Bifacial Solar Panel Market Report Scope & Overview:

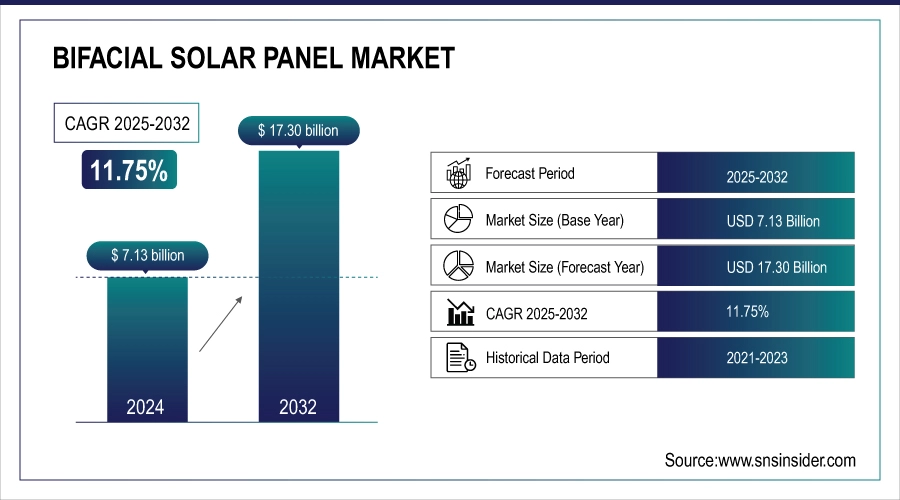

The Bifacial Solar Panel Market Size was valued at USD 7.13 billion in 2024 and is expected to reach USD 17.30 billion by 2032 and grow at a CAGR of 11.75% over the forecast period 2025-2032.

The growth of the Bifacial Solar Panel Market is poised for growth as demand for clean and renewable energy rise across countries as they pursue decarbonization and carbon-neutral targets. By design, bifacial modules capture irradiation from both the front and back sides of the panel, making bifacial modules higher performing panels than traditional monofacial panels and reducing the LCOE rate of electricity output. The performance is also enabled by technology such as transparent backsheets and advanced tracking systems yielding even higher levels of adoption. According to study, Utility-scale PV systems now more than ever monopolize by bifacial modules and single-axis trackers, which account for more than 90% of modules sold and over 60% of PV systems in the segment.

Bifacial Solar Panel Market Size and Forecast

-

Market Size in 2024: USD 7.13 Billion

-

Market Size by 2032: USD 17.30 Billion

-

CAGR: 11.75% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Bifacial Solar Panel Market - Request Free Sample Report

Key Bifacial Solar Panel Market Trends

-

Increasing adoption in utility-scale, commercial, and residential projects.

-

Rising energy yield due to dual-sided sunlight capture.

-

Integration with single-axis trackers for optimized performance.

-

Government incentives like the Inflation Reduction Act supporting growth.

-

Expansion into floating solar and high-albedo desert installations.

-

Technological advancements: transparent backsheets, lightweight glass, and AI monitoring.

-

IoT-enabled smart trackers for predictive maintenance and efficiency optimization.

-

Growing global focus on carbon neutrality driving renewable energy investments.

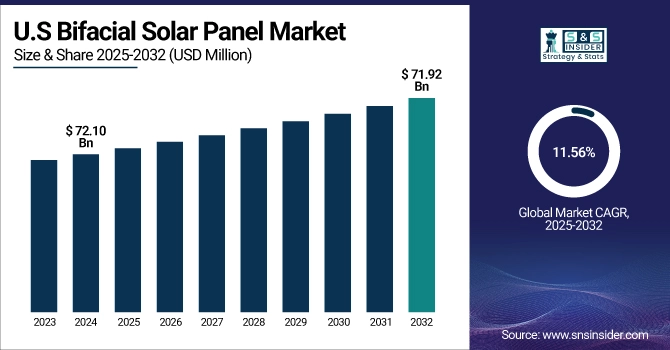

The U.S. bifacial solar panel market size was USD 72.10 billion in 2024 and is expected to reach USD 71.92 billion by 2032, growing at a CAGR of 11.56% over the forecast period of 2025-2032. driven by higher energy efficiency, strong federal incentives, and rising adoption in utility-scale projects.

Bifacial Solar Panel Market Growth Drivers:

-

Higher Efficiency and Growing Renewable Energy Adoption

The Bifacial Solar Panel is anticipated to be significant since these panels have a unique design that enables them to capture sunlight from either side, thus providing energy yields of more than 20% higher than traditional modules. This enhances project returns while mitigating LCOE for large-scale farms. Single-axis trackers boost performance by tracking the sun as it moves across the sky during the day. United States supportive policies such as the Inflation Reduction Act with its tax credits and subsidy mechanisms, further support adoption in utility, commercial, and residential contexts.With some utility-scale projects suggesting delivering electricity up to 16% more cheaply than monofacial systems, the carbon-neutrality pledges are underpinning the latest boom in bifacial investment.

Bifacial solar panels can achieve energy yields up to 35% higher than traditional monofacial panels when paired with single-axis trackers, significantly enhancing overall system performance.

Bifacial Solar Panel Market Restraints:

• High Installation Costs and Limited Efficiency in Low-Reflective Environments

Despite bifacial solar panels are more efficient, they also require more expensive mounting systems, and construction at considerably higher structures than single-sided types, and therefore have a higher upfront cost. They are highly dependent on albedo for their performance, meaning returns become fairly inadequate in low-reflective surroundings such as asphalt or grass. The fragmentation of rear-side gains complicates the price of rear-side gains, creating difficulty in financing and uncertainty for investors. Additionally, cheaper and more efficient monofacial panels are hard to beat for cost-sensitive buyers.

Bifacial Solar Panel Market Opportunities:

• Expansion in Utility-Scale, Floating Solar, and Emerging Markets

The technology has potential in large farms as well as floating solar and deserts where high albedo enhances the energy yield. In areas where the sun shines abundantly, such as Asia-Pacific, Latin America, and the Middle East, conditions are ripe for development Innovation in transparent backsheets, lightweight glass, and AI-enabled performance monitoring improve longevity and efficiency. Integrating with IoT and smart trackers enable predictive maintenance and optimized output. In contrast, bifacial modules in floating solar projects can provide roughly 20% greater yields than standard monofacial installations.

In June 2025, Jolywood announced the mass production of its new n-type TOPCon bifacial modules with improved light-induced degradation resistance, aimed at utility-scale applications.

Key Bifacial Solar Panel Market Segment Analysis

-

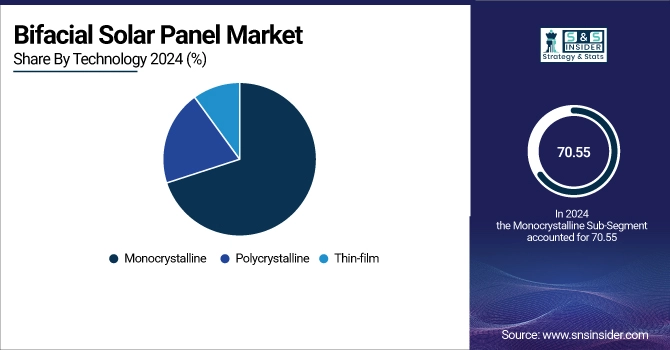

By Technology, Monocrystalline led with ~70.55% share in 2024; Thin-film fastest growing (CAGR 13.20%).

-

By Application, Residential dominated ~9.10% in 2024; Commercial fastest growing (CAGR 13.01%).

-

By Cell Structure, Half-cut led ~67.80% in 2024, Shingled fastest growing (CAGR 12.94%).

-

By Bifaciality Factor, Below 80% led ~5.80% in 2024, 80-90% fastest growing (CAGR 12.42%).

By Technology, Monocrystalline Leads Market While Thin-film Fastest Growth

In 2024, The Bifacial Solar Panel Market for Monocrystalline segment leads due to attributes such as higher efficiency, durability, and large-scale utility projects. These panels deliver higher power output, making them the preferred choice for developers aiming at maximum returns. During this period, the Thin-film segment is anticipated to experience the fastest growth in 2025–2032, The growth of the Thin-film segment can be attributed to its lightweight and flexibility as well as the adaptability of Thin-film solar panels to floating solar and niche installations. At the same time, Polycrystalline panels continue steady adoption in cost-sensitive projects in which price trumps power.

By Application, Residential Leads Market While Commercial Fastest Growth

In 2024, The Bifacial Solar Panel Market is dominated by the Residential segment due to increasing adoption of rooftop solar panels, favourable incentives, and growing consumer awareness regarding the benefits of clean energy. Commonly Found in Cities and Suburbs While they require a larger initial investment, these installations save you a lot in the long run. The Commercial segment is expected to grow at the fastest CAGR in the 2025–2032 period owing to the flexibility provided to businesses in terms of energy independence and effort to reduce operating costs as well as sustainability commitments. The Utility-scale segment also accounts for a large share as the use of bifacial modules in large solar farms increases, due to its ability to increase energy yield and reduce project LCOE.

By Cell Structure, Half-cut Leads Market While Shingled Fastest Growth

In 2024, On the basis of Bifacial Solar Panel type, Half-cut cell structure segment dominates the market and is likely to continue leading in the forecast period due to its higher efficiency along with low power loss and better durability which eventually optimize market to suit large installations. The Shingled cell segment is expected to exhibit the highest growth over the period 2025–2032 due to its unique design of shingled overlap, which offers reduced space consumption, increased performance and greater aesthetics. The segment with interdigitated back contact (IBD) is also being popular thanks to its prospects for top-notch efficiency in high-end applications of solar.

By Bifaciality Factor, Below 80% Leads Market While 80–90%Fastest Growth

In 2024, the Below 80% segment held the largest share of the Bifacial Solar Panel Market, primarily owing to its commercial availability, reduced manufacturing costs, and increased installation in residential and utility-scale applications. This category sees consistently high efficiency gains when compared to typical monofacial modules in a cost-competitive manner, thus proving to be the most frequently-implemented realm by developers and homeowners. The segment over the 80%–90% is expected to record the highest growth in 2025–2032 owing to continuous innovations in cell design, transparent backsheets, and encapsulation techniques.

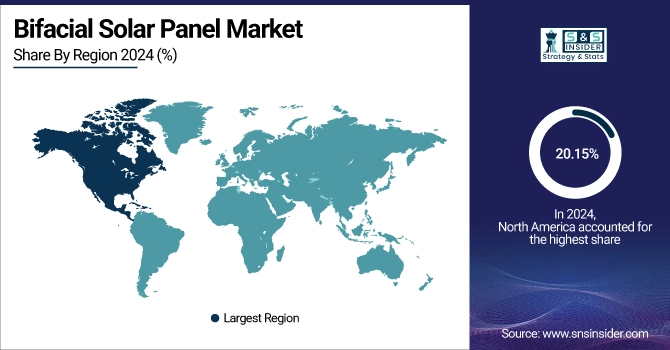

North America Bifacial Solar Panel Market Insights:

In 2024, North America held a 20.15% share of the Bifacial Solar Panel Market, due to large-scale renewable energy projects, governmental support incentives, and swift adoption of solar power in residential, commercial, and utility-scale projects. Tax credits and subsidies embedded in the U.S. Inflation Reduction Act is a significant growth catalyst with incentives associated with deployment of advanced solar technologies. Additionally, rising corporate sustainability goals, demand for energy independence, and increasing investments in solar farms are additional factors driving the market growth in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Leads Bifacial Solar Panel Market with Policy Support and High-Efficiency Deployment

The US leads the region, due to higher energy yields, strong federal incentives, and large-scale utility deployments. Policies conducive to adoption, such as the Inflation Reduction Act, spurs adoption across the residential, commercial, and utility scale sectors. Bifacial panels continue to be one of the key drivers of America's transition to a more renewable energy future with continuing advances in heterojunction and tracking technologies and strengthening domestic manufacturing.

Asia-Pacific Bifacial Solar Panel Market Insights

In 2024, Asia Pacific emerged as the fastest-growing bifacial solar panel market with a 12.53% share, supported by due to rapid industrial growth along with favorable government policies coupled with massive investments on renewable energy infrastructure. As energy needs and carbon reduction plans grow in the region, national expansion of utility-scale solar farms, floating solar and commercial rooftop systems are being pursued by countries all over. Falling module prices and strong levels of solar irradiance combined with better financing options helps to speed up adoption. Moreover, joint efforts between private enterprises and governments, and technology development in solar tracker and cell structure, all driving regional progress are putting Asia Pacific as the world, largest region in terms of bifacial solar deployment.

China and India Drive Rapid Growth in Bifacial Solar Panel Market

China leads the Asia Pacific bifacial solar panel market, driven by large-scale manufacturing capacity, aggressive renewable energy targets, and continuous investments in ultra-mega solar parks and floating solar projects across diverse terrains.

Europe Bifacial Solar Panel Market Market Insights

In 2024, Europe accounted for 20.68% of the bifacial solar panel market, facilitated by enabling policy frameworks, targets for carbon neutrality, and increasing installations of advanced solar systems in the residential, commercial, and utility-scale sectors. Favorable environment for bifacial technology adoption due to European Union´s Green Deal and national Renewable Energy Incentives Rooftop sunlight and massive bifacial farms are seeing big investments driven by high power expense and also the need for power self-sufficiency.

Germany Leads Europe in Bifacial Solar Panel Market Market Growth

Germany dominates the European bifacial solar panel market, supported by ambitious renewable targets, strong policy incentives, and rapid deployment of rooftop and utility-scale solar projects, reinforcing its leadership in Europe’s clean energy transition.

Latin America (LATAM) and Middle East & Africa (MEA) Bifacial Solar Panel Market Insights

In 2024, The Middle East & Africa and Latin America combination has maintained and increased its share of the bifacial solar panel market, driven by high solar irradiance levels, government support, and growing renewable energy investments. The Middle East has large desert environments that provide excellent high-albedo bifacial opportunities, while Latin America takes advantage of large energy demand and larger scale solar farms. Declining costs of panels, supportive international financing and encouragement of energy diversification are further boosting adoption in these regions, which are set to be new solar hubs for growth.

Competitive Landscape for Direct Imaging System Market

LONGi Green Energy Technology Co., Ltd. is a global leader in solar technology, specializing in high-efficiency monocrystalline and bifacial modules. The company focuses on durability, sustainability, and innovation in utility-scale and distributed solar projects, supported by strong R&D investments to enhance long-term performance.

-

In May 2025, LONGi introduced the Ice-Shield bifacial module, featuring a 3.2 mm tempered glass layer for enhanced durability.

Trina Solar Limited is a major provider of solar products and smart energy solutions, offering advanced photovoltaic modules, solar cells, and integrated energy systems. The company emphasizes next-generation solar innovations, including high-power modules and perovskite-silicon tandem technologies, to maximize efficiency and output in diverse applications.

-

In June 2025, Trina Solar unveiled a perovskite-silicon tandem solar module prototype delivering 841 W and 27.1% efficiency.

JinkoSolar Holding Co., Ltd. is one of the world’s largest solar manufacturers, known for its pioneering work in high-efficiency modules and advanced cell technologies. With a global supply chain and wide adoption across residential, commercial, and utility markets, JinkoSolar focuses on n-type TOPCon and bifacial innovations.

-

In June 2025, at SNEC 2025, JinkoSolar launched the Tiger Neo 3.0 series bifacial modules, featuring n-type TOPCon technology for enhanced efficiency.

Bifacial Solar Panel Companies are:

-

LONGi Solar

-

Trina Solar

-

JinkoSolar

-

Canadian Solar (CSI Solar)

-

JA Solar

-

Risen Energy

-

Astronergy (CHINT)

-

GCL System Integration (GCL-SI)

-

HT-SAAE

-

Suntech

-

Qcells (Hanwha)

-

EGing PV

-

Talesun

-

DMEGC

-

ZNShine Solar

-

Waaree Energies

-

Vikram Solar

-

Leapton Solar

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 7.13 Billion |

| Market Size by 2032 | USD 17.30 Billion |

| CAGR | CAGR of 11.75% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Monocrystalline, Polycrystalline, Thin-film) • By Application (Residential, Commercial, Utility-scale) • By Cell Structure (Half-cut, Shingled, Interdigitated Back Contact (IBC)) • By Bifaciality Factor (Below 80%, 80–90%, Above 90%) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | LONGi Solar, Trina Solar, JinkoSolar, Canadian Solar (CSI Solar), JA Solar, Risen Energy, Jolywood, Astronergy (CHINT), GCL System Integration (GCL-SI), HT-SAAE, Suntech, Qcells (Hanwha), EGing PV, Talesun, DMEGC, ZNShine Solar, Adani Solar, Waaree Energies, Vikram Solar, Leapton Solar, and Others. |

Frequently Asked Questions

North America dominated the Bifacial Solar Panel Market in 2024.

The Monocrystalline segment dominated the Bifacial Solar Panel Market.

The major growth factor of the bifacial solar panel market is the increasing demand for higher-efficiency solar modules and greater energy yield in utility-scale and commercial installations.

The Bifacial Solar Panel Market size was USD 7.13 billion in 2024 and is expected to reach USD 17.30 billion by 2032.

The Bifacial Solar Panel Market is expected to grow at a CAGR of 11.75% during 2025-2032.

Get in Touch