Security Analytics Market Report Scope & Overview:

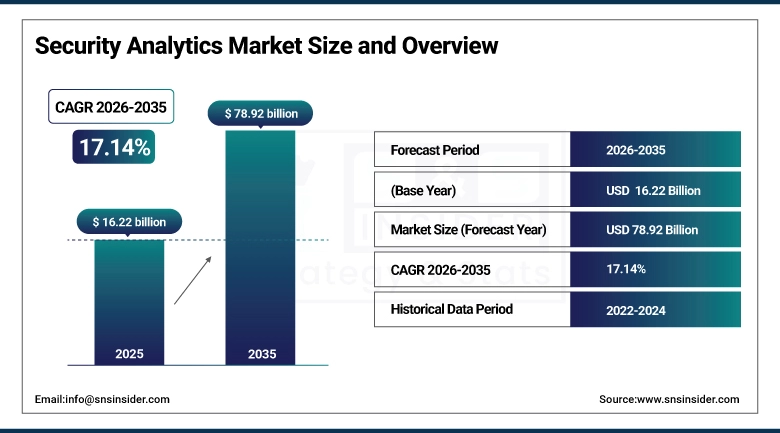

The Security Analytics Market size was valued at USD 16.22 billion in 2025 and is expected to reach USD 78.92 billion by 2035, growing at a CAGR of 17.14% over the forecast period of 2026-2035.

The global security analytics market trend is a growing demand for AI-driven threat detection platforms such as network security analytics tools, endpoint behavioral monitoring solutions, and user and entity behavior analytics (UEBA) systems as the growth of the market is driven by increasing frequency of advanced persistent threats, enterprise adoption of zero-trust security frameworks, and organizational demand for real-time visibility across hybrid IT environments. This trend is also driven by a growing integration of security information and event management (SIEM) platforms with machine learning analytics and the growing focus on proactive cyber threat intelligence as enterprises become more focused on reducing mean time to detect (MTTD) and are more willing to invest in cloud-native and on-premise security analytics infrastructure, resulting in growth in the domestic and international market for solution-based and service-based security analytics deployments.

For instance, in February 2025, growing enterprise awareness of insider threats and advanced malware campaigns drove a 27% increase in security analytics platform deployments for large organizations in North America, boosting threat detection accuracy and incident response efficiency across financial and government sectors.

Security Analytics Market Size and Forecast:

-

Market Size in 2025: USD 16.22 billion

-

Market Size by 2035: USD 78.92 billion

-

CAGR: 17.14% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Security Analytics Market - Request Free Sample Report

Security Analytics Market Trends

-

Security analytics platforms are being adopted because enterprises demand real-time threat detection, automated incident response workflows, and continuous monitoring across on-premise, cloud, and hybrid network environments.

-

Behavioral analytics and machine learning models embedded in SIEM and extended detection and response (XDR) platforms to identify anomalous user activity, lateral movement, and zero-day exploit patterns before breach escalation.

-

The development of AI-powered security operations center (SOC) automation tools, threat intelligence feeds, and open-source detection rule frameworks to improve analyst productivity and reduce alert fatigue across enterprise security teams.

-

Cloud-native security analytics deployment models, API-integrated log ingestion pipelines, and scalable data lake architectures are being adopted to support continuous telemetry collection from distributed enterprise IT environments.

-

Increased demand for managed security analytics services, co-managed SOC platforms, and threat hunting subscriptions to address internal cybersecurity talent shortages and reduce security operations overhead for mid-market organizations.

-

Collaboration between SIEM vendors, endpoint detection providers, and cloud security platform developers to build integrated security analytics ecosystems and improve detection coverage across multi-cloud and OT network environments.

-

CISA, NIST, GDPR, and SEC cybersecurity disclosure regulations promoting standards for threat detection logging, incident reporting timelines, data breach notification requirements, and security analytics audit trail retention.

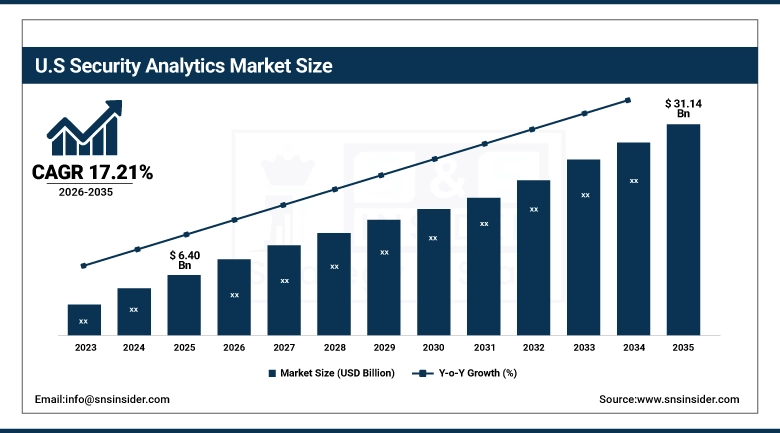

The U.S. Security Analytics Market was valued at USD 6.40 billion in 2025 and is expected to reach USD 31.14 billion by 2035, growing at a CAGR of 17.21% from 2026-2035.

The United States represents the largest market for security analytics, primarily driven by the high concentration of targeted cyberattack campaigns against critical infrastructure, stringent SEC cybersecurity disclosure requirements, and well-established enterprise cybersecurity technology procurement ecosystems. Federal mandates for zero-trust architecture adoption under Executive Order 14028, increasing BFSI sector investment in advanced threat analytics platforms, and growing cloud infrastructure security spending help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory support and swift adoption of cloud-based and on-premise security analytics solutions across large enterprise and government verticals.

Security Analytics Market Growth Drivers:

-

Rising Frequency of Advanced Cyberattacks and Zero-Trust Security Adoption is Driving the Security Analytics Market Growth

Rising frequency of advanced cyberattacks and zero-trust security adoption take the center stage as a growth driver for the security analytics market share, and are driven by the increasing volume of ransomware campaigns, supply chain compromise incidents, and nation-state threat actor activity targeting enterprise, government, and critical infrastructure networks globally. These solutions for proactive threat visibility and incident containment are driving the base of the market, the penetration of network and endpoint security analytics platforms, and adding to the overall market share globally.

For instance, in October 2024, enterprise security analytics and threat detection solutions accounted for 63% of total cybersecurity platform investment among Fortune 500 companies in the U.S., reflecting growing institutional demand for advanced detection capabilities and expanding market share.

Security Analytics Market Restraints:

-

Cybersecurity Talent Shortage and High Platform Deployment Complexity are Hampering the Security Analytics Market Growth

Cybersecurity talent shortage and high platform deployment complexity also restrict the security analytics market growth, as a large number of mid-sized enterprises and public sector organizations who have invested in security analytics licenses remain underutilizing platform capabilities or face difficulties configuring detection rules, integrating log sources, and tuning behavioral models without skilled SOC analyst teams. This might lead to poor threat detection outcomes, high false-positive alert volumes, and reduced return on security investment for organizations that lack dedicated analytics engineering resources. As a result, platform adoption stalls below intended capability thresholds, and market growth is stunted in regions where trained cybersecurity analyst talent and managed security service provider ecosystems remain underdeveloped.

Security Analytics Market Opportunities:

-

AI-Powered Threat Intelligence and Managed Security Analytics Services Drive Future Growth Opportunities for the Security Analytics Market

The opportunity in the AI-powered threat intelligence and managed security analytics services in the security analytics market is in the form of automated threat hunting workflows, predictive attack surface monitoring, and AI-generated incident investigation playbooks. These solutions provide for early detection of lateral movement in enterprise networks, individualized threat prioritization recommendations by vertical and risk profile, and real-time behavioral anomaly correlation across endpoint, cloud, and identity data sources. Through enhanced SOC efficiency, analyst workload reduction, and operational cost optimization, particularly in areas with growing SME cybersecurity compliance requirements, these technologies may improve breach prevention rates, decrease mean time to respond (MTTR), and expand the market.

For instance, in June 2024, industry research reported that 68% of enterprise security teams using AI-integrated analytics platforms reduced their mean time to detect threats by over 40%, highlighting growing demand for intelligent automation in security operations and increasing adoption of managed analytics service models.

Security Analytics Market Segment Analysis

-

By Component, solutions held the largest share of around 64.37% in 2025, and the services segment is expected to register the highest growth with a CAGR of 18.42%.

-

By Organization size, large enterprises dominated the market with approximately 67.18% share in 2025, while the SMEs segment is expected to register the highest growth with a CAGR of 19.56%.

-

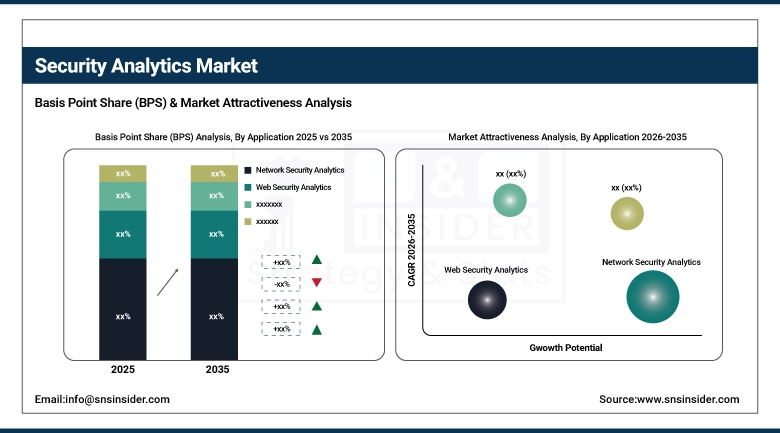

By Application, network security analytics accounted for the leading share of nearly 31.24% in 2025, and the endpoint security analytics segment is expected to register the highest growth with a CAGR of 18.93%.

-

By Vertical, BFSI accounted for the leading share of about 24.46% in 2025, and the healthcare segment is expected to register the highest growth with a CAGR of 19.28%.

By Application, Network Security Analytics Leads, and Endpoint Security Analytics Registers Fastest Growth

The network security analytics segment accounted for the largest share of the security analytics market with about 31.24%, owing to the foundational role of network traffic analysis in enterprise threat detection, the widespread deployment of intrusion detection systems and network behavioral analytics tools across data center and perimeter security architectures, and strong demand from BFSI, government, and telecom verticals for network-layer threat visibility. Reasons driving the network security analytics segment include increasing east-west traffic monitoring requirements in multi-cloud environments and growing adoption of network detection and response platforms. In addition, the endpoint security analytics segment is slated to grow at the fastest rate with a CAGR of around 18.93% throughout the forecast period of 2026–2035, as enterprises, government agencies, and healthcare organizations seek comprehensive endpoint behavioral monitoring platforms, ransomware execution detection capabilities, and identity-linked endpoint telemetry correlation for insider threat investigations. Increased focus on remote workforce device security and bring-your-own-device (BYOD) policy enforcement contribute to adoption, while improving EDR-to-XDR platform integration drives continued investment.

By Component, Solutions Lead the Market, While Services Registers Fastest Growth

The solutions segment accounted for the highest revenue share of approximately 64.37% in 2025, owing to strong enterprise preference for deploying owned SIEM, UEBA, and network detection and response (NDR) platforms, the integration flexibility of on-premise and cloud-hosted analytics software, and high upfront investment by large enterprises in security operations technology infrastructure. Emerging trends, including increasing adoption of XDR platforms and integrated security analytics suites with native AI detection capabilities, are sustaining solution segment dominance across new enterprise procurement cycles. In comparison, the services segment is anticipated to achieve the highest CAGR of nearly 18.42% during the 2026–2035 period, driven by the increasing demand for managed detection and response (MDR) services, co-managed SOC offerings, and security analytics implementation and tuning support from mid-market organizations lacking in-house cybersecurity expertise. Drivers include rising adoption of security-as-a-service consumption models and the preference for outcome-based managed analytics engagements over capital-intensive platform ownership.

By Organization Size, Large Enterprises Dominate, while SMEs Segment Registers Fastest Growth

By 2025, the large enterprises segment contributed the largest revenue share of 67.18% due to higher cybersecurity budget allocations, established security operations center infrastructure, and regulatory compliance obligations under GDPR, SOX, HIPAA, and SEC disclosure rules that mandate continuous threat monitoring and audit-ready detection logging. Growing adoption of enterprise-wide zero-trust frameworks and increasing integration of security analytics with IT service management and governance platforms are making large organizations increasingly aware of analytics-driven security posture improvement. The SMEs segment is projected to grow at the highest CAGR of about 19.56% between 2026 and 2035 due to the growing exposure of smaller businesses to ransomware and phishing campaigns, expanding availability of affordable cloud-native security analytics tools, and increasing cyber insurance requirements mandating active threat monitoring programs. Some of the reasons include better accessibility of managed analytics services for SMEs, improved pricing models for small business security tiers, and growing government grant programs supporting SME cybersecurity investment.

By Vertical, BFSI Leads, and Healthcare Registers Fastest Growth

The BFSI segment accounted for the highest revenue share of approximately 24.46% in 2025, owing to the high-value data assets of financial institutions, stringent PCI-DSS and SOX compliance obligations requiring continuous threat analytics logging, and strong investment capacity of banks, insurance companies, and capital markets firms in advanced security operations platforms. Emerging trends, including increasing adoption of fraud detection analytics integrated with transaction monitoring systems, are reinforcing BFSI’s market-leading vertical position through the near-term forecast period. In comparison, the healthcare segment is anticipated to achieve the highest CAGR of nearly 19.28% during the 2026–2035 period, driven by the increasing targeting of hospital networks and electronic health record systems by ransomware operators, HIPAA breach notification enforcement actions, and growing investment in medical device network security analytics across large health system IT programs. Drivers include rising telehealth platform security requirements and expanding HHS cybersecurity guidance for healthcare sector threat detection and incident response.

Security Analytics Market Regional Highlights:

North America Security Analytics Market Insights:

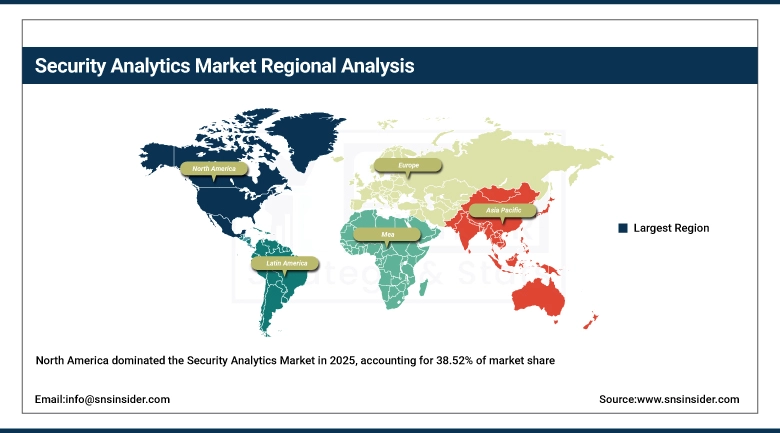

North America held the largest revenue share of over 38.52% in 2025 of the security analytics market due to an established enterprise cybersecurity procurement ecosystem, stringent federal and state-level data breach notification and cybersecurity disclosure regulations, and increased organizational awareness of the financial and reputational consequences of undetected cyber intrusions. Drivers include widespread SIEM platform adoption across Fortune 1000 enterprises, an improved managed security service provider market, growing zero-trust architecture mandate compliance, and greater acceptance of AI-driven threat detection following high-profile ransomware and supply chain attack incidents. At the same time, various federal cybersecurity executive orders, CISA threat advisory programs, and substantial enterprise investment in security operations center modernization are anchoring security analytics software and services in the market, and ensuring multibillion dollar revenues across domestic and cross-border enterprise security programs.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Security Analytics Market Insights:

Asia Pacific is the fastest-growing region in the security analytics market with a CAGR of 18.76%, as the awareness about enterprise cybersecurity threats, government-mandated data protection regulations, and digital infrastructure security investment in China, India, Japan, and Southeast Asian economies is growing. Factors including India’s expanding IT services sector cybersecurity compliance requirements, Japan’s Critical Infrastructure Protection framework modernization, and China’s Cybersecurity Law enforcement across industries are stimulating the market growth. National cybersecurity agency-led threat intelligence sharing programs and government-funded SOC development initiatives have been instrumental in improving enterprise-level security analytics adoption, especially in banking and telecommunications sectors. Public-private cybersecurity partnership programs and growing regional managed security service provider networks also help in advancing threat detection coverage and security analytics platform deployment. Increase in demand in Asia Pacific owing to rising enterprise cybersecurity budget allocations against historical spending levels and growing availability of cloud-native analytics platforms localized for regional compliance requirements.

Europe Security Analytics Market Insights:

The security analytics market in Europe is the second-dominating region after North America on account of GDPR breach notification obligations requiring active threat monitoring and audit-ready detection logging, NIS2 Directive compliance mandates for critical infrastructure security analytics adoption, and increasing enterprise security investment across financial services, healthcare, and government verticals in Germany, France, and the UK. Rising implementation of national cybersecurity agency threat intelligence platforms, advanced SOC maturity programs, favorable EU Cybersecurity Act funding for threat analytics research, and cross-border incident response coordination frameworks are also contributing to the sustained growth of the market in leading European economies.

Latin America (LATAM) and Middle East & Africa (MEA) Security Analytics Market Insights:

In Latin America, and Middle East & Africa, the growing enterprise digitization efforts and increase in internet connectivity with expanding cloud infrastructure adoption support the security analytics market growth. The rising awareness of ransomware threats targeting financial and government organizations and growing availability of affordable managed security analytics services, along with national cybersecurity strategy investments, will aid threat detection accessibility and security analytics platform adoption. The increasing enterprise IT modernization programs and improving regional managed security service provider availability in these regions are continuing to encourage market growth.

Security Analytics Market Competitive Landscape:

IBM Corporation (est. 1911) is a leading enterprise cybersecurity technology provider that focuses on AI-driven security analytics, SIEM platform development, and managed threat detection services for hybrid cloud and on-premise enterprise environments. It uses its QRadar SIEM platform and threat intelligence network to produce integrated security analytics workflows, with seamless integration across endpoint, network, and cloud security data sources.

-

In March 2025, launched QRadar Suite enhancements incorporating generative AI-powered threat investigation capabilities, enabling SOC analysts to accelerate incident triage, reduce investigation time by an average of 55%, and automate threat hunting playbooks across enterprise security operations deployments.

Microsoft Corporation (est. 1975) is a well-known global enterprise technology and cloud security platform provider focused on integrated security analytics, extended detection and response (XDR), and cloud-native SIEM solutions through its Microsoft Sentinel and Defender platforms. It invests in AI-driven threat intelligence correlation and automated incident response workflows with the hopes of revolutionizing enterprise security operations by delivering unified analytics visibility across identity, endpoint, cloud, and network security data at global scale.

-

In November 2024, expanded Microsoft Sentinel with new AI-powered threat hunting agents and natural language investigation capabilities, enabling security teams to conduct complex multi-source threat correlation queries without requiring advanced KQL query expertise across hybrid enterprise environments.

Splunk Inc. (Cisco) (est. 2003) is a leading data analytics and security intelligence platform provider in the fields of SIEM, observability, and enterprise threat detection solutions. The company’s security analytics product portfolio focuses on machine learning-based anomaly detection and high-speed log ingestion performance, and features a strong commitment to open detection framework integration and continuous platform innovation to complement its growing market presence in both large enterprise and mid-market security operations programs.

-

In January 2025, introduced Splunk Enterprise Security 8.0 with unified attack surface risk scoring and AI-assisted detection rule recommendations, strengthening threat prioritization capabilities and expanding adoption among large enterprise SOC teams managing high-volume multi-cloud security telemetry environments.

Security Analytics Market Key Players:

-

IBM Corporation

-

Splunk Inc. (Cisco)

-

Palo Alto Networks, Inc.

-

CrowdStrike Holdings, Inc.

-

Securonix, Inc.

-

Exabeam, Inc.

-

LogRhythm, Inc.

-

Rapid7, Inc.

-

Fortinet, Inc.

-

RSA Security LLC

-

Varonis Systems, Inc.

-

Elastic N.V.

-

Sumo Logic, Inc.

-

Trellix (Symphony Technology Group)

-

Gurucul Solutions LLC

-

Google LLC (Chronicle Security)

-

Amazon Web Services, Inc. (AWS Security Hub)

-

Darktrace Holdings Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.22 Billion |

| Market Size by 2035 | USD 78.92 Billion |

| CAGR | CAGR of 17.14% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component, (Solutions, Services) •By Organization Size, (Large enterprises, SMEs) •By Application, (Web Security Analytics, Network Security Analytics, Endpoint Security Analytics, Application Security Analytics, Others) •By Vertical, (BFSI, Telecom & IT, Retail, Healthcare, Government & Defense, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | IBM Corporation, Microsoft Corporation, Splunk Inc. (Cisco), Palo Alto Networks, Inc., CrowdStrike Holdings, Inc., Securonix, Inc., Exabeam, Inc., LogRhythm, Inc., Rapid7, Inc., SolarWinds Corporation, Fortinet, Inc., RSA Security LLC, Varonis Systems, Inc., Elastic N.V., Sumo Logic, Inc., Trellix (Symphony Technology Group), Gurucul Solutions LLC, Google LLC (Chronicle Security), Amazon Web Services, Inc. (AWS Security Hub), Darktrace Holdings Limited, and Others. |

Frequently Asked Questions

Ans: North America dominated the Security Analytics Market in 2025 with a 38.52% market share.

Ans: By component (type), the Solutions segment dominated the Security Analytics Market with a 64.37% revenue share in 2025.

Ans: The major growth factor is the widespread integration of AI and Machine Learning for proactive threat detection and predictive analysis, enabling real-time monitoring and smarter incident response.

Ans: The Security Analytics Market size was valued at USD 16.22 billion in 2025.

Ans: The Security Analytics Market is expected to grow at a CAGR of 17.14% from 2026 to 2035.

Get in Touch