Benign Prostatic Hyperplasia Treatment Market Report Scope & Overview:

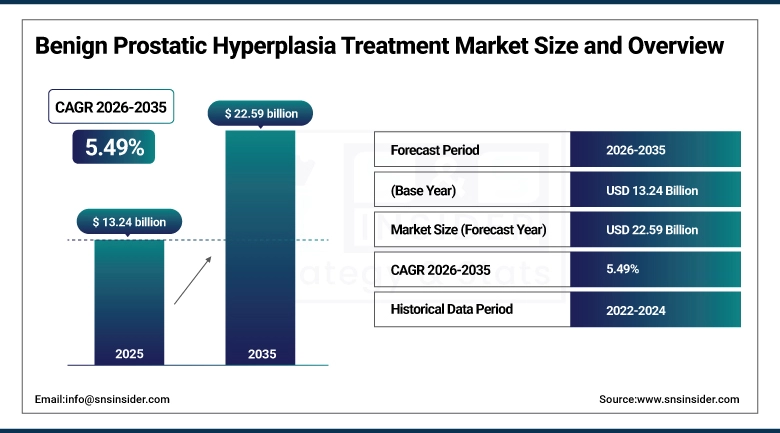

The Benign Prostatic Hyperplasia Treatment Market was estimated at USD 13.24 Billion in 2025 and is expected to reach USD 22.59 Billion by 2035 and grow at a CAGR of 5.49% over the forecast period of 2026-2035.

The global benign prostatic hyperplasia treatment market trend is rising prevalence of prostate enlargement in aging male populations, increasing awareness of minimally invasive surgical procedures, and advances in robotic-assisted technologies that are impacting the growth of the market. Another reason for this market growth is that more men are becoming aware of lower urinary tract symptoms and are more likely to seek treatment right away. This will lead to growth in both the surgical and pharmaceutical therapy markets, both in the U.S. and globally.

For instance, in March 2024, CDC reported that 29% of the U.S. men aged 40-70 experienced benign prostatic hyperplasia symptoms, highlighting rising condition prevalence and increasing demand for effective treatment modalities.

Market Size and Forecast:

-

Market Size in 2025: USD 13.24 billion

-

Market Size by 2035: USD 22.59 billion

-

CAGR: 5.49% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Benign Prostatic Hyperplasia Treatment Market - Request Free Sample Report

Benign Prostatic Hyperplasia Treatment Market Trends:

-

Rising cases of benign prostatic hyperplasia in males over 50 are increasing demand for minimally invasive and surgical treatments.

-

Adoption of patient-specific treatment plans based on prostate size, symptom severity, and comorbidities to improve outcomes.

-

Advancements in robotic-assisted systems, laser therapies, water vapor treatment, and prostatic urethral lift procedures to enhance precision and shorten recovery.

-

Integration of AI-based diagnostics, telemedicine, and remote monitoring for early detection, personalized care, and post-treatment follow-up.

-

Increasing preference for office-based procedures, same-day discharge, and outpatient facilities to improve convenience and reduce costs.

-

Collaborations among medical device companies, pharmaceutical firms, and research institutions to develop advanced therapies and accelerate clinical trials.

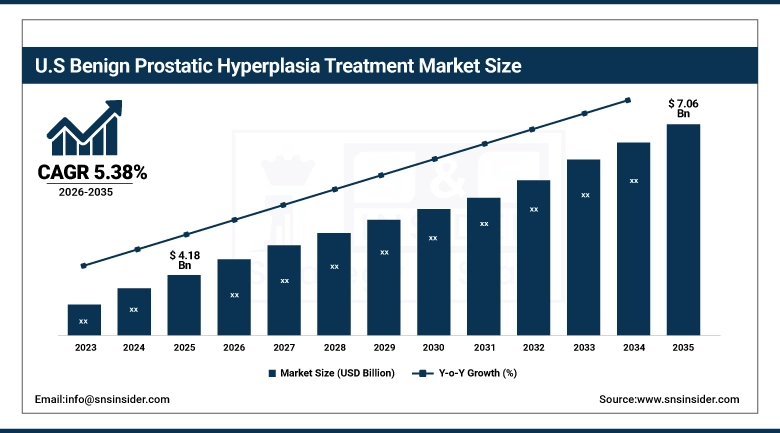

The U.S. Benign Prostatic Hyperplasia Treatment Market is estimated at USD 4.18 billion in 2025 and is projected to reach USD 7.06 billion by 2035, growing at a CAGR of 5.38% from 2026–2035. The U.S. has the biggest market share as prostate problems are so common, the healthcare system is so advanced, and less invasive therapies are becoming more popular. Favorable reimbursement rules, increasing healthcare spending, and growing awareness of urological health all help the market grow. The U.S. is also the biggest market in the world because of legislative support and early acceptance of new surgical technology and drugs.

Benign Prostatic Hyperplasia Treatment Market Growth Drivers:

-

Advanced Minimally Invasive Technologies are Driving the Benign Prostatic Hyperplasia Treatment Market Growth

Advanced minimally invasive technologies are becoming a major factor in the growth of the benign prostatic hyperplasia treatment market share. This is because robotic-assisted waterjet systems, laser enucleation, prostatic urethral lift devices, and water vapor thermal therapy are all being used to improve accuracy and recovery outcomes. These solutions for effectively relieving symptoms and preserving tissue are making the market stronger, leading to more people using them, and helping to grow the global market share.

For instance, in August 2024, the FDA granted 510(k) clearance to PROCEPT BioRobotics’ HYDROS AI-powered robotic system for Aquablation therapy, highlighting the rising adoption of precision surgical technologies and broader market penetration.

Benign Prostatic Hyperplasia Treatment Market Restraints:

-

High Treatment Costs and Limited Reimbursement are Hampering the Benign Prostatic Hyperplasia Treatment Market Growth

The expansion of the benign prostatic hyperplasia treatment market is slowed by high treatment costs and restricted reimbursement for new procedures. This is because many patients cannot afford innovative surgical and minimally invasive therapies without good insurance coverage. This leads to delayed treatment, more dependence on medication-based management, and poorer adoption rates in areas where people are sensitive to costs. Because of this, access to modern medicines is still limited, which slows down the total growth of the industry in places where healthcare is too expensive and insurance doesn't cover enough.

Benign Prostatic Hyperplasia Treatment Market Opportunities:

-

Artificial Intelligence and Digital Health Integration Drive Future Growth Opportunities for the Benign Prostatic Hyperplasia Treatment Market

Artificial intelligence and digital health integration in the benign prostatic hyperplasia treatment market can lead to new opportunities including AI-based imaging analysis, tools for predicting risk, and telemedicine platforms. These technologies help find diseases early, tailor treatment that works for each person, and keep an eye on symptoms from a distance. Better diagnosis, better treatment choices, and more patient involvement, especially in areas where urologists are hard to find, can all lead to better clinical results, fewer complications, and faster market growth.

For example, in January 2025, Mount Sinai Hospital became the first New York City facility to perform BPH procedures using the HYDROS Robotic System, demonstrating growing adoption of precision-guided technologies and rising demand for advanced BPH treatments.

Benign Prostatic Hyperplasia Treatment Market Segment Analysis:

-

By treatment, minimally invasive surgery held the largest share of about 58.32% in 2025, while invasive surgery is expected to grow steadily at a CAGR of 5.21%.

-

By procedure, transurethral resection of the prostate dominated with nearly 24.67% share in 2025, while prostate laser surgery is projected to register the highest growth at a CAGR of 6.18%.

-

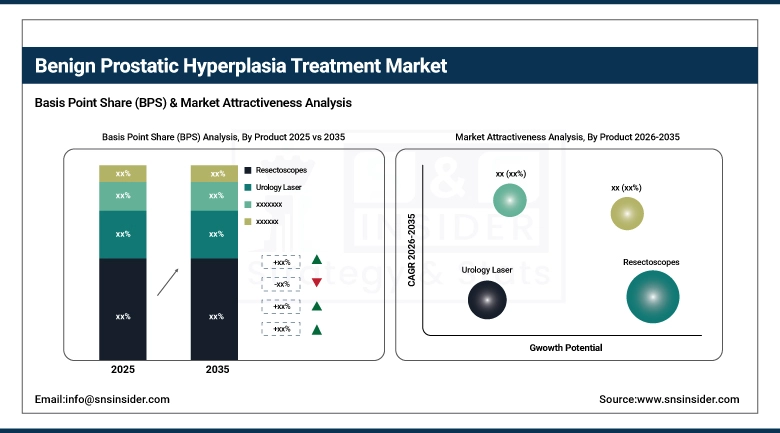

By product, resectoscopes accounted for around 28.45% share in 2025, while urology lasers are expected to grow fastest at a CAGR of 6.32%.

-

By end-use, hospitals led with approximately 62.74% share in 2025, while specialty facilities are forecast to expand at a CAGR of 5.89%.

By Product, Resectoscopes Lead, and Urology Lasers Register Fastest Growth

The resectoscopes segment held the largest share of the benign prostatic hyperplasia treatment market at about 28.45%, driven by their key role in standard transurethral resection procedures, established surgical practices, and ongoing device improvements. Market growth is supported by broad clinical use, compatibility with bipolar and monopolar systems, and steady demand from ambulatory surgery centers.

In addition, urology lasers are expected to register the fastest growth with a CAGR of around 6.32% during the forecast period of 2026–2035, as they enable precise tissue ablation, reduced bleeding, and strong hemostasis. Rising adoption is fueled by expanding indications across prostate sizes, lower equipment costs, favorable reimbursement, and improved safety compared to conventional electrocautery techniques.

By Treatment, Minimally Invasive Surgery Leads the Market, While Invasive Surgery Registers Steady Growth

The minimally invasive surgery segment held the largest revenue share of about 58.32% in 2025, driven by improved patient outcomes, shorter hospital stays, quicker recovery, and fewer complications than open surgery. Key trends include the growing use of prostatic urethral lift, water vapor therapy, and robotic-assisted procedures.

The invasive surgery segment is expected to register a steady CAGR of around 5.21% from 2025 to 2035, supported by its suitability for large prostate volumes and complex anatomies. Growth drivers include clinical need in severe obstruction cases and urologist preference for definitive tissue removal in treatment-resistant patients.

By Procedure, Transurethral Resection of the Prostate Segment Dominates, While Prostate Laser Surgery Shows Rapid Growth

The transurethral resection of the prostate segment held the largest revenue share of approximately 24.67% in 2025, supported by its gold-standard status, strong clinical evidence, and broad procedural familiarity among urologists worldwide. Key growth drivers include cost efficiency, proven long-term outcomes, and wide reimbursement coverage across healthcare systems.

The prostate laser surgery segment is expected to register the fastest CAGR of around 6.18% during 2026–2035, driven by advances in holmium and thulium laser technologies, lower bleeding risks, and reduced catheterization time. Additional drivers include rising preference for tissue-preserving procedures, improved safety for anticoagulated patients, and increased physician adoption of size-independent treatment options.

By End-use, Hospitals Lead, While Specialty Facilities Segment Grows Steadily

The hospitals segment held the largest revenue share of around 62.74% in the benign prostatic hyperplasia treatment market in 2025, driven by robust infrastructure, advanced surgical equipment, specialized care teams, and the ability to manage complex cases with extended monitoring. Growth is supported by strong referral networks, insurance-preferred status, and effective perioperative care management.

The specialty facilities segment is expected to register a CAGR of around 5.89% during the forecast period of 2026–2035, due to rising preference for outpatient care, dedicated urology centers, and efficient treatment workflows. Contributing factors include lower costs, reduced wait times, personalized care, and increasing adoption of office-based procedures.

Regional Insights

North America Benign Prostatic Hyperplasia Treatment Market Insights:

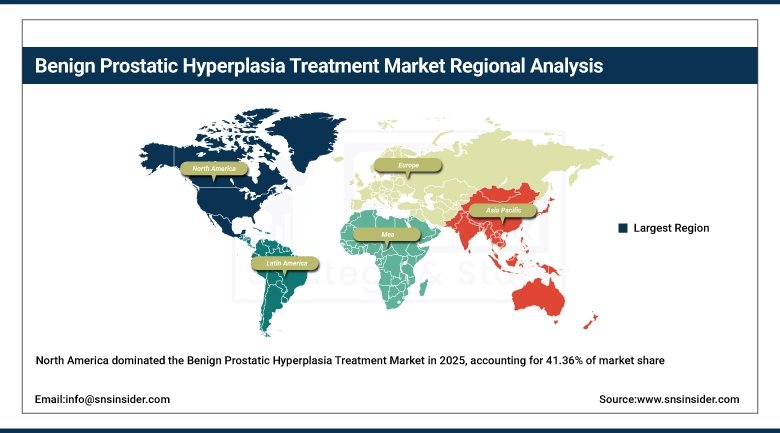

In 2025, North America had the highest share of the benign prostatic hyperplasia treatment market, with about 41.36% share due to the high number of older people with prostate enlargement, the advanced healthcare infrastructure, the wide range of insurance coverage, and the strong clinical awareness of urological disorders. Some of the main factors that are driving expansion are the widespread availability of improved surgical technology, high operation volumes, favorable payment policies, and the quick acceptance of minimally invasive treatments. Strong research funding, trained urologists, well-established clinical guidelines, and more and more men speaking up for their health also help the region stay on top of the market and bring in a lot of money from around the world.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Benign Prostatic Hyperplasia Treatment Market Insights:

Asia Pacific is the fastest-growing part of the benign prostatic hyperplasia treatment market, with a CAGR of 6.23% as more men are becoming conscious of their urological health, the population is becoming older, and healthcare infrastructure is getting better in emerging countries. Rapid urbanization, a growing number of older men, and more use of minimally invasive surgical technologies all help the region expand. Telemedicine growth and easier access to medical devices have made it easier for people to get treatment, especially in tier-2 and tier-3 cities. Government healthcare services and programs that train doctors urge people to get checked out and treated quickly. Also, lower treatment costs than in Western countries, together with more insurance coverage and better affordability, are still driving substantial growth in the Asia Pacific region.

Europe Benign Prostatic Hyperplasia Treatment Market Insights:

The market for benign prostatic hyperplasia therapy in Europe is the second largest after North America. This is because more and more older people are getting prostate problems, Europe has a well-developed healthcare system, and there are already established networks for urological care. The market is steadily growing in key European nations as more people using laser therapy and robotic-assisted operations, national health coverage that supports these treatments, EMA regulatory alignment, and government-backed men's health programs.

Latin America (LATAM) and Middle East & Africa (MEA) Benign Prostatic Hyperplasia Treatment Market Insights:

The benign prostatic hyperplasia treatment market is growing in Latin America and the Middle East & Africa as more people are becoming aware of prostate health, healthcare access is improving, diagnostics are getting better, and surgical treatments are becoming more widely available. More utilization of low-cost treatments, telemedicine consultations, and public health awareness campaigns leads to early diagnosis and quick treatment. Rapid urbanization, better economic conditions, and more middle-class people in these areas spending on healthcare are all still driving steady industry growth.

Competitive Landscape:

Boston Scientific Corporation (est. 1979) is a global medical technology leader focused on transforming lives through innovative medical solutions. It leverages extensive R&D investments and strategic acquisitions to produce cutting-edge benign prostatic hyperplasia devices with minimally invasive treatment capabilities.

-

In February 2025, it completed the USD 3.7 billion acquisition of Axonics, adding sacral neuromodulation devices for overactive bladder management, strategically expanding its urology portfolio and enhancing integrated treatment solutions for lower urinary tract symptoms.

PROCEPT BioRobotics Corporation (est. 2011) is a pioneering surgical robotics company revolutionizing BPH treatment through advanced image-guided systems. It develops AI-powered robotic platforms delivering Aquablation therapy with precision and consistency across diverse prostate anatomies.

-

In August 2024, received FDA 510(k) clearance for its HYDROS Robotic System with FirstAssist AI technology, representing a significant advancement in automated surgical precision and expanding market adoption of robotic-assisted BPH procedures nationwide.

Teleflex Incorporated (est. 1943) is a global provider of medical technologies designed to improve patient outcomes. Its UroLift System leads the prostatic urethral lift category, offering office-based treatment alternatives with rapid symptom relief and preserved sexual function.

-

In December 2024, launched the UroLift 2 System with Advanced Tissue Control, featuring laser-etched markers and customizable tissue manipulation capabilities for prostates up to 100 grams, significantly expanding procedural versatility and clinical applicability.

Benign Prostatic Hyperplasia Treatment Market Key Players:

-

Boston Scientific Corporation

-

PROCEPT BioRobotics Corporation

-

Teleflex Incorporated

-

Olympus Corporation

-

KARL STORZ SE & Co. KG

-

Lumenis Ltd.

-

Medtronic plc

-

Stryker Corporation

-

Cook Medical

-

Coloplast Group

-

Richard Wolf GmbH

-

Dornier MedTech

-

Biolitec AG

-

Urologix LLC

-

Asahi Kasei Corporation

-

B. Braun Melsungen AG

-

Urotronic Inc.

-

OmniGuide Inc.

-

Medifocus Inc.

-

ProArc Medical Ltd.

-

Merit Medical Systems

-

Quanta System S.p.A.

-

Convergent Laser Technologies

-

Prostalund Operations AB

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.24 Billion |

| Market Size by 2035 | USD 22.59 Billion |

| CAGR | CAGR of 5.49% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment (Minimal Invasive Surgery, Invasive Surgery) • By Procedure (Transurethral Resection of the Prostate, Prostate Laser Surgery, Transurethral Microwave Thermotherapy, Transurethral Needle Ablation of the Prostate, Prostatic Urethral Lift, Water Vapor Therapy, Robot-Assisted Laparoscopic Prostatectomy, Aquablation Therapy, Prostatic Artery Embolization, Open Prostatectomy, Bipolar Enucleation of Prostate, Transurethral Incision of the Prostate, High-Intensity Focused Ultrasound) •By Product (Resectoscopes, Urology Laser, Radiofrequency Ablation, Electrodes, Catheters, Prostatic Stents, Implants, Others) • By End-use (Hospitals, Specialty Facilities, Research and Manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Boston Scientific Corporation, PROCEPT BioRobotics Corporation, Teleflex Incorporated, Olympus Corporation, KARL STORZ SE & Co. KG, Lumenis Ltd., Medtronic plc, Stryker Corporation, Cook Medical, Coloplast Group, Richard Wolf GmbH, Dornier MedTech, Biolitec AG, Urologix LLC, Asahi Kasei Corporation, B. Braun Melsungen AG, Urotronic Inc., OmniGuide Inc., Medifocus Inc., ProArc Medical Ltd., Merit Medical Systems, Quanta System S.p.A., Convergent Laser Technologies, Prostalund Operations AB |

Frequently Asked Questions

Ans: North America dominated the Benign Prostatic Hyperplasia (BPH) Treatment market.

Ans: High Treatment Costs and Limited Reimbursement are Hampering the Benign Prostatic Hyperplasia Treatment Market Growth

Ans: Advanced Minimally Invasive Technologies are Driving the Benign Prostatic Hyperplasia Treatment Market Growth

Ans: The Benign Prostatic Hyperplasia (BPH) Treatment market is expected to reach USD 22.59 Billion by 2035.

Ans: The Benign Prostatic Hyperplasia (BPH) Treatment market is anticipated to grow at a CAGR of 5.49% from 2026 to 2035.

Get in Touch