Broadband Services Market Report Scope & Overview:

This report provides a detailed analysis of broadband service trends across key connection technologies and regions.

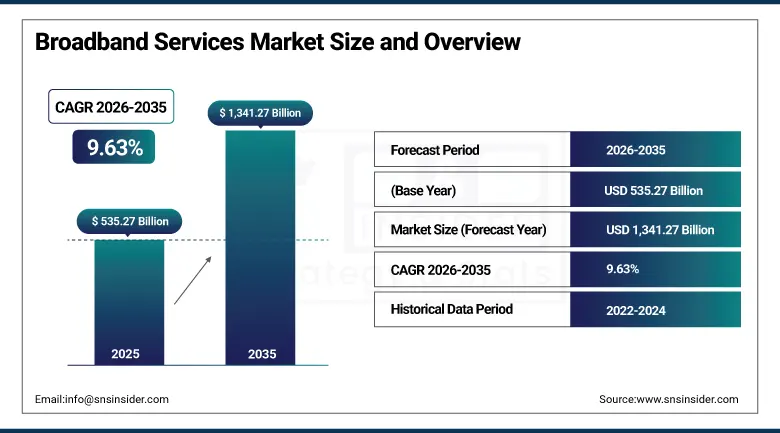

The Broadband Services Market size was USD 535.27 Billion in 2025 and is expected to reach USD 1,341.27 Billion by 2035, growing at a CAGR of 9.63% from 2026–2035.

Broadband services provide high-speed Internet connections to homes and businesses around the world. As reliance on streaming, remote work and digital collaboration tools continues to increase, demand continues to grow. Adoption of high-speed broadband continues to grow steadily in both the residential and commercial sectors. The deployment of fibre and building out of network infrastructure is accelerating in developing economies. Growth in fixed wireless access subscribers is strong in both urban and rural areas. These networks provide flexible, low cost broadband alternatives to traditional cabled infrastructure. Everywhere broadband penetration is increasing and average connection speeds are rising. The rising demand for bandwidth-hungry applications is pushing providers towards faster network technologies. Service providers are layering on value-added services such as security and entertainment bundles on top of core connectivity.

Frontier Communications announced that it was planning to buy Verizon for about USD 20 billion. The deal is seen as a boost to Verizon’s fibre broadband services and a substantial expansion of its market footprint. The acquisition is another example of the wider consolidation reshaping the broadband services industry. Larger carriers are buying smaller fiber-focused providers to quickly expand their network reach. Such consolidation driven by scale should continue to change competitive dynamics across the broadband industry. Regulators in different markets are still reviewing such deals for competitive impact before approving them.

Market Size and Forecast

-

Market Size in 2026E: USD 586.71 Billion

-

Market Size by 2035: USD 1341.27 Billion

-

CAGR: 9.63% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Broadband Services Market - Request Free Sample Report

Broadband Services Market Trends

-

Fiber optic network deployment keeps expanding rapidly across both developed and developing economies.

-

Fixed wireless access adoption is growing significantly across urban and rural areas alike.

-

Rising bandwidth-intensive application use is pushing average household connection speeds higher.

-

5G-based fixed wireless access is emerging as a cost-effective alternative to cabled infrastructure.

-

Government rural broadband programs are expanding internet access across underserved communities.

-

Telecom industry consolidation through mergers and acquisitions is reshaping competitive market structure.

-

Bundled service offerings combining internet, TV, and mobile plans continue gaining customer popularity.

The U.S. Broadband Services Market Outlook

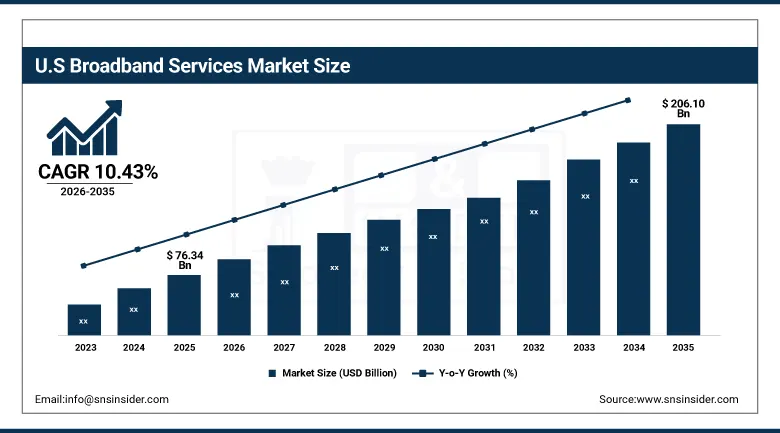

The U.S. Broadband Services Market was valued at approximately USD 76.34 Billion in 2025. It is expected to reach approximately USD 206.10 Billion by 2035. The market is growing at a CAGR of approximately 10.43%.

U.S. growth is driven by streaming, online gaming and remote work, with a growing need for high-speed internet. The continued expansion of fiber-optic technology and the rollout of 5G-based fixed wireless access are improving connectivity and reliability. Government programmes are increasing access in underserved areas, including efforts to deploy rural broadband. This blend of technology adoption and policy support continues to drive overall U.S. market penetration. Major carriers continue to make heavy investments in next generation network infrastructure around the country. “There’s competition between fibre, cable and wireless providers that pushes service quality and speeds ever higher across the country.

Charter Communications has agreed to acquire Liberty Broadband in a stock deal. The deal also cements Charter’s position in the broader U.S. broadband space. Consolidation activity such as this is a sign of greater competition for scale in fibre and cable networks. Bigger combined companies can negotiate better terms with key suppliers for content and equipment. This trend towards industry consolidation is expected to continue to change the competitive landscape in the future. The consolidation continues and smaller regional players could become increasingly acquisition targets.

Broadband Services Market Segment Analysis

-

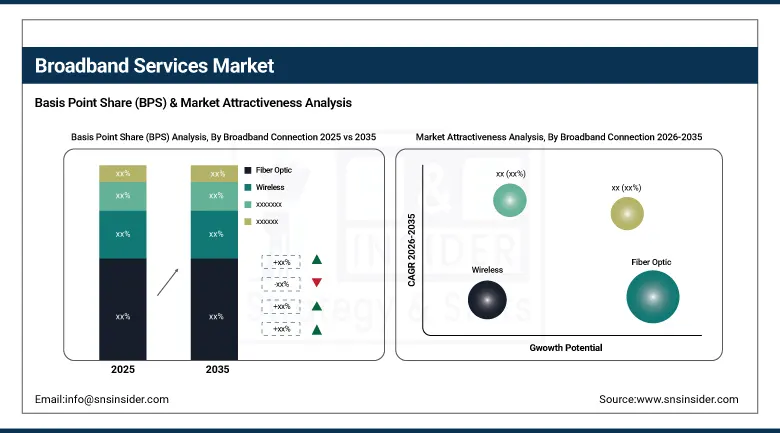

By Broadband Connection, fiber optic segment dominated the broadband services market with approximately 38% share in 2025. The wireless segment is growing fastest.

-

By End-Use, the business segment dominated the broadband services market in 2025. The household segment is growing fastest.

-

By Subscription Type, the monthly subscription segment dominated the broadband services market in 2025, accounting for approximately 68.5% of total market revenue, while annual subscription segment is projected to be the fastest-growing during 2026–2035, expanding at a CAGR of approximately 8.9%.

By Broadband Connection, fiber optic dominates, wireless grows fastest

In the broadband connection category, fibre optic led in 2025 with a share of around 38%. Fibre gives high quality network signals that go straight from the operator’s equipment to the end users. These networks are considered future-proof, readily incorporating new technologies as they are developed to increase bandwidth. Businesses and homes can increase their usage without having to build brand new networks. The combination of quality and scalability continues to make fibre optic the leading type of connection. The top priority for telecom operators is fibre buildout because it is cheaper in the long run than doing repeated upgrades. But wireless broadband is a real competitive threat to fiber’s continued dominance.

Wireless broadband is the fastest growing type of connection. This growth is driven by the technological advancement and user friendly nature of wireless platforms. Wireless service uses radio waves, rather than physical cables to connect as other types of connections do. Demand is being driven by the evolution of mobile wireless technology from 3G to 4G and now emerging 5G. The fast adoption of this connection type is increased by the increasing diversity of applications across society. As 5G deployment continues to expand around the world, wireless broadband growth should continue to accelerate.

By End-Use, business dominates, household grows fastest

Business end-use led this category in 2025, supported by rising reliance on high-speed internet. Companies increasingly depend on broadband for cloud services, video conferencing, and digital collaboration tools. Businesses are seeking out fiber-optic and high-data broadband solutions for seamless task execution. Work-from-home and hybrid work models continue reinforcing this business-focused demand pattern. This combination of operational dependency keeps business end-use as the leading category. Enterprise customers also tend to pay premium rates for guaranteed uptime and dedicated support. As digital collaboration tools keep proliferating, business broadband demand should remain consistently strong.

Household broadband is growing the fastest among end-use categories. Rising demand for streaming services, online education, gaming, and smart home applications drives this growth. The shift toward work-from-home and online learning has intensified demand for low-latency home bandwidth. Fixed wireless access and fiber-optic broadband are emerging as strong options, especially across suburbs and rural areas. Multi-device households increasingly require higher bandwidth tiers to support simultaneous usage. As home-based digital activity keeps expanding, household broadband demand should keep climbing rapidly.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Broadband Services Market Insights

North America continues to grow with the support of government initiatives aimed at reducing unserved and underserved areas. In Canada, there has been investment in high-speed internet infrastructure due to the demand for remote work and e-learning tools. 5G and other next generation technologies are still a key focus for the region, leading to increased broadband coverage. Major carriers are racing to expand fibre footprint in both urban and rural markets. Public-private infrastructure partnerships are also speeding up network buildout timelines in a number of states.

The United States accounts for about 82.5% of North American revenue. We continue to enhance regional connectivity and reliability through widespread adoption of fiber-optic and 5G fixed wireless. Government rural broadband programmes continue to deliver access to underserved American communities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Broadband Services Market Insights

Europe held a significant market share in 2025, supported by mature telecommunications infrastructure. Germany, France, and the UK continue investing in next-generation fiber and 5G network expansion. Regulatory harmonization across the EU continues supporting consistent broadband service quality standards. Open-access fiber network models are also gaining traction across several European markets. The European Commission's Digital Decade targets continue pushing member states toward gigabit connectivity goals.

Germany accounts for approximately 24.6% of European revenue. Strong fixed and mobile broadband competition keeps driving continued network investment across the region. This competitive dynamic should keep supporting steady European market growth.

Asia Pacific Broadband Services Market Insights

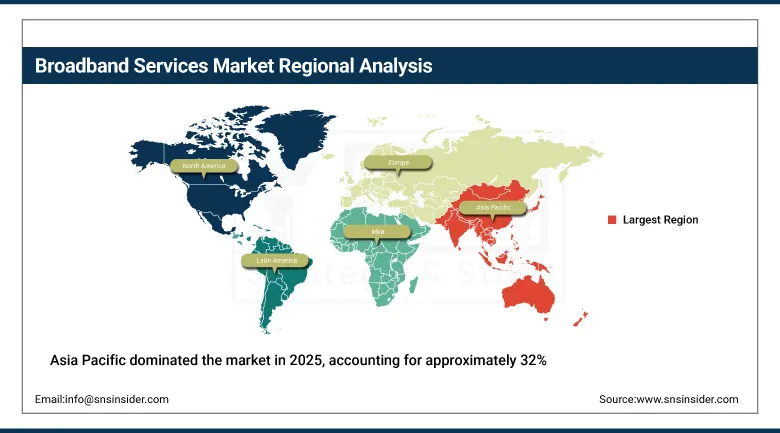

Asia Pacific dominated the market in 2025, accounting for approximately 32% of global revenue. A large user base and rapid emergence of new technologies both support this regional leadership. Government initiatives across the region continue actively promoting broadband infrastructure expansion.

China accounts for approximately 40.6% of Asia Pacific revenue. Ultra-fast broadband adoption across China and Japan keeps leading global usage rate growth. This combination of scale and technology adoption should sustain Asia Pacific's leading position.

MEA & Latin America Broadband Services Market Insights

The UAE leads MEA revenue, growing broadband infrastructure investment and rising digital adoption both support this position. Saudi Arabia is also expanding its national fiber and 5G network coverage. Government-led digital economy initiatives across the Gulf region continue reinforcing this momentum. South Africa leads broadband expansion across Sub-Saharan Africa through expanding fiber and mobile network investment.

Brazil leads Latin American revenue, expanding broadband access and rising digital adoption both drive this regional lead. Mexico and Argentina contribute secondary demand through their own expanding telecommunications infrastructure.

Market Dynamics

Growth Drivers: Rising streaming, remote work, and IoT usage driving broadband adoption

The key driver of growth is the increasing adoption of digital platforms for streaming, e-learning, remote work and gaming. We extend fibre optic network reach, and pair it with 5G fixed wireless access, to deliver ultra-fast, low-latency connectivity. This mix is leading to a better overall user experience for residential and business users alike. The increasing integration of smart home and Internet of Things devices further drives demand for high-quality broadband. Streaming services, in particular, continue to drive the incremental increase in the average bandwidth needed by households each year. Cloud gaming services are also becoming a significant new source of bandwidth demand.

The market is primarily driven by the increasing adoption of advanced broadband services in rural and underserved areas. This trend is being accelerated by government efforts to close the digital divide, especially in developed countries. This driver is likely to remain strong over the forecast period as the use of digital platforms continues to increase across the globe. International development agencies are also funding broadband expansion projects in less-developed countries.

Restraints: Expensive rural network installation hampering broadband expansion

Deploying broadband networks, especially fiber-optic and 5G infrastructure, to remote areas is expensive. Smaller market participants are often deterred by the large capital expenditure required for cable installation and infrastructure upgrades. Add on more ongoing cost burden to maintain network quality across sparsely populated areas. Right-of-way permits and local regulatory approvals can also extend the time it takes to build out a network.

These retail cost pressures can slow the rate at which low-density network expansion occurs. Affordability constraints among certain demographics may also restrict high-speed broadband uptake in fast-scaling economies. These combined cost factors continue limiting faster broadband expansion across the most remote regions. Subsidy programs in several countries are attempting to offset these affordability barriers directly.

Opportunities: Fixed wireless access offering cost-effective, scalable rural connectivity

The boom in 5G-based fixed wireless access technology represents a significant market opportunity. FWA provides high-speed 4G and 5G-style internet access without requiring extensive upfront cabled infrastructure investment. This makes FWA particularly well suited for rural and underserved service areas specifically. Operators can deploy FWA considerably faster than traditional fiber rollout in many target markets.

FWA network scalability, lower deployment costs, and flexibility enable more efficient telecom customer base expansion. Government demands for rural broadband coverage should help accelerate FWA adoption further. As rural connectivity initiatives keep expanding globally, this opportunity should keep growing through the forecast period.

Recent Developments:

-

2024: Verizon announced plans to acquire Frontier Communications for approximately USD 20 billion, aiming to enhance its fiber broadband services and market presence.

-

2024: Charter Communications agreed to acquire Liberty Broadband in an all-stock transaction, consolidating its position in the broadband market.

-

2024: Liberty Global completed the spin-off of its Swiss business, Sunrise Communications, into a separate publicly traded company.

Broadband Services Market Key Players are:

-

AT&T Inc.

-

Verizon Communications Inc.

-

Comcast Corporation

-

Charter Communications Inc.

-

CenturyLink (Lumen Technologies)

-

T-Mobile US, Inc.

-

Cox Communications

-

Frontier Communications

-

British Telecommunications (BT Group)

-

Vodafone Group

-

Orange S.A.

-

Deutsche Telekom AG

-

Telefónica S.A.

-

Nippon Telegraph and Telephone Corporation (NTT)

-

Rakuten Group, Inc.

-

China Telecom Corporation

-

Bharti Airtel Limited

-

América Móvil S.A.B. de C.V.

-

Telecom Italia S.p.A.

-

Viasat, Inc.

Broadband Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 535.27 Billion |

| Market Size by 2035 | USD 1,341.27 Billion |

| CAGR | CAGR of 9.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Broadband Connection (Fiber Optic, Wireless, Satellite, Cable, Digital Subscriber Line) • By Subscription Type (Monthly, Annual, Others) • By End-Use (Business, Household, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AT&T Inc., Verizon Communications Inc., Comcast Corporation, Charter Communications Inc., CenturyLink (Lumen Technologies), T-Mobile US, Inc., Cox Communications, Frontier Communications, British Telecommunications (BT Group), Vodafone Group, Orange S.A., Deutsche Telekom AG, Telefónica S.A., Nippon Telegraph and Telephone Corporation (NTT), Rakuten Group, Inc., China Telecom Corporation, Bharti Airtel Limited, América Móvil S.A.B. de C.V., Telecom Italia S.p.A., and Viasat, Inc. |

Frequently Asked Questions

The Broadband Services Market is expected to grow at a CAGR of 9.63% from 2026 to 2035.

The Broadband Services Market was valued at USD 535.27 Billion in 2025.

Rising streaming, remote work, and IoT adoption, along with expanding fiber and 5G fixed wireless infrastructure, are the primary growth factors. Government-led rural broadband programs are also playing a meaningful supporting role.

The Fiber Optic segment dominated the Broadband Services Market with approximately 38% share in 2025.

Asia Pacific dominated the Broadband Services Market with approximately 32% revenue share in 2025.

Get in Touch