Personalized Medicine Outsourcing Market Report Scope & Overview:

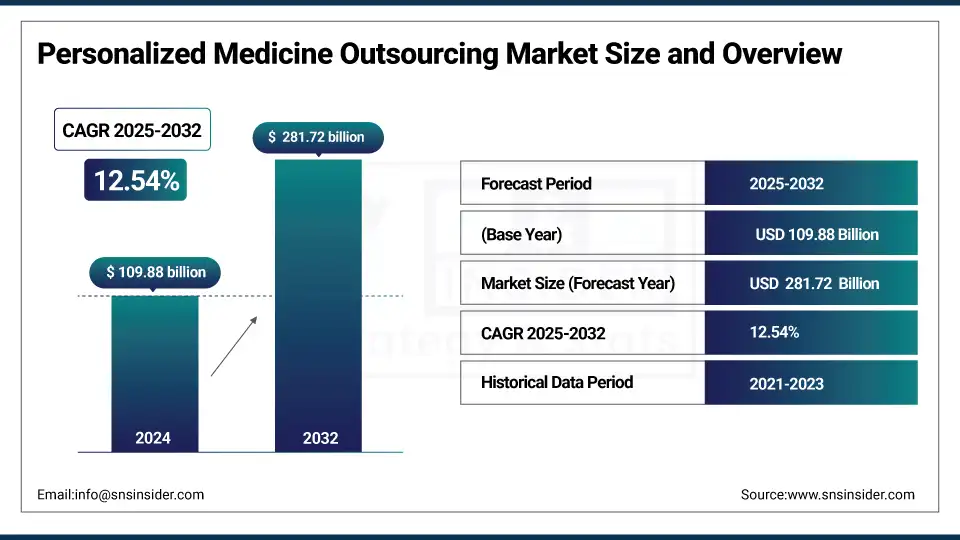

The personalized medicine outsourcing market size was valued at USD 109.88 billion in 2024 and is expected to reach USD 281.72 billion by 2032, growing at a CAGR of 12.54% over the forecast period of 2025-2032.

The global personalized medicine outsourcing market is growing rapidly as an increase in tailored therapeutic solutions, fortifying genomic research, and cost-effective outsourcing strengthens the market demand. Biopharma companies are increasingly using CROs, CDMOs, and diagnostic service providers to speed R&D and time-to-market. Rising incidence of chronic diseases and rare diseases, increasing application of companion diagnostics, and increasing adoption of AI-based analytics are also assisting in the market growth.

To Get more information On Personalized Medicine Outsourcing Market - Request Free Sample Report

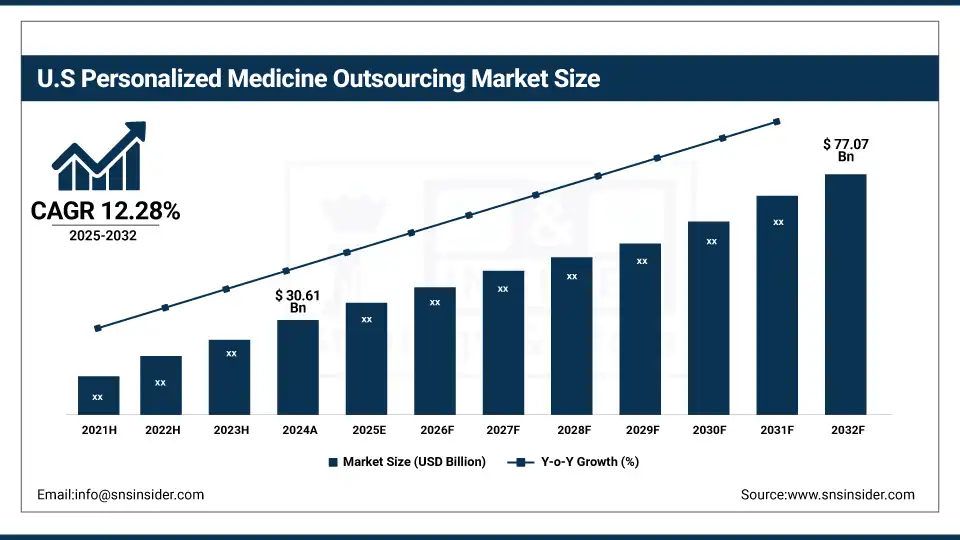

The U.S. personalized medicine outsourcing market size was valued at USD 30.61 billion in 2024 and is expected to reach USD 77.07 billion by 2032, growing at a CAGR of 12.28% over the forecast period of 2025-2032.

North America leads the personalized medicine outsourcing market, with the U.S. leading the charge given its well-established healthcare system, large budgets towards research & development, and the rising prevalence of precision medicine itself in the country. Moreover, a favorable number of CROs as well as pharmaceutical companies enables a strong customization-driven market.

Market Dynamics:

Drivers

- The High Cost and Complex Nature of Personalized Medicine R&D to be Conducted In-House have accelerated the Market Growth

Personalized medicine advances technology such as genomics, bioinformatics, and molecular diagnostics. These tools require an initial investment and the building out of skilled labor. For both larger companies and especially small to mid-sized pharmaceutical and biotech firms, having these in-house capabilities is and remains cost-prohibitive. This has led to organizations increasingly seeking out outsourcing partners that already possess these capabilities. This change, especially for component developers, enables companies to reduce R&D costs, shorten time-to-market, and have access to niche technology expertise without having to build internal infrastructure.

- Increase in the Market Share is Driven by Advancements in Omics Technologies and Companion Diagnostics

Ever-advancing omics technologies—spanning genomics, proteomics, and metabolomics—have been driving the increase of personalised medicine forward. These tools enable accurate patient stratification and biomarker discovery, which is critical for therapy selection. In the same vein, companion diagnostics are essential to confirm it is safe and efficacious to administer a specific treatment to a patient with a particular genetic signature. The advanced nature of the tools often comes with a different set of infrastructure and analytical skills that many of the right businesses simply do not have yet. Thus, they depend on outsourcing partners for sample handling, biomarker validation, and diagnostic development, which in turn boosts the personalized medicine outsourcing market growth.

Restraint

- High Complexity in Developing Personalized Therapeutics is Restraining the Market from Growing

These personalized therapies require complex science, including biomarker discovery, high-throughput sequencing, tailored treatment design, and regulatory approvals for each personalized product. That complexity tends to result in longer R&D durations, greater costs, and growing reliance on advanced technologies and specialized skill sets. As noted in section R&D process innovation, for CROs or other outsourcing partners, customizing to the molecular or genomic profile of each patient can push at the boundaries of standardization or scaling each of those services. This impacts operational efficiency and may also curb the ability of smaller or diversely skilled outsourcing players from being able to compete effectively, and slow overall market growth.

Segmentation Analysis:

By Phase

The clinical phase segment accounted for the largest share of the personalized medicine outsourcing market in 2024, with a 66.41%, due to the increasing number of precision medicine clinical trials, growing patient recruitment across oncology, rare diseases, and chronic illnesses, and increasing complexity of the study designs requiring specialized outsourcing services. Clinical Research Organizations (CROs) are instrumental in conducting large-scale, multi-site clinical studies and bring a wealth of experience in regulatory affairs, biomarker validation, and companion diagnostic integration. The segment is further driven by the increased requirement for real-world data, patient-centric trial designs, and customized treatment approaches in clinical environments.

The preclinical segment is anticipated to grow at the fastest rate during the forecast period due to a surge in investment for early-stage drug discovery for personalized therapies. To reduce timelines and costs associated with development, biotech and pharma companies are outsourcing preclinical studies, which include genomics, proteomics, and in vitro/in vivo modeling. In addition, the adoption of AI-driven screening tools, which would be followed by the development of more personalized cell-based models to improve the accuracy of early-stage testing, is propelling demand for outsourcing in preclinical research.

By Application

The personalized medicine outsourcing market share in 2024 dominated the oncology segment with 55.2%, owing to the high occurrence of different cancers and associated benefits of targeted therapies. Currently, oncology is leading the way in precision medicine, with extensive biomarker-directed clinical trial pipelines and a large number of treatment decisions being guided by companion diagnostics. Due to cancer biology has become so complex, much of the clinical development, lab testing, and genomics work is outsourced by pharmaceutical and biotechnology companies focused on this specialized research. However, firm funding and regulatory support for cancer research are other factors fuelling the high share of the oncology segment in this market.

The rare diseases segment is expected to grow significantly in the forecast years, owing to the increasing emphasis on developing orphan drugs and the growing implementation of genomics and personalized treatment plans. Due to the restricted patient population and the heightened variety of rare diseases, the need for a personalized approach is heavy; this spurs an outsourcing modus operandi of sorts to facilitate quick but nimble research, clinical work, and regulatory aid. More and more investment in this area is being encouraged by enhanced incentives for orphan drug development—fast-track approvals, market exclusivity, et cetera. This is fostering the rapid growth of this application area, as more companies are leveraging outsourcing partners to deal with the associated scientific and regulatory challenges.

By Service

Due to the growing requirement for scalable production of custom-made therapeutics, particularly cell and gene therapeutics, which demand highly specialized manufacturing environments, the contract manufacturing segment occupied the largest value share of the personalized medicine outsourcing market in 2024. As infrastructure costs came to an all-time high, more advanced technologies and rigid regulatory requirements pushed several pharmaceutical and biotechnology companies to outsource manufacturing to Contract Manufacturing Organizations (CMOs). Increasing use of biologics, personalized drugs, and short production timelines made companies depend more on end-to-end CMO manufacturing solutions in the year 2024.

During the forecast years, the contract development segment is expected to experience the highest growth, as increasing personalized medicine development has become increasingly complex, and requires highly specialized capabilities that include expertise in assay development, biomarker identification, and companion diagnostic co-development. CDOs provide outsourced early-phase development activities, thereby helping companies to quickly get to market the results from the drug discovery process, and to lower their R&D expenses and technical risk. More companies are partnering with contract development organizations (CDOs) in response to the rising trend of targeted drug design for rare diseases and immunotherapy, which should contribute to strong growth in this segment.

By Type

Due to their extensive use in targeted therapies for chronic and life-threatening conditions such as cancer, autoimmune diseases, and cardiovascular disorders, the inhibitor drugs segment dominated the personalized medicine outsourcing market in 2024. Drugs that act as inhibitors (e.g., kinase and protease inhibitors) are a key component of precision medicine strategies that act with high specificity to modulate pathways that contribute to disease. To minimize time-to-market and take advantage of off-the-shelf expertise, pharmaceutical and biotechnology companies have increasingly outsourced the development and production of these drugs. Furthermore, established clinical profiles of several classes of inhibitors and the development of mature regulatory pathways have made this segment commercially viable and a standard option among many global markets.

The cell & gene therapy segment is anticipated to register fastest growth over the forecast period, owing to significant technological breakthroughs, increasing approvals from the FDA and EMA, and growing investment by pharmaceutical giants into this area. They are on the cutting edge of precision therapy and, unlike classical drugs, provide the promise of a cure from genetic and rare diseases. Demand for outsourcing is escalating quickly, as sponsors look for contract research and manufacturing partners with the requisite specialized infrastructure, regulatory knowledge, and scalable solutions to meet the demanding needs of these therapies. In addition, improvements in vector engineering, CRISPR technology, and patient-specific manufacturing are driving adoption further, making this sector an important foundation for future market growth.

Regional Analysis:

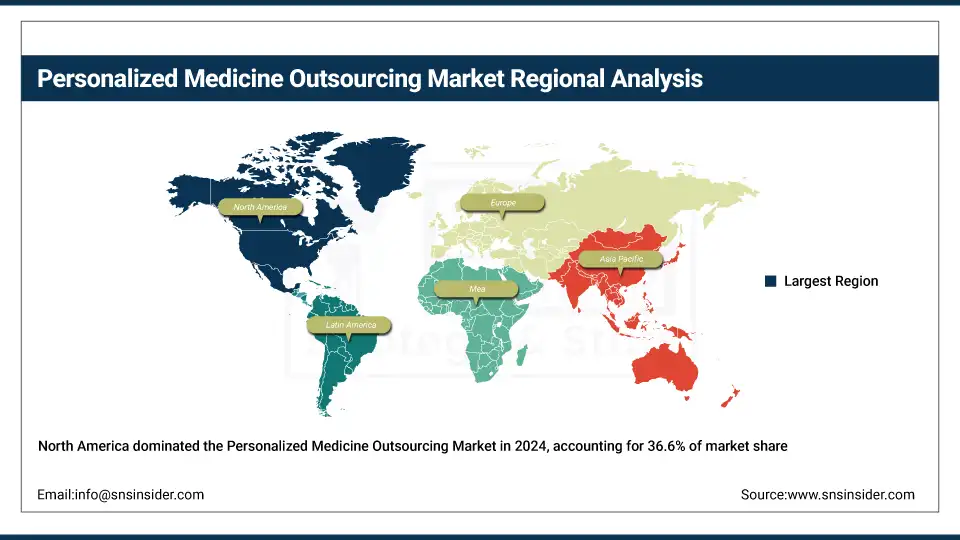

Due to the established healthcare infrastructure, vigorous regulatory frameworks, and high health expenditure, the global personalized medicine outsourcing market is primarily driven by North America, with a 36.6% market share in 2024. The region has top pharmaceutical and biotechnology firms investing billions in personalized medicine research. In addition to that, there is the availability of advanced genomic laboratories, state-of-the-art technologies, and competent personnel, which aid in the outsourcing of services such as biomarker discovery, companion diagnostics development, and bioinformatics. Increasing embrace of precision medicine strategies by healthcare providers and academic institutions is likely to contribute to the demand for outsourced services.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is projected to be the fastest-growing region in the personalized medicine outsourcing market trend due to an increase in healthcare expenditure, the increasing pharmaceutical manufacturing activities, and the increasing number of clinical trial activities. Places such as China, India, and South Korea represent low-cost third-world outsourcing areas, where highly-skilled manpower is readily available, and infrastructure is becoming more modernised. Moreover, the presence of supportive government initiatives for biotechnology and precision medicine, rising awareness for personalized therapies, and an extensive genetically diverse population further provide lucrative prospects for Asia Pacific to become an ideal location for market expansion and outsourced R&D operations.

Europe is growing significantly in the personalized medicine outsourcing market analysis owing to its solid healthcare infrastructure, strong focus on biomedical research, and a favorable regulatory regime. The developments and outsourcing of personalized med solutions are witnessing rapid investments in genomics, molecular diagnostics, and translational medicine from nations such as Germany, the UK, France, and others. In addition, the growing partnerships forged in the region across academia, biopharmaceutical companies, and commercial contracts research organizations (CROs) will continue to drive outsourcing of clinical trials and biomarker discovery.

In addition, the European Medicines Agency (EMA) has taken a proactive position in favor of embedding personalized strategies in the clinics by facilitating approval routes for personalized therapies. The rising incidences of chronic diseases & cancer in the region increase demand for customized therapy, thus resulting in the outsourcing of related services to specialized service providers in the market. Increase in uses of precision diagnostics and companion diagnostics also adds to this region being one of the major contributors to the global personalized medicine outsourcing market.

The personalized medicine outsourcing market in Latin America and the Middle East & Africa (MEA) shows moderate growth. Factors such as slow improvements in healthcare infrastructure, more awareness regarding personalized therapies, and increased emphasis on cost-effective healthcare solutions are driving the growth of the market in this region. The increase in investments made by several developing countries, including Brazil, Mexico, South Africa, and the UAE, in enhancing their healthcare infrastructure and clinical research capabilities has further boosted the outsourcing activities.

Growth is, however, limited by the lack of access to high-end technologies, regulatory complications, and the dearth of trained professionals faced by several key players in the region. However, with a greater patient pool and lower inventories, international pharmaceutical and biotechnology companies are progressively eyeing these regions for trial outsourcing and lab services, notwithstanding these obstacles. Investment and harmonization of regulations should steadily improve their share of the global personalized medicine outsourcing market for both Latin America and MEA.

Key Players:

The personalized medicine outsourcing market companies are Aurigene Pharmaceutical Services, Syngene, Syneos Health, Infosys, Parexel, Catalent, ICON, HCL Technologies, Lonza, Thermo Fisher Scientific, LabCorp, Charles River Laboratories, WuXi AppTec, PRA Health Sciences, PPD, IQVIA, Recipharm AB, Samsung Biologics, Fujifilm Diosynth, Eurofins Scientific, Bio‑Rad Laboratories, Frontage Laboratories, Svar Life Science, Sino Biological, Almac Group, SCTbio, Ology Bioservices, BioSpring, and other players.

Recent Developments:

- July 2024 – Aurigene Pharmaceutical Services, a contract research, development, and manufacturing organization (CRO/CDMO) based in India, said that it has signed an agreement to offer discovery services in cell therapy to Edity Therapeutics, an Israeli-headquartered biotechnology firm.

- July 2024 – Syngene International, a contracted research, development, and manufacturing organization (CRDMO), launched a novel protein manufacturing platform for rapid and efficient protein production. The platform combines a cell line and transposon-based technology licensed from ExcellGene, a Swiss company with expertise in developing mammalian cell lines.

Personalized Medicine Outsourcing Market Report Scope:

Report Attributes Details Market Size in 2024 USD 109.88 Billion Market Size by 2032 USD 281.72 Billion CAGR CAGR of 12.54% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Product (Clinical, Preclinical)

• By Application (Oncology, Rare Diseases, Infectious Diseases, Others)

• By Service (Contract Manufacturing, Contract Development)

• By Type (Inhibitor Drugs, Monoclonal Antibodies, Cell & Gene Therapy, Others)

• By End Use (Pharmaceutical Companies, Biotechnology Companies, Others)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles The personalized medicine outsourcing market companies are Aurigene Pharmaceutical Services, Syngene, Syneos Health, Infosys, Parexel, Catalent, ICON, HCL Technologies, Lonza, Thermo Fisher Scientific, LabCorp, Charles River Laboratories, WuXi AppTec, PRA Health Sciences, PPD, IQVIA, Recipharm AB, Samsung Biologics, Fujifilm Diosynth, Eurofins Scientific, Bio Rad Laboratories, Frontage Laboratories, Svar Life Science, Sino Biological, Almac Group, SCTbio, Ology Bioservices, BioSpring, and other players.

Frequently Asked Questions

North America dominated the personalized medicine outsourcing market in 2024.

The “clinical” segment dominated the personalized medicine outsourcing market.

The high cost and complex nature of personalized medicine R&D to be conducted in-house have accelerated the market growth.

The personalized medicine outsourcing market was USD 109.88 billion in 2024 and is expected to reach USD 281.72 billion by 2032.

The personalized medicine outsourcing market is expected to grow at a CAGR of 12.54% from 2025 to 2032.

Get in Touch