Capillary Electrophoresis Market Report Scope & Overview:

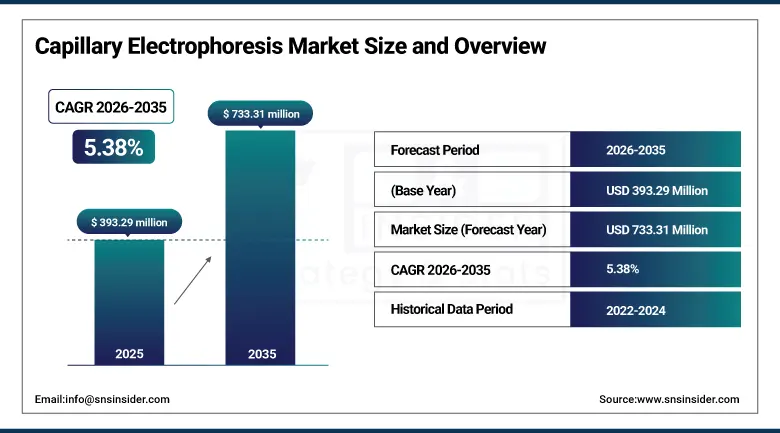

The Capillary Electrophoresis Market was valued at USD 393.29 Million in 2025 and is expected to reach USD 733.31 Million by 2035, growing at a CAGR of 5.38% from 2026–2035.

The global capillary electrophoresis market is growing at a sustained and commercially broad-based pace. Capillary electrophoresis is an analytical separation technique that resolves ionic species by their charge and size within a narrow silica capillary under high voltage, providing high-resolution, high-efficiency separation of complex biological, pharmaceutical, and chemical samples. The technique is indispensable for DNA sequencing, monoclonal antibody characterisation, biopharmaceutical lot-release testing, and food safety contaminant analysis. Market growth is driven by rapid advancements in biotechnology, rising pharmaceutical R&D, increasing genomic research funding, and the growing application of CE in biologics characterisation for regulatory submission support.

In 2024, Agilent Technologies introduced dynamically coated capillaries designed to enhance separation efficiency and reproducibility in capillary electrophoresis applications. The coating technology reduces protein adsorption to capillary walls that creates peak asymmetry and carryover in biopharmaceutical protein analysis, directly improving the analytical quality of biologics characterisation workflows whose regulatory submission accuracy depends on the CE separation's reproducibility and resolution performance.

Market Size and Forecast:

-

Market Size in 2026E: USD 414.45 Million

-

Market Size by 2035: USD 733.31 Million

-

CAGR: 5.38% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Capillary Electrophoresis Market - Request Free Sample Report

Capillary Electrophoresis Market Trends:

-

Growing biologics and biosimilar development is increasing demand for capillary electrophoresis systems used in protein characterization, purity testing, and quality control applications

-

Adoption of multi-capillary electrophoresis platforms is expanding in genomics laboratories due to their high-throughput DNA analysis and sequencing capabilities

-

Integration of capillary electrophoresis with mass spectrometry (CE-MS) is enhancing analytical performance for proteomics, metabolomics, and impurity profiling applications

-

Development of microchip-based electrophoresis technologies is enabling faster, portable, and low-sample-volume analysis for clinical and research applications

-

Increasing regulatory compliance requirements are driving investment in advanced capillary electrophoresis software, data management, and validation solutions across pharmaceutical laboratories

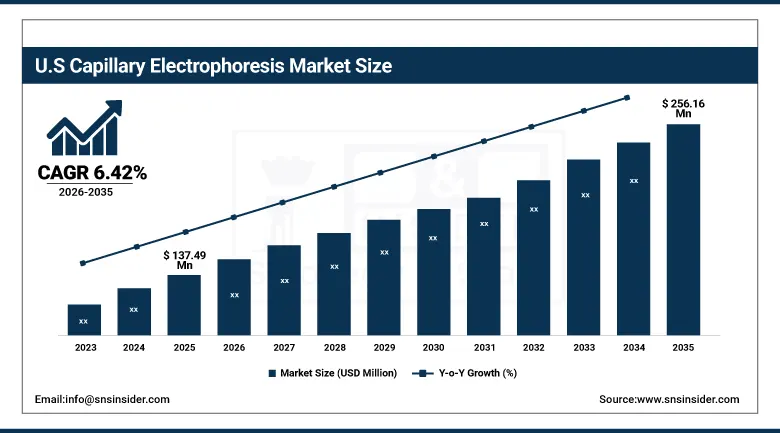

U.S. Capillary Electrophoresis Market Outlook:

The U.S. Capillary Electrophoresis Market was valued at approximately USD 137.49 Million in 2025 and is expected to reach approximately USD 256.16 Million by 2035, growing at a CAGR of approximately 6.42%.

The U.S. is the most commercially significant national capillary electrophoresis market within North America's dominant ~40% global revenue share. Agilent Technologies, Thermo Fisher Scientific, SCIEX, and Beckman Coulter's U.S. operations define the commercial CE landscape. The biopharmaceutical industry's extensive CE deployment for IgG charge variant analysis, purity determination, and glycan profiling sustains above-average per-facility CE procurement. NIH's USD 45 billion research budget creates consistent academic CE procurement.

A leading U.S. research consortium received major federal funding in 2025 to integrate advanced CE systems into personalised medicine and genomics programmes, supporting the deployment of multi-capillary CE arrays for large-scale DNA fragment analysis and next-generation sequencing library quality assessment. The funding reflects the strategic national investment in analytical infrastructure whose CE component creates structured institutional procurement that sustains the academic and government laboratory CE market independently of commercial pharmaceutical procurement cycles.

Capillary Electrophoresis Market Segment Analysis:

-

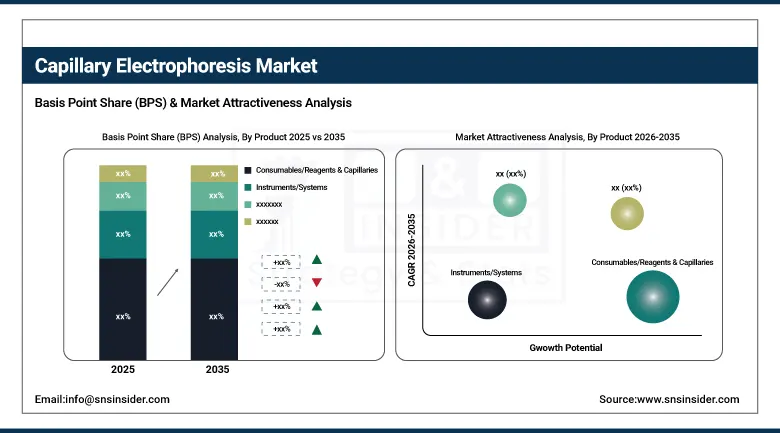

By Product, the Consumables segment dominated the Capillary Electrophoresis Market with approximately 58% share in 2025, while the Instruments segment is the fastest growing.

-

By Mode, the Capillary Zone Electrophoresis (CZE) segment dominated the Capillary Electrophoresis Market with 42.5% share in 2025, while the Capillary Isoelectric Focusing (CIEF) segment is the fastest growing.

-

By Application, the Nucleic Acid Analysis segment dominated the Capillary Electrophoresis Market with 37.73% share in 2025, while the Environmental & Food Safety Testing segment is the fastest growing.

-

By End User, the Pharmaceutical & Biotechnology Companies segment dominated the Capillary Electrophoresis Market with 35.5% share in 2025, while the Contract Research Organizations segment is the fastest growing.

By Product, consumables dominate, instruments grow fastest

Consumables retained the dominant product position with approximately 58% of the capillary electrophoresis market in 2025. CE consumables' commercial primacy reflects the recurring replacement model whose bare fused-silica capillary replacement after a defined number of injection cycles, buffer replenishment for each analysis sequence, and proprietary reagent kit consumption for each application create consistent per-installation revenue that scales with analytical throughput volume. The pharmaceutical lot-release laboratory's high daily CE run volume creates proportional consumable consumption that sustains commercial relationships across multi-year instrument operational periods. Each new CE system installation creates a decade-scale consumable procurement relationship whose aggregate value substantially exceeds the instrument's capital cost over its operational lifetime.

Instruments are the fastest-growing product because the biopharmaceutical industry's systematic adoption of CE for biologics characterisation and the genomic laboratory's high-throughput DNA fragment analysis requirements are creating new system installation demand beyond replacement procurement. Each new biopharmaceutical manufacturing facility that establishes CE-based lot-release testing methodology creates instrument procurement whose validation and regulatory filing sustains long-duration installation relationships. The introduction of technologically advanced systems like Agilent's dynamically coated capillary platforms creates performance differentiation that motivates laboratory upgrade procurement beyond normal lifecycle replacement timing.

By Mode, CZE dominates, CIEF grows fastest

Capillary zone electrophoresis retained the dominant mode position with 42.5% of the capillary electrophoresis market in 2025. CZE's commercial dominance reflects its position as the most universally applicable CE mode whose separation principle based on differential electrophoretic mobility under applied voltage creates a broadly applicable framework for pharmaceutical purity testing, protein charge analysis, and small molecule separation that requires no gel matrix or specialised buffer chemistry beyond the aqueous background electrolyte system. Each pharmaceutical small molecule impurity profile by CE, each amino acid analysis for protein sequence confirmation, and each charge heterogeneity assessment for peptide therapeutics creates CZE procurement that compounds with the pharmaceutical analytical testing volume's growth.

CIEF is the fastest-growing mode because monoclonal antibody charge variant profiling has become a critical quality attribute whose regulatory submission requirement across the biopharmaceutical industry's extraordinary mAb pipeline creates systematic CIEF method adoption. Each biopharmaceutical company that files an IND for a new monoclonal antibody therapeutic creates CIEF charge variant profile data whose ICH Q6B guideline requirement sustains CIEF instrument and method procurement across the clinical development programme. The biosimilar industry's analytical similarity testing requirement for charge variant comparability with the reference product creates additional CIEF procurement that compounds with the extraordinary biosimilar pipeline growth.

By Application, nucleic acid analysis dominates, food safety grows fastest

Nucleic acid analysis retained the dominant application position with 37.73% of the capillary electrophoresis market in 2025. The multi-capillary CE platform's role as the analytical workhorse of forensic DNA typing, clinical genetic testing, and NGS library quality assessment creates a consistently high-volume capillary consumable consumption category whose annual procurement per instrument reflects the frequency of fragment analysis runs in routine laboratory settings. Each forensic laboratory performing STR typing, each clinical genetic laboratory performing fragment analysis for mutation detection, and each NGS core facility performing library quality control creates CE capillary consumption that compounds with testing volume growth in each of these laboratory categories.

Environmental and food safety testing is the fastest-growing application because regulatory expansion of food contaminant monitoring programmes, pesticide residue limits, and environmental pollutant detection requirements creates growing CE adoption outside the pharmaceutical sector where the technique's existing deployment is well established. The EU's progressive tightening of pesticide maximum residue levels, China's food safety law implementation, and U.S. FDA's food safety modernisation act compliance create structured institutional CE procurement from food testing laboratory networks whose combined expansion sustains above-average environmental and food safety application growth.

By End User, pharma & biotech dominate, CROs grow fastest

Pharmaceutical and biotechnology companies retained the dominant end-user position with 35.5% of the capillary electrophoresis market in 2025. The biopharmaceutical industry's systematic deployment of CE across drug discovery's pharmacokinetic sample analysis, clinical development's formulation characterisation, and commercial manufacturing's lot-release quality control creates consistent multi-phase procurement relationships whose combined value across a single drug programme's development lifecycle creates above-average per-organisation CE procurement. The regulatory requirement for validated CE methods in biologics lot-release testing creates non-discretionary instrument and consumable procurement whose pharmaceutical GMP environment sustains above-commodity pricing for quality-assured CE systems and consumables.

CROs are the fastest-growing end user because the pharmaceutical industry's progressive outsourcing of analytical method development, biopharmaceutical characterisation, and quality control testing to specialist analytical CROs creates concentrated CE procurement at organisations whose multiple concurrent client programmes create above-average aggregate CE utilisation. Each CRO that establishes CE characterisation capability for biologics clients creates instrument and consumable procurement whose commercial scale compounds with the CRO sector's expanding share of outsourced pharmaceutical analytical testing.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Capillary Electrophoresis Market Insights

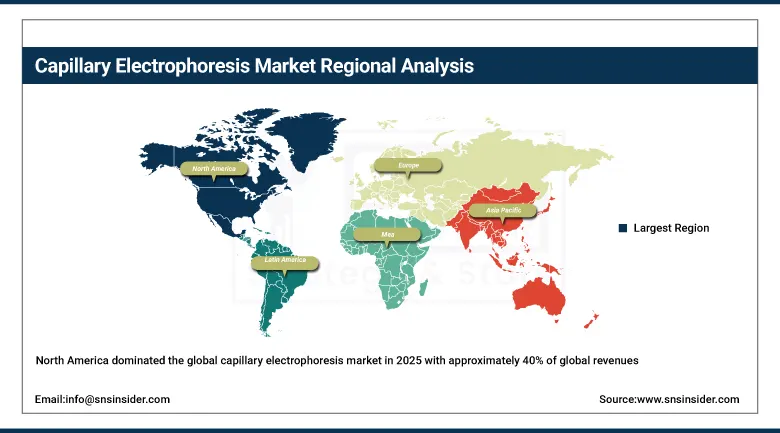

North America dominated the global capillary electrophoresis market in 2025 with approximately 40% of global revenues. The United States accounts for approximately 87.4% of North American revenues through its combination of strong healthcare infrastructure, substantial investment in research and development, the presence of Agilent Technologies, Thermo Fisher Scientific, SCIEX, and Beckman Coulter, and the NIH's USD 45 billion research budget that sustains academic CE procurement.

Canada contributes approximately 12.6% of North American revenues through its university genomic research programmes in Toronto and Vancouver, the pharmaceutical industry's analytical laboratory investment, and the National Research Council's life sciences programme whose CE method applications sustain consistent procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Capillary Electrophoresis Market Insights

Europe is a technically sophisticated capillary electrophoresis market where the European Pharmacopoeia's CE method monographs, EMA's biologics characterisation regulatory expectations, and the pharmaceutical industry's analytical chemistry investment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its pharmaceutical industry's CE quality control, the chemical industry's analytical laboratory, and Analytik Jena's domestic market presence.

The United Kingdom and France are significant secondary markets where the NHS's clinical CE laboratory investment, the pharmaceutical industry's analytical method development, and university research programmes create consistent CE procurement. EU pesticide residue monitoring regulation creates growing environmental testing CE procurement across European food safety laboratory networks.

Asia Pacific Capillary Electrophoresis Market Insights

Asia Pacific is the fastest-growing regional capillary electrophoresis market, driven by the National Natural Science Foundation of China's 20% budget increase for life sciences research in 2024 to USD 3.5 billion, India's expanding pharmaceutical analytical laboratory infrastructure, Japan's advanced pharmaceutical manufacturing CE adoption, and South Korea's biosimilar industry's analytical characterisation investment. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary biotechnology research investment, the domestic pharmaceutical industry's growing quality control infrastructure, and the government genomics programme's CE procurement.

India's rapidly growing pharmaceutical manufacturing sector's quality control laboratory investment, South Korea's Samsung Biologics and Celltrion's CE characterisation capability, and Japan's established pharmaceutical industry CE adoption create significant secondary markets whose combined procurement reinforces Asia Pacific's fastest-growing regional status.

MEA & Latin America Capillary Electrophoresis Market Insights

UAE leads MEA revenues at approximately 38.4% through its biomedical research investment, the advanced hospital sector's clinical laboratory CE adoption, and the growing pharmaceutical manufacturing sector's analytical quality control infrastructure. Brazil leads Latin American revenues at approximately 44.2% through its pharmaceutical manufacturing industry's analytical laboratory, ANVISA's analytical method requirements, and university research programmes' CE adoption.

Saudi Arabia's King Abdullah University of Science and Technology's analytical research and South Africa's academic pharmaceutical analytical chemistry create significant MEA secondary markets whose CE procurement reflects growing life sciences research investment.

Market Dynamics:

Growth Drivers: Biopharmaceutical lot-release regulatory requirement and genomics research funding creating systematic CE demand

Biopharmaceutical lot-release testing's CE regulatory requirement is the capillary electrophoresis market's most commercially certain structural growth driver. ICH Q6B's requirement for charge heterogeneity assessment of therapeutic proteins, the FDA's expectation of CE-based isoelectric point measurement for biologics applications, and the European Pharmacopoeia's CE method monographs for pharmaceutical quality testing collectively create non-discretionary CE procurement across the biopharmaceutical industry's commercial manufacturing facilities. Each biopharmaceutical facility that implements CE-based lot-release creates multi-instrument installation procurement whose consumable consumption sustains long-duration commercial relationships.

Genomics research funding's extraordinary growth through NIH, ERC, and national research council investments sustains consistent academic and research institute CE procurement for DNA fragment analysis, sequencing library QC, and forensic DNA typing. Each government research programme that specifies multi-capillary CE for genetic analysis creates instrument procurement whose capillary consumable consumption sustains recurring revenue across the funded programme's duration.

Restraints: Limited availability of skilled CE operators and competition from alternative analytical platforms

Skilled CE operator scarcity creates adoption barriers in laboratories whose analytical chemistry staffing cannot accommodate the method development, troubleshooting, and data interpretation expertise that CE's technical complexity requires. Each laboratory that adopts CE without adequate operator training creates underperformance risk whose practical impact on adoption decisions delays CE implementation beyond technology readiness.

Competition from alternative analytical platforms including high-performance liquid chromatography, mass spectrometry, and gel electrophoresis creates specification competition in applications where multiple techniques can satisfy the analytical requirement. Each analytical laboratory's equipment capital budget constrained choice between CE and HPLC creates adoption competition whose commercial outcome depends on demonstrating CE's specific performance advantages that justify investment alongside existing analytical infrastructure.

Opportunities: CE-MS hyphenation and biosimilar analytical characterisation market expansion

CE-MS hyphenation represents the most commercially premium technology direction whose mass spectrometric detection creates qualitative analytical capability beyond standalone CE's UV and fluorescence detection. Each CE-MS system installation creates instrument procurement that combines CE's separation resolution with mass spectrometry's molecular identification, creating a premium analytical tool whose pharmaceutical proteomics, metabolomics, and impurity characterisation applications command above-standard pricing.

Biosimilar analytical characterisation represents the most commercially certain near-term growth opportunity. Each biosimilar IND application requires analytical similarity data demonstrating comparable charge variant profile, purity, and molecular characteristics to the reference biologic, creating CIEF, CZE, and CGE procurement that compounds with the extraordinary biosimilar pipeline's regulatory submission activity globally.

Recent Developments:

-

2024: Agilent Technologies introduced dynamically coated capillaries in 2024 to enhance separation efficiency and reproducibility, reducing protein adsorption in biopharmaceutical analysis and improving CE performance for biologics characterisation workflows.

-

2025: A leading U.S. research consortium received major federal funding in 2025 to integrate advanced CE systems into personalised medicine and genomics programmes, supporting multi-capillary CE deployment for large-scale DNA fragment analysis and NGS library quality assessment.

-

2024: Lumex Instruments expanded its CE instrument portfolio with new automated capillary electrophoresis systems for pharmaceutical quality control in 2024, targeting biopharmaceutical lot-release testing laboratories requiring validated, 21 CFR Part 11-compliant CE data management systems.

Capillary Electrophoresis Market Key Players:

-

Agilent Technologies Inc.

-

Thermo Fisher Scientific Inc.

-

SCIEX (Danaher)

-

Bio-Rad Laboratories Inc.

-

Beckman Coulter Inc. (Danaher)

-

PerkinElmer Inc.

-

Shimadzu Corporation

-

Hitachi High-Tech Corporation

-

Lumex Instruments

-

Analytik Jena GmbH

-

Harvard Bioscience

-

Helena Laboratories

-

Sebia

-

Tosoh Corporation

-

Analis Group

-

LECO Corporation

-

Cambrex Corporation

-

Anton Paar GmbH

-

Promega Corporation

-

Sievers Instruments

Capillary Electrophoresis Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 393.29 Million |

| Market Size by 2035 | USD 733.31 Million |

| CAGR | CAGR of 5.38% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Instruments/Systems, Consumables/Reagents & Capillaries, Software & Services) • by Mode (Capillary Zone Electrophoresis/CZE, Capillary Gel Electrophoresis/CGE, Capillary Isoelectric Focusing/CIEF, Micellar Electrokinetic Capillary Chromatography/MEKC, Others) • by Application (Nucleic Acid Analysis/DNA Sequencing, Protein & Peptide Analysis, Drug Discovery & Pharmaceutical Quality Control, Environmental & Food Safety Testing, Clinical Diagnostics, Others) • by End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Clinical Laboratories, Contract Research Organizations/CROs, Environmental & Food Testing Laboratories) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Agilent Technologies Inc., Thermo Fisher Scientific Inc., SCIEX (Danaher), Bio-Rad Laboratories Inc., Beckman Coulter Inc. (Danaher), PerkinElmer Inc., Shimadzu Corporation, Hitachi High-Tech Corporation, Lumex Instruments, Analytik Jena GmbH, Harvard Bioscience, Helena Laboratories, Sebia, Tosoh Corporation, Analis Group, LECO Corporation, Cambrex Corporation, Anton Paar GmbH, Promega Corporation, Sievers Instruments |

Frequently Asked Questions

The Capillary Electrophoresis Market is expected to grow at a CAGR of 5.38% from 2026 to 2035.

The Capillary Electrophoresis Market was valued at USD 393.29 Million in 2025.

Biopharmaceutical lot-release testing's regulatory requirement for CE-based charge variant profiling and genomics research funding sustaining consistent academic CE procurement for DNA fragment analysis and sequencing applications.

Consumables dominated the Capillary Electrophoresis Market with approximately 58% share in 2025, while Instruments is the fastest growing segment.

North America dominated the Capillary Electrophoresis Market with approximately 40% of global revenues in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch