Laboratory Products and Services Outsourcing Market Report Scope & Overview:

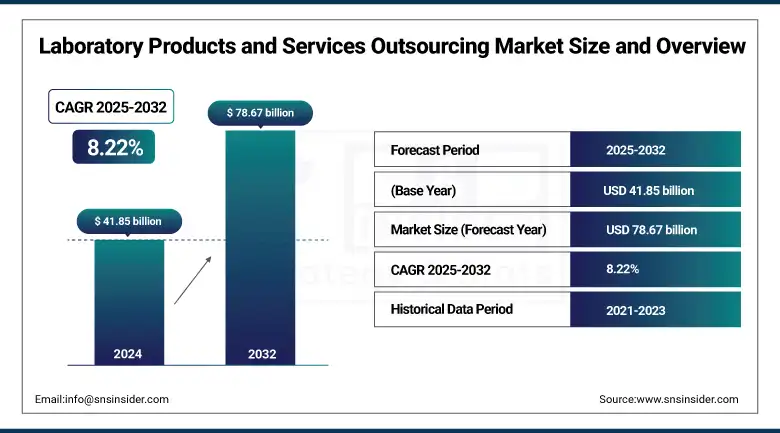

The laboratory products and services outsourcing market size was valued at USD 41.85 billion in 2024 and is expected to reach USD 78.67 billion by 2032, growing at a CAGR of 8.22% over 2025-2032.

The global laboratory products and services outsourcing market is being reshaped as pharmaceutical R&D grows more complex, cost pressures increase, and the need to bring new drugs to market more quickly intensifies. Laboratory operations, including bioanalytical testing, preclinical development, clinical trial support, and quality control, are being outsourced by companies to specialized service providers.

One of the contributing factors that is responsible for the laboratory products and services outsourcing market growth is the increase in the biopharmaceutical R&D investment, which exceeded USD 238 billion globally in 2023, and the U.S. contributed over half of this total. Additionally, increasing regulation and requirements for GLP and GMP studies are driving pharma companies to work with CROs and lab service providers that can provide compliant infrastructure and know-how.

To Get more information On Laboratory Products and Services Outsourcing Market - Request Free Sample Report

In March 2024, Eurofins Scientific unveiled digital tools for lab support that aim to facilitate data sharing and remote project tracking, indicating a direction for the lab services market that goes toward automation and AI-based service provision.

The scientific laboratory products and services outsourcing market is also driven by fast-paced technological developments and government support to improve research infrastructure in the U.S. Growing interest in personalized medicine, biologics, and precision diagnostics has increased outsourcing to optimize efficiency and scale. Furthermore, the growth of interest in venture capital and private equity investments in biotech start-ups, which exceeded USD 27 billion in 2023, also fuels demand for outsourced services.

In April 2024, Thermo Fisher Scientific added to its North American bioanalytical lab services in response to growing demand for the outsourcing of preclinical and clinical testing services.

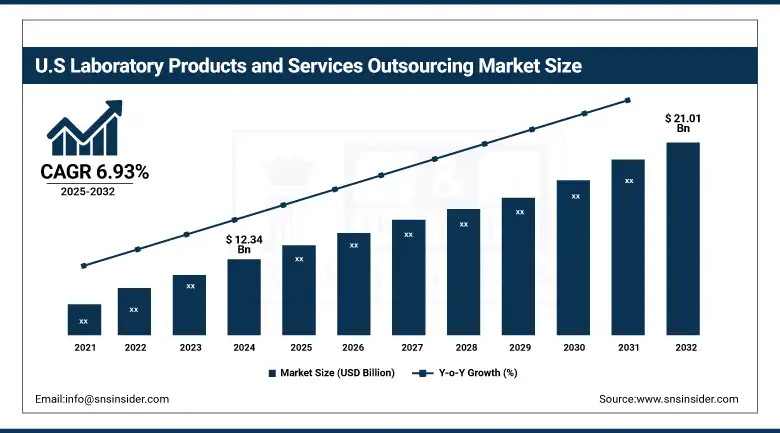

The U.S. Laboratory Products and Services Outsourcing market size was valued at USD 12.34 billion in 2024 and is expected to reach USD 21.01 billion by 2032, growing at a CAGR of 6.93% over 2025-2032.

Market Dynamics:

Drivers:

-

Rising Demand for R&D Efficiency and Technological Advancement Propels Market Growth

The laboratory products and services outsourcing market growth is predominantly driven by the increasing R&D spending in the pharmaceutical and biopharmaceutical industry, growing demand for specialized testing services, and pressure to reduce the cost and drug development timelines. Nowadays, pharmaceutical companies tend to contract out their laboratory work to CROs to avoid expensive machines.

R&D expenditure is well more than USD 248 billion, according to the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA). An increase and acceptance of services, such as bioanalytical testing, method validation, stability studies, and toxicology checks, has occurred. Advancements in digital lab automation, robotics, and AI applications, when integrated with data analytics, are driving the laboratory products and services outsourcing market trends for the outsourcing of complex biologics and gene therapies.

Regulatory agencies, such as the FDA and EMA, have also made outsourcing regulations more flexible and have increased vendor compliance disclosure requirements. Also, the core players are drawing their attention from the small lab outsourcing segment by entering into strategic alliances with niche companies to enhance scalability and to establish global footprints, which would in turn enhance the laboratory products and services outsourcing market share. Rising investment in biotech (more than 6,000 clinical trials underway globally in 2023) makes demand even stronger, validating the optimism in the laboratory products and services outsourcing market forecast.

Restraints:

-

Data Confidentiality Risks and Regulatory Complexities Hamper Market Growth

Despite strong growth potential, the laboratory products and services outsourcing market is met with significant restraints, such as concerns related to the confidentiality of data, stringent regulatory requirements, and varying quality standards between service providers. Pharma and biotech firms are frequently reluctant to outsource laboratory products and services outsourcing market share, and their product research data to third-party labs because of IP vulnerabilities or cybersecurity attacks. In a Deloitte 2023 study, more than 52% of life sciences CEOs stated that data integrity and compliance risk were their primary challenge in outsourcing. In addition, a mix of regulations (FDA 21 CFR Part 11, EU GMP Annex 11, and ISO 17025) presents a hurdle to global outsourcing management. These intricacies of practice undermine smooth working relationships and generate compliance burdens, particularly in multi-site research. The availability of well-qualified contract labs for emerging markets is also one of the impediments to the scalability from the supply side.

Common regulatory approval time lags and disparate accreditation standards in various geographies contribute to lengthy project periods, which affect client satisfaction and service delivery. These are the factors that are restraining the growth of the laboratory products and services outsourcing market and they require a well- structured plan to overcome these barriers, which includes strong vendor audits, data security enhancement, and the harmonization of global standards to foster laboratory products and services outsourcing market analysis and confidence in outsourcing business.

Segmentation Analysis:

By Type

Product is the largest segment of the global laboratory products and services outsourcing market in 2024, with a revenue share of over 62.41%. This predominance is mainly on account of the growing requirement for superior quality laboratory consumables, instruments, and diagnostic kits in R&D and the routine testing process. An increasing number of clinical trials, in combination with strict quality requirements, have increased the demand for standardized products, thereby increasing dependence on third-party suppliers.

Among the modes of operation, services are expected to register the highest growth owing to increasing adoption of outsourcing of complex analytical tasks, regulatory compliance, and quality assurance, which help suppliers and manufacturers, pharmaceutical and biotech companies, to focus on more complex drug development activities and reduce their operating expenditure.

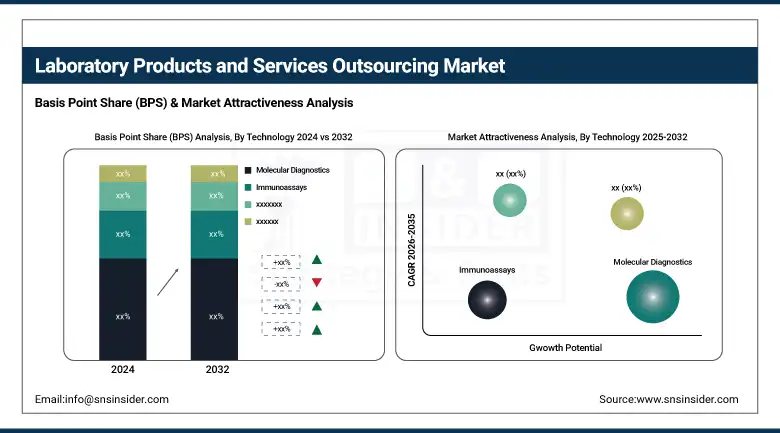

By Technology

The market size of molecular diagnostics was the largest in 2024, owing to its indispensable position in the areas of precision medicine, infectious disease testing, and oncology diagnostics. The growing use of PCR and next-generation sequencing (NGS) platforms has further expanded its applicability in clinical and research laboratories.

In contrast, immunoassays were identified as the fastest growing market segment, attributed to their higher sensitivity, potential for automation, and use in biomarker testing and infectious disease diagnostics, particularly after the pandemic.

By End-Use

Pharmaceutical and biotech companies dominated the global laboratory products and services outsourcing market in 2024, due to extensive R&D pipelines and the ongoing requirement for specialized testing, regulatory submissions, and commercialization assistance. This segment is supported by strong outsourcing levels in discovery, preclinical, and clinical stages.

At the same time, medical device companies as the fastest growing end-user segment, driven by increasing complexity of device design, software and diagnostics integration, and the growing need for outsourced testing to enter the market via regulatory approvals, including FDA and EU MDR approval.

Regional Analysis:

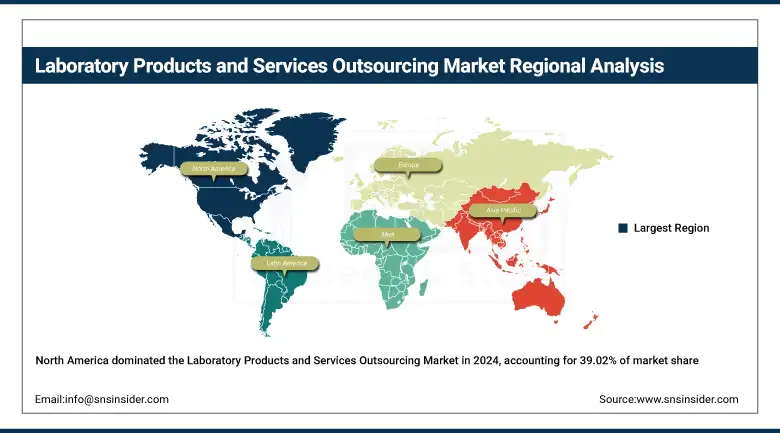

North America held the largest share of the laboratory products and services outsourcing market, followed by 39.02% 2024, owing to its well-established pharmaceutical & biotechnology industry, strong adoption of clinical trials, and a considerable R&D expenditure. Leading the region is the U.S., supported by the highest number of clinical trials underway globally and federal R&D investment of over USD 170 billion in 2023. The growing number of FDA regulations on laboratory and safety requirements has stimulated companies to outsource laboratory operations to meet these mandates. Canada is also rising on the radar, due to government funding that is supporting biopharma R&D and widening CROs’ network. The region's dominance is also maintained with growing relationships between the U.S. pharma companies and dedicated lab service providers.

Get Customized Report as per Your Business Requirement - Enquiry Now

The outsourcing market for laboratory products and services in Europe is the second fastest-growing region, due to the aging population, pipeline changes, and increasing adoption of outsourcing to comply with EU regulations. Germany is in the lead as the region boasts of strong pharmaceutical manufacturing base and intensive R&D spending, where more than 1,100 companies are involved in drug development. The U.K. is a major player too, not least due to its burgeoning biotech industry and its rising number of public-private partnerships in clinical research. The growing need for affordable and niche testing systems and investments in lab automation continues to drive growth in Western and Eastern Europe.

Asia Pacific is the fastest-growing market for laboratory products and services outsourcing market owing to low cost of the tests, large patient base, and rising healthcare infrastructure investments. China is the dominant player in the region, backed by government incentives to facilitate clinical trials and outsourcing projects, and over 800 CRO providers conducting business in the nation. India is also experiencing a fast increase in the medical R&D market, owing to low operating costs, skilled labor, and increasing support from the government for medical R&D, such as the "Make in India" campaign. Japan strongly contributes, especially in molecular diagnostics and clinical chemistry, on the back of its robust technology and growing elderly population. Regulatory harmonization and increasing biotech startup activity add to the region’s momentum.

Key Players:

Leading laboratory products and services outsourcing companies in the market comprise Thermo Fisher Scientific, Charles River Laboratories, Eurofins Scientific, Labcorp, Quest Diagnostics, Parexel International, Agilent Technologies, PerkinElmer, Bio-Rad Laboratories, SGS SA, Intertek Group plc, and WuXi AppTec.

Recent Developments:

In May 2025, Thermo Fisher Scientific unveiled its advanced spectral flow cytometer, targeting the high-value biopharma and omics markets, part of a broader USD 2 billion investment in the U.S. manufacturing and internal R&D (which reached USD 1.39 billion in 2024).

In May 2025, Charles River Laboratories announced a major board restructuring, adding four new independent directors and launching a comprehensive strategic review under activist investor Elliott, which propelled its stock up ~15–16% in a single day.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 41.85 billion |

| Market Size by 2032 | USD 78.67 billion |

| CAGR | CAGR of 8.22% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Products (Equipment (General, Analytical, Clinical, Support, and Specialty), Disposables, and Others), Services, (Pharmaceutical, (Bioanalytical Testing, (ADME, PK, PD, Bioavailability, Bioequivalence, and Others), Method Development & Validation (Extractable & Leachable, Impurity Method, Technical Consulting, and Others), Stability Testing (Drug Substance, Stability Indicating Method Validation, Accelerated Stability Testing, Photostability Testing, and Others), Others), Medical Device (Biocompatibility Tests, Chemistry Test, Microbiology & Sterility Testing, and Others) • By Technology (Immunoassays, Molecular Diagnostics, Microbiology, Clinical Chemistry, Flow Cytometry, Mass Spectroscopy, Chromatography, and Others) • By End Use (Pharmaceutical & Biotech Companies, Medical Device Companies, CRO & CDMO, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific, Charles River Laboratories, Eurofins Scientific, Labcorp, Quest Diagnostics, Parexel International, Agilent Technologies, PerkinElmer, Bio-Rad Laboratories, SGS SA, Intertek Group plc, and WuXi AppTec |

Frequently Asked Questions

Future trends include growing adoption of digital lab automation, AI integration, and increased outsourcing of high-complexity testing like molecular diagnostics and precision medicine.

North America leads due to advanced research infrastructure, followed by Europe and Asia Pacific, which are rapidly expanding with cost-effective outsourcing hubs.

Major players include Thermo Fisher Scientific, Charles River Laboratories, Eurofins Scientific, Labcorp, Quest Diagnostics, and WuXi AppTec.

Rising R&D spending, increasing demand for cost-efficient testing, and the need for regulatory compliance are key drivers fueling market growth.

The laboratory products and services outsourcing market size was valued at USD 41.85 billion in 2024 and is expected to reach USD 78.67 billion by 2032, growing at a CAGR of 8.22% over 2025-2032.

Get in Touch