Butane Market Report Scope & Overview:

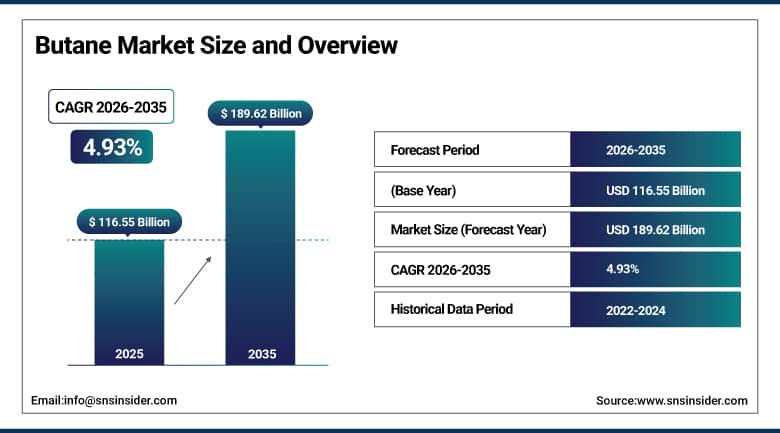

The Butane Market was valued at USD 116.55 Billion in 2025 and is expected to reach USD 189.62 Billion by 2035, growing at a CAGR of 4.93% from 2026 to 2035.

The global butane market is seeing strong momentum owing to high global demand in residential, commercial, and industrial uses, especially in liquefied petroleum gas manufacturing, petrochemical raw material usage, and refrigeration. Butane is an odorless, flammable, and easily liquefied light hydrocarbon represented chemically as C4H10. It exists commercially in two isomeric forms: the straight-chain form known as n-butane and the branched-chain form referred to as isobutane. The isomers of butane are obtained in the processes of natural gas and crude oil refining for different commercial uses including fuel, petrochemicals, aerosols, and refrigerants. The important determinants of the market growth are growing energy consumption, fast urbanization in emerging countries, and increased petrochemical production in Asia Pacific and the Middle East.

In 2023, Enterprise Products Partners L.P. completed the expansion of its NGL fractionation facility in Mont Belvieu, Texas, boosting butane processing capacity to meet rising domestic and export demands from Asian and European markets. This expansion reflects the commercial significance of U.S. shale gas extraction in creating above-average butane supply growth whose export orientation sustains North American commercial activity beyond domestic consumption growth.

Market Size and Forecast

-

Market Size in 2026E: USD 122.30 Billion

-

Market Size by 2035: USD 189.62 Billion

-

CAGR: 4.93% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Butane Market - Request Free Sample Report

Butane Market Trends

-

Growing adoption of isobutane (R-600a) as an environmentally friendly refrigerant is driving demand from household refrigeration and commercial cooling equipment manufacturers seeking low-global-warming-potential alternatives

-

Expansion of LPG infrastructure and clean cooking fuel programs across developing economies is increasing butane consumption in residential and commercial energy applications

-

Rising integration of butane feedstocks in petrochemical complexes is supporting demand for ethylene, butadiene, and other chemical production processes, particularly in Asia Pacific and the Middle East

-

Seasonal use of butane in gasoline blending is sustaining refinery demand by enhancing fuel volatility and performance during colder weather conditions

-

Increasing shale gas and natural gas liquids (NGL) production in North America is expanding global butane supply and supporting growing export flows to regions with strong LPG and petrochemical demand

U.S. Butane Market Outlook

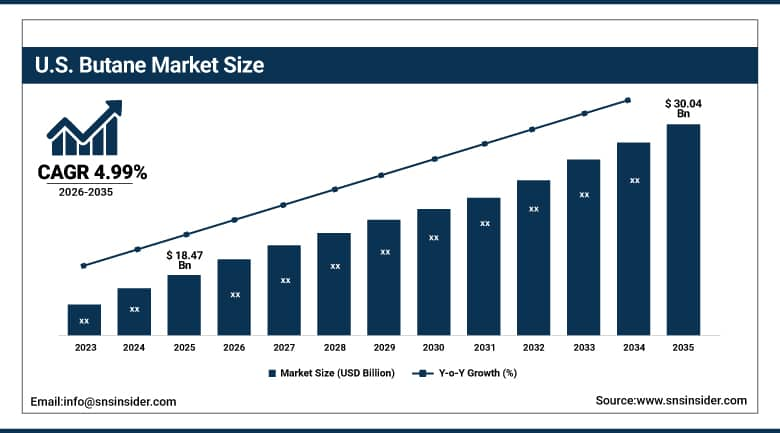

The U.S. Butane Market was valued at approximately USD 18.47 Billion in 2025 and is expected to reach approximately USD 30.04 Billion by 2035, growing at a CAGR of approximately 4.99%.

The United States held the largest market share within the North American butane market, accounting for 72% of regional revenue in 2023, primarily due to strong refining capacity, abundant natural gas reserves, and high demand across industrial and commercial sectors. Major refining hubs in Texas, Louisiana, and California contribute to large-scale butane production whose export orientation sustains domestic commercial activity beyond domestic consumption. The U.S. is a leading producer of LPG including butane, with the expanding petrochemical industry utilising butane as a key feedstock for ethylene and synthetic rubber production. Enterprise Products Partners, Phillips 66, and ExxonMobil collectively define the domestic butane production and fractionation commercial landscape. Growing adoption of butane across industrial, residential, and automotive fuel applications, combined with increasing exports to Asia and Europe, strengthens the U.S. market position.

In 2024, Phillips 66 invested USD 350 million in modernising its Freeport butane export terminal in Texas, boosting butane export handling capacity by 22% and reducing vessel loading times by 30%. This investment reflects the commercial opportunity of U.S. shale-derived butane surplus that positions American producers as swing exporters to Asia Pacific and European markets experiencing LPG demand growth above their domestic production capacity.

Butane Market Segment Analysis

-

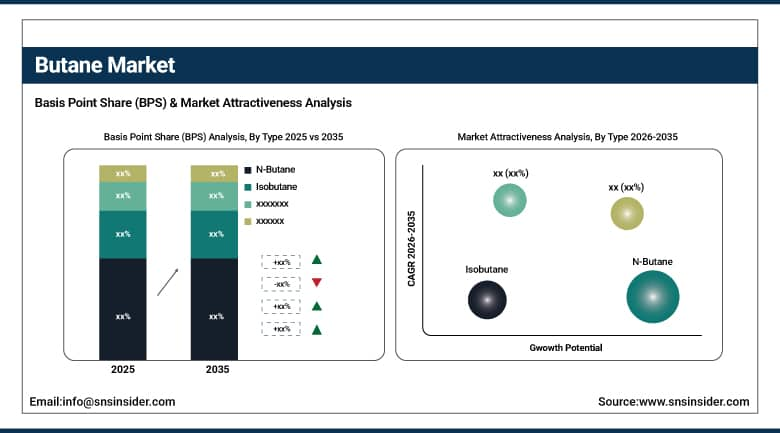

By Type, the N-Butane segment dominated the Butane Market with approximately 60% share in 2025, while the Isobutane segment is the fastest growing.

-

By Application, the Liquefied Petroleum Gas segment dominated the Butane Market with approximately 45% share in 2025, while the Petrochemicals segment is the fastest growing.

-

By End User, the Residential & Commercial segment dominated the Butane Market with approximately 53% share in 2025, while the Industrial segment is the fastest growing.

By Type, n-butane dominates, isobutane grows fastest

N-butane retained the dominant type position with approximately 60% of the butane market in 2025. Its commercial primacy reflects the extraordinary aggregate volume of LPG residential and commercial fuel consumption across global markets where butane is the primary or co-primary LPG component alongside propane. Each household that transitions from biomass, coal, or kerosene cooking to LPG creates n-butane procurement whose commercial aggregate across the hundreds of millions of developing world households undergoing energy transition sustains the segment's dominant volume position. N-butane's role as a winter gasoline blending agent, whose vapour pressure contribution to cold weather fuel formulation creates seasonal procurement from refinery blending operations across North America and Europe, creates an additional commercial demand stream that compounds with LPG fuel consumption. The steam cracking of n-butane to produce ethylene and 1,3-butadiene by petrochemical operators creates a third demand category whose commercial significance grows with petrochemical complex expansion in Asia Pacific.

Isobutane is the fastest growing type because its applications in eco-friendly refrigeration, high-octane gasoline production through refinery alkylation, and aerosol propellant formulation collectively create above-average demand growth across three commercially distinct sectors. The global refrigeration industry's regulatory-driven transition from HFC refrigerants toward R-600a isobutane creates structured procurement growth whose regulatory mandate timeline creates predictable demand expansion. Each household refrigerator, chest freezer, or commercial display cabinet that specifies R-600a instead of R-134a creates isobutane procurement whose commercial aggregate across global appliance production sustains fastest-growing type designation. Sinopec's 2024 inauguration of a USD 600 million butane isomerisation facility in Shandong Province, boosting isobutane production by 18%, demonstrates the commercial investment scale in isobutane supply capacity expansion.

By Application, LPG dominates, petrochemicals grow fastest

LPG retained the dominant application position with approximately 45% of the butane market in 2025. LPG's commercial dominance reflects its role as the most widely available bottled clean cooking and heating fuel for the global residential sector, particularly in developing economies where natural gas pipeline infrastructure is limited. India's Pradhan Mantri Ujjwala Yojana programme, which has distributed subsidised LPG connections to over 90 million below-poverty-line households, represents the world's most commercially significant government-led LPG adoption programme whose butane consumption impact compounds annually with connection utilisation rates. China's urban and rural LPG distribution network, Indonesia's LPG subsidy programme, and Vietnam's growing LPG adoption collectively sustain Asia Pacific's residential and commercial LPG consumption dominance. The autogas segment, encompassing approximately 27 million vehicles globally powered by propane-butane blends, creates an automotive application whose growth compounds with LPG vehicle adoption programmes in Turkey, South Korea, Poland, and Australia.

Petrochemicals is the fastest growing application because the extraordinary expansion of petrochemical complex capacity in Asia Pacific and the Middle East, whose ethylene crackers, butadiene extraction units, and isobutylene synthesis facilities create above-average butane feedstock procurement growth. Each new naphtha and LPG steam cracker that specifies mixed feed including butane creates long-duration procurement relationships whose take-or-pay contract structures sustain consistent butane demand independent of short-term price cycle variation. ExxonMobil, Saudi Aramco, and Sinopec's investments in large-scale petrochemical projects create the most commercially certain long-duration butane feedstock demand in the market. The global petrochemical market's projection to reach USD 5 trillion by 2030 underscores the integral role butane plays as a flexible feedstock across the most commercially dynamic chemical production expansion.

By End User, residential & commercial dominates, industrial grows fastest

Residential and commercial retained the dominant end user position with approximately 53% of the butane market in 2025. The category encompasses hundreds of millions of household LPG cooking and heating consumers across South Asia, Southeast Asia, sub-Saharan Africa, and Latin America whose combined consumption creates the world's most commercially distributed butane demand base. Each developing world household that adopts LPG for cooking eliminates the indoor air pollution, deforestation, and health consequences of biomass fuel use while creating durable butane consumption whose continuation is reinforced by the capital investment in LPG cylinder and appliance purchase. Commercial food service operations, hospitality sector heating applications, and the small enterprise manufacturing sector's process heating requirements create the commercial sub-segment whose aggregate reinforces residential dominance in the combined category.

Industrial is the fastest growing end user because petrochemical feedstock procurement, manufacturing process heating, aerosol product propellant manufacturing, and specialty chemical production collectively create above-average industrial-grade butane demand growth that compounds with manufacturing sector expansion across Asia Pacific and the Middle East. Each new petrochemical complex, each aerosol product manufacturer expanding production, and each industrial refrigeration installation converting from HFC refrigerants to isobutane creates industrial butane procurement whose commercial aggregate across a growing and diversifying industrial application set sustains the fastest-growing end user designation throughout the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

72.0% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Butane Market Insights

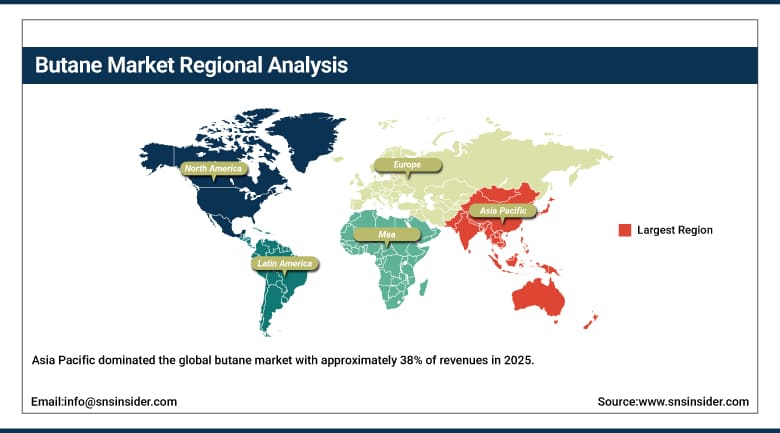

Asia Pacific dominated the global butane market with approximately 38% of revenues in 2025. This dominance is underpinned by massive demand for LPG in residential sectors across India, China, Indonesia, and Vietnam, combined with the region's industrial expansion, increasing urbanisation, and proactive government policies to promote clean cooking fuels. China accounts for approximately 44.8% of Asia Pacific revenues through its large LPG distribution network, the extraordinary domestic petrochemical complex's feedstock procurement, and the growing automotive LPG adoption.

India represents the most commercially dynamic emerging market within Asia Pacific where the Pradhan Mantri Ujjwala Yojana programme's household LPG connection expansion, the growing petrochemical sector's butane feedstock requirements, and the urban commercial sector's LPG adoption create above-average demand growth that compounds with India's energy transition trajectory.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Butane Market Insights

North America is the second-largest butane market with approximately 25% of global revenues in 2025, driven by the presence of major industry players, export potential, and developing shale gas extraction creating above-average production growth. The United States accounts for approximately 72% of North American revenues through its large refinery network, Enterprise Products Partners, Phillips 66, and ExxonMobil's NGL fractionation operations.

Canada contributes approximately 28% of North American revenues through its oil sands natural gas liquid extraction, the petrochemical sector's butane feedstock procurement in Alberta, and the LPG distribution network serving residential and agricultural heating applications across the Prairie provinces.

Europe Butane Market Insights

Europe is a technically sophisticated butane market where the EU's aerosol regulation, HFC refrigerant phase-out framework, and energy security investment create structured demand evolution. Germany accounts for approximately 22.3% of European revenues through its chemical industry's isobutane feedstock procurement, the refrigeration sector's R-600a adoption, and the LPG distribution network serving residential and commercial applications.

Russia, the United Kingdom, and France are significant secondary markets where North Sea gas production's LPG output, industrial butane processing, and the growing aerosol product manufacturing sector create consistent commercial procurement. Shell's and BP's European LPG operations sustain regional commercial supply infrastructure.

MEA & Latin America Butane Market Insights

Saudia Arabia dominates MEA revenues with around 31.2%, attributed to the top-notch NGL recovery and LPG export capabilities of Saudi Aramco, the procurement of butane feedstock for the domestic petrochemical industry, and the usage of LPG by the residential sector in the Gulf. The NGL activities of ADNOC and QatarEnergy provide an important complement in terms of Gulf demand and supply. Brazil is the dominant player in Latin America with around 44.2%, due to the domestic LPG market of the residential sector, feedstock demand from the petrochemical industry, and the NGL activities of Petrobras.

Market Dynamics

Growth Drivers: Rising LPG demand in developing economies and petrochemical feedstock expansion in Asia Pacific and the Middle East

Rising LPG demand in developing economies is the butane market's most commercially certain structural growth driver. The global energy transition's first-order priority in most developing nations is transitioning households from biomass and kerosene cooking fuels to clean-burning LPG, whose health, deforestation, and indoor air quality benefits create policy motivation that sustains government subsidy investment through national development plan cycles. India's Pradhan Mantri Ujjwala Yojana programme, Indonesia's LPG subsidy framework, and Africa's Cooking Clean Initiative collectively create the most commercially certain multi-decade LPG demand expansion in the butane market.

Petrochemical feedstock demand expansion in Asia Pacific and the Middle East, whose new crackers and derivative production facilities create long-duration butane procurement relationships, represents the most commercially significant industrial demand driver. Saudi Aramco's, ExxonMobil's, and Sinopec's investments in large-scale petrochemical projects create structured feedstock procurement whose take-or-pay contract structures sustain consistent commercial demand independent of short-term LPG price cycle variation.

Restraints: Crude oil price volatility and environmental regulations on LPG emissions

Crude oil and natural gas price volatility creates pricing uncertainty for butane producers whose production cost is directly linked to crude oil feedstock pricing and whose sales price follows LPG benchmark indices that fluctuate with crude oil market movements. Each major oil price cycle creates production economics variation that impacts butane producer margin predictability and investment planning, moderating capacity expansion decisions during periods of sustained low oil prices.

Environmental regulations targeting LPG distribution infrastructure emissions, LNG vehicle adoption as an alternative to LPG autogas, and the long-term energy transition toward electrification create structural demand displacement concerns for the residential and automotive LPG market segments. Each electricity grid expansion into LPG-dependent rural communities and each electric vehicle adoption programme that targets LPG autogas vehicles creates potential demand displacement that moderates long-term butane market growth expectations beyond the 10-year forecast horizon.

Opportunities: R-600a refrigerant adoption and butane-to-olefins petrochemical pathway investment

R-600a isobutane refrigerant adoption represents the most commercially certain near-term market expansion opportunity whose regulatory mandate creates a defined demand growth timeline. Each jurisdiction that implements HFC refrigerant phase-out schedules under the Kigali Amendment to the Montreal Protocol creates structured isobutane refrigerant procurement whose commercial aggregate across global appliance manufacturing sustains above-average isobutane demand growth. The global household refrigerator replacement cycle, which generates approximately 100 million new unit sales annually, creates an R-600a procurement stream that sustains isobutane demand growth proportional to HFC phase-out timeline implementation.

Butane-to-olefins investment, whose on-purpose light olefin production from dedicated butane dehydrogenation units creates propylene and butylene supply supplementing steam cracker output, represents the most commercially premium petrochemical feedstock opportunity. Each isobutane dehydrogenation unit whose isobutylene production supplies MTBE and alkylate blending stock creates a premium butane demand category whose pricing above commodity LPG-grade butane sustains producer investment motivation.

Recent Developments:

-

2025: Sinopec partnered with CATL in April 2025 to establish 10,000 battery swap stations across China by end of 2025, reflecting broader energy diversification strategy while continuing its core butane and LPG production and distribution operations across domestic and export markets.

-

2024: Sinopec inaugurated a USD 600 million butane isomerisation facility in Shandong Province in March 2024, enhancing isobutane production capacity by 18% to directly feed alkylation units and growing R-600a refrigerant demand across domestic appliance manufacturing.

-

2024: Phillips 66 invested USD 350 million in modernising its Freeport butane export terminal in Texas in 2024, boosting butane export handling capacity by 22% and reducing vessel loading times by 30% to capture growing Asian import demand.

-

2024: Indian Oil Corporation announced plans to invest in a large-scale LPG bottling plant in West Bengal, India in 2024, targeting increasing rural demand for LPG and enhancing butane consumption regionally through expanded last-mile distribution infrastructure.

-

2023: Enterprise Products Partners L.P. completed the expansion of its NGL fractionation facility in Mont Belvieu, Texas in 2023, boosting butane processing capacity to meet rising domestic and export demand from Asia Pacific and European LPG markets.

Butane Market Key Players

-

Saudi Aramco

-

Sinopec

-

ADNOC

-

China National Petroleum Corporation (CNPC)

-

ExxonMobil Corporation

-

Kuwait National Petroleum Company (KNPC)

-

Phillips 66 Company

-

Bharat Petroleum Corporation Ltd.

-

Pemex

-

TotalEnergies SE

-

QatarEnergy

-

Equinor ASA

-

BP plc

-

PJSC Gazprom

-

Chevron Phillips Chemical Company LLC

-

ConocoPhillips Company

-

Shell plc

-

Enterprise Products Partners L.P.

-

Ecopetrol S.A.

-

Indian Oil Corporation Ltd

Butane Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 116.55 Billion |

| Market Size by 2035 | USD 189.62 Billion |

| CAGR | CAGR of 4.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (N-Butane, Isobutane) • by Application (Liquefied Petroleum Gas/LPG, Petrochemicals, Refineries, Aerosol Propellants, Others) • by End User (Residential & Commercial, Industrial, Automotive) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Saudi Aramco, Sinopec, ADNOC, China National Petroleum Corporation (CNPC), ExxonMobil Corporation, Kuwait National Petroleum Company (KNPC), Phillips 66 Company, Bharat Petroleum Corporation Ltd., Pemex, TotalEnergies SE, QatarEnergy, Equinor ASA, BP plc, PJSC Gazprom, Chevron Phillips Chemical Company LLC, ConocoPhillips Company, Shell plc, Enterprise Products Partners L.P., Ecopetrol S.A., Indian Oil Corporation Ltd. |

Frequently Asked Questions

Asia Pacific led the Butane Market in the region with the highest revenue share in 2023.

Growing demand for liquefied petroleum gas (LPG) in residential and commercial sectors drives the butane market growth.

Residential/Commercial will grow rapidly in the Butane Market from 2024 to 2032.

The expected CAGR of the global Butane Market during the forecast period is 4.93%

The Butane Market was valued at USD 105.84 billion in 2023.

Get in Touch