Chelating Agents Market Report Scope & Overview:

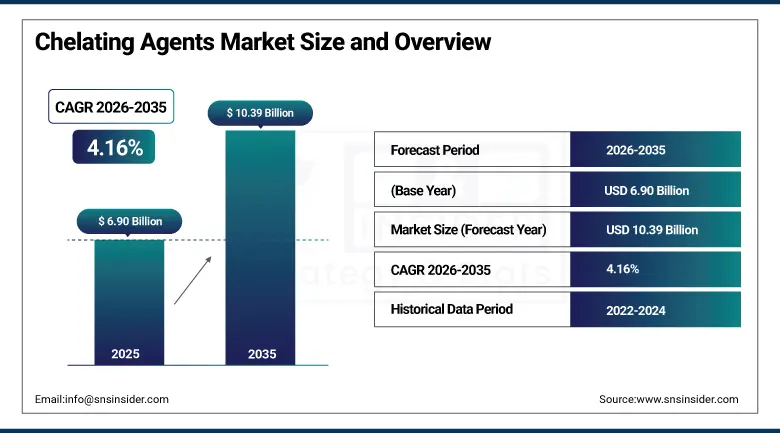

The Chelating Agents Market was valued at USD 6.90 Billion in 2025 and is expected to reach USD 10.39 Billion by 2035, growing at a CAGR of 4.16% from 2026 to 2035.

The chelating agents market across the globe is growing steadily on the back of increasing use of metal scavenging agents in water treatment, pulp & paper, consumer and industrial cleaning products, agrochemicals, and pharmaceutical industries, at the same time, undergoing a massive change in the product portfolio due to increasing regulations on the use of non-biodegradable chelating agents and growing trend of using biodegradable chelating agents such as MGDA, GLDA, and IDS among others. Chelating agents work by forming complexes with metal ions and inhibit catalytic action of metals causing formation of scales, color and oxidizing effect in the processes.

BASF SE, the global market leader in chelating agent production, has invested substantially in expanding its Trilon portfolio of biodegradable chelating agents including MGDA and GLDA that comply with the EU Detergent Regulation and EPA environmental guidelines, developing cost-efficient manufacturing processes for biodegradable alternatives that enable price competitive substitution of conventional EDTA in mainstream detergent and cleaning formulations.

Market Size and Forecast

-

Market Size in 2026E: USD 7.19 Billion

-

Market Size by 2035: USD 10.39 Billion

-

CAGR: 4.16% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Chelating Agents Market - Request Free Sample Report

Chelating Agents Market Trends

-

Biodegradable chelating agents such as MGDA, GLDA, and IDS are gaining adoption due to sustainability and regulatory compliance requirements.

-

Regulatory pressure on conventional chelating agents and phosphate-based formulations is driving demand for eco-friendly alternatives.

-

Growing investments in industrial and municipal water treatment infrastructure are increasing the use of chelating agents for metal ion control and scale prevention.

-

Rising pharmaceutical applications are supporting demand for high-purity chelating agents used in drug stabilization and formulation.

-

Expansion of precision agriculture is boosting the adoption of chelated micronutrient fertilizers to improve nutrient availability and crop productivity.

U.S. Chelating Agents Market Outlook

The U.S. Chelating Agents Market was valued at approximately USD 1.43 Billion in 2025 and is expected to reach approximately USD 2.14 Billion by 2035, growing at a CAGR of approximately 4.10%.

America is the world's largest commercial chelating agents market, both in terms of value due to high industrial end use demand from water treatment, pulp and paper, and domestic cleaning, strict regulation from the EPA in limiting traditional non-biodegradable chelating agents and forcing the adoption of biodegradable substitutes, and the existence of Dow Chemical, Olin Corp., and Nouryon manufacturing operations in the United States.

The EPA restrictions of phosphate detergents and promoting the use of biodegradable substitutes for chelating agents form the most complete regulatory adoption driver of any national market, allowing sustained above average growth in the purchase of biodegradable chelating agents for both consumer and industrial products formulation applications. The consumption of chelating agents in the pharmaceutical industry in America for injectable and eye drops formulations forms specialty demand with premium prices.

In 2024, Nouryon expanded its IDS (iminodisuccinic acid) biodegradable chelating agent production capacity at its U.S. manufacturing facilities to meet growing demand from household cleaning and industrial cleaning customers reformulating away from EDTA and NTA under EPA guidance, reflecting the sustained investment by specialty chemical producers in biodegradable chelating agent supply chain expansion that enables the transition from conventional to sustainable chelating chemistry in mainstream consumer and industrial applications.

Chelating Agents Market Segment Analysis

-

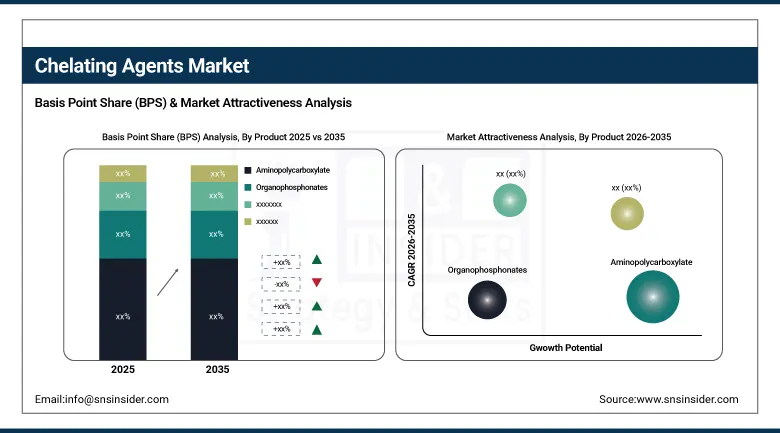

By Product, the Aminopolycarboxylate segment dominated the chelating agents market with approximately 64% share in 2025, while the Organophosphonates segment is the fastest growing driven by expanding water treatment scale inhibition and threshold effect applications where phosphonate chelating agents provide effective calcium carbonate.

-

By Application, the Pulp & Paper segment dominated the chelating agents market with approximately 27% share in 2025, while the Water Treatment segment is the fastest growing as expanding industrial water treatment infrastructure.

By Product, aminopolycarboxylate dominates, organophosphonates grow fastest

In 2025, aminopolycarboxylate held a leading share of nearly 64% in the chelating agents market. The versatility of EDTA for uses in applications like water treatment, detergent formulations, pulp & paper bleaching, chemical process industries, food preservatives, medicines, and analytical chemistry has the most diversified range of end use application of all kinds of chelating agents chemicals.

The organophosphonate is the fastest growing segment owing to the efficiency of phosphonate chelating agents like ATMP, HEDP, DTPMP, and PBTC as inhibitors of scale formation in industrial cooling waters, oilfield water injection and geothermal energy where the hardness of calcium and the temperatures generated by industrial process water systems are beyond the effective working range of aminopolycarboxylates.

By Application, pulp and paper dominates, water treatment grows fastest

The pulp and paper application remained the topmost application area, accounting for about 27% share in terms of volume in the chelating agents market in 2025. Systematic application of hydrogen peroxide bleaching chelation in the global paper manufacturing industry, wherein addition of EDTA and DTPA to pulp bleaching process is a widespread practice worldwide among kraft pulp mills, constitutes the volume-heavy single application of chelating agents in any industrial segment. One tonne of bleached kraft pulp produced around the globe results in the consumption of chelating agents that sum up, in the aggregate of the approximately 170 million tons annually produced volume of global bleached pulp, to the largest industrial chelating agents demand segment in terms of volume.

Water treatment emerged as the fastest growing application segment, owing to increasing water treatment plant installations in developing countries, increased investments in municipal water purification due to urbanization and stringent regulations on water quality, and increased applications of chelating agents in membrane scale-inhibitor formulations in reverse osmosis and nanofiltration systems.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

74.0% |

|

Europe |

Germany |

26.8% |

|

Asia Pacific |

China |

56.3% |

|

Middle East & Africa |

Saudi Arabia |

32.4% |

|

Latin America |

Brazil |

48.6% |

North America Chelating Agents Market Insights

The North American region is the market leader in chelating agents by value due to the high-end pharmaceutical, personal care and specialty cleaning use of the product. The U.S. represents about 74.0% of total revenues generated in the region on account of its wide-ranging industrial uses in applications such as water treatment, pulp and paper, household cleaning and pharmaceuticals within the EPA regulatory environment that mandates biodegradable chelating agents.

Canada makes up approximately 26.0% of the revenues in North America on account of its global leadership position in pulp and paper production which requires the use of chelating agents, water treatment in its oil sands deposits where scale inhibitors are required, and agricultural micronutrients for its major cereal crop and horticulture segments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Chelating Agents Market Insights

Europe has taken the lead in terms of biodegradable chelating agent use due to the EU Detergent Regulation phosphate limitation, the overall chemical safety regulation via REACH, and the restriction on traditional chelating agents in water environment by ECHA. Germany generates about 26.8% of total European revenue due to Trilon biodegradable chelating agent sales by BASF, sophisticated sustainability compliance in the domestic paper and cleaning industries, and pioneering efforts of the German chemical industry in creating biodegradable chelating agent alternatives.

Netherlands, France, and the UK can be considered as secondary important European regions that ensure steady demand for specialty chelating agents due to Dutch operations of Nouryon, French cleaning and personal care products, and pharmaceutical and food ingredient applications in the UK. Progressive restriction timeframe for traditional chelating agents in the EU ensures continuity of biodegradable adoption transition in Europe.

Asia Pacific Chelating Agents Market Insights

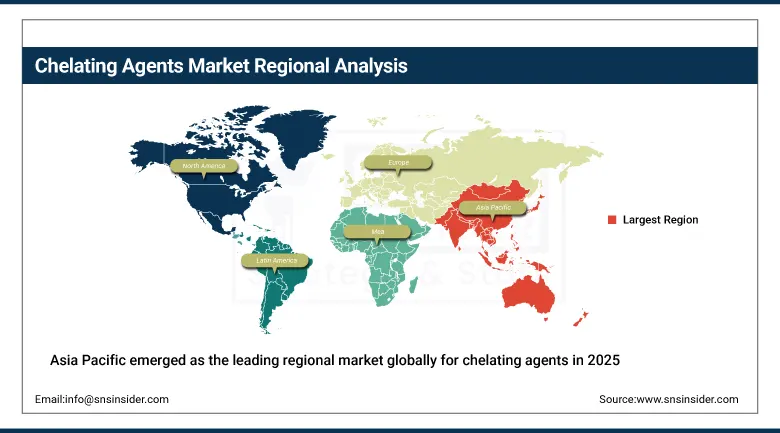

Asia Pacific emerged as the leading regional market globally for chelating agents in 2025 with an approximate 42% revenue share owing to the exceptional consumption of chelating agents within the industries of China, India, Japan, South Korea, and Southeast Asia with respect to the scale of the pulp and paper industry, water treatment industry, textile industry, and agrochemical industry which makes it the largest regional chelating agents market on the basis of volumes. China has the largest share in Asia Pacific region revenues, estimated at around 56.3%, due to the presence of the large scale paper manufacturing industry, the largest infrastructure for industrial water treatment, and the agricultural chelated micronutrients industry which individually are larger than some secondary regional markets.

India is the fastest-growing national market within Asia Pacific region due to the growth of the paper manufacturing industry, the growth of the industrial water treatment market due to the expansion of manufacturing sector, the growth of the agrochemical chelated micronutrients market, and the pharmaceutical sector's requirement of specialty chelating agents.

MEA & Latin America Chelating Agents Market Insights

The dominant share of MEA market revenues is that of Saudi Arabia accounting for roughly 32.4% due to its desalination and industrial water treatment scale inhibitor purchases as well as increasing agrochemical chelated micronutrient usage in precision irrigation agriculture alongside UAE and Egypt-based water treatment and cleaning activities. Brazil has the largest revenue share in the Latin American region accounting for about 48.6% due to its global-scale production of eucalyptus kraft pulp and chelated micronutrients in agriculture along with soybean, sugarcane, and citrus farming, while Mexico and Colombia add secondary industrial water treatment demand until 2035.

Market Dynamics

Growth Drivers: Biodegradable chelating agent transition driven by environmental regulation and expanding water treatment infrastructure

The regulatory move to biodegradable chelating agents constitutes the key commercial structural shift within the market. EPA regulation on phosphates and promotion of EDTA biodegradable alternatives for use in the U.S., phosphate ban in European detergents and European Reach regulations limiting persistent chelating agents, alongside progressive pollution regulations in China, constitute regulatory adoption drivers, ensuring steady growth in the biodegradable chelating agents market at a rate greater than the total chelating agents market growth rate.

Expansion in investments into industrial and municipal water treatment plants constitutes the key volume growth driver within the market. The industrial application of chelating agents for water treatment purposes in cooling water scale inhibition, reverse osmosis anti-scalants and process water purification constitutes a direct function of the expansion in manufacturing operations in Asia-Pacific, Middle East and Latin America regions.

Restraints: Regulatory restriction on conventional chelating agents and raw material price volatility

The compliance costs associated with the regulation of non-biodegradable conventional chelating agents, which drive the revenue growth of biodegradable products, are a factor which limits market growth potential, even though they drive the revenue growth of biodegradable products. In each instance where there is a need to replace EDTA or phosphonates by biodegradable products, there will be formulation cost, registration cost, testing cost, and supply chain qualification cost associated with the change. The high cost of production of biodegradable products compared to conventional EDTA products makes it difficult to adopt them.

Opportunities: Pharmaceutical and personal care specialty applications and precision agriculture chelated micronutrient demand

Application growth in the pharmaceutical and personal care industries for chelating agents is the most profitable business opportunity for chelating agents. Utilization of pharmaceutical grade EDTA in injectable drug formulation stability, ophthalmic solution microbial chelation, and increased bioavailability of oral drugs creates demand at prices that far outstrip the commodity pricing of industrial chelating agents. Every FDA approved injectable drug formulation that uses the chelating agents EDTA or citric acid is a source of sustainable pharmaceutical demand that has been established through a process of patent protection and regulation that carries switching costs, sustaining the relationship. Personal care utilization of chelating agents in skin, hair, and cosmetic applications because of their property of enhancing product stability creates consumer demand that generates profits beyond commodity chelating agents.

Recent Developments:

-

2024: Nouryon expanded its IDS biodegradable chelating agent production capacity in 2024 at European and U.S. manufacturing facilities to meet accelerating demand from household and industrial cleaning formulation customers requiring EDTA replacement solutions compliant with EPA and EU environmental guidelines.

-

2024: BASF launched new Trilon M MGDA biodegradable chelating agent formulations in 2024 with enhanced performance in hard water dishwashing and automatic industrial cleaning applications, expanding the addressable substitution scope for EDTA replacement in mainstream institutional cleaning products.

Chelating Agents Market Key Players

-

BASF SE

-

Nouryon (formerly AkzoNobel Specialty Chemicals)

-

Dow Chemical Company

-

Lanxess AG

-

Evonik Industries AG

-

Olin Corporation

-

Innospec Inc.

-

Mitsubishi Chemical Corporation

-

Nippon Shokubai Co. Ltd.

-

Huntsman Corporation

-

Kemira Oyj

-

Solutia Inc. (Eastman Chemical)

-

Jiangsu Yida Chemical Co. Ltd.

-

Shanghai Trustin Chemical Co. Ltd.

-

Zhejiang Juhua Co. Ltd.

-

AVA Chemicals Pvt. Ltd.

-

Lishui Boruite New Material Technology Co. Ltd.

-

QualiChem Inc.

-

Tronox Holdings plc

-

Ascend Performance Materials LLC

Chelating Agents Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.90 Billion |

| Market Size by 2035 | USD 10.39 Billion |

| CAGR | CAGR of 4.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Sodium Gluconate, Organophosphonates, Aminopolycarboxylate, Others) • Application (Household & Industrial Cleaning, Pulp & Paper, Chemical Processing, Water Treatment, Agrochemicals, Consumer Products, Pharmaceutical, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Nouryon (formerly AkzoNobel Specialty Chemicals), Dow Chemical Company, Lanxess AG, Evonik Industries AG, Olin Corporation, Innospec Inc., Mitsubishi Chemical Corporation, Nippon Shokubai Co. Ltd., Huntsman Corporation, Kemira Oyj, Solutia Inc. (Eastman Chemical), Jiangsu Yida Chemical Co. Ltd., Shanghai Trustin Chemical Co. Ltd., Zhejiang Juhua Co. Ltd., AVA Chemicals Pvt. Ltd., Lishui Boruite New Material Technology Co. Ltd., QualiChem Inc., Tronox Holdings plc, and Ascend Performance Materials LLC. |

Frequently Asked Questions

The Chelating Agents Market is expected to grow at a CAGR of 4.16% from 2026 to 2035.

The Chelating Agents Market was valued at USD 6.90 Billion in 2025.

The regulatory transition toward biodegradable chelating agents driven by EPA and ECHA restrictions on conventional EDTA and phosphonate compounds, and expanding industrial and municipal water treatment infrastructure investment creating growing metal ion sequestration demand.

Aminopolycarboxylate dominated the Chelating Agents Market with approximately 64% share in 2025, while Organophosphonates is the fastest growing segment.

Asia Pacific dominated the Chelating Agents Market in 2025 with approximately 42% share, driven by China's massive pulp and paper, water treatment, and agrochemical industries, while North America leads by revenue value per tonne through premium pharmaceutical and specialty application demand.

Get in Touch