Battery Packaging Market Report Scope & Overview

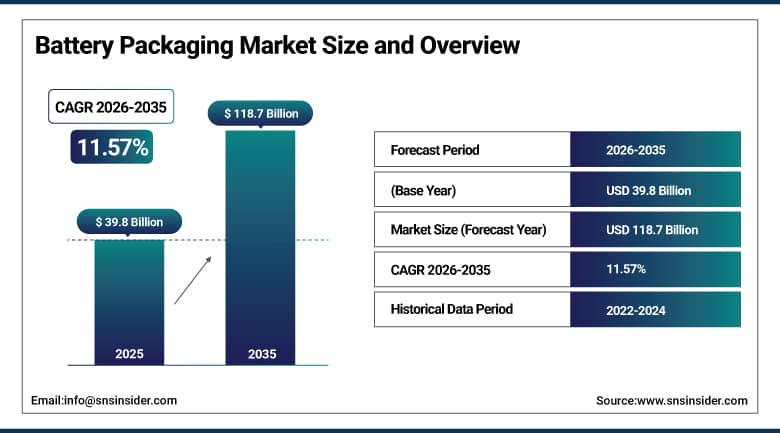

The Battery Packaging Market was valued at USD 39.8 billion in 2025 and is expected to reach USD 118.7 billion by 2035, growing at a CAGR of 11.57% from 2026–2035.

The battery packaging refers to the type of packaging materials used to protect the batteries against various hazards such as mechanical damage, thermal abuse, moisture, and chemical exposure. With the rapid development of electric vehicles and the increasing importance of energy storage in maintaining the stability of the grid as well as incorporating renewable energies into the grid, there has been growing interest in high-performance packaging technologies of batteries by manufacturers, car makers, and energy companies. The development of batteries with high energy density, such as lithium iron phosphate batteries and solid-state batteries, has resulted in an increased need for better packaging materials.

The EV industry is the single largest growth driver for battery packaging. A single electric vehicle contains a battery pack weighing hundreds of kilograms, and every cell within that pack requires protective packaging. As global EV production scales to tens of millions of vehicles per year, the demand for safe, high-performance battery packaging will follow in lockstep.

Recycling is becoming an important consideration when designing batteries. There is increasing pressure on governments and automobile manufacturers to develop a system that would allow for better recyclability of batteries, and this has led to increased funding for recyclable batteries and modular packs that can easily be taken apart.

Market Size and Forecast

-

Market Size in 2025: USD 39.8 Billion

-

Market Size by 2035: USD 118.7 Billion

-

CAGR: 11.57% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Battery Packaging Market - Request Free Sample Report

Battery Packaging Market Trends

-

The quick growth of electric vehicle manufacturing all around the globe is resulting in increased demand for superior battery packaging that is made out of various materials and has different designs to accommodate large lithium-ion battery production and logistics needs.

-

The rising number of environmental laws and sustainable practices is fostering the use of environmentally friendly, lightweight, and reusable materials for battery packaging since more companies want to decrease their use of plastic.

-

Faster growth in battery technology and safety standards is fueling demand for battery packaging that can help maintain the optimal temperature of battery cells and improve their overall lifespan.

-

The increasing trend in the usage of prismatic and pouch battery cells for EVs is redefining the battery packaging needs because of their high space utilization, lightweight, and energy density advantages over cylindrical batteries.

-

Battery cell designs based on the cell-to-pack or cell-to-chassis concepts are changing the packaging needs due to their high efficiency and reduced use of battery modules.

-

Manufacturers have begun to develop sophisticated packing materials for lithium-ion batteries with the use of cardboard and fiber to transport batteries safely according to the rules of sustainability and dangerous goods transportation laws.

-

With the increasing usage of large energy batteries for storage purposes to integrate renewable energy, there is an ever-growing demand for better packaging for batteries.

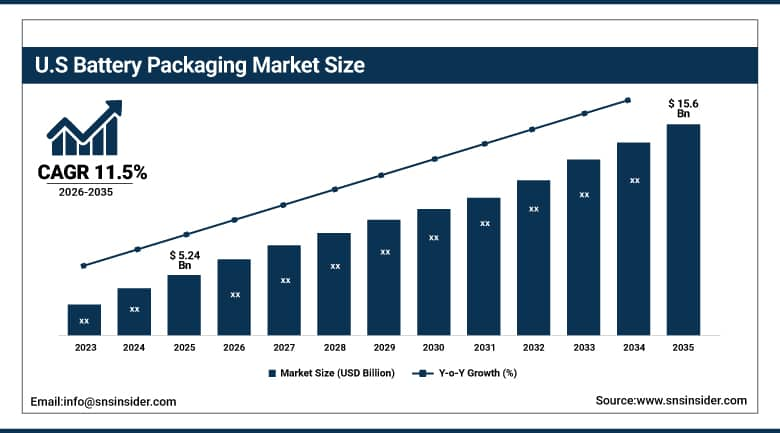

The U.S. Battery Packaging Market was valued at USD 5.24 billion in 2025 and is expected to reach USD 15.6 billion by 2035, growing at a CAGR of 11.5% from 2026 to 2035.

The U.S. battery packaging industry is being propelled by the fast-paced development of electric vehicle manufacturing in the country, significant capital allocation towards building battery gigafactories, and the booming grid-scale energy storage industry. The Inflation Reduction Act has boosted EV manufacturing and battery manufacturing in the country, generating strong demand for packaging materials and solutions. Giants such as Tesla, General Motors, and Ford are establishing battery manufacturing facilities in the U.S., which will need large amounts of packaging materials.

The CHIPS and Science Act and the Inflation Reduction Act together are transforming the U.S. into a major domestic battery manufacturing hub. As battery gigafactories come online in states like Georgia, Kentucky, and Nevada, local battery packaging supply chains are developing around them, creating both market opportunity and employment in these regions.

Battery Packaging Market Segment Analysis

-

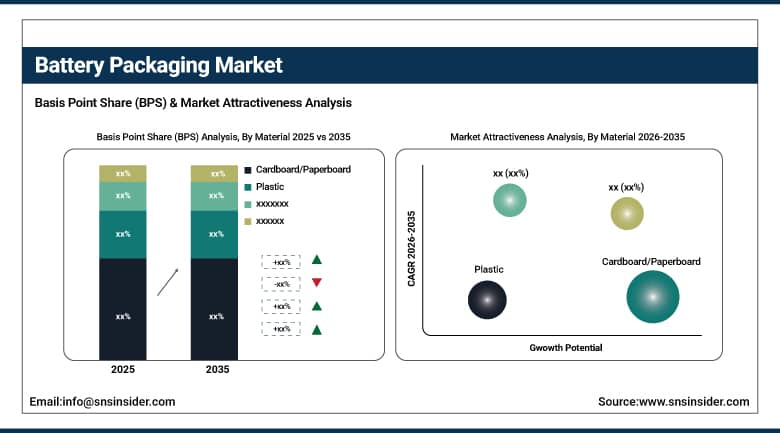

Based on Material, Cardboard/Paperboard led with 61.23% market share in 2025, driven by sustainability trends and cost advantages for consumer and small-format batteries.

-

Based on Casing Type, Cylindrical casings held the largest share at 55.28%; Prismatic is the fastest-growing casing type in EV applications.

-

Based on Packaging Type, Cell & Pack Packaging dominated with 63.38% market share; this segment grows in line with battery production volumes.

-

Based on Battery Type, Lithium-Ion was the largest segment at 39.65%; Lead Acid is expected to grow at the highest CAGR at 12.38% due to its ongoing use in industrial applications.

-

Based on End-Use, Electric Vehicles is the largest and fastest-growing end-use segment.

By Material: Cardboard Leads for Sustainability, Metal Critical for EVs

Paper board and cardboard products commanded the largest market share for battery packaging in 2025, representing 61.23%. The dominance can be attributed to the extremely high demand for cardboard battery packaging in the shipment of consumer electronics. Plastic to cardboard is increasingly becoming the choice packaging for this category due to environmental restrictions and corporate sustainability goals. DS Smith and Smurfit Kappa companies are working on the development of special corrugated packaging aimed at securing lithium-ion batteries during transportation.

The metal case is common for cylindrical and prismatic battery types used in EV battery packs. Aluminium material has been chosen for its lightness and strength. Steel materials are used when extra mechanical strength is required. Metal package quality is crucial for battery performance in the expensive category of electric vehicles.

Plastic battery packaging solutions have been applied in small batteries, some categories of consumer electronic batteries, and internal packaging of batteries. Special high-grade plastics able to resist heat cycling and chemical environment have been used in EVs.

By Casing Type: Cylindrical Largest, Prismatic Fastest Growing

The cylindrical cell continues to dominate as the most popular form factor worldwide, used in consumer electronic devices and power tools, as well as numerous electric vehicle applications, such as those developed by Tesla. As such, the standardized nature of the form factor allows for interchangeability and efficient production of cylindrical cells. Cylindrical casings captured 55.28% of market revenues in 2025.

The second fastest-growing form factor in the sector belongs to prismatic batteries, as well as the associated packaging solutions. Prismatic batteries provide enhanced energy density compared to alternative form factors and are easier to integrate into the overall design of the battery pack. Chinese electric vehicle producers have adopted prismatic battery technology in mass volumes, alongside the likes of CATL and BYD. The development of the cell-to-pack format, where the module layer is bypassed and prismatic cells are directly connected to the battery pack frame, is boosting growth of this segment.

Pouch cells provide the highest energy density per unit of volume but also the most complex packaging solution due to expansion.

By End-Use: Electric Vehicles Dominate Growth

Electric vehicles are the largest and fastest-growing end-use segment for battery packaging. Each EV contains a battery pack with hundreds or thousands of cells, each requiring packaging. As EV production scales globally, the demand for battery packaging grows proportionally. Battery manufacturers supplying the EV industry have become among the largest buyers of packaging materials and components in the world.

Consumer electronics remains a large segment by volume. Smartphones, laptops, tablets, and wearables all use batteries that need retail, transport, and product-level packaging. While the growth rate in this segment is lower than EVs, the enormous unit volume of consumer devices maintains it as a major revenue contributor.

Grid-scale energy storage systems are a fast-growing end-use segment. As more wind and solar power is installed, the need to store energy for use when the sun is not shining and wind is not blowing grows. Large battery storage installations require specialized packaging that prioritizes safety, thermal management, and modular scalability.

Battery Packaging Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

75% |

|

Europe |

Germany |

32% |

|

Asia Pacific |

China |

52% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

50% |

North America Battery Packaging Market Insights

The North American region captured about 20% of the global Battery Packaging Market’s revenue share in 2025, with significant contributions from the United States. The high demand for electric vehicles in the domestic market, driven by financial incentives as per the Inflation Reduction Act (IRA), is contributing towards the fast-growing supply chain of the battery packaging industry in the region. The growing investments in gigafactories of companies like Panasonic Corporation, Samsung SDI, and LG Energy Solution, coupled with rising investments from automotive companies in the country, are contributing to increased demands for advanced battery packaging products and thermal protection solutions. Moreover, the growing popularity of energy storage projects in various states like California and Texas is boosting demand for safe packaging materials for lithium-ion batteries.

Europe Battery Packaging Market Insights

Europe is a prominent and continuously increasing segment of the worldwide Battery Packaging Market due to its robust goals regarding electric vehicle usage and investment in batteries' manufacture within the region. Several countries, such as Germany, France, Sweden, and Poland, are now rising to become prominent producers and suppliers of batteries due to their ongoing development of gigafactories and environmental-friendly energy programs backed by governments. Furthermore, the European Battery Alliance, along with other EU sustainability policies, is driving up the demand for battery packaging products within Europe. Moreover, stringent European Union policies concerning recyclable batteries, carbon emissions, hazardous substance management, and sustainable materials for battery packaging encourage the development of innovative battery packaging technologies.

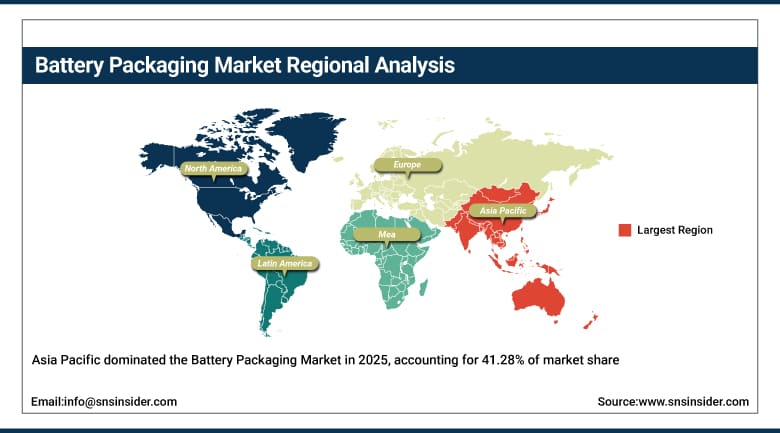

Asia Pacific Battery Packaging Market Insights

The Asia Pacific region emerged as the key contributor to the Global Battery Packaging Market in 2025, contributing about 41.28% of the overall market revenue. Some of the prominent regional markets that contribute to the growth of the industry include China, Japan, South Korea, and India. China currently leads as the largest producer of batteries in the world, owing to the widespread manufacture of electric vehicles, increasing energy storage installations, and an extensive network for producing lithium-ion batteries, thereby becoming the largest market for battery packaging products. On the other hand, South Korea hosts leading battery manufacturers like Samsung SDI, LG Energy Solution, and SK On. The export of batteries and collaborations with EV makers have created significant opportunities for the market in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

MEA and Latin America Battery Packaging Market Insights

Energy storage has become an area of focus in the Middle East for grid stability and for use with renewable energy sources, increasing the demand for battery packaging products. Saudi Arabia has its Vision 2030 initiative related to energy, while the UAE has plans to develop clean energy that increases the use of batteries. Africa is in an early stage of development for the battery packaging market, with some projects involving solar energy combined with storage in remote areas and for businesses.

The Latin American region is expected to grow as well, being one of the emerging markets in this industry. In Brazil there is great potential for renewable energy, and with more installations, there will be a need for batteries. In Mexico, there is a strong automobile industry and especially electric vehicle production, hence, the need for battery packages.

Battery Packaging Market Growth Drivers

-

Electric vehicle adoption and energy storage investment are transforming the market

The global shift away from the use of fossil fuels is at the heart of the growth in demand for battery packaging. The production of EVs is rising from several million units per year to tens of millions over the forecast horizon, and each car will need a battery system with proper packaging. Additionally, there is increasing demand for batteries in renewable energy applications. Both trends represent demand drivers that are structural in nature and will continue despite short-term changes in economic conditions.

Policy action is one of the biggest catalysts for such demand. The Inflation Reduction Act in the U.S., the European Union's Battery Regulation, and China's NEV policies provide strong financial support and mandates that result in increased demand for electric vehicles and their batteries. Every dollar spent on EV subsidies through policy results in higher demand for battery packaging.

Battery Packaging Market Restraints

-

Supply chain complexity and raw material price volatility create cost pressure

In terms of battery packaging, many types of materials may be needed, which include engineering plastics, aluminum, steel, and films. The procurement of these materials is not simple and can be influenced by some political developments, trade sanctions, or any shortages of these materials. Changes in aluminum and engineering plastics prices will affect the costs related to packaging. Battery manufacturers that are cost-oriented would find this difficult to manage.

Battery Packaging Market Opportunities

-

Next-generation battery formats and solid-state batteries require new packaging solutions

As technology moves towards advanced batteries such as solid-state batteries, there will be a considerable change in the demands made on the packaging system. Solid-state batteries function under much higher pressure and temperature ranges compared to liquid electrolytes and demand more precise mechanical contact between the layers of the cell. This opens up possibilities for innovative packaging design that can meet the needs of advanced batteries. Firms who innovate in solid-state battery packaging will enjoy early market entry into the space.

Recent Developments

-

2026: The CATL battery system called "Kirin Battery" was introduced, which consisted of cell-to-pack batteries having superior thermal management packaging that could also function as a structural element for the vehicles, thus saving the need for packaging modules separately. This design also allowed more energy efficiency, with a 13% improvement over previous models.

-

2026: The Nefab Group introduced battery packaging solutions for North America's electric vehicles with the opening of its advanced engineering center in Mexico dedicated to designing lithium-ion battery packaging.

-

2025: Energizer Holdings introduced new battery packaging solutions that were completely recyclable and plastic-free.

Battery Packaging Market Key Players

-

Amcor Plc

-

DS Smith Plc

-

Smurfit Kappa Group

-

Sealed Air Corporation

-

Integer Holdings Corporation

-

Tekni-Plex Inc.

-

Evonik Industries AG

-

BASF SE

-

Crown Holdings Inc.

-

EnerSys

-

Nefab Group

-

Schoeller Allibert

-

UFP Technologies Inc.

-

Sonoco Products Company

-

ZARGES GmbH

-

East Penn Manufacturing

-

Exide Technologies

-

Bollore Group

-

Elkem ASA

-

Sigma Lithium Corporation

Battery Packaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 39.8 Billion |

| Market Size by 2035 | USD 118.7 Billion |

| CAGR | CAGR of 11.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Cardboard/Paperboard, Plastic, Metal, Others) • By Casing Type (Cylindrical, Prismatic, Pouch) • By Packaging Type (Cell & Pack Packaging, Module Packaging, Battery Management System Packaging) • By Battery Type (Lithium-Ion, Lead Acid, Lithium Iron Phosphate, Nickel-Based, Others) • By End-Use (Electric Vehicles, Consumer Electronics, Energy Storage Systems, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amcor Plc, DS Smith Plc, Smurfit Kappa Group, Sealed Air Corporation, Integer Holdings Corporation, Tekni-Plex Inc., Evonik Industries AG, BASF SE, Crown Holdings Inc., EnerSys, Nefab Group, Schoeller Allibert, UFP Technologies Inc., Sonoco Products Company, ZARGES GmbH, East Penn Manufacturing, Exide Technologies, Bollore Group, Elkem ASA, Sigma Lithium Corporation |

Frequently Asked Questions

The market is expected to grow at a CAGR of 11.57% from 2026 to 2035.

The market was valued at USD 39.8 billion in 2025.

Cardboard/Paperboard leads with 61.23% market share due to sustainability drivers and widespread use in consumer electronics packaging.

Asia Pacific dominates with 41.28% revenue share, driven by China's dominant battery manufacturing capacity.

Electric vehicle production scale-up and grid-scale energy storage investment are the primary growth drivers.

Get in Touch