Battery Test Equipment Market Report Scope & Overview:

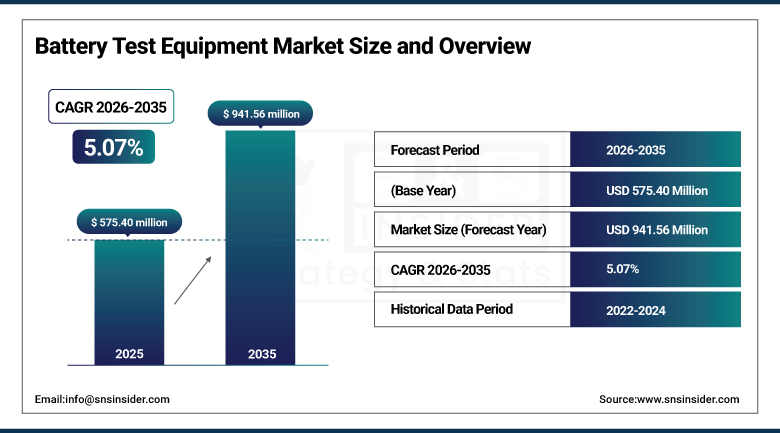

The Battery Test Equipment Market was valued at USD 575.40 million in 2025 and is expected to reach USD 941.56 million by 2035, growing at a CAGR of 5.07% from 2026–2035.

The battery test equipment market is witnessing strong growth in the global market owing to rising adoption of electric vehicles and energy storage systems. Expanding lithium-ion battery production is driving strong demand for advanced testing solutions. Growing focus on battery safety and performance validation is improving testing accuracy standards. Rising investments in EV charging infrastructure are supporting market expansion. Increasing integration of high-power battery systems is accelerating technological innovation. Governments are focusing on clean energy transition and EV adoption, further boosting market growth.

According to the IEA Global EV Outlook 2025, the number of electric cars globally crossed the 40 million mark, which accounted for more than 20% of the total car sales, which resulted in the need for huge infrastructure of batteries testing. According to the Battery500 Consortium by the U.S. Department of Energy and the EU Battery Regulation, all batteries of an industry exceeding 2 kWh require validation regarding performance, safety, and life cycle testing.

Market Size and Forecast:

-

Market Size 2026E: USD 603.42 million

-

Market Size 2035: USD 941.56 million

-

CAGR (2026 - 2035): 5.07%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Battery Test Equipment Market - Request Free Sample Report

Battery Test Equipment Market Trends:

-

The quick rise in the use of electric vehicles is creating the need for modern battery test equipment in various auto manufacturing industries around the world.

-

The rise in lithium-ion batteries' production has increased the demand for precise battery test equipment due to performance and safety concerns.

-

The increased attention towards battery safety standards is forcing the manufacturers to opt for modern testing methods of their products.

-

Artificial Intelligence (AI) and digital twin technology integration have increased efficiency in battery testing processes.

-

The investments in gigafactories and big energy storage projects have led to the rapid adoption of automated and powerful battery test equipment.

-

Good regulatory frameworks within both energy and auto manufacturing sectors have forced compliance leading to increased battery test equipment demand.

U.S. Battery Test Equipment Market Outlook:

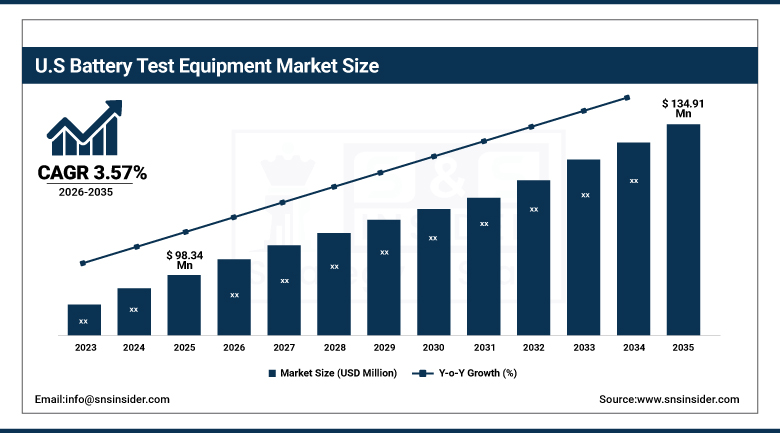

The U.S. Battery Test Equipment Market was valued at USD 98.34 million in 2025 and is expected to reach around USD 134.91 million by 2035, growing at a CAGR of 3.57% from 2026–2035.

The U.S. battery test equipment market is growing steadily owing to rising electric vehicle adoption and increasing demand for advanced battery validation systems. Expanding lithium-ion battery manufacturing is enhancing need for high-precision testing equipment. Strong investments in EV infrastructure and grid storage systems are supporting market expansion. Growing focus on battery safety and performance standards is improving testing accuracy across industries. Rising deployment of high-power battery systems in automotive sector is accelerating technological advancements. Continuous innovation in testing automation and analytics is further driving adoption across end users.

As indicated by the U.S. Department of Energy's Vehicle Technologies Office and the Battery500 Consortium progress report, efforts to improve the energy density of lithium-ion batteries have met cell-level target densities above 300 Wh/kg in advanced prototypes up to the 2025 benchmark date. According to the U.S. Geological Survey Mineral Commodity Summaries 2025, the country continues to rely heavily on imports of key battery components like graphite and lithium compounds, with import reliance exceeding 50% for several components.

Battery Test Equipment Market Segment Analysis:

-

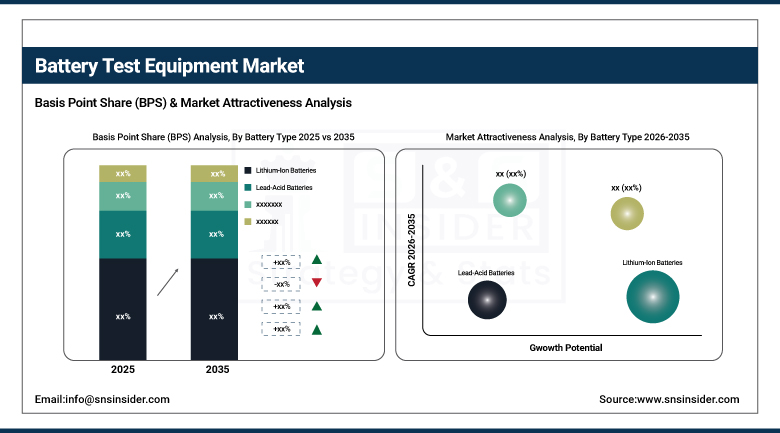

By Battery Type, lithium-ion batteries dominated the market with 57.60% share in 2025 and is also the fastest growing segment during 2026 to 2035 with a CAGR of 7.56%.

-

By Test Type, capacity and rate testing dominated the market with 41.50% share in 2025; while safety testing is the fastest growing segment with CAGR of 9.22% during 2026 to 2035.

-

By Application, electric vehicles dominated the market with 46.20% share in 2025; while energy storage systems are the fastest growing segment with CAGR of 5.22% during 2026 to 2035.

-

By End User, battery manufacturers dominated the market with 48.90% share in 2025; while automotive industry is the fastest growing segment with CAGR of 9.67% during 2026 to 2035.

-

By Range, medium power (1000A–5000A) dominated the market with 51.40% share in 2025; while high power (more than 5000A) are the fastest growing segment with CAGR of 9.79% during 2026 to 2035.

By Battery Type, lithium-ion batteries segment dominates the battery test equipment market in 2025 and is also the fastest growing segment.

Lithium-Ion Batteries dominated the battery test equipment market by generating the dominated revenue share in 2025. The growth can be attributed to its wide usage in the production of electric vehicles, consumer electronics, and energy storage systems. The high energy density, extended lifecycle, and decreasing cost of batteries have played a crucial role in growing its volume production. The increasing demand for testing and quality assurance of batteries in the large-scale production of lithium-ion batteries is making it dominant in the market.

Lithium-Ion Batteries are projected to be the fastest-growing segment during the forecast period, i.e., 2026–2035, owing to the quick expansion of electric mobility and renewable energy storage solutions. The growing innovations in battery chemistry and fast-changing technology have raised the complexity of testing. The rise in investments in gigafactories and incentives by governments for electric vehicles is raising the production capacity.

By Test Type, capacity and rate testing dominated the battery test equipment market in 2025, while safety testing is the fastest growing segment.

Capacity and Rate Testing segment dominated the battery test equipment market in terms of revenue share in 2025. The capacity and rate testing equipment segment is dominant owing to its key role in battery performance, efficiency, and battery charging process testing. It is being utilized in both EV battery and energy storage system applications. Quality validation and lifetime evaluation of batteries are crucial functions of capacity and rate testing equipment used by manufacturers.

Safety Testing segment is estimated to be growing at a rapid CAGR from 2026 to 2035. This growth is attributed to increasing awareness regarding thermal runaway and battery safety risks such as fire and explosion dangers. Regulatory requirements and safety norms are mandating manufacturers to implement sophisticated safety validation systems. Increasing adoption of EVs and energy storage is fueling the demand further. Safety testing technology is rapidly evolving in this industry.

By Application, electric vehicles dominated the battery test equipment market in 2025, while energy storage systems are the fastest growing segment.

Electric Vehicles held the dominated revenue share of the battery test equipment market in 2025. The growing number of electric vehicle users, high-volume manufacturing of lithium-ion batteries, and increased demand for performance testing systems are driving this market dominance. Increasing demand for testing of batteries' safety, efficiency, and durability in automotive applications is reinforcing market position. Growing production capacity of EVs and constant advancements in battery technology are ensuring continued dominance in all geographical regions.

The Energy Storage Systems segment is projected to register the fastest CAGR during the forecast period. Growth in this segment will be fuelled by rising incorporation of renewable energy sources and increased demand for grid stabilization solutions. Increased implementation of solar energy and wind energy projects is creating an increased demand for advanced testing of storage systems. Constant advancements in the energy efficiency and sustainability goals are fuelling the growth of the market.

By End User, battery manufacturers dominated the battery test equipment market in 2025, while automotive industry is the fastest growing segment.

Battery Manufacturers segment accounted for the dominated revenue share in the battery test equipment market in 2025 owing to mass production of lithium-ion batteries and requirement for their performance tests. The growing requirement for quality testing and lifecycle testing is adding to this growth. Growing battery gigafactories and production capabilities are further enhancing the use of advanced testing equipment.

The Automotive Industry segment is expected to witness the fastest CAGR over 2026–2035 due to quick adoption of electric vehicles and incorporation of advanced batteries in vehicles. The focus on safety and performance of these vehicles is further adding to the growth of testing solutions. The expansion of automobile electrification projects and investment in advanced batteries is further fueling the growth of this market segment.

By Range, medium power (1000A–5000A) dominated the battery test equipment market in 2025, while high power (more than 5000A) is the fastest growing segment.

Medium Power (1000A-5000A) accounted for the fastest market share by revenues in the battery test equipment market in 2025. The reasons behind such market dominance include wide application for electric vehicle battery pack testing and industrial energy storage system validation. It is the most balanced option in terms of costs and test accuracy. The segment enjoys wide popularity among manufacturers due to standardized testing applications. The increase in EV production helps drive demand from global battery testing centers.

High Power (above 5000A) is set to witness the fastest CAGR during the forecast period of 2026-2035. The factors driving its growth are the growing development of large capacity EV batteries and grid energy storage systems. There is an increasing demand for rapid charge systems and heavy-duty electric vehicles. The advanced requirements for next-generation battery testing chemistry are another factor helping segment expand. Growth in ultra-high power test equipment infrastructure investments also helps.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.40% |

|

Europe |

Germany |

28.60% |

|

Asia Pacific |

China |

43.20% |

|

Middle East & Africa |

UAE |

18.40% |

|

Latin America |

Brazil |

48.10% |

North America Battery Test Equipment Market Insights.

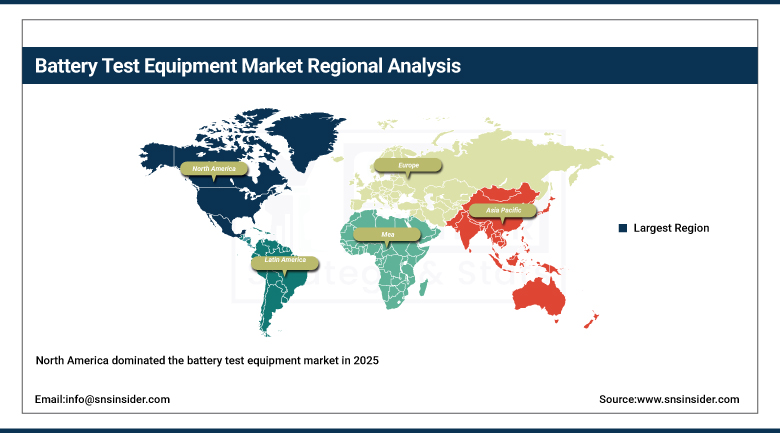

North America dominated the battery test equipment market in 2025 owing to strong EV adoption and R&D activities. The region benefits from advanced automotive manufacturing infrastructure and established testing laboratories. Increasing lithium-ion battery production is improving demand for high precision testing systems. Rising investments in grid energy storage projects are driving equipment deployment. Strong government support for clean mobility is further boosting market growth across key applications.

As per the U.S. Department of Energy Vehicle Technologies Office and Argonne National Laboratory 2025 Battery Framework, energy density of lithium-ion battery has increased from 100 Wh/kg in 2010 to above 250 Wh/kg in the currently available batteries, and this requires complex validation testing and cycling up to 1,000-2,000 times per qualification.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Battery Test Equipment Market Insights.

Europe battery test equipment market is characterized by steady growth in 2025 owing to strict battery safety and environmental regulations. Key countries include Germany, France, United Kingdom, and Italy. Rising EV penetration and strong focus on decarbonization are driving demand for advanced testing solutions. Increasing establishment of battery gigafactories is boosting equipment installation. Expansion of renewable energy storage systems is further supporting market growth across the region.

As per the EU's Critical Raw Materials Act 2025 and the Eurostat energy storage indicators, the objective is that by 2030, the EU shall have a domestic processing capacity of not less than 40% for strategic battery materials. According to the IEA Global EV Outlook 2025, the market share of Europe in terms of electric cars exceeds 25%, and battery electric vehicles exceed 15% in terms of new car registrations.

Asia Pacific Battery Test Equipment Market Insights.

Asia Pacific dominated the battery test equipment market with a share of about 44.60% in 2025 and is expected to register the fastest CAGR of about 6.54% during 2026–2035. Strong battery manufacturing expansion is driving regional leadership. Rapid growth of EV production in China, India, Japan, and South Korea is supporting strong demand. Increasing investments in gigafactories and energy storage systems are boosting testing equipment adoption. Rising focus on renewable integration is enabling large scale deployment of advanced battery validation systems across the region.

According to the International Energy Agency Global EV Outlook 2025, Asia Pacific accounts for more than 60% of global electric vehicle stock, with China alone representing over 50% of annual EV sales. As per the IEA Battery Supply Chain, global lithium-ion battery manufacturing capacity is highly concentrated in Asia, with China contributing over 70% of cell production. The International Renewable Energy Agency reports that global installed battery storage capacity grew by more than 40% year-on-year, driven primarily by Asia Pacific grid-scale deployments, increasing demand for advanced battery testing and validation infrastructure across manufacturing ecosystems.

Middle East & Africa and Latin America battery test equipment market Insights.

The Middle East & Africa along with Latin America regions are witnessing steady growth due to rising renewable energy investments and EV adoption. Key contributing countries include Brazil, Mexico, UAE, Saudi Arabia, and South Africa. Increasing deployment of solar and wind energy storage systems is driving demand for battery testing solutions. Expanding automotive electrification initiatives are supporting market expansion. Growing focus on infrastructure modernization is further boosting equipment adoption across regions.

As per the International Energy Agency Global EV Outlook 2025 report, the number of electric vehicles in Latin America exceeded 2 million, whereas the Middle East and Africa region together made up less than 2% of the adoption rate of electric vehicles on a global scale, thus pointing towards initial electrification compared to developed economies. As per the report of the United Nations Economic Commission for Latin America and the Caribbean, there is an expansion of batteries manufacturing in more than 15 nations within the region via energy transition strategies adopted by individual nations.

Market Dynamics:

Growth Drivers: Rising focus on battery safety standards and stringent regulatory compliance across global energy and automotive sectors

Rising safety issues associated with battery failure and thermal runaway have led to a need for more comprehensive testing systems. Regulatory bodies are imposing strict compliance regulations on EV batteries and energy storage systems. Manufacturers are investing in sophisticated testing equipment for their reliable operation and reducing risks. The construction of battery manufacturing plants on a large scale has led to quality assurance needs. Increased incorporation of high-power battery systems has raised the need for safety validations.

According to the report of the International Energy Agency Global EV Outlook 2025, the sales of global electric cars have crossed 14 million cars, which have a share of more than 20% in total car sales, thereby requiring standardized battery testing and validation systems. According to United Nations Economic Commission for Europe Regulation Number 100, there is a need for safety requirements for electric vehicle battery systems.

Restraints: Technical complexity and slow standardization across global battery testing protocols creating operational challenges

The complexity of testing high energy density batteries makes operations even more challenging for both producers and testing centers. The absence of universal worldwide standards leads to differences in testing methods. Frequent changes in the chemical composition of the batteries lead to the need for constant updating of equipment. Introduction of automation and AI testing system necessitates availability of qualified specialists. Compatibility problems with other types of batteries reduce the effectiveness of testing process.

Opportunities:Technological advancements in high-power and automated testing systems enabling next-generation battery innovation ecosystem

Research & development initiatives aimed at developing new generation batteries is creating a huge demand for state-of-the-art testing machines. The use of AI and analysis capabilities is leading to better test methods. Increased demand for fast-charging batteries requires special testing equipment. Testing technology based on digital twin technique is being employed by companies. New testing technology is being developed because of electric mobility.

According to the IEA Global EV Outlook 2025 report, the percentage of sales of electric cars was more than 20% of all sales of vehicles worldwide, resulting in rapid growth of lithium-ion battery production capacity. According to the U.S. Department of Energy’s Battery Manufacturing & Recycling Grants program, there has been substantial growth in capacity for battery production in the United States via federal support for gigafactory-scale facilities that include automated formation & power cycling tests.

Recent Developments:

-

2026: Emerson Electric Co. advanced NI platform integration for automated test workflows enhancing battery validation and industrial measurement efficiency.

-

2025: Chroma ATE Inc. introduced 17040E regenerative battery test system enabling 1500V simulation for EV and energy storage applications.

-

2025: Rohde & Schwarz expanded automotive battery test solutions portfolio supporting EV validation and high precision measurement applications globally.

-

2024: Keysight Technologies completed integration of ESI Group acquisition enhancing simulation and validation capabilities for battery testing workflows.

Battery Test Equipment Market Key Players are:

-

Keysight Technologies

-

Rohde & Schwarz

-

Chroma ATE Inc.

-

Emerson Electric Co.

-

Yokogawa Electric Corporation

-

HIOKI E.E. Corporation

-

Kikusui Electronics Corporation

-

ITECH Electronic Co., Ltd.

-

EA Elektro-Automatik GmbH

-

Arbin Instruments

-

Maccor Inc.

-

Bitrode Corporation

-

Digatron Power Electronics

-

Shenzhen Neware Technology Co., Ltd.

-

Cadex Electronics Inc.

-

AVL List GmbH

-

HORIBA Ltd.

-

AMETEK Inc.

-

BioLogic Science Instruments

-

Dewesoft d.o.o.

Battery Test Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 575.40 Million |

| Market Size by 2035 | USD 941.56 Million |

| CAGR | CAGR of 5.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Battery Type (Lead-Acid Batteries, Lithium-Ion Batteries, Nickel-Based Batteries, Other Battery Types) • By Test Type (Capacity and Rate Testing, Safety Testing, Battery Cycle Testing, Other Test Types) • By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Other Applications) • By End User (Battery Manufacturers, Automotive Industry, Research and Development Institutions, Other End Users) • By Range (Low Power (less than 1000A), Medium Power (1000A–5000A), High Power (more than 5000A)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Keysight Technologies, Rohde & Schwarz, Chroma ATE Inc., Emerson Electric Co., Yokogawa Electric Corporation, HIOKI E.E. Corporation, Kikusui Electronics Corporation, ITECH Electronic Co., Ltd., EA Elektro-Automatik GmbH, Arbin Instruments, Maccor Inc., Bitrode Corporation, Digatron Power Electronics, Shenzhen Neware Technology Co., Ltd., Cadex Electronics Inc., AVL List GmbH, HORIBA Ltd., AMETEK Inc., BioLogic Science Instruments, Dewesoft d.o.o. |

Frequently Asked Questions

Asia Pacific dominated the battery test equipment market in 2025 due to strong manufacturing, EV growth, gigafactory investments, and storage demand.

The Electric Vehicles segment dominated the market in 2025 due to large-scale adoption, lithium-ion testing demand, and automotive validation requirements.

The battery test equipment market is expected to grow at a CAGR of 5.07% from 2026 to 2035.

The battery test equipment market was valued at USD 575.40 million in 2025.

The major growth factors include EV adoption, lithium-ion production expansion, battery safety demand, energy storage growth, EV charging investments, gigafactory development, and strict regulatory focus on testing standards and clean energy transition.

Get in Touch