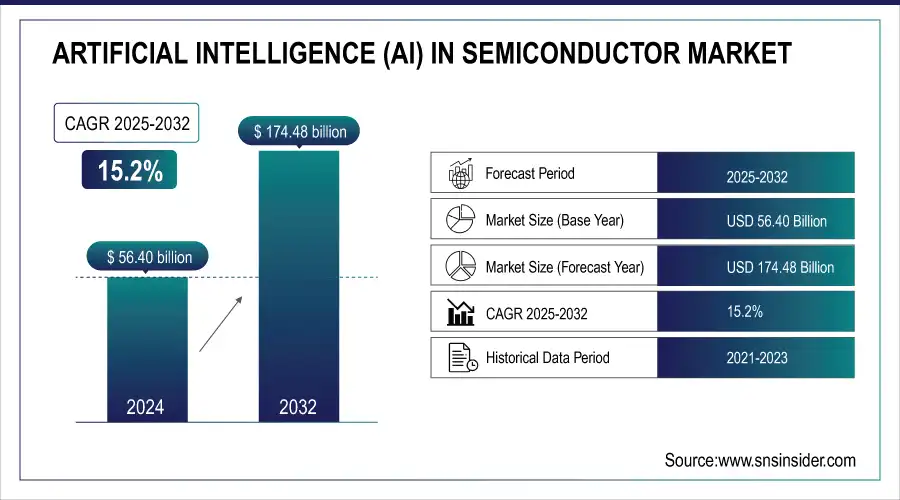

Artificial Intelligence (AI) in Semiconductor Market Size:

The Artificial Intelligence (AI) in Semiconductor Market Size was valued at USD 56.40 Billion in 2024 and is expected to reach USD 174.48 Billion by 2032 and grow at a CAGR of 15.2% over the forecast period 2025-2032.

To get more information on Artificial Intelligence (AI) in Semiconductor Market - Request Free Sample Report

The market can be further enhanced with data on the adoption of AI technologies across various industries. For example, the rate of AI integration in sectors such as healthcare (e.g., adoption of AI in diagnostics), automotive (e.g., penetration of chips in autonomous vehicles), and consumer electronics. Additionally, statistics on R&D investment in AI chip development, the number of AI-related startups, and the volume of AI semiconductor patents filed can offer valuable insights into innovation trends and the market's future trajectory.

Market Size and Forecast:

-

Market Size in 2024 USD 56.40 Billion

-

Market Size by 2032 USD 174.48 Billion

-

CAGR of 15.2% From 2025 to 2032

-

Base Year 2024

-

Forecast Period 2025-2032

-

Historical Data 2021-2023

Artificial Intelligence (AI) in Semiconductor Market Trends:

-

Growing adoption of AI technologies across healthcare, automotive, and consumer electronics is driving demand for AI-optimized semiconductors.

-

AI-based applications such as diagnostics, autonomous driving, and smart devices are increasing the need for high-performance processors.

-

Rising emphasis on automation, real-time data processing, and decision-making fuels AI semiconductor market growth.

-

Strategic partnerships among major semiconductor companies accelerate development of next-generation AI chips.

-

Collaboration-driven innovations focus on improving computational power, energy efficiency, and real-time processing capabilities in AI chips.

Artificial Intelligence (AI) in Semiconductor Market Growth Drivers:

-

Expanding Adoption of AI Applications in Key Industries Fuels Growth of the Artificial Intelligence (AI) in Semiconductor Market

The increasing use of AI technologies across diverse industries such as healthcare, automotive, and consumer electronics is a major driver of the AI in Semiconductor Market. AI solutions are being integrated into critical applications such as AI-based diagnostics in healthcare, autonomous driving in the automotive sector, and smart devices in consumer electronics. These advancements require high-performance semiconductor chips, propelling the demand for AI-optimized processors. As businesses seek to enhance automation, data processing, and real-time decision-making, the semiconductor market for AI chips is experiencing rapid expansion.

Artificial Intelligence (AI) in Semiconductor Market Restraints:

-

Supply Chain Disruptions and High Manufacturing Costs Limiting Growth in the Artificial Intelligence (AI) in Semiconductor Market

While the AI in Semiconductor Market shows promise, supply chain disruptions and high manufacturing costs present significant barriers to growth. The complexity of producing AI-specific semiconductors, such as GPUs and ASICs, requires advanced fabrication technologies and raw materials that are often in limited supply. Additionally, the increasing demand for cutting-edge AI chips has caused delays in production and shipping, leading to higher costs. Semiconductor manufacturers are also facing difficulties in scaling production to meet global demand, impacting the overall growth of the AI semiconductor sector.

Artificial Intelligence (AI) in Semiconductor Market Opportunities:

-

Strategic Partnerships and Collaborations Drive Innovation in AI Chip Development for the Semiconductor Market

Strategic collaborations between semiconductor giants like Intel, Nvidia, and Amazon Web Services (AWS) present a significant opportunity for the AI in Semiconductor Market. These partnerships are focused on developing next-generation AI chips that improve computational power, energy efficiency, and real-time processing capabilities. By leveraging combined expertise, research, and resources, companies can accelerate AI semiconductor innovations and meet the increasing demand for AI-powered applications. As a result, these collaborations are poised to shape the future of AI chip development and offer new growth avenues in the semiconductor market.

Artificial Intelligence (AI) in Semiconductor Market Segment Analysis:

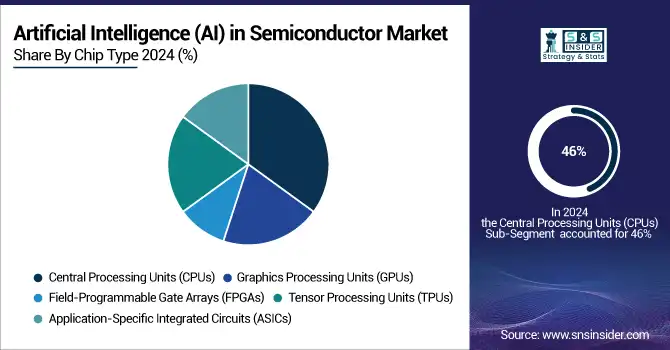

By Chip Type

In 2024, the Central Processing Units (CPUs) segment held the largest revenue share of 46% in the AI semiconductor market, driven by their essential role in powering AI applications across industries. Companies like Intel and AMD are leading this segment with significant advancements in CPU technology tailored for AI workloads. For instance, Intel’s Xeon Scalable Processors and AMD’s Ryzen AI chips have been optimized to handle AI tasks such as data processing and machine learning. Intel's recent push towards integrating AI acceleration into its Xeon processors for AI-based inference applications shows its commitment to supporting AI innovations.

The Graphics Processing Units (GPUs) segment is experiencing significant growth, with a projected CAGR of 16.64% during the forecasted period, due to their ability to efficiently handle complex AI workloads, such as deep learning and neural networks. GPUs are designed for parallel processing, making them ideal for the high computational demands of AI algorithms. Major companies like Nvidia and AMD are leading this segment. Nvidia’s A100 Tensor Core GPUs and H100 GPUs are specifically designed for AI applications, offering massive computational power for AI training and inference. Nvidia's Jetson AGX Orin platform also targets edge AI devices, enabling real-time AI computations in robotics and autonomous vehicles.

By Application

In 2024, the AI Training segment captured the largest revenue share of 39% in the AI semiconductor market, driven by the increasing demand for high-performance hardware to power AI model training. AI training involves processing massive datasets and complex algorithms, which require specialized hardware like Graphics Processing Units (GPUs), Tensor Processing Units (TPUs), and FPGAs. Companies like Nvidia with its A100 and H100 Tensor Core GPUs, and Google with its TPU v4, have been at the forefront of product development in this space.

The Edge AI segment is projected to grow at the highest CAGR of 17.19% within the forecast period, driven by the growing need for AI-enabled devices that perform data processing locally, reducing latency and dependency on cloud services. Companies like Qualcomm and Nvidia have launched innovative products tailored to edge computing. Qualcomm's Snapdragon AI Engine and Nvidia’s Jetson Orin platform are specifically designed to enable real-time AI inferencing on edge devices such as autonomous vehicles, smart cameras, and IoT devices.

By End-use

In 2024, the Consumer Electronics segment dominated the AI semiconductor market with the largest revenue share of 35%, driven by the increasing adoption of AI in smartphones, wearables, and smart home devices. AI chips are integral in enabling smart features like voice recognition, facial recognition, and real-time image processing in consumer devices. Apple’s A16 Bionic chip and Samsung’s Exynos AI chips are examples of processors that support AI-based functionalities in their smartphones and wearables, enhancing user experience through intelligent voice assistants and personalized features.

The Automotive segment is witnessing the largest CAGR of 16.77% in the forecasted period, reflecting the growing integration of AI technologies in autonomous vehicles and advanced driver assistance systems (ADAS). The adoption of AI-powered in-car assistants, navigation systems, and safety features is propelling the demand for high-performance semiconductors. AI chips in automotive applications are responsible for processing data from LiDAR, radar, and cameras, enabling vehicles to understand their surroundings and make intelligent decisions.

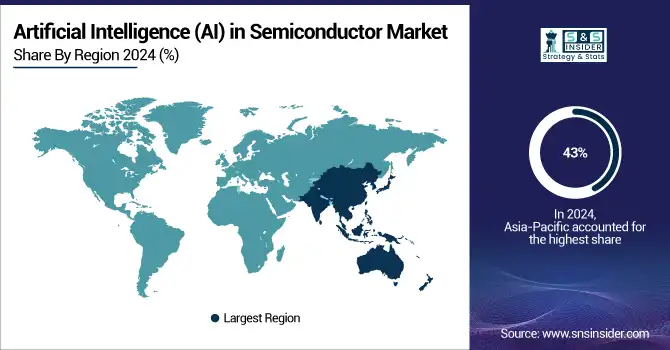

Artificial Intelligence (AI) in Semiconductor Market Regional Analysis:

Asia Pacific Artificial Intelligence (AI) in Semiconductor Market Insights

In 2024, the Asia Pacific (APAC) region held a dominant position in the Artificial Intelligence (AI) Semiconductor Market, with an estimated market share of approximately 43%. The region's leadership can be attributed to the presence of major semiconductor manufacturers like Samsung Electronics, TSMC, and Nvidia, as well as a robust demand for AI technologies in industries such as consumer electronics, automotive, and healthcare. China and South Korea are key players in this market, with rapid advancements in AI-based consumer electronics and automated manufacturing.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Artificial Intelligence (AI) in Semiconductor Market Insights

In 2024, North America emerged as the fastest-growing region in the AI in Semiconductor Market, with an estimated CAGR of 16.8% during the forecast period. The region’s rapid growth can be attributed to advanced AI research and development led by major tech companies and startups based in the U.S. Nvidia, Intel, and Google are at the forefront of AI chip innovation, developing cutting-edge GPUs, TPUs, and specialized processors for AI training and inference applications. For instance, Nvidia’s H100 Tensor Core GPUs are specifically designed for AI workloads and have seen wide adoption in data centers and AI research.

Europe Artificial Intelligence (AI) in Semiconductor Market Insights

Europe’s AI semiconductor market is driven by increasing adoption of AI across industries such as automotive, healthcare, and consumer electronics. Investments in AI research, strong government support for innovation, and the presence of leading semiconductor players accelerate market growth. The focus on energy-efficient, high-performance AI chips for cloud computing, edge devices, and industrial applications further strengthens the region’s market expansion.

Latin America (LATAM) and Middle East & Africa (MEA) Artificial Intelligence (AI) in Semiconductor Market Insights

The AI semiconductor market in LATAM and MEA is growing due to rising digitalization, industrial automation, and AI adoption in automotive, healthcare, and consumer electronics sectors. Expanding data centers, cloud infrastructure, and government initiatives for technological advancement boost demand. Increasing investments in AI chip development and local manufacturing capabilities are creating opportunities for market growth across these emerging regions.

Artificial Intelligence (AI) in Semiconductor Market Key Players:

Some of the Artificial Intelligence (AI) in Semiconductor Market Companies are

-

Nvidia Corporation (Nvidia A100 Tensor Core GPU, Nvidia Jetson AGX Orin)

-

Intel Corporation (Intel Gaudi2 AI Accelerator, Intel Xeon Scalable Processors)

-

Advanced Micro Devices, Inc. (AMD Instinct MI300, AMD Ryzen AI)

-

Xilinx, Inc. (Xilinx Versal AI Core, Xilinx Alveo U50)

-

Google Inc. (Alphabet Inc.) (Google TPU v5e, Google Edge TPU)

-

Qualcomm Incorporated (Qualcomm Cloud AI 100, Qualcomm Snapdragon AI Engine)

-

IBM Corporation (IBM AIU (AI Unit), IBM Watson Machine Learning Accelerator)

-

Samsung Electronics Co., Ltd. (Samsung Exynos AI, Samsung HBM-PIM)

-

Huawei Technologies Co., Ltd. (Huawei Ascend 910, Huawei Kunpeng AI Processor)

-

Amazon Web Services, Inc. (AWS Inferentia, AWS Trainium)

-

Broadcom Inc. (Broadcom Trident AI Switch, Broadcom Jericho3-AI)

-

Texas Instruments (TI TDA4VM Processor, TI AM62A AI Vision Processor)

-

MediaTek Inc. (MediaTek Dimensity AI, MediaTek NeuroPilot)

-

Arm Holdings (Arm Cortex-M85, Arm Ethos-U65)

-

Synopsys, Inc. (Synopsys DSO.ai, Synopsys ARC EV Processors)

Competitive Landscape for Artificial Intelligence (AI) in Semiconductor Market:

Nvidia Corporation is a global leader in AI-focused semiconductors, offering GPUs and AI accelerators such as the A100 Tensor Core and Jetson AGX Orin. Its products enable high-performance computing, machine learning, and deep learning applications across industries including healthcare, automotive, and data centers. Nvidia’s innovations in AI chip design, energy efficiency, and parallel processing capabilities drive advancements in real-time analytics, autonomous systems, and cloud AI solutions, strengthening its position in the AI semiconductor market.

-

In December 2024, Ibiden Co., a key supplier of chip package substrates for Nvidia Corp., considered accelerating its production capacity expansion to meet the surging demand for AI applications. CEO Koji Kawashima noted that sales of AI-use substrates were robust, with customers purchasing all available stock.

Intel Corporation is a leading semiconductor company providing AI-optimized processors, including Xeon Scalable CPUs and Gaudi2 AI accelerators. Its solutions support high-performance computing, machine learning, and deep learning across industries such as healthcare, automotive, and cloud computing. Intel focuses on enhancing computational power, energy efficiency, and real-time processing capabilities, enabling enterprises to deploy AI applications effectively and solidifying its position in the global AI semiconductor market.

-

In September 2024, Intel Corporation and Amazon Web Services (AWS) expanded their strategic collaboration to enhance U.S.-based chip manufacturing. Intel agreed to produce a custom AI fabric chip for AWS using its advanced Intel 18A process node and a custom Xeon 6 chip on Intel 3.

| Report Attributes | Details |

| Market Size in 2024 | USD 56.40 Billion |

| Market Size by 2032 | USD 174.48 Billion |

| CAGR | CAGR of 15.2% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chip Type (Central Processing Units (CPUs), Graphics Processing Units (GPUs), Field-Programmable Gate Arrays (FPGAs), Application-Specific Integrated Circuits (ASICs), Tensor Processing Units (TPUs)) • By Application (AI Training, AI Inference, Edge AI, Cloud AI, Others) • By End-use (Healthcare, Automotive, Consumer Electronics, Industrial Automation, Banking and Finance, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nvidia Corporation, Intel Corporation, Advanced Micro Devices, Inc., Xilinx, Inc., Google Inc. (Alphabet Inc.), Qualcomm Incorporated, IBM Corporation, Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., Amazon Web Services, Inc., Broadcom Inc., Texas Instruments, MediaTek Inc., Arm Holdings, Synopsys, Inc. |

Frequently Asked Questions

Ans: Asia Pacific dominated the Artificial Intelligence (AI) in Semiconductor Market in 2024.

Ans: The Central Processing Units (CPUs) segment dominated the AI Semiconductor Market.

Ans: The major growth factor of Artificial Intelligence in Semiconductor Market is the increasing demand for high-performance AI chips to support advanced applications in industries like automotive, healthcare, and consumer electronics.

Ans: The Artificial Intelligence (AI) in Semiconductor Market Size was valued at USD 56.40 Billion in 2024 and is expected to reach USD 174.48 Billion by 2032 and grow at a CAGR of 15.2% over the forecast period 2025-2032

Ans: The AI in Semiconductor Market is expected to grow at a CAGR of 15.2% during 2025-2032.

Get in Touch