AI in Diagnostics Market Report Scope & Overview:

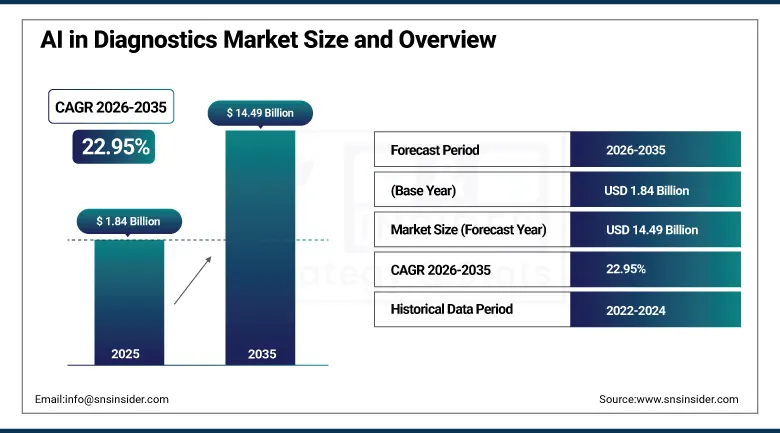

The AI in Diagnostics Market was valued at USD 1.84 Billion in 2025 and is expected to reach USD 14.49 Billion by 2035, growing at a CAGR of 22.95% from 2026 to 2035.

The AI in Diagnostics Market will remain to grow very quickly as the growth in the market is being fuelled by developments in the realms of machine learning and deep learning which help create quicker and more accurate diagnostic solutions. The AI-powered diagnostic tools continue to change the approach towards diagnosing various diseases around the world including diagnosing the early stages of cancer as well as predicting any problems related to the heart. The application of such technologies has grown rapidly in the fields of radiology, oncology, cardiology, neurology, and pathology. With the increase in the amount of images created and lack of corresponding personnel, the market will remain to grow as a core element of healthcare systems.

Metropolis Healthcare introduced a state-of-the-art testing platform using Component Resolved Diagnostics technology in May 2023 to detect allergies in India, with this fourth-generation technology leveraging artificial intelligence to help clinicians make more informed treatment decisions and offering deeper insights that continue aiding optimization of allergy treatment plans.

Market Size and Forecast

- Market Size in 2026E: USD 2.26 Billion

- Market Size by 2035: USD 14.49 Billion

- CAGR: 22.95% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

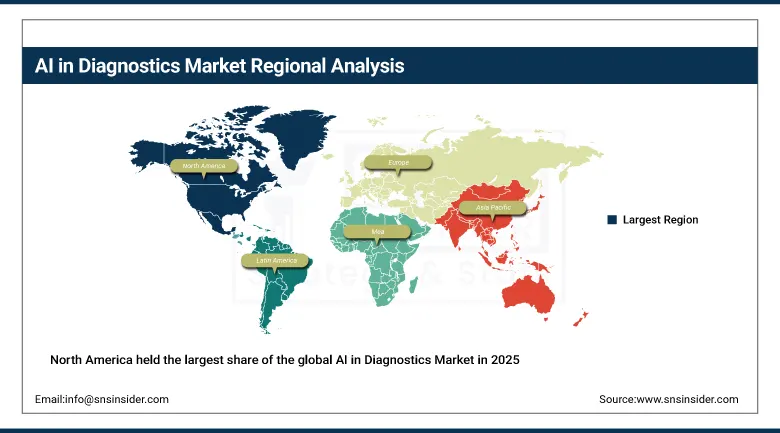

- Largest Region: North America

To Get more information On AI in Diagnostics Market - Request Free Sample Report

AI in Diagnostics Market Trends

- Maturing regulation, dedicated reimbursement codes, and accelerating algorithmic performance gains continue driving expansion.

- As imaging volumes rise faster than staff rosters, AI in diagnostics continues becoming core infrastructure rather than an optional add-on.

- AI-powered image analysis tools continue enhancing diagnostic precision, reducing human error, and shortening interpretation time.

- National policies increasingly combine grants, standards, and payment reform to support AI-enabled diagnostic device adoption.

- Government-backed AI programs and expanding healthcare digitization continue accelerating adoption across emerging healthcare markets.

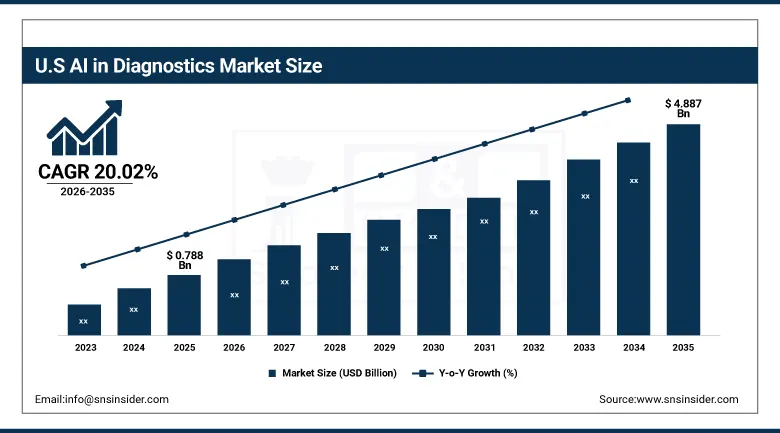

The United States AI in Diagnostics Market Outlook

The United States AI in Diagnostics Market was valued at USD 0.788 Billion in 2025 and is expected to reach USD 4.887 Billion by 2035, growing at a CAGR of 20.02% from 2026 to 2035.

The United States occupied a dominant market position in North American AI diagnostics in terms of market revenue share due to its robust research infrastructure, efficient health care sector, and supportive government regulations. In January 2025, FDA released its guidance regarding AI-enabled medical devices in order to specify requirements in terms of clinical trials and post-market supervision. Meanwhile, the U.S. Department of Health and Human Services (HHS) Artificial Intelligence Strategy allocated money for pilot hospital projects and established HHS AI Council.

AliveCor, headquartered in Mountain View, California, continued expanding its AI-powered cardiac diagnostic device portfolio in 2025, reinforcing its position as a leading American developer of personal ECG and cardiac monitoring technology enhanced by machine learning algorithms.

AI in Diagnostics Market Segmentation Analysis

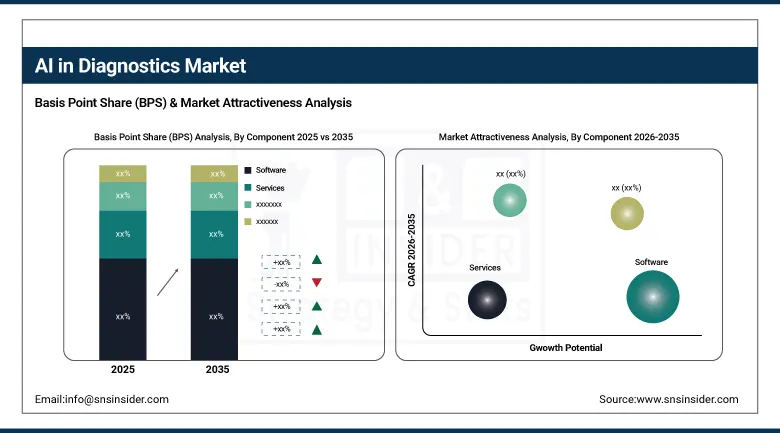

- By Component, the software segment held approximately 46.20% share in AI in diagnostics market in 2025, while the same segment is also the fastest growing.

- By Diagnostic Type, the neurology segment held approximately 25.00% share in ai in diagnostics market in 2025, while the radiology segment is the fastest growing.

- By Diagnostic Modality, the imaging segment held approximately 57.64% share in ai in diagnostics market in 2025, while the in vitro diagnostics segment is the fastest growing, with a CAGR of approximately 32.90%.

- By End-User, the hospitals segment held approximately 57.88% share in ai in diagnostics market in 2025, while the diagnostic laboratories segment is the fastest growing, with a CAGR of approximately 32.85%.

By Component, software dominated the AI in diagnostics market and grew fastest

The software segment dominated the component category in 2025, holding approximately 46.20% of total revenue, and is also expected to showcase the fastest CAGR during the forecast period, anchored by AI algorithms that power image analysis, predictive analytics, and natural language processing across diagnostic workflows. That dual leadership and fastest-growth position reflects how comprehensively software-driven diagnostic intelligence continues capturing value relative to the broader component segmentation.

Services, including implementation, training, and clinical integration support, continue holding a meaningful share of overall AI in diagnostics demand, as healthcare providers increasingly seek expert guidance to deploy increasingly sophisticated diagnostic algorithms responsibly. That professional services layer keeps this component category relevant even as software continues capturing the largest share of overall market growth.

By Diagnostic Type, neurology dominated the AI in diagnostics market, radiology grew fastest

The neurology segment held the largest diagnostic type share in 2025, at approximately 25.00%, accounting for the greatest number of regulatory approvals among AI-based medical diagnostics platforms. That substantial regulatory approval base keeps neurology firmly at the top of the broader diagnostic type segmentation across nearly every major AI diagnostics program worldwide.

The radiology segment is projected to grow at the fastest CAGR during the forecast period, on account of growing improvement of AI-based software for diagnostic imaging that continues enhancing precision and reducing interpretation time. As imaging volumes keep rising faster than available radiologist staffing, rising demand for AI-assisted diagnostic imaging continues pushing this diagnostic type category's growth rate ahead of the broader diagnostic type segmentation.

By Diagnostic Modality, imaging dominated the AI in diagnostics market, in vitro diagnostics grew fastest

The imaging segment held the largest diagnostic modality share in 2025, at approximately 57.64%, anchored by AI's established, well-validated role in analyzing medical imaging scans across radiology, oncology, and neurology applications. That established clinical validation keeps imaging firmly at the top of the broader diagnostic modality segmentation across the majority of current AI diagnostics deployments worldwide.

The in vitro diagnostics segment is projected to grow at the fastest CAGR of approximately 32.90% during the forecast period, as AI algorithms increasingly enhance laboratory-based diagnostic testing including genetic analysis and biomarker detection. Rising demand for AI-enhanced laboratory diagnostics continues pushing this diagnostic modality category's growth rate ahead of the broader diagnostic modality segmentation.

By End-User, hospitals dominated the AI in diagnostics market, diagnostic laboratories grew fastest

The hospitals segment held the largest end-user share in 2025, at approximately 57.88%, anchored by comprehensive diagnostic infrastructure and specialist availability that continues supporting complex AI-assisted diagnostic workflows. That established clinical infrastructure keeps hospitals firmly at the top of the broader end-user segmentation across nearly every major AI in diagnostics deployment worldwide.

The diagnostic laboratories segment is projected to grow at the fastest CAGR of approximately 32.85% during the forecast period, as centralized reference laboratories increasingly process high-throughput AI-enhanced diagnostic testing for multiple healthcare provider networks simultaneously. Rising outsourcing of specialized AI-enhanced testing continues pushing this end-user category's growth rate ahead of the broader end-user segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.20% |

|

Europe |

Germany |

27.40% |

|

Asia Pacific |

China |

36.60% |

|

Middle East & Africa |

UAE |

26.50% |

|

Latin America |

Brazil |

37.20% |

North America AI in Diagnostics Market Insights

North America held the largest share of the global AI in Diagnostics Market in 2025, at approximately 54.80%, driven by increasing technological advancements and emphasis on utilizing advanced tools for maintaining tedious diagnostic workflows across the region. Strong research infrastructure, advanced healthcare systems, and favorable regulatory support continued reinforcing this leadership position throughout the year.

The USA had around 86.20% contribution to the regional revenue, given that it has leading developers of AI diagnostic platforms and a well-established system of healthcare reimbursements. Canada, on its part, had a lesser share, though growing, due to AI healthcare technologies being adopted in Canada, thus keeping North America way ahead of all other regions within the market segment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe AI in Diagnostics Market Insights

Europe held a substantial share of the global AI in Diagnostics Market in 2025, supported by well-established national health insurance coverage and strong biotechnology and medical device innovation across the continent. Germany accounted for roughly 27.40% of regional revenue, supported by its concentration of medical technology companies and advanced healthcare infrastructure.

France, the United Kingdom, and the Nordic countries followed a broadly similar trajectory, as continued investment in AI-enabled healthcare technology extended AI diagnostics adoption across the continent's largest healthcare markets. Continued regulatory support for AI-enabled medical devices is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific AI in Diagnostics Market Insights

Asia Pacific was the fastest-growing region in the global AI in Diagnostics Market, driven by government-backed AI programs and expanding healthcare digitization across the region's largest and most populous economies. Rising healthcare infrastructure investment continued driving regional demand at a pace considerably faster than more mature Western markets.

China was responsible for almost 36.60% of regional revenues due to its aggressive AI healthcare policies within the country along with technological development in diagnostics. Both Japan and South Korea were major contributors to the regional revenues due to adoption of healthcare technology within these countries, and thus Asia Pacific is clearly the growth leader.

MEA & Latin America AI in Diagnostics Market Insights

The Middle East and Africa region recorded steady growth in AI in diagnostics adoption in 2025, driven by expanding healthcare infrastructure investment and growing government support for AI-enabled diagnostic technology across the Gulf states in particular. The UAE accounted for roughly 26.50% of regional revenue, supported by national healthcare modernization strategies and rising demand for advanced diagnostic technology.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.20% of regional revenue, where growing healthcare infrastructure investment continued to support category growth. Mexico and Argentina followed a similar trajectory as regional AI healthcare technology adoption expanded further through the remainder of the forecast period.

Growth Drivers: Rising diagnostic imaging volumes and regulatory maturation

Advancements in machine learning and deep learning, enabling faster, more accurate diagnostic solutions, continue to be the central force behind AI in diagnostics market growth. As imaging volumes keep rising faster than staff rosters, the AI in diagnostics market continues becoming core infrastructure rather than an optional add-on across nearly every major healthcare system worldwide.

Maturing regulation, the arrival of dedicated reimbursement codes, and accelerating algorithmic performance gains continue reinforcing structural demand growth. National policies combining grants, standards, and payment reform, exemplified by the U.S. HHS AI Strategy earmarking funding for hospital pilots, continue reinforcing sustained market expansion across the broader AI in diagnostics market.

Restraints: Clinical validation requirements and integration complexity

Rigorous clinical validation requirements for AI-driven diagnostic tools continue requiring substantial evidence generation before algorithmic tools can be fully integrated into regulated diagnostic workflows. That validation burden continues adding time and cost to AI deployment even as the underlying regulatory environment grows more supportive following recent guidance clarifications.

Integrating AI diagnostic tools with existing hospital information systems and picture archiving and communication systems continues requiring genuine technical expertise that can complicate deployment timelines for organizations lacking dedicated IT resources. That integration complexity continues concentrating the most sophisticated AI diagnostics deployments among organizations with adequate technical implementation capability.

Opportunities: In vitro diagnostics expansion and emerging market healthcare digitization

Growing application of AI algorithms to laboratory-based diagnostic testing presents substantial opportunity for developers positioned to serve this rapidly expanding in vitro diagnostics category beyond traditional imaging applications. Companies capable of delivering genuinely accurate, AI-enhanced laboratory diagnostic tools stand to capture a growing share of demand as this technology continues maturing.

Expanding government-backed AI programs and healthcare digitization across emerging markets presents a further significant growth avenue, as more regions develop the infrastructure and regulatory framework that AI diagnostics adoption requires. Companies capable of delivering affordable, scalable AI diagnostic solutions stand to capture meaningful new revenue streams as these markets continue developing through 2035.

Recent Developments:

- 2023: Qritive launched QAi Prostate in March, an AI-powered diagnosis tool designed to assist clinicians in detecting and characterizing prostate cancer with improved precision and reduced interpretation time.

- 2025: PathAI continued expanding its AI-powered pathology diagnostic platform, strengthening its position serving laboratories and pharmaceutical companies requiring precise, algorithm-assisted tissue analysis for cancer diagnosis and drug development.

- 2026: GE HealthCare announced expanded AI-powered diagnostic imaging capabilities across its Edison digital health platform, introducing advanced workflow automation and clinical decision support to improve radiology efficiency and diagnostic accuracy across multiple imaging modalities.

AI in Diagnostics Market key players are:

- AliveCor, Inc.

- IBM Corporation

- GE HealthCare

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- Google LLC

- Microsoft Corporation

- PathAI, Inc.

- Paige.AI, Inc.

- Aidoc Medical Ltd.

- Viz.ai, Inc.

- Butterfly Network, Inc.

- Qure.ai Technologies Pvt. Ltd.

- Arterys Inc.

- Corti ApS

- Cleerly, Inc.

- HeartFlow, Inc.

- Enlitic, Inc.

- Tempus AI, Inc.

- Metropolis Healthcare Limited

AI in Diagnostics Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.84 Billion |

| Market Size by 2035 | USD 14.49 Billion |

| CAGR | CAGR of 22.95% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Diagnostic Type (Neurology, Radiology, Pathology, Others) • By Diagnostic Modality (Imaging, In Vitro Diagnostics) • By End-User (Hospitals, Diagnostic Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AliveCor, Inc., IBM Corporation, GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., Google LLC, Microsoft Corporation, PathAI, Inc., Paige.AI, Inc., Aidoc Medical Ltd., Viz.ai, Inc., Butterfly Network, Inc., Qure.ai Technologies Pvt. Ltd., Arterys Inc., Corti ApS, Cleerly, Inc., HeartFlow, Inc., Enlitic, Inc., Tempus AI, Inc., Metropolis Healthcare Limited |

Frequently Asked Questions

The AI in Diagnostics Market is expected to grow at a CAGR of 22.95% from 2026 to 2035.

The AI in Diagnostics Market was valued at USD 1.84 Billion in 2025.

Advancements in machine learning and deep learning combined with rising diagnostic imaging volumes and maturing regulation is the major growth factor.

The Software segment held approximately 46.20% share in 2025 and was also the fastest-growing component segment.

North America held the largest share of the AI in Diagnostics Market in 2025, at approximately 54.80%.

Get in Touch