Brain Implants Market Report Scope & Overview:

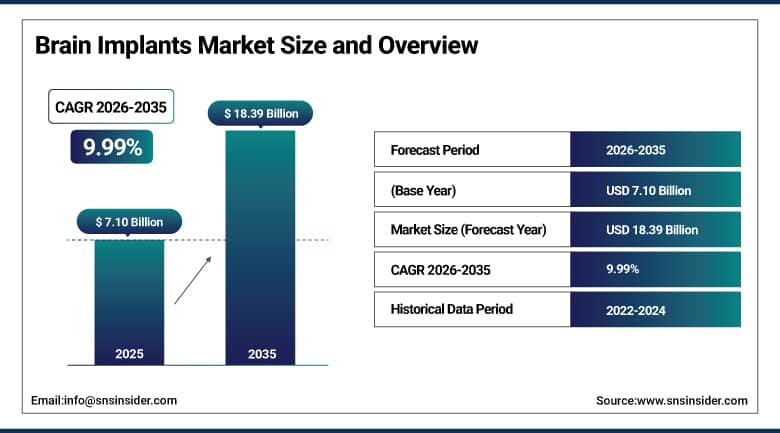

The Brain Implants Market was valued at USD 7.10 Billion in 2025 and is expected to reach USD 18.39 Billion by 2035, growing at a CAGR of 9.99% from 2026 to 2035.

The global brain implants market is experiencing significant and sustained growth driven by advancements in neurotechnology, a rising prevalence of neurological disorders, and expanding clinical acceptance of implantable neuromodulation as a therapeutic alternative to pharmaceutical management. Brain implants, also referred to as neural implants or neuroprosthetics, are electronic devices that are surgically implanted in the brain or adjacent neural structures to diagnose, monitor, and treat various neurological conditions by interfacing directly with the brain's neural circuits.

With applications ranging from epilepsy management and Parkinson's disease treatment to cognitive enhancement, chronic pain relief, and emerging brain-computer interface applications, brain implants offer promising therapeutic options for conditions where pharmacological alternatives provide inadequate symptom control. More than 10 million individuals worldwide are affected by Parkinson's disease and approximately 50 million people live with epilepsy according to the WHO, creating a large and growing addressable patient population for implantable neurostimulation therapy.

In January 2025, Elon Musk announced the implantation of a Neuralink brain-computer interface device in a third human patient, featuring more electrodes, higher bandwidth data transmission, and longer battery life compared to previous Neuralink implants.

Brain Implants Market Size and Forecast:

-

Market Size in 2026E: USD 7.81 Billion

-

Market Size by 2035: USD 18.39 Billion

-

CAGR: 9.99% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Brain Implants Market - Request Free Sample Report

Brain Implants Market Trends:

-

Closed-loop stimulation systems are improving treatment outcomes through real-time adjustment of neural stimulation based on brain activity.

-

Rechargeable and wireless charging technologies are extending implant lifespan and reducing replacement surgeries.

-

Brain-computer interface (BCI) innovations are expanding applications beyond therapy into direct neural-digital communication.

-

MRI-compatible implant designs are increasing patient eligibility by enabling safe post-implant imaging procedures.

-

Minimally invasive implantation techniques are reducing surgical risks and supporting wider adoption of brain implant procedures.

U.S. Brain Implants Market Outlook:

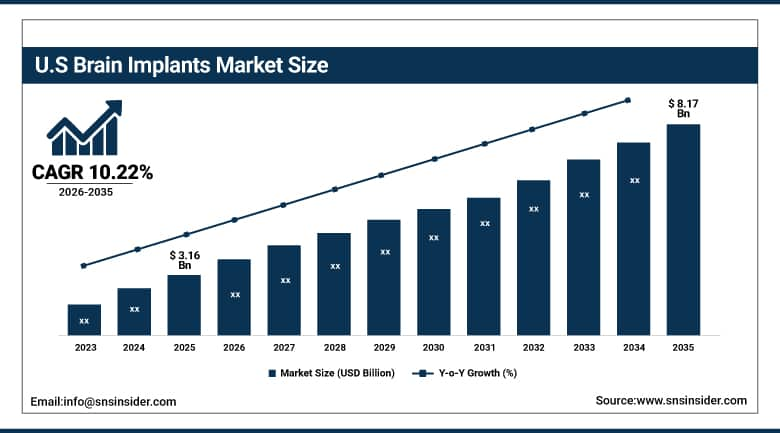

The U.S. Brain Implants Market was valued at approximately USD 3.16 Billion in 2025 and is expected to reach approximately USD 8.17 Billion by 2035, growing at a CAGR of approximately 10.22%.

The U.S. market is the most significant commercial brain implants market in the world owing to its North American regional dominance. Medtronic’s Activa and Percept DBS systems, Abbott’s Infinity DBS systems, Boston Scientific’s Vercise Genus systems, and LivaNova’s VNS Therapy systems are all the players which create the commercial market environment domestically. The approval of DBS for indications such as obsessive-compulsive disorder, treatment-resistant depression, and epilepsy along with the existing indications like Parkinson’s disease and essential tremors through progressive approvals by the FDA becomes the regulatory base for adoption.

The presence of academic medical centers that have experience of implanting brain implants in Boston, Cleveland, San Francisco, and New York builds the referral infrastructure responsible for higher implant volumes. The annual NIH funding for neuroscience disorders research of more than USD 3 billion makes the discovery process for brain implants viable.

In 2024, Medtronic received FDA clearance for Percept RC, a recharge-enabled deep brain stimulation system with integrated brain sensing capability that enables closed-loop adaptive stimulation based on real-time local field potential signals from the implanted electrode.

Brain Implants Market Segment Analysis:

-

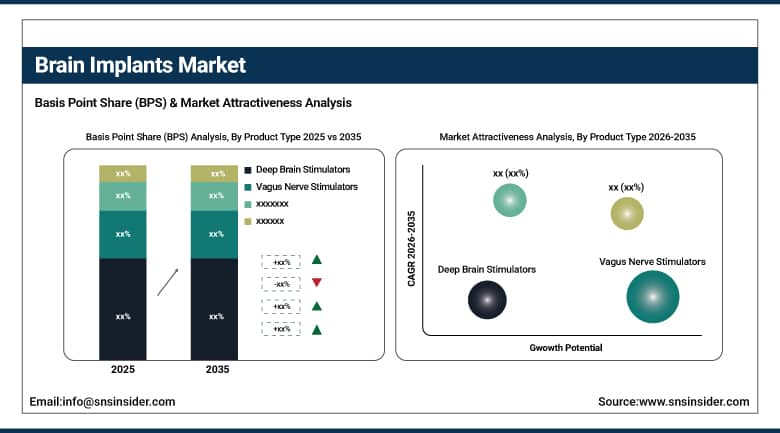

By Product Type, the Deep Brain Stimulators segment dominated the brain implants market with approximately 37.6% share in 2025, while the Vagus Nerve Stimulators segment is the fastest growing at the highest CAGR.

-

By Application, the Parkinson's Disease segment dominated the brain implants market with approximately 34.3% share in 2025, while the Alzheimer's Disease segment is the fastest growing.

-

By End User, the Hospitals segment dominated the brain implants market with the largest revenue share in 2025, while the Specialty Clinics and Neurological Centers segment is the fastest growing.

By Product Type, deep brain stimulators dominate, vagus nerve stimulators grow fastest

DBS accounted for about 37.6% of the brain implant market share in 2025. The main factor behind the commercial success of DBS is that it is the most tested brain implant treatment available with FDA approval for decades in conditions like Parkinson's disease, essential tremors, and dystonia, thus offering the framework of neurosurgical expertise, reimbursement policies, and recognition by patients leading to superior commercial success.

Vagus nerve stimulators constitute the fastest growing segment on the grounds of expansion in the number of indications due to the clinical evidence in cases of VNS in epilepsy, treatment-resistant depression, stroke rehabilitation, and rheumatoid arthritis.

By Application, Parkinson's disease dominates, Alzheimer's grows fastest

The Parkinson's disease application was the leading application with about 34.3% of brain implant market in 2025. The dominance of the Parkinson's disease application due to its commercial supremacy can be explained by the outstanding efficiency of deep brain stimulation as a method of treatment of movement disorders associated with Parkinson's disease, high prevalence of about 10 million people suffering from Parkinson's disease around the world that is the aged patient base providing steady increase in the number of patients, and extensive referring network of neurologists and movement disorder specialists to neurosurgical DBS centers.

Alzheimer's disease application is the fastest growing application for brain implants because of the outstanding progress made by the development of methods of treatment of Alzheimer's disease, especially after FDA approval of drugs aimed at amyloid deposits treatment that leads to the situation when brain stimulation therapy is studied as a complimentary method of treatment on the circuit level. Fornix, entorhinal cortex, and nucleus basalis of Meynert targeting to improve the memory circuit and responsive neurostimulation therapy are investigated in clinical trials and provide the grounds for further researches that will make Alzheimer's disease application the most commercially attractive next application.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Brain Implants Market Insights

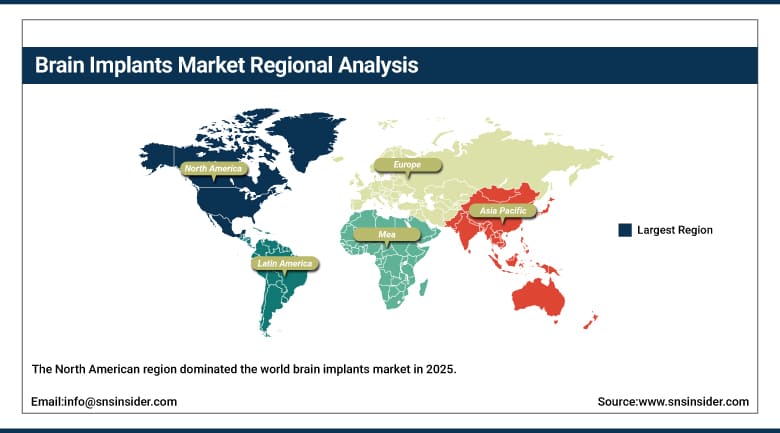

The North American region dominated the world brain implants market in 2025 because of high incidence of neurological disorders, advanced healthcare infrastructure, positive reimbursement environment for neurostimulation procedures, and presence of Medtronic, Abbott, Boston Scientific, and LivaNova firms. The US has accounted for around 87.4% of North America revenues due to its academic neurosurgery centers, FDA approved DBS indications, and NIH funds for neuroscience research.

Canada has contributed around 12.6% to the North America revenues due to its universal health coverage of DBS procedure in Parkinson's disease and essential tremor, implantation program at academic medical centers, and increasing knowledge about neuromodulation among Canadian neurologists treating movement disorders.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Brain Implants Market Insights

The European brain implants market is technologically advanced since there exists CE marking approvals for the use of medical devices, highly technologically advanced neuroscience research centers located at Charité Berlin, UCL Queen Square, and Pitié-Salpêtrière Paris, as well as universal health insurance coverage of DBS treatments. Germany accounts for around 22.3% of Europe's market share through its neurosurgery centers, presence of Medtronic and Abbott within its domestic market, as well as the application of DBS therapy through the DGN guidelines for movement disorders.

Other secondary brain implant markets include the UK, France, and Italy through their provision of DBS treatments for Parkinson's disease and dystonia through NHS and positive technology appraisals for neuromodulation treatments by NICE and an active AMC network.

Asia Pacific Brain Implants Market Insights

The Asia Pacific is considered the dominant brain implants market due to the presence of a number of driving forces such as neurological disorders rising in China, neurosurgical facilities being advanced in China, an increased number of movement disorder specialists in India, advanced neuromodulation procedures performed in Japan, high level of technology used in medical devices in South Korea, and rising coverage for neurological disorder treatments in the region. The China market accounts for 44.8% of the Asia Pacific revenues due to the huge Parkinson's patient population in China, which is estimated at 2.9 million people, investments in healthcare infrastructure, and advanced DBS procedures in Chinese neurosurgery centers.

The India market is considered the most commercial emerging market in the Asia Pacific region due to the increased number of movement disorder specialists, growing number of private neuroscience hospitals in metropolitan areas, and rising patient awareness on DBS as the Parkinson's disease treatment procedure.

MEA & Latin America Brain Implants Market Insights

The market lead in terms of revenue in the MEA region is held by Saudi Arabia with 31.2%, based on advanced tertiary neuroscience hospitals, healthcare investments under the Vision 2030 strategy towards advanced treatment technologies, and expansion of Deep Brain Stimulation (DBS) treatment in King Faisal Specialist Hospital and other prominent Saudi hospitals. Cleveland Clinic Abu Dhabi and Mediclinic City Hospital from UAE also add their share to the market revenues in the Gulf region. Brazil leads in the Latin American region with a 44.2% revenue share because of the high prevalence of Parkinson's disease and the DBS program at the academic neurosurgical center of USP and UNIFESP.

Market Dynamics:

Growth Drivers: Rising neurological disorder prevalence and closed-loop neuromodulation technology creating superior therapeutic outcomes

The rise in the global prevalence of neurological conditions is the main structurally-driven driver of growth in the market of brain implants. The WHO numbers concerning the number of neurological conditions that exceeds 1 billion worldwide, the number of Parkinson’s disease sufferers that exceeds 10 million according to Parkinson’s Foundation and the number of epileptic patients that reaches 50 million according to the International League Against Epilepsy together present an enormous target population of patients who can be treated with the help of brain implants.

The development of closed-loop adaptive neurostimulation systems is the major technologically-driven advance in the market of brain implants since its integration of neural signal sensing with parameter adjustment makes its clinical performance superior to that of open-loop stimulation systems. The FDA approval of Medtronic’s Percept RC and Abbott's Infinity BrainSense System demonstrate the opportunity of applying the advantages of closed-loop systems in practice and mark the start of the upgrade cycle of technology, pushing the requirements of high-end system specifications.

Restraints: High device and surgical costs limiting access and the requirements for specialized neurosurgical expertise

High costs related to the cost of implantable device required for the DBS procedure ranging from USD 20,000 to USD 50,000 together with the surgical cost ranging from USD 30,000 to USD 100,000 creates economic and healthcare barriers that preclude procedure access in cases where the procedure has no coverage. Each patient eligible for the DBS treatment, but has not undergone the procedure due to the absence of adequate coverage or financial capacity becomes an opportunity that requires changes in reimbursement strategy.

The demand for the specialized neurosurgical skill needed for conducting the DBS procedure becomes the main barrier limiting the accessibility of DBS in the majority of markets other than the tertiary neuroscience centers. Each hospital with the capability of DBS through training of the neurosurgeon represents an increase in the commercial market size.

Opportunities: Brain-computer interface commercialization and psychiatric indication expansion

Commercialization of BCI technology provides the greatest longer-term transformational market expansion opportunity due to its direct neural-digital interface capability, and the motor restoration for paralysis and eventual cognitive enhancement capabilities that would provide BCI market segments potentially orders of magnitude greater than those seen today with therapeutic neurostimulation applications. The combined efforts of Neuralink's three-patient clinical trial program, Synchron's Stentrode commercialization plan, and the academic research efforts of BrainGate provide insight into the path acceleration will take to bring near-term BCI market opportunities outside of today's research environment.

Extension into conditions like treatment-resistant depression, obsessive-compulsive disorder, and PTSD provides the most compelling near-term application growth opportunity in terms of numbers of patients suffering from an unmet condition exceeding the movement disorder market segment. Each FDA approval of deep brain stimulation for a psychiatric condition represents a new market opportunity whose volume of procedures, assuming physician acceptance and patient satisfaction follows clinical evidence, provides great potential within the brain implant market.

Recent Developments:

-

2025: Elon Musk announced the implantation of a Neuralink brain-computer interface in a third human patient in January 2025, featuring more electrodes, higher bandwidth, and longer battery life, demonstrating the commercial progression of BCI technology toward broader clinical application.

-

2024: Medtronic received FDA clearance for the Percept RC recharge-enabled deep brain stimulation system in 2024, incorporating integrated brain sensing capability for closed-loop adaptive stimulation based on real-time local field potential signals from implanted DBS electrodes.

-

2024: Abbott received CE Mark expansion for its Infinity DBS system in 2024 with enhanced BrainSense technology enabling directional closed-loop stimulation based on biomarker-guided parameter adjustment for improved Parkinson's disease symptom management.

Brain Implants Market Key Players:

-

Medtronic plc

-

Abbott Laboratories (St. Jude Medical)

-

Boston Scientific Corporation

-

LivaNova plc

-

NeuroPace Inc.

-

Nalu Medical Inc.

-

Synchron Inc.

-

Neuralink Corporation

-

BioElectronics Corporation

-

Renishaw plc

-

Aleva Neurotherapeutics SA

-

Saluda Medical Pty Ltd.

-

Second Sight Medical Products Inc.

-

Medtronic BioMonitor III

-

Sensata Technologies

-

Soterix Medical Inc.

-

Nexim Inc.

-

Inivio AS

-

Battelle Memorial Institute

-

Kernel Co.

Brain Implants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.10 Billion |

| Market Size by 2035 | USD 18.39 Billion |

| CAGR | CAGR of 9.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Deep Brain Stimulators, Vagus Nerve Stimulators, Responsive Neurostimulation Systems) • By Application (Parkinson's Disease, Epilepsy, Alzheimer's Disease, Essential Tremor, Chronic Pain, Depression/OCD, Schizophrenia, Others) • End User (Hospitals, Specialty Clinics and Neurological Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic plc, Abbott Laboratories (St. Jude Medical), Boston Scientific Corporation, LivaNova plc, NeuroPace Inc., Nalu Medical Inc., Synchron Inc., Neuralink Corporation, BioElectronics Corporation, Renishaw plc, Aleva Neurotherapeutics SA, Saluda Medical Pty Ltd., Second Sight Medical Products Inc., Medtronic BioMonitor III, Sensata Technologies, Soterix Medical Inc., Nexim Inc., Inivio AS, Battelle Memorial Institute, and Kernel Co. |

Frequently Asked Questions

The Brain Implants Market is expected to grow at a CAGR of 9.99% from 2026 to 2035.

The Brain Implants Market was valued at USD 7.10 Billion in 2025.

Rising global prevalence of neurological disorders including Parkinson's disease affecting more than 10 million and epilepsy affecting approximately 50 million people worldwide creating structured neuromodulation therapy demand, and closed-loop adaptive stimulation technology demonstrating objectively superior therapeutic outcomes that create a commercial technology upgrade cycle above conventional open-loop system.

Deep Brain Stimulators dominated the Brain Implants Market with approximately 37.6% share in 2025.

North America dominated the Brain Implants Market in 2025.

Get in Touch