Cable Assembly Market Report Scope & Overview:

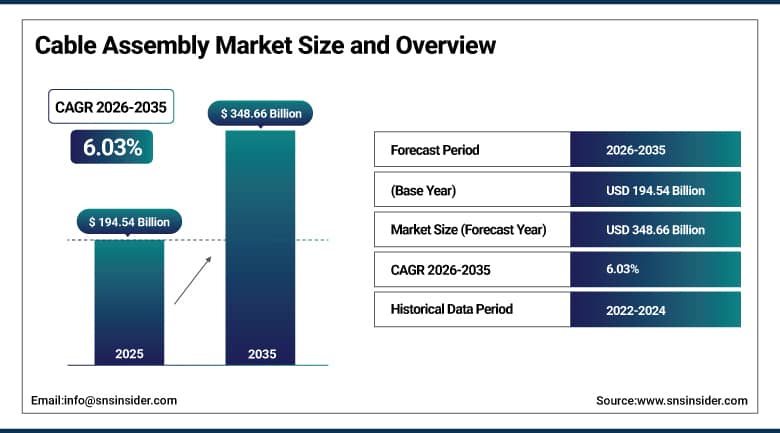

The Cable Assembly Market was valued at USD 194.54 billion in 2025 and is expected to reach USD 348.66 billion by 2035, growing at a CAGR of 6.03% from 2026–2035.

The cable assembly market is experiencing consistent growth on a global scale owing to the growing demand for secure connection technology within various applications. Adoption of automation technologies, IoT, and high data communication technologies will generate demand for technologically sophisticated cable assemblies. Demand for cable assemblies will be fueled by growth within the field of automotive electronics, aerospace industry, and industrial machinery. The use of data centers and cloud computing will create demands for efficient cable assembly products. The rise in renewable energy and smart grids will increase demand for rugged assemblies. Increase in electronic content in vehicles will also contribute to the market growth.

In accordance with UNICS/UN data as well as structural industry data provided by OECD, optical fibre cables production is indicated in metric tonnes, including the production of 1,127.40 metric tonnes in Brazil in 2015 and 2,249.44 metric tonnes in Brazil in 2014.

As per the OECD, value chains include cable assemblies used in electronics, telecommunication, and industry sectors, and as per UN trade statistics, electrical machinery and parts as HS-coded products are accounted for in more than 140 countries around the world.

Market Size and Forecast:

-

Market Size 2026E: USD 205.88 billion

-

Market Size 2035: USD 348.66 billion

-

CAGR (2026 - 2035): 6.03%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Cable Assembly Market - Request Free Sample Report

Cable Assembly Market Trends:

-

Faster adaptation of high-speed fiber optic cables results in improved data transmission capabilities exceeding 30% worldwide in 2025.

-

Tightened e-waste laws lead to 25% growth in recycled cable assembly materials utilization among industrial manufacturers in 2024.

-

The rise in electric car manufacturing contributes to a growing need for light cable assembly systems, with a significant growth rate of 28% expected in 2026 within automotive applications.

-

A higher number of AI-based data centers necessitates high-density cable assembly solutions, leading to increased interconnect density and power savings by 35%.

-

Smart factories using Industrial IoT result in increased use of modular cable assembly solutions, saving 22% of installation and maintenance time.

U.S. Cable Assembly Market Size Outlook:

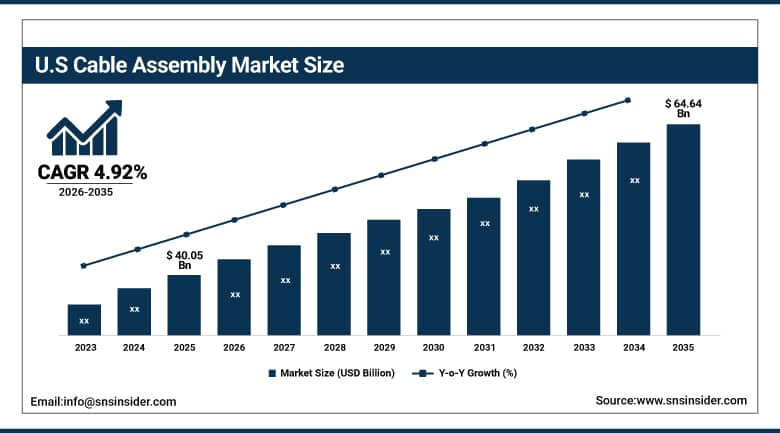

The U.S. Cable Assembly Market was valued at USD 40.05 Billion in 2025 and is expected to reach around USD 64.64 Billion by 2035, growing at a CAGR of 4.92% from 2026–2035.

The U.S. Cable Assembly Market is witnessing strong growth because of increasing demand for high-performance connectivity solutions and advanced power distribution systems. Cable assembly deployment across aerospace electronics, data centers, and automotive industries has been responsible for strong market expansion. Increasing investments in 5G infrastructure and semiconductor ecosystem development have led to rising demand for advanced cable assembly systems. Growing development of electric vehicles, defense electronics, and industrial automation is further supporting market adoption. Continuous focus on technological innovation and next-generation communication networks is strengthening market growth.

According to the U.S. Census Bureau Annual Survey of Manufactures and associated industry statistics programs, U.S. manufacturing plants for NAICS industries 31–33 maintain annual production, employment, payroll, and value-added statistics for measuring industrial production, which includes electrical wiring and cable assembly.

Cable Assembly Market Segment Analysis:

-

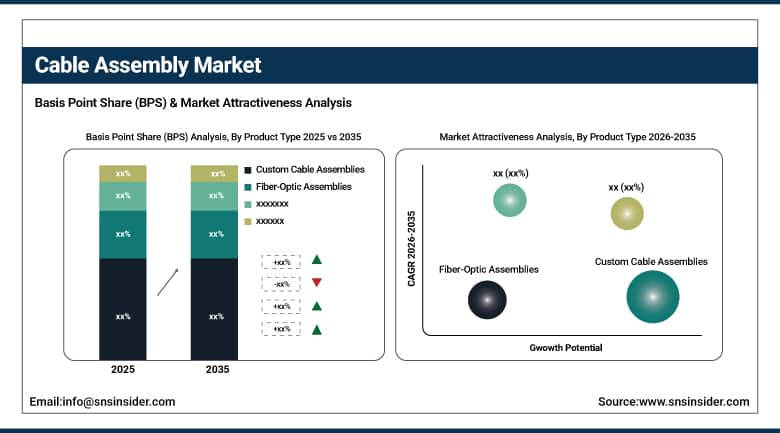

By Product Type, Custom Cable Assemblies dominated the Cable Assembly Market with 41.87% share in 2025; while Fiber-Optic Assemblies are the fastest growing segment with CAGR of 15.17% during 2026 to 2035.

-

By Cable Type, Power dominated the Cable Assembly Market with 45.36% share in 2025; while Fiber-Optic are the fastest growing segment with CAGR of 11.40% during 2026 to 2035.

-

By End-Use Industry, Automotive & Transportation dominated the Cable Assembly Market with 39.84% share in 2025; while IT & Data Centers are the fastest growing segment with CAGR of 11.41% during 2026 to 2035.

-

By Application, Power Distribution dominated the Cable Assembly Market with 37.90% share in 2025; while Data Transfer & Communication are the fastest growing segment with CAGR of 10.74% during 2026 to 2035.

By Product Type, Custom Cable Assemblies dominated the Cable Assembly Market in 2025, while Fiber-Optic Assemblies are the fastest growing segment.

Custom Cable Segment held the dominated market share in terms of revenue during the period 2025 in the Cable Assembly Market. The dominance of the segment is attributed to the growing demand for application-specific customized cables in various sectors such as automotive, aerospace, industrial automation, and telecom infrastructure. Companies like using customized cables due to their flexibility, durability, and suitability to be used in complex applications. The increased use of customized cables in hostile and critical operations will fuel their adoption.

Fiber-Optic Assemblies Segment is expected to register the fastest CAGR between 2026 and 2035. The rapid growth of the segment will result from the increasing demand for ultra-high-speed data transmission capabilities, lower latencies, and broadband network capabilities. The expanding use of 5G networks, data centers, cloud computing, and AI-enabled workloads will drive growth. Increased usage in the defense sector, aerospace applications, and telecom networks will also contribute to the growth of the segment.

By Cable Type, Power dominated the Cable Assembly Market in 2025, while Fiber-Optic are the fastest growing segment.

The Power Segment accounted for the dominated revenue share in the Cable Assembly Market in 2025. It is highly influenced by increased usage in industrial applications, automotive applications, and infrastructure power distribution. The growing need for energy transfer and delivery through such cables has resulted in an increased demand for the segment. Growth in the development of electrification projects, renewable energy, and automation has also fueled demand for the segment, which makes it the most stable in the market.

The Fiber Optic segment is anticipated to have the fastest CAGR during the forecast period. High demand for fiber optic technology due to the rise in usage for transmitting data at high speeds is driving growth. Growing developments in the field of telecommunications, aerospace engineering, and data centers are also contributing to the growth of the segment in the market. Technological advancements and ongoing digital transformation efforts worldwide are boosting the segment's prospects.

By End-Use Industry, Automotive & Transportation dominated the Cable Assembly Market in 2025, while IT & Data Centers are the fastest growing segment.

Automotive & Transportation Segment emerged as the dominated player in the Cable Assembly Market in terms of market share in 2025. The large share is attributed to the increased usage of cable assemblies in EVs, infotainment, battery management systems, and ADAS. Vehicle electrification trends and increased requirement for high-quality wiring harness assembly solutions further fuel adoption levels. Increase in global automobile production, as well as the inclusion of smart electronics into cars, also plays an important role in maintaining market dominance.

The IT & Data Centers segment is projected to witness the fastest CAGR during 2026-2035. The fast growth in the market is on account of growing demand for high bandwidth and speed requirements in connection with data transfer operations, cloud computing, and AI-based workloads. Development of hyperscale data centers, as well as growth in internet traffic, also fuels adoption rates of premium fiber optic and cable assemblies in the market. Investments in 5G technologies, edge computing, and digital transformation initiatives fuel market growth rates.

By Application, Power Distribution dominated the Cable Assembly Market in 2025, while Data Transfer & Communication are the fastest growing segment.

The Power Distribution sub-segment accounted for the dominated market share in revenue among all segments of the Cable Assembly Market in 2025. This was mainly due to the extensive use of the product across industry systems, automotive wire harnesses, and power grid networks. The need for reliable distribution of electricity in different manufacturing facilities and commercial settings remains one of the key factors boosting its usage. Investments in renewable energy and smart grid systems increase the demand for durable cable assemblies in this application field.

The Data Transfer & Communication sub-segment is expected to have the fastest CAGR between 2026 and 2035. Demand for the product is driven by rising numbers of advanced communication and data transfer solutions. Adoption of cloud computing systems, 5G technology, and artificial intelligence-based infrastructure contributes to growth. The adoption of fiber optic cables in telecom infrastructure enhances the performance of these systems.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.64% |

|

Europe |

Germany |

27.80% |

|

Asia Pacific |

China |

41.20% |

|

Middle East & Africa |

UAE |

17.60% |

|

Latin America |

Brazil |

44.30% |

Asia Pacific Cable Assembly Market Insights.

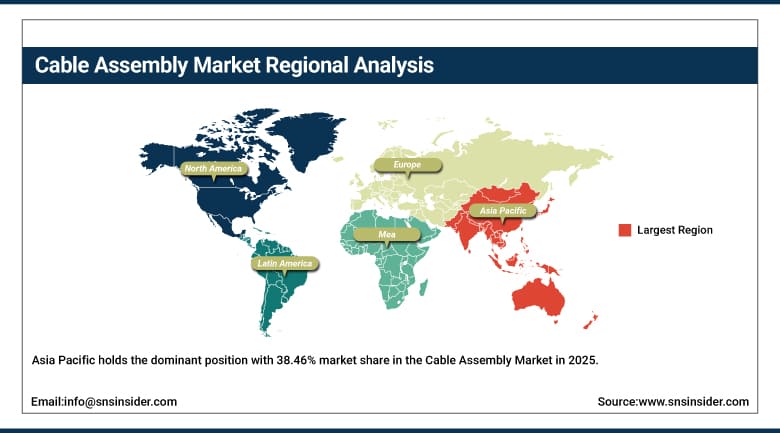

Asia Pacific holds the dominant position with 38.46% market share in the Cable Assembly Market in 2025 and is also the fastest growing region with a CAGR of 7.69% due to strong demand expansion across electronics manufacturing and telecommunications infrastructure. China, Japan, South Korea, India, and Taiwan are key contributors. Rising demand for consumer electronics, data centers, and 5G networks is boosting adoption. Expanding manufacturing capacity, government-backed digital programs, and fiber-optic deployment are further strengthening regional market growth.

According to the Asian Development Bank Key Indicators Database and UN ESCAP publications on the electronics value chain in Asia and the Pacific, Asia has a substantial portion of the world's electronics manufacturing activities, which account for more than 80% of ICT products manufactured globally and more than 12% of global merchandise exports being associated with electronic products. In the Asia Pacific region, insulation wire and cables production amounted to 19 million tons in 2024, representing a 7.3% yearly growth, whereas optical fibers, cables, and bundles amounted to 1.1 million tons.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Cable Assembly Market Insights.

North American cable assembly market's significance has been attributed to the region's robust aerospace electronic demands and highly developed infrastructure facilities for connectivity. Some of the key strengths in the North American region include the presence of major technology firms, defense systems, and advanced data center networks. The growing demand for fiber optics connections, automobile electronics, and industrial automation systems will continue to fuel the regional market's growth going forward.

In accordance to U.S. Census Bureau NAICS system, manufacturing activities related to cable assembly fall under the manufacturing activities of fiber optic cables and insulated wire and cable industry, with more than 50% of the material used in U.S. conductors being consumed in the manufacture of electrical/communication cables, mainly due to standardization of materials used in North America.

Europe Cable Assembly Market Insights.

The Europe Cable Assembly Market makes an important contribution in 2025 owing to strong industrial automation and automotive electronics demand. Countries like Germany, United Kingdom, France, Italy, and Netherlands are leading contributors to regional demand. High focus on renewable energy integration, electric vehicle production, and industrial connectivity solutions is supporting consistent market growth. Increasing investments in European digital strategy and smart manufacturing programs are strengthening adoption across transportation and telecom sectors.

As per Eurostat PRODCOM manufacturing statistics, EU production data for electrical cable-related assemblies is systematically recorded across NACE industrial classifications covering manufacturing enterprises in EU-27 countries. As stated by EU statistical frameworks, intra-EU trade represents a major share of electrical component flows, while Central and Eastern European countries account for a significant portion of manufacturing output due to industrial relocation trends and integrated European automotive and electronics supply chains.

Middle East & Africa and Latin America Cable Assembly Market Insights.

The Middle East & Africa region along with Latin America will exhibit steady growth in the Cable Assembly Market up to 2025 due to increasing investments in infrastructure modernization and telecommunications expansion. Countries such as UAE, Saudi Arabia, South Africa, Brazil, and Mexico are emerging contributors. Growing demand for smart cities, broadband connectivity, and industrial automation is increasing adoption. Infrastructure development and renewable energy projects are further driving market expansion across both regions.

As per the United Nations Conference on Trade and Development, along with ITU Telecommunications Indicators, Africa and Latin America contribute around 2.5% towards global ICT service exports, which is quite insignificant in view of their lack of participation in the sophisticated digital hardware production process. As per the World Bank ICT Development database and telecom regulatory reviews, the Middle Eastern nations are experiencing an increase in mobile broadband penetration that exceeds 80% of the overall population in certain Gulf states, whereas the average internet usage rate in Latin America has exceeded 70%.

Market Dynamics:

Growth Drivers: Increasing demand for high-speed connectivity across digital infrastructure and communication networks expansion globally

Due to rapid growth of data center technology, cloud technology, and 5G networking, the demand for modern cable assemblies is increasing. High speed data transmission needs in telecom, IT infrastructure, and corporate networks have promoted the use of fiber optics and hybrid cables. Digitalization trends in different industries including automotive, health care, and manufacturing have increased the demand further. The need for continuous improvement of communication systems along with higher internet penetration around the world is leading to increased deployments of high-quality cable assemblies.

According to ITU’s Global Connectivity Report 2025, global Internet traffic is still increasing at a fast pace, with Internet usage worldwide growing to approximately 6 billion users by the year 2025. As reported by the broadband indicators from the OECD, the trend towards fiber networks for fixed broadband is rising to support increased data transfer speeds.

Restraints:Intense market competition and presence of low-cost alternatives restricting profit margins across global cable assembly industry

Rapid growth in the manufacturing and installation of electric vehicles has raised the need for high-quality power and signal cable assemblies. Projects that harness renewable energy sources like solar and wind require efficient cable assembly solutions. Industrial electrification and intelligent grids are providing additional avenues for their growth. Rising concern for sustainable energy solutions along with the rise in automotive technology is paving the way forward for the market’s growth.

According to World Trade Organization and UNCTAD statistics, more than 80% of global merchandise trade consists of manufactured goods, intensifying price-based competition among suppliers worldwide. UNCTAD reports that global value chains account for around 50% of international trade, increasing exposure to low-cost sourcing and alternative suppliers across multiple regions. This high substitutability of standardized cable assembly products contributes to persistent margin pressure in highly fragmented manufacturing markets globally sector worldwide.

Opportunities: Growing electric vehicle adoption and renewable energy infrastructure development creating new application areas for cable assemblies

Rapid expansion in manufacturing and charging stations of electric vehicles (EVs) has resulted in a growing need for power and signal cable assemblies. Renewable energy sources like solar or wind energy generation projects are using reliable connectivity products. There has been increased use of connectivity solutions with industrial and smart grid electrification. Growing emphasis on energy sustainability and automobile electronics technologies has created new opportunities. Technological improvements in energy storage and power management solutions have provided further impetus to market growth.

According to the International Renewable Energy Agency, the world’s renewable power capacity stood at 4,448 GW in 2024, whereby solar and wind energy made up more than 96% of all the new capacity additions, signifying significant infrastructure growth. As per the IEA, there were more than 5 million publicly accessible charging points for electric vehicles worldwide in 2024, out of which more than 1.3 million were installed within one year.

Recent Developments:

-

2026: Molex introduced Impress co-packaged copper solutions enabling 224Gbps PAM-4 near-ASIC connectivity for AI-driven hyperscale data center architectures.

-

2025: TE Connectivity launched Ultra Low-Profile PCIe Gen 7 connectors and cable assemblies delivering 128 GT/s performance for next-generation AI and data centers

-

2025: Molex introduced VersaBeam expanded beam optical interconnect solutions for hyperscale data centers improving fiber density and deployment efficiency.

-

2024: Amphenol Corporation strengthened aerospace and defense interconnect demand through expanded harsh environment product manufacturing capabilities.

Cable Assembly Market Key Players are:

-

Amphenol Corporation

-

TE Connectivity

-

Molex

-

Aptiv

-

Yazaki Corporation

-

Sumitomo Electric Industries

-

LEONI AG

-

Nexans

-

Prysmian Group

-

Belden Inc.

-

Samtec Inc.

-

Rosenberger Group

-

Radiall

-

Hirose Electric Co., Ltd.

-

Carlisle Companies Incorporated

-

Luxshare Precision Industry Co., Ltd.

-

Foxconn Interconnect Technology Limited

-

Japan Aviation Electronics Industry, Ltd.

-

Glenair, Inc.

-

Fischer Connectors

Cable Assembly Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 194.54 Billion |

| Market Size by 2035 | USD 348.66 Billion |

| CAGR | CAGR of 6.03% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Custom Cable Assemblies, Standard / Off-the-Shelf Assemblies, Overmolded Cable Assemblies, Fiber-Optic Assemblies, Other) • By Cable Type (Fiber-Optic, Coaxial, Power, Ribbon / Flat, Other) • By End-Use Industry (Automotive & Transportation, IT & Data Centers, Telecommunications, Industrial & Manufacturing, Aerospace & Defense, Healthcare) • By Application (Data Transfer & Communication, Power Distribution, Signal & Control, High-Performance Computing, Other) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amphenol Corporation, TE Connectivity, Molex, Aptiv, Yazaki Corporation, Sumitomo Electric Industries, LEONI AG, Nexans, Prysmian Group, Belden Inc., Samtec Inc., Rosenberger Group, Radiall, Hirose Electric Co., Ltd., Carlisle Companies Incorporated, Luxshare Precision Industry Co., Ltd., Foxconn Interconnect Technology Limited, Japan Aviation Electronics Industry, Ltd., Glenair, Inc., Fischer Connectors |

Frequently Asked Questions

The Cable Assembly Market is expected to grow at a CAGR of 6.03% from 2026 to 2035.

The Cable Assembly Market was valued at USD 194.54 billion in 2025.

Power Distribution dominated the market in 2025 due to widespread use in industrial, automotive, and grid applications.

Rising demand for high-speed connectivity, EV adoption, 5G expansion, and industrial automation are driving market growth.

Asia Pacific dominated the Cable Assembly Market due to strong manufacturing base, telecom expansion, and electronics production.

Get in Touch