Centrifuge Market Report Scope & Overview:

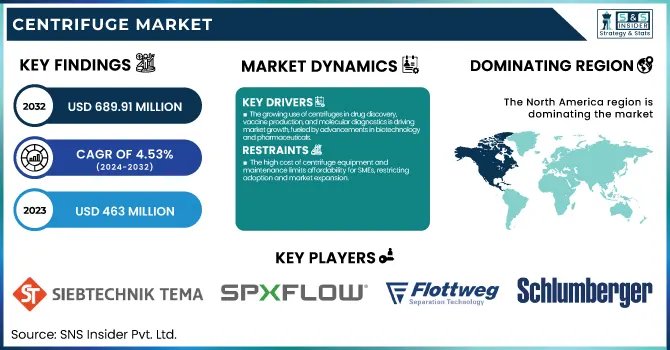

The Centrifuge Market Size was estimated at USD 463 million in 2023 and is expected to arrive at USD 689.91 million by 2032 with a growing CAGR of 4.53% over the forecast period 2024-2032.

This report offers a unique perspective on the Centrifuge Market by analyzing manufacturing output trends and regional utilization rates, highlighting efficiency levels across key markets. It examines maintenance and downtime metrics, providing insights into operational challenges and cost implications. The study also evaluates technological adoption rates by region, showcasing innovations such as automation and IoT integration in centrifuge systems. Additionally, it presents export/import data, revealing trade dynamics and supply chain shifts. To enhance insights, the report includes sustainability adoption trends, focusing on energy-efficient centrifuges and regulatory impacts shaping market demand.

Centrifuge Market Size and Forecast

-

Market Size in 2023: USD 463 Million

-

Market Size by 2032: USD 689.91 Million

-

CAGR: 4.53% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2023

To Get more information on Centrifuge Market - Request Free Sample Report

Centrifuge Market Trends

-

Growing demand in biopharmaceuticals and clinical diagnostics is driving centrifuge adoption, with the life sciences sector accounting for over 55% of total demand.

-

Increasing R&D investments in drug development and genomics are boosting usage, with global biotech R&D spending growing at 8–10% annually.

-

Rising need for high-speed and ultra-centrifuges is improving processing efficiency, reducing sample separation time by 20–30%.

-

Expansion of food, environmental, and industrial testing is supporting market growth, contributing to over 25% of centrifuge applications.

-

Technological advancements such as automation and digital control systems are enhancing operational efficiency, with automated centrifuges improving workflow productivity by 15–20%.

The U.S. Centrifuge Market is projected to grow steadily, with a CAGR of 4.14% from 2023 to 2032. The market size is expected to increase from 154.83 million in 2023 to 223.04 million by 2032, driven by advancements in biotechnology, pharmaceuticals, and industrial applications. The rising adoption of automated and energy-efficient centrifuge systems is enhancing operational efficiency across various sectors. Additionally, stringent regulatory standards and increasing demand for high-performance separation technologies in healthcare and research facilities are further fueling growth. With consistent investments in technological innovation and a strong manufacturing base, the U.S. remains a dominant player in the global centrifuge industry.

Centrifuge Market Dynamics

Drivers

-

The growing use of centrifuges in drug discovery, vaccine production, and molecular diagnostics is driving market growth, fueled by advancements in biotechnology and pharmaceuticals.

The centrifuge market is witnessing significant growth, driven by increasing demand in biotechnology and pharmaceuticals. Centrifuges are essential for drug discovery, vaccine development, and molecular diagnostics, as they allow for processes such as cell separation, protein purification, and genetic evaluation. In addition, the increasing prevalence of personalized medicine, regenerative therapies, and cell-based research are also expected to drive the market demand. Innovations like accelerated ultracentrifuges, automation, and intelligent observation, are optimizing effectiveness. Advancement of bioprocessing and increase in gene therapy and monoclonal antibody production has extended the reach of centrifuge applications. North America and Europe account for most of the market share because of extensive investment in R&D, while Asia-Pacific remains the promising growth region because of the growth of the pharmaceutical and biotechnology sectors. On the whole, a rise in healthcare innovation would spur the ongoing market growth.

Restraint

-

The high cost of centrifuge equipment and maintenance limits affordability for SMEs, restricting adoption and market expansion.

Centrifuge equipment requires a high initial investment, making it a significant financial burden for small and medium enterprises (SMEs). Advanced centrifuge systems, particularly high-speed and industrial grade systems, and also typically have expensive components, smart automation and precision engineering, all pushing up the costs. You are also expected to incur maintenance costs, where servicing, calibration, and regular parts replacement like rotors, seals, and bearings are required to keep your aircraft flying efficiently and for long. They often require specialized technicians for upkeep, significantly increasing operational costs. Industrial centrifuge energy consumption builds additional operating costs. These high costs limit adoption for the SMEs with smaller budgets; thus they have to seek out alternative separation technologies such as filtration or sedimentation. Manufacturers are also working to deliver energy-efficient designs, leasing options, modular systems, and a lower product entry point to make centrifuge solutions more cost-effective and accessible for smaller businesses. Nevertheless, affordability continues to be an obstacle to expansion of market penetration.

Opportunities

-

The integration of IoT and AI in centrifuges enables real-time monitoring, automation, and predictive maintenance, enhancing efficiency and reducing downtime.

The integration of IoT and AI in centrifuge technology is transforming the market by enhancing efficiency, precision, and automation. IoT based smart site centrifuges allow real-time monitoring, predictive maintenance, and remote operation by allowing customers to run the equipment with less downtime and operational cost. Using AI-driven algorithms, it can analyze performance data to optimize speed, balance, and energy consumption, thereby harmonizing productivity and extending the equipment lifespan. Such innovations are of notable significance in the field of healthcare, pharmaceuticals as well as industrial applications, where precise separation along with stringent contamination control is critical. Cloud-based connectivity enables ice to be easily integrated with LIS (laboratory information systems) and ICS (industrial control systems) for making data-driven decisions. Moreover, AI tools in diagnostics can identify abnormality before a failure takes place and prevent the disruption to a minimum level. The ongoing transition to Industry 4.0 will fuel the demand for automated and intelligent centrifuge, boosting research, diagnostics and manufacturing. As the world becomes more data-driven and automated, companies that invest in smart centrifuge technology will find a competitive edge.

Challenges

-

Fluctuations in raw material costs and supply chain disruptions impact centrifuge manufacturing, leading to higher costs, delays, and pricing challenges.

Supply chain disruptions and fluctuating raw material costs pose significant challenges in the centrifuge market. Their availability and price are the two most critical factors affecting the cost and timeline of production. Material shortages are worsened by the supply chain bottlenecks, geopolitical tensions, adverse trading conditions, leading to product delivery delays. Moreover, increasing energy and inflation rates lead to a rise in procurement and ultimately force manufacturers to change pricing strategies. It also makes the market susceptible to logistics disruptions and transportation delays since the critical electronic components and casesupply chain, as well as bearings, have become increasingly dependent on global suppliers. Companies are turning away from single place sourcing, alliances and using other materials particular to regions as a risk management compensation. Short-term cost volatility remains a crippling issue because such solutions require enormous investments and longer timelines. With the rising demand for centrifuges in sectors such as biotechnology and wastewater treatment, manufacturers must embrace flexible supply chain strategies to ensure consistent production and pricing.

Centrifuge Market Segmentation Analysis

By Type

The Decanters region dominated with a market share of over 54% in 2023, due to their extensive use across wastewater treatment, chemical processing, and food & beverage industries. These centrifuges are ideal for the separation of solids from liquids – in high-capacity and in continuous mode. Decanter centrifuges play a vital role in wastewater treatment to eliminate sludge and treat solids, ultimately increasing efficiency and decreasing disposal costs. They are used in the chemical industry for separating chemical compounds and purifying products. In most foods & beverages the decanter is utilized in juice clarification, edible oil extraction, or dairy. Although they are straightforward machines, their ability to handle many kinds of materials, coupled with robust design and little maintenance required make them the prevailing centrifuge type on the market.

By Drilling & Excavation Activity

The Horizontal Directional Drilling (HDD) segment is the second-largest in the Centrifuge Market, driven by its increasing adoption in oil & gas, telecommunications, and infrastructure projects. Horizontal Directional Drilling (HDD) is a trenchless method widely used to install underground pipelines, cables, and conduits with little surface damage. The market demand for this segment is expected to be high due to their uses in separating the drilling fluid, improving the performance and minimize the operational cost. The segment also benefits from the rising expansion of renewable energy projects, including geothermal drilling. This steady growth of HDD is driven by the advancement in drilling technology, along with the growing pipeline network across the globe, making it one of the most significant segments in the centrifuge market.

By Application

The solids control segment dominated with a market share of over 38% in 2023, due to its critical role in drilling operations, particularly in the oil and gas industry. Centrifuges in solids control separate drilling mud from the cuttings well and help retrieve precious drilling fluids while also ensuring that the operations are most efficient. This streamlines waste generation and meets stringent regulatory environmental standards. At a time when sustainability is becoming more important, companies have started to implement solids control systems to reduce their disposal costs and enhance resource use. Moreover, the increasing demand for energy and technological innovations in the drilling sector are also contributing to the growth of the market.

Centrifuge Market Regional Outlook

North America region dominated with a market share of over 44% in 2023, due to the presence of well-established healthcare infrastructure, significant investments in research and development (R&D), and the presence of key industry players. Advanced biotech and pharmaceutical industries that depend on centrifuges for applications such as drug development, diagnostics, and clinical research are in the area. The increase in adoption of advanced laboratory technologies and high regulatory standards accelerates the growth of high-performance centrifugation equipment. Industrial applications such as wastewater treatment, food processing, and others are expected to contribute to the growth of the market. North America dominates the market with the presence of leading manufacturers and ongoing technological developments, and investments in innovation and automation continue to ensure its place at the forefront of the global centrifuge market.

Asia-Pacific is the fastest-growing region in the centrifuge market, driven by rapid industrialization and advancements in biotechnology and pharmaceutical industries. The growing healthcare industry in the region, driven by growing healthcare expenditure and government initiatives, has considerably increased the demand for centrifuges to be used in medical diagnostics and research applications. Countries such as China, India, and Japan are seen investing significantly in life sciences, drug discovery and clinical research thereby leading to an addition in the growth of the market. The expansion of the food and beverage industry and rising environmental concerns have further accelerated the use of centrifuge for wastewater treatment and quality control processes. Asia-Pacific is likely to continue its rapid growth in the coming years due to the continuous technological development and increasing manufacturing activities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Siebtechnik Tema GmbH (Screen Scroll Centrifuges, Pusher Centrifuges)

-

SPX Flow Inc. (Industrial Decanter Centrifuges, Disc Stack Centrifuges)

-

Flottweg SE (Decanter Centrifuges, Tricanter® Centrifuges)

-

Schlumberger Limited (Oilfield Decanter Centrifuges, Solids Control Centrifuges)

-

Ferrum Ltd. (Peeler Centrifuges, Pusher Centrifuges)

-

Mitsubishi Kakoki Kaisha Ltd. (Disc Stack Centrifuges, Industrial Clarifiers)

-

FLSmidth (Solid Bowl Decanter Centrifuges, Horizontal Centrifuges)

-

GEA Group AG (Separator Centrifuges, Dairy Centrifuges)

-

Alfa Laval (Disc Stack Centrifuges, Industrial Separators)

-

Andritz (Decanter Centrifuges, Pusher Centrifuges)

-

Thermo Fisher Scientific Inc. (Laboratory Centrifuges, High-Speed Centrifuges)

-

Beckman Coulter Inc. (Ultracentrifuges, Benchtop Centrifuges)

-

Eppendorf AG (Microcentrifuges, Clinical Centrifuges)

-

Hettich Instruments (Blood Separation Centrifuges, Research Centrifuges)

-

Becton, Dickinson and Company (BD) (Hematology Centrifuges, Plasma Separation Centrifuges)

-

Kubco Decanter Services Inc. (Oilfield Decanter Centrifuges, Dewatering Centrifuges)

-

HAUS Centrifuge Technologies (Decanter Centrifuges, Olive Oil Centrifuges)

-

Thomas Broadbent & Sons Ltd. (Industrial Centrifuges, Textile Centrifuges)

-

Fisher Scientific (High-Speed Centrifuges, Lab Centrifuges)

-

Pennwalt Ltd. (Basket Centrifuges, Three-Phase Centrifuges)

Suppliers for (separation technologies, particularly for industrial and environmental applications like wastewater treatment) on the Centrifuge Market

-

GEA Group AG

-

Andritz AG

-

FLSmidth

-

Alfa Laval AB

-

Flottweg SE

-

HAUS Centrifuge Technologies

-

Thermo Fisher Scientific

-

Beckman Coulter

-

Eppendorf AG

-

Stalwart International

Recent Development

- In May 2023: GEA Group AG announced a EUR 50 million investment to modernize its centrifuge production facilities in Germany by 2024, focusing on sustainability, digitalization, and automation to drive growth in food, beverage, and pharmaceutical industries.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 463 Million |

| Market Size by 2032 | USD 689.91 Million |

| CAGR | CAGR of 4.53% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Decanters, High-Speed Separators, Others) • By Drilling & Excavation Activity (Tunnel Boring, Horizontal Directional Drilling, Exploration Drilling, Others) • By Application (Solids Control, Mud Cleaning, Dewatering, Fluid Clarification, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Siebtechnik Tema GmbH, SPX Flow Inc., Flottweg SE, Schlumberger Limited, Ferrum Ltd., Mitsubishi Kakoki Kaisha Ltd., FLSmidth, GEA Group AG, Alfa Laval, Andritz, Thermo Fisher Scientific Inc., Beckman Coulter Inc., Eppendorf AG, Hettich Instruments, Becton, Dickinson and Company (BD), Kubco Decanter Services Inc., HAUS Centrifuge Technologies, Thomas Broadbent & Sons Ltd., Fisher Scientific, Pennwalt Ltd. |

Frequently Asked Questions

Ans: North America dominated the Centrifuge Market in 2023

Ans: The “Decanters” segment dominated the Centrifuge Market.

Ans: The growing use of centrifuges in drug discovery, vaccine production, and molecular diagnostics is driving market growth, fueled by advancements in biotechnology and pharmaceuticals.

Ans: The Centrifuge Market was USD 463 million in 2023 and is expected to reach USD 689.91 million by 2032.

Ans: The Centrifuge Market is expected to grow at a CAGR of 4.53% during 2024-2032.

Get in Touch