Ballast Water Treatment Market Report Scope & Overview:

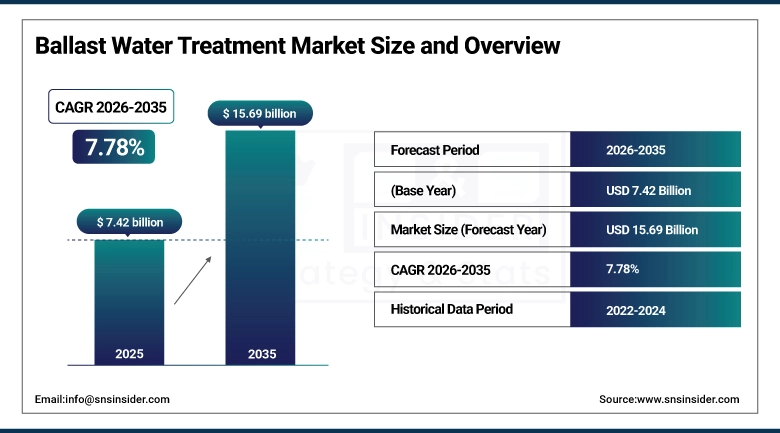

The Ballast Water Treatment Market size was valued at USD 7.42 Billion in 2025 and is projected to reach USD 15.69 Billion by 2035, growing at a CAGR of 7.78% during 2026–2035.

The Ballast Water Treatment Market primarily includes technologies that eliminate or inactivate harmful aquatic life carried in ballast water, which causes an imbalance of flora and fauna. The Ballast Water Treatment Market has experienced growth with the implementation of stringent international norms, awareness of the environment, and the need for a green environment. Advanced treatment systems are employed, which include filtration, UV, and chemical treatment, thus contributing significantly to the growth of the Ballast Water Treatment Market. Innovation, digital monitoring, and retrofitting activities are also contributing to the growth of the Ballast Water Treatment Market.

Ballast Water Treatment Market Size and Growth:

-

Market Size in 2025: USD 7.42 Billion

-

Market Size by 2035: USD 15.69 Billion

-

CAGR: 7.78% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Ballast Water Treatment Market - Request Free Sample Report

Ballast Water Treatment Market Key Trends:

-

Increasing adoption of UV-based and chemical-free ballast water treatment systems due to stricter environmental regulations

-

Rising retrofitting of existing vessels to comply with IMO Ballast Water Management Convention

-

Growing demand for energy-efficient and low-maintenance treatment technologies among ship operators

-

Integration of digital monitoring and automation for real-time system performance and compliance tracking

-

Expansion of global maritime trade and fleet size driving installation of advanced ballast water management systems

U.S. Ballast Water Treatment Market Size Outlook:

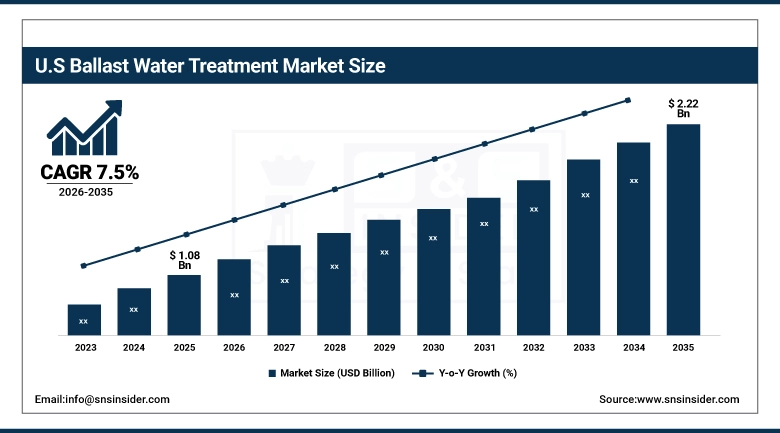

The U.S. Ballast Water Treatment Market has been valued at USD 1.08 Billion in 2025 and is expected to reach USD 2.22 Billion in 2035, growing at a CAGR of 7.5% from 2026 to 2035, Growth is driven by strict U.S. Coast Guard regulations, increasing vessel retrofitting, rising maritime trade, adoption of advanced treatment technologies, and growing emphasis on marine ecosystem protection and regulatory compliance.

Ballast Water Treatment Market Drivers:

-

Stringent International Environmental Regulations Propel the Demand for Advanced Ballast Water Treatment Solutions Globally.

International laws like the IMO’s Ballast Water Management Convention have made it mandatory for ballast water treatment systems to be fitted, which will prevent the spread of invasive species. This has created a global demand for better treatment systems like UV treatment and electro chlorination systems. This has made it more complex for ship operators to find better, more effective, but at the same time reliable, as well as environmentally friendly solutions, which has created a huge Ballast Water Treatment Market Growth.

Ballast Water Treatment Market Restraints:

-

Limited Availability of Skilled Technicians for Installation and Maintenance Hampers Efficient Adoption of Treatment Systems.

Installation, tuning, and maintenance of the systems require technically competent experts for a successful rollout of BWTS. Marine engineers and marine technicians who have been exposed to training in this field are not readily available, as there are several technologies involved in BWTS globally. The lack of qualified manpower in this field has led to a delay in the development, increased hazards, and a rise in the cost of training. The lack of workers is a barrier in the free flow of the market, even as retrofits continue.

Ballast Water Treatment Market Opportunities:

-

Technological Advancements in Compact and Energy-Efficient Systems Offer New Growth Opportunities Across Vessel Types.

UV-C LEDs, filtration-free technologies, and chemical-free disinfection technologies are changing the Ballast Water Treatment Industry as we know it. These advanced generation technologies have smaller footprints, lower power requirements, and easier retrofit potential. With ship owners looking to invest in reliable, cost-effective, and green technologies, those offering new-gen technologies would reap the benefits of having a competitive edge in the market and receiving more orders.

Ballast Water Treatment Market Segments:

-

By Vessel Type: In 2025, Stationary systems dominated with 72% share; Portable systems fastest growing segment during 2026–2035

-

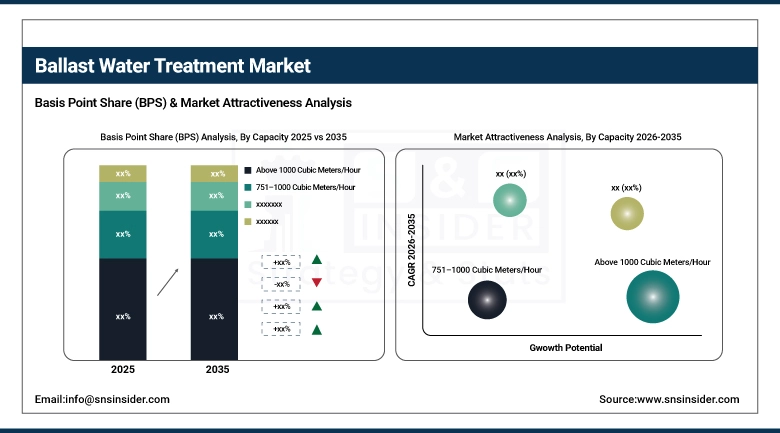

By Capacity: In 2025, Above 1000 Cubic Meters/Hour dominated with 38% share; 250–500 Cubic Meters/Hour fastest growing segment during 2026-2035

-

By Vessel Type: In 2025, Bulk Carriers dominated with 29% share; Container Ships fastest growing segment during 2026-2035

-

By System Type: In 2025, UV Treatment dominated with 41% share; Chemical Disinfection fastest growing segment during 2026-2035

By Vessel Type: Stationary Systems Dominate, Portable Systems Fastest-Growing

Stationary systems hold the highest share in the vessel segment, which is approximately 72%, mainly because they are widely installed in large commercial vessels. Stationary systems are meant to operate permanently, making them highly efficient in ballast water treatment in accordance with IMO regulations. The increase in retrofitting operations on existing fleets and the obligatory implementation of ballast water treatment systems in global maritime operations have enhanced the position of stationary systems.

Portable systems have the highest growth rate, mainly because they are cost-effective and flexible, particularly in smaller vessels. The popularity of portable systems is growing, particularly in ship operations where temporary ballast water treatment is needed, thus making them highly sought after by ship owners seeking to avoid costly retrofitting operations. They are highly suitable for vessels in less regulated operations, particularly in regional operations.

By Capacity: Above 1000 Cubic Meters/Hour Dominate, 250–500 Cubic Meters/Hour Fastest-Growing

Systems with a capacity greater than 1000 cubic meters per hour hold the largest share in the market, estimated at 38%, as they are mostly used in large ships such as bulk carriers, oil tankers, and container ships. These ships require large-capacity ballast water treatment systems to treat large quantities of ballast water. The rise in maritime trade across the globe and the use of large ships to transport goods have contributed to the large share held by this category.

The 250-500 cubic meters per hour category is growing at the fastest rate due to the growing demand from medium-sized ships and regional shipping. This category offers the best option to shipping companies looking to comply with regulations without incurring high costs. The expansion in short-distance maritime trade also contributes to the growth in this category.

By Vessel Type: Bulk Carriers Dominate, Container Ships Fastest-Growing

The largest share of 29% is held by bulk carriers in the vessel type category. This is because bulk carriers are used to transport large quantities of materials such as coal, iron ore, and grains over large distances. This results in the frequent exchange of ballast water. This category has the largest number of vessels in operation across the world. Also, ballast water management systems were first installed in bulk carriers.

Container ships constitute the fastest-growing category. This is owing to the rapid expansion in global trade and e-commerce. Investments in container ships are on the rise. This is in addition to the growing need to transport goods efficiently. There is also a growing need to implement advanced ballast water treatment systems in container ships. This is owing to environmental regulations.

By System Type: UV Treatment Dominates, Chemical Disinfection Fastest-Growing

UV treatment systems lead the market in terms of market share, which is approximately 41%. This is due to their effectiveness, safety, and low chemical usage. These systems use ultraviolet light to kill microorganisms, thus being highly compliant with international environmental regulations. The low complexity of UV systems has made them the preferred choice among ship operators, as it is also eco-friendly.

Chemical disinfection systems are growing at a rapid rate due to their high disinfection potential. These systems can be used in high-capacity ships as they are effective in handling high volumes of ballast water. These systems can be used in varying water conditions. Advances in technology, which focus on minimizing chemical residues, have increased their use in high-capacity ships.Top of FormBottom of Form

Ballast Water Treatment Market Regional Analysis:

Asia-Pacific Ballast Water Treatment Market Insights:

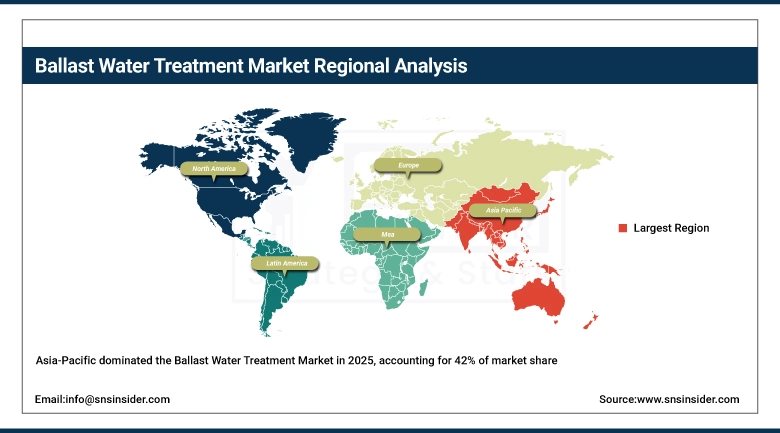

Asia-Pacific is the leader in the Ballast Water Treatment Market with a global market share of 42% in 2025. This is because this region has a strong base for shipbuilding in China, South Korea, and Japan, which contribute to a large proportion of global shipbuilding. In addition to this, a large number of commercial vessels and increasing trade activities in this region are also driving the Ballast Water Treatment Market. Furthermore, strong compliance with IMO regulations and increasing retrofitting activities are also driving the Ballast Water Treatment Market in this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Ballast Water Treatment Market Insights:

The North American market is growing at a rapid pace in the Ballast Water Treatment Market. It is expected to grow at a CAGR of 8.59% over the forecast period, i.e., 2026-2035. This is because of the stringent implementation of US Coast Guard regulations on ballast water management. Moreover, there is an increased need to comply with regulations for both domestic and international ships. The North American market is seeing an increase in retrofitting existing ships as well as the implementation of advanced technologies for efficient ballast water management. Strong maritime trade activity is also contributing to the growth. Investments are being made in developing infrastructure at ports.

Europe Ballast Water Treatment Market Insights:

The need for ballast water treatment market in the Europe region is critical, considering the high level of environmental regulation imposed and the high level of enforcement in this area. The forward looking nature of the EU in marine ecosystem preservation has also catalyzed the significant market for sophisticated ballast water treatment systems. In addition, the technology providers and system manufacturers also find their place in the market. Factors such as increasing retrofitting of aging fleets, a maturing maritime industry, and high awareness of the problem of invasive species are also driving the market in the region.

Latin America Ballast Water Treatment Market Insights:

Latin America is expected to show substantial growth of ballast water treatment market, however, it will happen more steadily as maritime trade will be stimulating significantly and implementation of international ballast water conventions will be moving slowly. Brazil and Mexico and other Latin American nations are investing in port modernization as well as commitment to IMO conventions. Furthermore, Ballast Water Treatment Market is also driven by growth in oil & gas, and bulk shipping activities in Latin America. In addition, a greater emphasis on marine ecosystem protection and invasive species prevention is also driving a trend for shipping operators to choose Ballast Water Management systems.

Middle East & Africa (MEA) Ballast Water Treatment Market Insights:

Middle East region is supported by the booming maritime trade are expected to be the factors driving robust growth for Ballast Water treatment market across Middle East & Africa. Gulf, including UAE and Saudi Arabian countries are at forefront in investing their efforts to renew their port infrastructure and renew the fleet to modern fleet which is increasing the ballast water treatment systems market for the sure. Furthermore, increasing compliance with IMO regulations and increasing awareness of marine environmental protection are also bolstering market growth on critical shipping route and energy transport routes.

Ballast Water Treatment Market Competitive Landscape:

Founded in 1883, Alfa Laval is a Swedish company, and global leader within the development of specialized products and engineering downstream solutions. Ceres Technologies develops, manufactures, and integrates technologies that drive efficiency, sustainability, and environmentally-friendly compliance across the energy, marine, and food & water industries. Alfa Laval is a manufacturer of a range of heat transfer, separation and fluid handling products, and has a sizeable marine business, including ballast water treatment systems. Operating in more than 100 countries and serving the industrial and commercial markets globally.

-

In March 2024, Alfa Laval strengthened its marine environmental solutions portfolio by advancing its ballast water treatment technologies, focusing on energy efficiency and compliance with evolving IMO regulations for global shipping fleets.

Wärtsilä Corporation was established in 1834 and is a Finland-based global leader in smart technologies and lifecycle solutions for the marine and energy markets. The company provides a wide range of products including engines, power systems, and environmental solutions designed to optimize vessel performance and reduce emissions. Wärtsilä is a key player in ballast water treatment systems, offering advanced solutions that support regulatory compliance and sustainable marine operations. The company operates in more than 80 countries and has a strong global service network.

-

In May 2024: Wärtsilä enhanced its ballast water management systems by introducing digital monitoring and optimization features, aimed at improving operational efficiency and ensuring compliance with international environmental standards.

Ballast Water Treatment Companies are:

-

Alfa Laval

-

Xylem Inc.

-

Veolia Water Technologies

-

Mitsubishi Heavy Industries Ltd.

-

Optimarin AS

-

Ecochlor Inc.

-

Hyde Marine Inc.

-

Panasia Co., Ltd.

-

Samsung Heavy Industries

-

NK Co., Ltd.

-

JFE Engineering Corporation

-

Sunrui Marine Environment Engineering Co., Ltd.

-

ERMA FIRST ESK Engineering Solutions S.A.

-

Desmi A/S

-

Headway Technology Group (Qingdao) Co., Ltd.

-

OceanSaver AS

-

Aquarius Marine Co., Ltd.

-

Techcross Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.42 Billion |

| Market Size by 2035 | USD 15.69 Billion |

| CAGR | CAGR of 7.78% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application: (Stationary, Portable) • By Capacity: (below 250 cubic meters per hour, 250–500 cubic meters per hour, 501–750 cubic meters per hour, 751–1000 cubic meters per hour, above 1000 cubic meters per hour) • By Vessel Type: (Bulk Carriers, Oil Tankers, Container Ships, General Cargo Ships, Gas Carriers, Cruise Ships) • By System Type: (Filtration, Chemical Disinfection, UV Treatment, Deoxygenation, Heat Treatment, Ultrasonic Treatment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Alfa Laval, Wärtsilä Corporation, Xylem Inc., Veolia Water Technologies, Mitsubishi Heavy Industries Ltd., Optimarin AS, Ecochlor Inc., Hyde Marine Inc., BIO-UV Group, Panasia Co., Ltd., Samsung Heavy Industries, NK Co., Ltd., JFE Engineering Corporation, Sunrui Marine Environment Engineering Co., Ltd., ERMA FIRST ESK Engineering Solutions S.A., Desmi A/S, Headway Technology Group (Qingdao) Co., Ltd., OceanSaver AS, Aquarius Marine Co., Ltd., Techcross Inc. |

Frequently Asked Questions

The Ballast Water Treatment Market is expected to grow at a CAGR of 7.78% during 2026–2035.

The market was valued at USD 7.42 Billion in 2025 and is projected to reach USD 15.69 Billion by 2035.

The key drivers of the Ballast Water Treatment Market include stringent IMO regulations, increasing vessel retrofitting, expanding global maritime trade, rising concerns over invasive aquatic species, and adoption of advanced, energy-efficient treatment technologies.

The UV Treatment segment dominated during the projected period.

Asia-Pacific dominated the Ballast Water Treatment Market in 2025.

Get in Touch