasoline Vehicles Dominate While EV/HEV Grow Rapidly:

The gasoline-powered segment holds the maximum market share in 2025, owing to their continued presence in the global market. On the other hand, EVs and HEVs are expected to see the fastest CAGR due to the increased adoption of electric mobility solutions, incentives offered by the government, and consumer demand for eco-friendly mobility solutions. The need for better power management and energy efficiency is boosting the demand for semiconductors.

By Application, Powertrain Dominates While Safety and ADAS Grow Rapidly:

The Powertrain segment had the highest market share due to the importance of semiconductors in managing the engine, electric drive, and energy optimization. The Safety and ADAS segment will see the fastest growth rate due to the increase in mandates, consumer demand for advanced safety features, and the need to drive autonomous vehicles. The Telematics, Infotainment, and Body Electronics segments are contributing to the rising semiconductor content in vehicles.

Automotive Semiconductor Market Regional Analysis:

Asia-Pacific Automotive Semiconductor Market Insights:

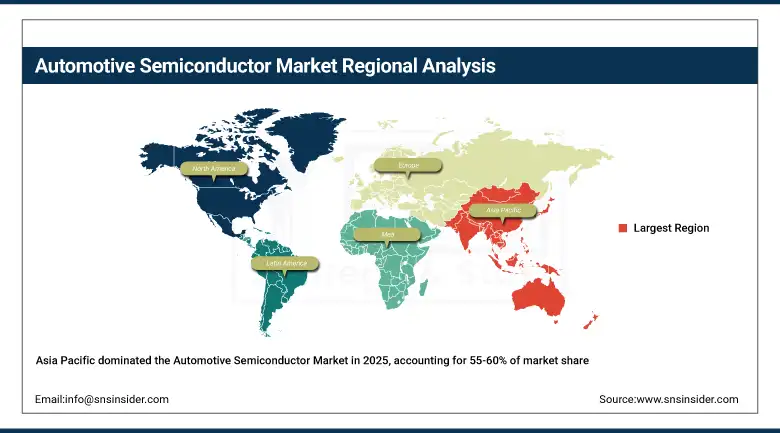

Asia Pacific accounts for the highest share in the global automotive semiconductor industry, with almost 55-60% of the global share held by this region. This is mainly because the automobile industry in this region is growing enormously, especially in China and India, with the rising population, higher disposable income, and increased urbanization, along with the high automotive production capacity in this region. The government initiatives in these countries, such as the adoption of electric and hybrid vehicles, and the high adoption rate of ADAS, also add to the growth of the automotive semiconductor industry in the Asia Pacific region, as major players in the global as well as regional semiconductor industry have set up their production plants in this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Automotive Semiconductor Market Insights:

North America is the second-largest market in the automotive semiconductor market, driven by the well-developed automotive market and the presence of renowned semiconductor companies in the market. The demand for high-tech products, including infotainment, ADAS, and electrification, is the major growth driver of the market in this region. The rise of regulations aimed at increasing the safety of vehicles and reducing emissions is another major growth driver of the market in this region.

Europe Automotive Semiconductor Market Insights:

The region of Europe continues to experience steady growth in the automotive semiconductor market, driven by stringent mandates for safety, emissions, and the adoption of electric and hybrid vehicles. The region of Europe has existing automotive manufacturers, and these have driven investments for R&D, enabling the adoption of innovative semiconductor technologies, especially for ADAS and connected vehicle solutions.

Latin America Automotive Semiconductor Market Insights:

Latin America is growing at the fastest rate, with a growth rate of 6-8%. The growth is fueled by the growing transportation and logistics industries, wherein commercial vehicles increasingly need advanced electronic content. The growth is fueled by the growing rate of urbanization, growing income levels in the middle-class population, and growing personal vehicle ownership. The government is taking various initiatives in countries such as Brazil and Mexico to increase electric vehicle adoption as well as ensure road safety.

Middle East & Africa (MEA) Automotive Semiconductor Market Insights:

Middle East & Africa offers emerging opportunities with the development of infrastructure, the rising trend of connected vehicles, and the growing need for advanced automotive technology. Even though the market share is relatively low compared to other regions, economic diversification and supportive government initiatives are likely to improve the market in the future.

Automotive Semiconductor Market Competitive Landscape:

ESMC GmbH is a joint venture established in 2023 by Robert Bosch, TSMC, Infineon, and NXP in Dresden, Germany. The company is engaged in building a 300mm wafer fabrication facility to provide advanced semiconductor manufacturing solutions to meet the growing needs of automotive and industrial markets in Europe and worldwide.

-

In August 2023: In a major European development, Robert Bosch, TSMC, Infineon, and NXP joined forces to establish ESMC GmbH in Dresden, Germany. This venture aims to construct a 300mm fab and provide advanced chip manufacturing to support the growing automotive and industrial sectors.

Micron Technology is a leading global semiconductor leader with expertise in memory and storage technologies such as DRAM, NAND, and NOR Flash. Founded in 1978 and based in Boise, Idaho, Micron Technology provides high-performance technologies for the automotive, datacenter, mobile, and industrial segments, helping to enable innovation across AI, 5G, and computing technologies.

-

In June 2023: Micron Technology expanded its DRAM and NAND assembly and test facility in Gujarat, India. This move aimed to address both domestic and international demand for these memory products.

Automotive Semiconductor Companies are:

-

Analog Devices Inc

-

NXP Semiconductors N.V.

-

Renesas Electronics Corp.

-

Robert Bosch GmbH

-

STMicroelectronics N.V.

-

Toshiba Corp.

-

Texas Instruments Inc

-

ON Semiconductor

-

Qualcomm Technologies Inc

-

Micron Technology Inc

-

Intel Corporation

-

Xilinx Inc (AMD)

-

Marvell Technology Inc

-

Cadence Design Systems Inc

-

Keysight Technologies Inc

-

Arm Ltd

-

GlobalFoundries Inc

-

Microchip Technology Inc

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 56.28 Billion |

| Market Size by 2035 | USD 148.65 Billion |

| CAGR | CAGR of 10.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Processor, Analog IC, Discrete Power Device, Sensor, Memory, Lighting Device) • By Vehicle Type (Passenger Car, LCV, HCV) • By Fuel Type (Gasoline, Diesel, EV/HEV) • By Application (Powertrain, Safety, Body Electronics, Chassis, Telematics and Infotainment) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Analog Devices, Inc., Infineon Technologies AG, NXP Semiconductors N.V., Renesas Electronics Corp., Robert Bosch GmbH, ROHM Co., Ltd., STMicroelectronics N.V., Toshiba Corp., Texas Instruments, Inc., ON Semiconductor, Qualcomm Technologies, Inc., Micron Technology, Inc., Intel Corporation, Xilinx, Inc. (AMD), Marvell Technology, Inc., Cadence Design Systems, Inc., Keysight Technologies, Inc., Arm Ltd., GlobalFoundries Inc., Microchip Technology, Inc. |

Frequently Asked Questions

Ans: The Power Electronics Market is expected to grow at a CAGR of 10.20% during 2026–2035.

Ans: The market was valued at USD 56.28 Billion in 2025 and is projected to reach USD 148.65 Billion by 2035.

Ans: Increasing demand for energy-efficient devices, rapid adoption of electric vehicles (EVs), growth in renewable energy systems, and advancements in power semiconductor technologies.

Ans: The Power Discrete Devices segment dominated the Power Electronics Market during the projected period.

Ans: Asia Pacific dominated the Power Electronics Market in 2025.

Get in Touch