BATTERY-AS-A-SERVICE MARKET KEY INSIGHTS:

To get more information on Battery-as-a-Service Market - Request Sample Report

The Battery-as-a-Service Market Size was valued at USD 3.02 Billion in 2023 and is expected to reach USD 13.50 Billion by 2032 and grow at a CAGR of 18.15% over the forecast period 2024-2032.

Battery-as-a-Service Market is gaining significant traction as industries seek to innovate in addressing the challenges of energy storage, sustainability, and mobility. Users are now renting batteries instead of buying them outright; this offers flexibility and decreases upfront costs, which is most popular in automotive and transport, energy, and industrial applications where demand for effective and sustainable energy solutions is rising.

In countries such as the United States, China, and Europe, governments are implementing policies which support electric vehicles and renewable energy sources directly aligned to the growth of Battery-as-a-Service. The US Administration's incentivizing EVs and infrastructure investment is another key driver for this sector. In the U.S. Tax incentives and subsidies in the pursuit of increased EV adoption created fertile ground for growth in the Battery-as-a-Service service provider sector, particularly in the automotive segment. China is another key market that has established an aggressive EV policy framework, with mandated battery swapping standards and incentives to manufacturers who adapt to Battery-as-a-Service models, making it a global leader in battery-as-a-service.

Recent developments in battery technology are also driving the Battery-as-a-Service market. Improvement in Battery Lifecycle Management and Swapping Technology ensures faster, more efficient battery replacement with higher customer convenience levels. Companies are now developing modular batteries that can easily swap out in EVs, so the vehicle is always operational for most of the time. Time down is minimized, and the overall efficiency of the vehicle increases. New innovations such as Solid-State Batteries and Fast-Charging Technology in the energy storage sector play a huge role in extending the life of the battery while improving energy density that can make Battery-as-a-Service viable across industries.

There is much potential for Battery-as-a-Service unlocking very significant opportunities within the near future, especially for Renewable Energy and Grid Storage. Decarbonization is gaining rapid attention all over the world, and thus the need for scalable energy solutions going to grow exponentially. Scalable energy solutions can be managed by the energy providers and industrial users efficiently through Battery-as-a-Service. This flexibility can then also be transferred to new industrialization processes that may not have even been considered before, like the residential energy storage sector. For example, here, leasing batteries can help reduce the burden the family would have with regard to the installation of such solar energy-generating systems.

MARKET DYNAMICS

KEY DRIVERS:

-

Increasing adoption of EVs necessitates flexible battery leasing models.

A surge in sales of electric vehicles leads to a surge in demand for efficient and cost-effective battery solutions. Battery-as-a-Service customers can lease the batteries instead of buying them, thereby saving the upfront cost for the purchase of Electric Vehicles. According to official government sources, in 2022, EVs accounted for 7.2% of new car sales worldwide, and their number will balloon considerably with growing official incentives for the adoption of EVs, starting with tax credits and subsidies in key markets such as the U.S., China, and Europe. The EV market is likely to experience a 35%-40% EV sales due to EV policies, thereby unlocking huge potential for battery leasing services as companies like Tesla and NIO expand their battery-swapping and leasing models.

-

Demand for renewable energy storage solutions driving Battery-as-a-Service adoption

Renewable energy sources, such as solar and wind, are increasingly being embraced, requiring large-scale, flexible, and scalable battery storage solutions. For energy companies and grid operators, battery-as-a-service will help to manage energy storage without big capital investments. For example, the trend on increasing renewable energy adoption is seen in policies like the European Green Deal and the U.S. Infrastructure Bill that provides billions for renewable energy infrastructure, including battery storage. The US government data shows that in 2023, renewable energy accounted for more than 21% of electricity generation in the country, and this percentage will rise. As a result, more battery leasing solutions will be in demand. Battery-as-a-Service advantages energy storage companies with more flexibility in renting storage capacity rather than buying an expensive battery system at the frontline. This makes it much easier to introduce renewables into the energy grid.

RESTRAIN:

-

High front-end infrastructure costs pose a major restraint to the adoption of this market across the globe.

One of the main barriers to entry for the Battery-as-a-Service market is the substantial upfront investment to establish battery-swapping stations and supporting infrastructure. Establishing a Battery-as-a-Service network, especially in the automobile domain, requires quite significant investments in technologies, physical infrastructures, and battery supply chains. Companies that would want to provide the service of leasing batteries need to establish or captivate battery swapping stations and ensure a steady supply of high-performance batteries. These costs are prohibitively high in hinterland regions, where penetration for EVs is still low. According to government data, setting up a single battery-swapping station for EVs would cost anywhere from USD 500,000 to USD 1 million, which varies with the region and capacity of the station. Logistics of maintaining, charging, and distributing batteries also entail heavy operational expenditures. For that reason, such small and medium-sized companies in developing economies may not be able to enter this market.

KEY SEGMENTATION ANALYSIS

BY SERVICE

Stationary Equipment led the market in 2023, with a 57% market share. Stationary batteries are primarily used in renewable energy grid energy storage solutions, industrial uses, and backup power systems. Growing deployments of renewable energy sources, especially solar and wind energy, enhance large-scale stationary battery storage solutions demand. Stationary Battery-as-a-Service allows energy companies and industries to lease battery storage instead of purchasing expensive battery systems much-needed solution to achieve equilibrium in the supply and demand curves for renewable energy grids.

On the other hand, Mobile Equipment, which includes EV batteries and other mobile applications, will register the highest CAGR of 18.70% during the forecast period of 2024-2032. There is therefore fast growth that has been supported by the adoption of EVs in most parts of the world and the need for efficient replacement of EV batteries. In economies such as China, mobile Battery-as-a-Service models have almost completely come into effect, whereby the drivers of EVs replace the spent battery with a full one at charging stations. The mobile Battery-as-a-Service market is likely to boom exponentially with the growing adoption rate of EVs, especially in the U.S. and Europe.

BY APPLICATION

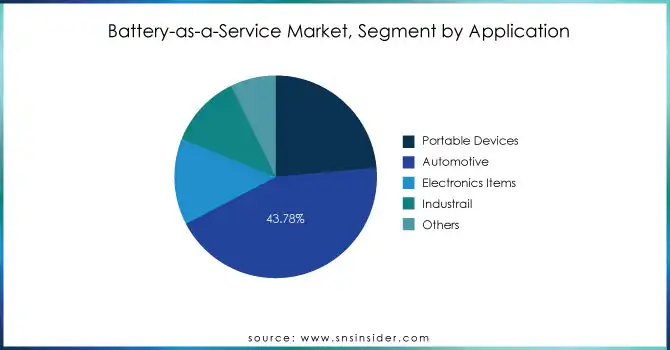

In 2023, Automotive and Transport will lead the market with a majority share of 51%. The general automotive sector, especially electric vehicles, is the major application for Battery-as-a-Service. OEMs as well as service providers are increasingly offering battery leasing options as a part of their EV offers, thereby reducing the financial burden on consumers. The growth in the adoption of EVs across the globe, backed by government initiatives and incentives, is driving growth in Battery-as-a-Service for this segment.

More insightful information can be obtained in this report, where the Automotive and Transport sector is anticipated to advance with the fastest CAGR of 18.61% during the forecast period of 2024–2032. Growth is mainly ascribed to growing consumer demand for EVs and the expansion of battery-swapping networks. Battery leasing in the segment is essential to overcome such challenges regarding high battery costs and a long time consumed in recharging, considered major hurdles in the adoption of EVs.

REGIONAL ANALYSIS

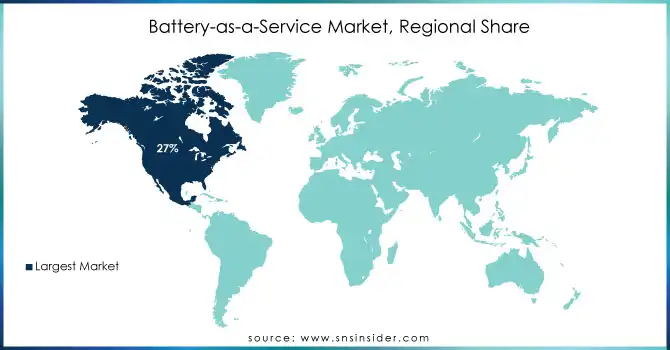

In terms of the regional analysis, North America held the highest market share of 27% in the Battery-as-a-Service market in 2023. The main reason behind the above is that the U.S. leads the region's automotive industry, with increasing adoption of electric vehicles and due support from their government toward renewable energies. The infrastructure bill by the U.S. government that allocates funds for electric vehicle infrastructure and energy storage solutions has spurred the adoption of Battery-as-a-Service across both automotive and energy sectors. Major operators in North America are now contracting with battery producers to expand their battery-swapping and leasing.

However, Asia Pacific is expected to grow at the highest CAGR of 19.23% during the forecast period of 2024 to 2032. China is a world leader in Battery-as-a-Service, through a mature battery-swapping structure, and with the government having proactive policies supporting adoption of EVs and battery leasing models. India and Japan are emerging markets for Battery-as-a-Service and are driven by increasing investment into renewables and automotive sectors.

Get Customized Report as per Your Business Requirement - Enquiry Now

KEY PLAYERS

Some of the major players in the Battery-as-a-Service Market are

-

NIO (Battery swapping, EVs)

-

Tesla (Energy storage solutions, EV batteries)

-

BYD (Energy storage systems, EV batteries)

-

CATL (Battery systems, energy solutions)

-

Panasonic (EV batteries, energy storage)

-

LG Energy Solution (Battery systems, EV batteries)

-

Northvolt (Energy storage solutions, battery cells)

-

Envision AESC (EV batteries, energy storage)

-

Gotion High-Tech (Battery systems, EV solutions)

-

A123 Systems (Battery technology, energy storage)

-

CBAK Energy Technology (EV batteries, energy storage)

-

Amperex Technology Limited (Battery systems, mobile equipment)

-

EnerSys (Battery solutions, energy storage)

-

Enevate (Battery technology, fast-charging solutions)

-

Samsung SDI (Battery systems, EV batteries)

-

Leclanché (Energy storage solutions, battery systems)

-

Kion Group (Battery systems, industrial applications)

-

Hitachi Chemical (Battery components, energy solutions)

-

Mitsubishi Electric (Energy storage, industrial batteries)

-

ABB (Energy storage, EV charging solutions)

-

Charge Zone

MAJOR CLIENTS

-

Ford

-

General Motors

-

BMW

-

Audi

-

Daimler

-

Volkswagen

-

Rivian

-

Lucid Motors

-

Nissan

-

Toyota

RECENT TRENDS

-

October 2024: India-based EV charging network ChargeZone recently launched its new Battery Passport System, an online platform that generates a comprehensive life cycle record of any battery. It collects detailed information for every stage, thereby helping to move from a linear to a circular economy by providing transparent information in the lifetime of the battery. With this transparency, all stakeholders in the EV battery ecosystem would be facilitated, from buyers of EVs to manufacturers, recyclers, and other economic operators.

-

October 2024: In an effort to strengthen its market leadership in battery electric vehicles, Tata Motors is exploring the feasibility of a Battery-as-a-Service model for a few of its products, sources privy to the development said. The battery rental option for consumers would help reduce the ex-showroom prices of its BEVs by 25-30 per cent, and the BaaS model is likely to be offered for the electric variant of Tiago, Punch, Tigor, Nexon, and others.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 3.02 Billion |

| Market Size by 2032 | US$ 13.50 Billion |

| CAGR | CAGR of 18.15 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Battery Ownership Models (Battery Purchase, Battery Lease, Battery Subscription), • By Energy Storage Capacity (Less than 50 kWh, 50-100 kWh, Over 100 kWh), • By Application (Automotive and Transport, Energy, Industrial, and Others) • By Service (Stationary Equipment, Mobile Equipment) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | NIO, Tesla, BYD, CATL, Panasonic, LG Energy Solution, Northvolt, Envision AESC, Gotion High-Tech, A123 Systems, CBAK Energy Technology, Amperex Technology Limited, EnerSys, Enevate, Samsung SDI, Leclanché, Kion Group, Hitachi Chemical, Mitsubishi Electric, ABB. |

| Key Drivers | • Increasing adoption of EV necessitates flexible battery leasing models. • Demand for renewable energy storage solutions driving Battery-as-a-Service adoption. |

| Restraints | • High front-end infrastructure costs pose as a major restraint to the adoption of this market across the globe. |

Frequently Asked Questions

Ans: North America dominated the Battery-as-a-Service Market in 2023.

Ans: The Stationary Equipment segment dominated the Battery-as-a-Service Market.

Ans: The major growth factors of the Battery-as-a-Service Market are Increasing adoption of EV and Demand for renewable energy storage solutions.

ns: Battery-as-a-Service Market size was USD 3.02 Billion in 2023 and is expected to Reach USD 13.50 Billion by 2032.

Ans: The Battery-as-a-Service Market is expected to grow at a CAGR of 18.15% during 2024-2032.

Get in Touch