Automotive Shredded Residue (ASR) Market Report Scope & Overview:

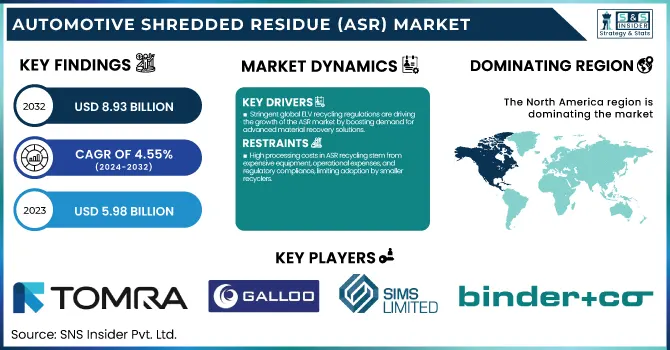

The Automotive Shredded Residue (ASR) Market Size was estimated at USD 5.98 billion in 2023 and is expected to arrive at USD 8.93 billion by 2032 with a growing CAGR of 4.55% over the forecast period 2024-2032.

To Get more information on Automotive Shredded Residue (ASR) Market - Request Free Sample Report

This report uniquely explores ASR generation trends across key regions, highlighting recycling and recovery rates alongside shifting landfilling vs. recycling patterns. It examines the adoption of advanced ASR processing technologies and evaluates export/import dynamics of recovered materials. Additionally, the report tracks the regulatory push towards circular economy models, the rise of AI-driven ASR sorting, and the impact of global supply chain disruptions on material recovery efficiency.

The U.S. fuel transfer pumps market is projected to grow steadily from USD 0.95 billion in 2023 to USD 1.46 billion by 2032, reflecting a CAGR of 4.92%. This growth is driven by increasing demand in industries such as construction, agriculture, and transportation, along with advancements in fuel transfer technology and infrastructure development.

Automotive Shredded Residue (ASR) Market Dynamics

Drivers

-

Stringent global ELV recycling regulations are driving the growth of the ASR market by boosting demand for advanced material recovery solutions.

Governments worldwide are implementing stringent regulations on end-of-life vehicle (ELV) recycling, significantly driving the growth of the Automotive Shredded Residue (ASR) market. As the emphasis grows on sustainable practices and circular economy principles, governments are requiring increased recycling and material recovery rates, decreasing reliance on landfills. As a result, the EU ELV Directive and similar legislation in North America and Asia are encouraging greater utilization of advanced ASR processing technologies by both automakers and recyclers. There has been a gradual increasing trend toward investment in automated sorting, pyrolysis, and chemical recycling processes to reclaim valuable metals and non-metallics. Moreover, surging use of recycled raw materials for generating new automobiles is propelling the market growth. With EVs becoming more prevalent, ASR processing is developing further, spurring new forms of recovery of both batteries and composite materials. The ASR market is likely to remain steady due to supportive regulatory frameworks, technological advancements, and the rising demand for sustainable automotive recycling solutions.

Restraint

-

High processing costs in ASR recycling stem from expensive equipment, operational expenses, and regulatory compliance, limiting adoption by smaller recyclers.

High processing costs pose a significant barrier to the widespread adoption of advanced ASR recycling technologies. Separating valuable materials from ASR entails the use of advanced technology, such as sensor-based separation plants, shredders, and chemical recovery units, which involves high capital costs. Moreover, operational costs such as energy usage, labor, and maintenance also drive up the costs for recyclers. Advanced recovery methods can prove too costly for smaller recycling firms, which utilize expensive tech and other resources, hindering many from being able to afford them. Additionally, the sample rates for recovered materials, particularly plastics and non-ferrous metals, can create challenges in obtaining a stable return on investment. Strict environmental regulations also lead to compliance costs, which make it difficult for companies to maintain profitability. Consequently, many recyclers choose traditional disposal methods, like landfilling or incineration, over these expensive processing technologies, which impedes the overall advancement in the sustainable ASR valorization process.

Opportunities

-

Adapting ASR recycling technologies for e-waste and composite materials enhances material recovery, reduces landfill waste, and creates new revenue streams for recyclers.

The expansion of e-waste and composite material recycling presents a significant opportunity for the automotive shredded residue (ASR) market. Technologies for ASR recycling, like advanced sorting, pyrolysis, and chemical recovery, can be repurposed for the processing of e-waste and composite materials, the latter of which is on the rise with the greater uptake of electric vehicles (EVs) and lightweight automotive components. E-waste is rich in gold, silver, and copper, and its composite materials (carbon fiber and reinforced plastics) should have high-performance applications if appropriately recycled. Integrating these ASR processing techniques into these waste streams allows recyclers to improve material recovery rates while minimizing reliance on landfills. Furthermore, the increasing need for sustainable and recycled raw materials in manufacturing opens prospects for revenue generation. The growth of efficient recycling processes for electronics waste and composites will aid in sustainability alongside profitability for the ASR sector.

Challenges

-

Concerns over the quality, consistency, and performance of ASR-derived materials hinder their acceptance in industrial applications.

Public perception and industry hesitation toward ASR-derived materials stem from concerns about their quality, consistency, and usability in industrial applications. And many manufacturers are hesitant to use recycled ASR components because of possible impurities, structural weaknesses, and performance limits compared to virgin materials. In addition, a lack of consistent processing techniques leads to inconsistency in recovered materials, which hampers larger adoption. Specific sectors, including automotive, construction, and manufacturing, demand stringent material specifications, which make it difficult for products based on ASR to be accepted. Consumer skepticism about how durable and safe recycled materials are also hampers demand. Additionally, resistance from both the public and industrial sectors is driven by a lack of understanding and knowledge of advanced processing technologies for ASR. This is necessary due to increased investment in quality control, regulatory benefits, and technological development to enhance ASR material QXRG. Developing robust relationships with the industry and showcasing the economic and environmental advantages of recycling ASR will help drive change in this sector and bring growth to the market.

Automotive Shredded Residue (ASR) Market Segmentation Analysis

By Application

The landfill segment dominated with a market share of over 42% in 2023, due to the significant volume of non-recyclable materials generated from vehicle dismantling. Many elements, like mixed plastics, rubber, and some composites, are hard to separate and reuse effectively. And large-scale recycling is constrained by the absence of infrastructure for advanced recovery. In short, landfilling is the most convenient way to get rid of it. Although stricter landfill regulations exist in some areas, traditional waste management is still common in many countries, where they are not only cheaper but also logistically easier. But growing environmental concerns and more stringent regulations are spurring other approaches for other solutions like energy recovery and advanced material sorting, and these solutions may also decrease landfill reliance in the upcoming years.

By Composition

The Plastics segment dominated with a market share of over 38% in 2023. With increasing environmental worries and strict recycling requirements, there is a significant shift toward recovering and reusing plastic to lessen dependence on landfills. Innovations in sorting and separation technologies, including AI-driven optical sorting and chemical recycling, are also enabling the effective extraction of plastics from ASR. Moreover, the increasing adoption of circular economy models by automakers, as well as international regulatory mandates for sustainable material usage, will ensure the segment’s potent growth. To bring that to life, we have innovations and developments in bio-based and recyclable plastics as solutions to bring the people to a higher recovery rate and less environmental impact from ASR.

By Technology

The magnetic separation segment dominated with a market share of over 34% in 2023, due to its effectiveness in recovering ferrous metals, which make up a large share of ASR. With its efficiency, affordability, and widespread use among companies involved in metal recycling, it is no wonder that the top-tier clubs in the sport reside there. Nonetheless, it is the developments in optical sorting driven by artificial intelligence (AI) recognition and sensor developments in sorting that are emerging as the fastest-growing segment. Non-ferrous metals, valuable materials (like plastics), and even shredded tires will also be more efficiently recovered due to this technology. Increasing regulatory push, stricter landfill regulations, and the global transition toward a circular economy are propelling the adoption of accurate ASR separation technologies, with optical sorting being a primary point of innovation and investment within the market.

Automotive Shredded Residue (ASR) Market Regional Outlook

The North America region dominated with a market share of over 42% in 2023, owing to a highly developed auto recycling sector, stringent environmental policies, and a greater emphasis on sustainable material recovery. The region enjoys a well-established system of shredding facilities, metal recovery plants, and advanced separation technologies, facilitating effective ASR processing. It is further strengthening its leadership with high vehicle scrappage rates, driven by strict end-of-life vehicle (ELV) regulations. It also helps explain why North America leads, including through an abundance of large recycling firms and tech innovators. The ongoing industry focus towards building advanced sorting and metal extraction systems and government-level incentives for advanced circular economy initiatives are other important factors fuelling the growth of ASR recycling in North America, which is becoming a world hub for sustainable waste solutions.

Asia-Pacific is the fastest-growing region in the Automotive Shredded Residue (ASR) Market, due to the rapidly accelerating speed of industrialization, growth in the car dismantling process, and increasing investments aimed toward recycling technologies. Rising automotive sector and growing environmental concerns in countries such as China, India, and Japan are driving the ASR processing market. More stringent waste management regulations and policies encouraging sustainable material recovery are driving industries toward better advanced recycling solutions. Moreover, government-backed initiatives that promote circular economy practices are also driving the development of efficient ASR sorting and recovery infrastructure. Rising demand for high-value recovered materials, coupled with the development of AI-driven separation technologies further propelling the ASR market growth in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Tomra Systems ASA (Sensor-based sorting systems)

-

Galloo (Metal recycling, post-shredder technology)

-

Sims Limited (Metal recycling, ferrous & non-ferrous recovery)

-

MBA Polymers Inc. (Recycled plastics, polymer separation)

-

Binder+Co. (Screening, sensor-based sorting equipment)

-

PLANIC (ASR processing solutions)

-

Axion Ltd (Resource recovery, plastic recycling)

-

SRW metal float GmbH (Metal separation technologies)

-

Machinex Industries Inc. (Sorting systems, material recovery facilities)

-

Wendt Corporation (Shredders, separation technologies)

-

CP Manufacturing Inc. (Recycling equipment, advanced sorting systems)

-

BT-Wolfgang Binder GmbH (Material handling, processing equipment)

-

Agilyx (Plastic waste conversion technologies)

-

Steinert (Magnetic and sensor-based sorting systems)

-

Eriez Manufacturing Co. (Magnetic separators, metal detectors)

-

Bezner (Waste management, sorting systems)

-

Sesotec GmbH (Sorting, detection systems for recycling)

-

Picvisa (Optical sorting, robotic waste recovery)

-

Fornnax Technology Pvt Ltd (Shredders, granulators)

-

Lindner Washtech (Washing and sorting systems for plastics)

Suppliers for (metal recycling and ASR treatment, specializing in recovering ferrous and non-ferrous metals), Automotive Shredded Residue (ASR) Market

-

Galloo

-

MBA Polymers Inc.

-

Sims Limited

-

Tomra Systems ASA

-

STEINERT

-

SGM Magnetics

-

ELDAN Recycling

-

All controls

-

Ruijie Equipment

-

American Pulverizer Company

Recent Development

In June 2023, Galloo (Belgium) announced a joint venture with Stellantis (Netherlands) to advance end-of-life vehicle recycling. The service, set to launch in late 2023, will initially target France, Belgium, and Luxembourg, with plans for further expansion across Europe.

In January 2023, Wendt Corporation (US) partnered with Proman Infrastructure Services Ltd. (India) to establish Wendt Proman Metal Recycling Pvt. Ltd. This venture aims to tap into India’s growing demand for shredding and separation technologies in the recycling sector.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 5.98 Billion |

| Market Size by 2032 | USD 8.93 Billion |

| CAGR | CAGR of 4.55% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Landfill, Energy Recovery, Recycling) • By Composition (Metals, Plastics, Rubber, Textile, Others) • By Technology (Air Classification, Optical Sorting, Magnetic Separation, Eddy Current Separation, Screening, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Tomra Systems ASA, Galloo, Sims Limited, MBA Polymers Inc., Binder+Co., PLANIC, Axion Ltd, SRW metal float GmbH, Machinex Industries Inc., Wendt Corporation, CP Manufacturing Inc., BT-Wolfgang Binder GmbH, Agilyx, Steinert, Eriez Manufacturing Co., Bezner, Sesotec GmbH, Picvisa, Fornnax Technology Pvt Ltd, Lindner Washtech |

Frequently Asked Questions

North America dominated the Automotive Shredded Residue (ASR) Market in 2023

The “landfill” segment dominated the Automotive Shredded Residue (ASR) Market.

Stringent global ELV recycling regulations are driving the growth of the ASR market by boosting demand for advanced material recovery solutions.

The Automotive Shredded Residue (ASR) Market was USD 5.98 billion in 2023 and is expected to reach USD 8.93 billion by 2032.

The Automotive Shredded Residue (ASR) Market is expected to grow at a CAGR of 4.55% from 2024-2032.

Get in Touch