Clinical Decision Support Systems Market Report Scope & Overview:

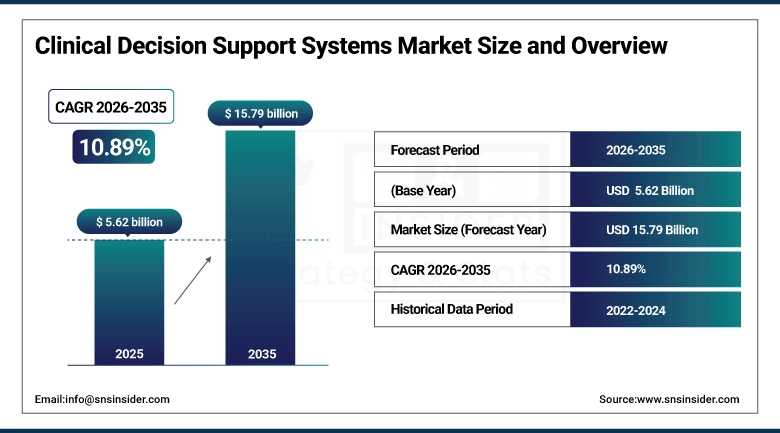

The Clinical Decision Support Systems Market size was valued at USD 5.62 Billion in 2025 and is projected to reach USD 15.79 Billion by 2035, growing at a CAGR of 10.89% during 2026–2035.

Rising number of implementations of digital healthcare solutions and electronic health records for ensuring clinical efficiency is the factor that triggering the growth of Clinical Decision Support Systems market. The market is also propelled to rapid growth due to the growing demand for accuracy and versatility in diagnostics, coupled with the advancements of artificial intelligence (AI) and big data analytics into the diagnostics sector. Moreover, rising incidence of chronic diseases, favorable government initiatives and transition towards value based care is further increasing adoption of CDSS among healthcare providers to improve patient outcomes and minimize medical errors.

Clinical Decision Support Systems Market Size and Forecast:

-

Market Size in 2025: USD 5.62 Billion

-

Market Size by 2035: USD 15.79 Billion

-

CAGR: 10.89% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Clinical Decision Support Systems Market - Request Free Sample Report

Clinical Decision Support Systems Market Key Trends:

-

EVs, ADAS, and digital health platforms are driving the fastest-growing application segment in clinical decision support systems.

-

Cloud-based CDSS solutions are gaining popularity due to scalability and real-time data access, while integrated EHR-based systems remain the dominant deployment model.

-

Increasing demand for AI-driven and data analytics-enabled decision support tools that improve diagnostic accuracy and patient outcomes.

-

Expansion in applications across telemedicine, remote patient monitoring, and personalized medicine.

-

High dependence on healthcare data interoperability and regulatory compliance, which poses implementation challenges.

-

Growing demand for mobile and user-friendly CDSS platforms to support clinicians in real-time decision-making.

-

Specialized CDSS solutions are required for critical care, oncology, and chronic disease management, where high accuracy and reliability are essential.

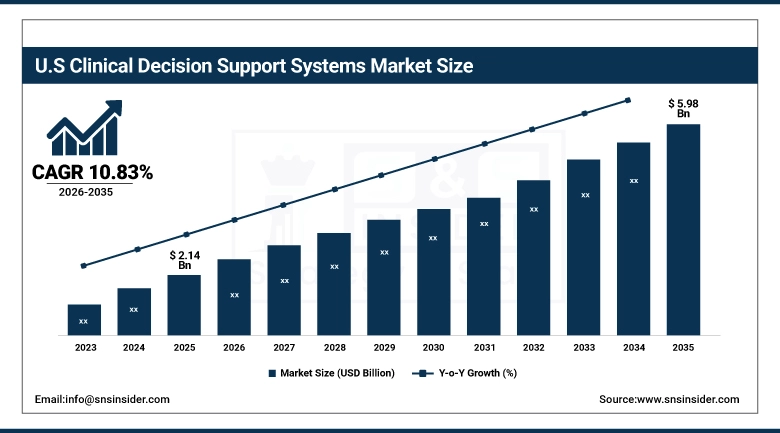

The U.S. Clinical Decision Support Systems Market size was valued at USD 2.14 Billion in 2025 and is projected to reach USD 5.98 Billion by 2035, growing at a CAGR of 10.83% during 2026–2035. Growth in the U.S. Clinical Decision Support Systems market is driven by widespread EHR adoption, rising demand for AI-powered diagnostics, increasing chronic disease burden, supportive healthcare regulations, and the need to improve clinical efficiency, reduce errors, and enhance patient outcomes across healthcare systems.

Clinical Decision Support Systems Market Key Drivers:

-

Rising adoption of electronic health records (EHRs) and digital healthcare infrastructure is driving the demand for clinical decision support systems.

The adoption of CDSS is being fuelled by the rising incidence of chronic diseases and the increasing demand for effective and timely clinical decision-making. Healthcare providers are also increasingly focusing on improving the accuracy of diagnosis, minimizing medical errors, and enhancing patient care outcomes making integration of artificial intelligence, machine learning, and big data analytics the part of routine healthcare systems, hence supporting overall market growth.

Clinical Decision Support Systems Market Key Restraints:

-

Data privacy concerns and integration challenges with existing healthcare IT systems are restraining the growth of clinical decision support systems.

The extensive demand for CDSS solution is hampered due to the comparatively stringent regulatory requirements along with the safety issues related patient data safety and privacy. Moreover, high cost of implementation and maintenance and non-interoperability of various systems and resistance from health professionals due to disruption of workflow are major restraining factors for the growth of Maestro Care Market.

Clinical Decision Support Systems Market Key Opportunities:

-

Growing demand for AI-driven personalized healthcare and telemedicine solutions is creating significant opportunities for clinical decision support systems.

However, the steady proliferation of remote patient monitoring, telehealth platforms and value-based care models are providing CDSS with new opportunities to scale. Growing investments in healthcare IT and higher penetration of predictive analytics and cloud based solutions are making CDSS more efficient, scalable, and actionable in real-time, and therefore a prominent feature of future healthcare systems.

Clinical Decision Support Systems Market Segments:

-

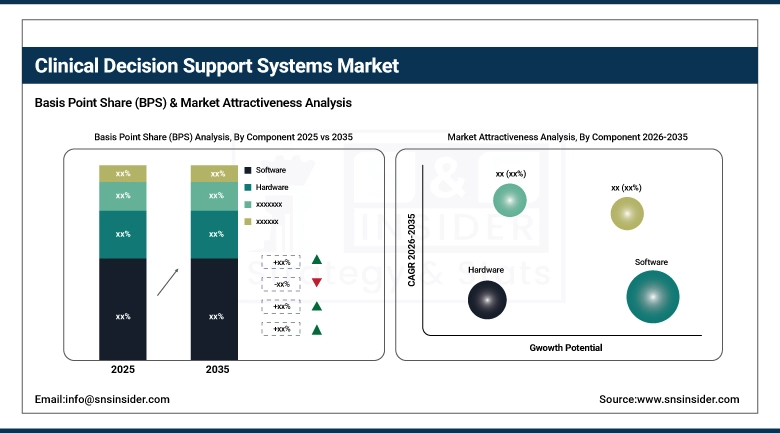

By Component: In 2025, Software dominated with 48% share; Services fastest growing segment during 2026–2035

-

By Delivery Mode: In 2025, On-Premise dominated with 46% share; Cloud-Based fastest growing segment during 2026–2035

-

By Application: In 2025, Clinical Decision Support dominated with 41% share; Drug Allergy Alerts fastest growing segment during 2026–2035

-

By End User: In 2025, Hospitals dominated with 45% share; Clinics fastest growing segment during 2026–2035

Clinical Decision Support Systems Market Segment Analysis:

By Component, Software Dominate While Services Grow Rapidly:

Software components comprised a larger share of the clinical decision support systems market due to their importance in CDSS platforms that analyze data and utilize clinical rule engines to provide decision-making support. Ongoing developments in AI, machine learning and predictive analytics are making this segment even more robust.

The service segment is the fastest-growing segment with the increasing requirement for system integration, maintenance, training, and support. Thus, healthcare providers are spending on consulting and implementation solutions for the efficient deployment and use of CDSS solutions.

By Delivery Mode, On-Premise Dominate While Cloud-Based Grow Rapidly:

The clinical decision support systems market share is majorly held by On-Premise solutions owing to the availability of robust data security and the control over in-house infrastructure and systems. Such systems are preferred in scenarios, where compliance with stringent regulations and protection of patient privacy is a key challenge.

The adoption of Cloud-Based systems is the broadening segment as it offers scalability and cost-effectiveness and the ability to access data in real-time from various healthcare environments! Increase in telehealth and remote care services is the primary driving factor for the growth of cloud-based CDSS platforms.

By Application, Clinical Decision Support Dominates While Drug Allergy Alerts Grow Rapidly:

The clinical decision support systems market by component is dominated by clinical decision support, which finds extensive application in helping physicians with diagnostic, treatment planning, and clinical workflow. The growth in this segment can be attributed to the rising adoption of evidence based medicine which aim to overcome medical errors and improve patient outcomes.

Another rapidly growing segment is the Drug Allergy Alerts segment which is driven by the necessity for patient safety and avoidance of adverse drug reactions. The growth of this segment is driven by emerging trend of integration of CDSS with e-prescribing systems and electronic health records.

By End User, Hospitals Dominate While Clinics Grow Rapidly:

Because of huge patient data, complex clinical workflows, and higher adoption of advanced healthcare IT systems, the hospitals accounted for the highest share in the market. CDSS are commonly used by hospitals to support decision-making, patient safety, and operations.

The clinic segment accounts for the fastest growing segment owing to rising digitization among small healthcare facilities coupled with high adoption of cost-effective and cloud-based CDSS solutions. This segment is also expected to grow at the highest rate during the forecast period due to the increasing need for patient management and rapid clinical decision making in outpatient settings.

Clinical Decision Support Systems Market Regional Analysis:

North America Clinical Decision Support Systems Market Insights:

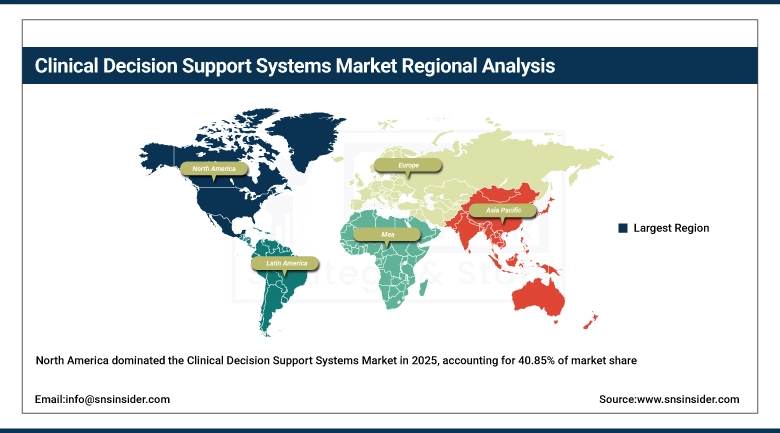

The Clinical Decision Support Systems Market was led by North America, which accounted for 40.85% of the market due to its high level of healthcare IT infrastructure and a high adoption of Electronic Health Records (EHRs). Strong governmental initiatives, increased healthcare expenditure, and early adoption of AI-based clinical solutions is expected to drive the growth of the region. Market growth is also supported by the presence of leading digital healthcare IT companies continuing to innovate in the digital health space. Furthermore, the need for enhanced patient safety, lower medical errors, and better clinical efficiency are prompting hospitals and healthcare systems to adopt CDSS.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Clinical Decision Support Systems Market Insights:

The regional segment for the Asia-Pacific Clinical Decision Support Systems Market is the most lucrative segment that is expected to grow at a CAGR of 12.34% during the period from 2025 to 2035. Rapid development of the overall healthcare infrastructure, increasing adoption of digital health technologies, coupled with rising government initiatives to utilize digital health technologies in countries such as China, India, and Japan are contributing to growth. The region will witness a substantial market growth attributed to the large patient population, increasing healthcare spending and rising awareness regarding enhanced clinical solutions.

Europe Clinical Decision Support Systems Market Insights:

Europe is a prominent region in the Clinical Decision Support Systems Market owing to the availability of well-developed healthcare system and increasing acceptance of digital healthcare technologies. Growing attention towards patient safety, regulatory compliance, and embedding predictive and prescriptive analytics into point-of-care settings is expected to act as a growth accelerator. Moreover, growing investments in healthcare IT infrastructure and robust government support are expected to further fuel the demand for the market.

Latin America Clinical Decision Support Systems Market Insights:

The Latin America Clinical Decision Support Systems Market is driven by improving healthcare infrastructure, rising awareness of digital health solutions, and rising adoption of healthcare IT systems in developing economies including Brazil and Mexico and many others. In addition, growing government initiatives coupled with slow recovery in the accessibility of health care is also positively giving way to the market growth.

Middle East & Africa (MEA) Clinical Decision Support Systems Market Insights:

Rising healthcare infrastructure, rising digital health investments, and rising adoption of advanced healthcare technology in UAE, Saudi, South Africa are some of the major factors driving the Middle East & Africa Clinical Decision Support Systems Market. The regional market growth is backed up by various government initiatives, increasing healthcare expenditure, and focus towards improving patient care.

Clinical Decision Support Systems Market Competitive Landscape:

IBM Corporation is a global leader in technology and consulting, a leader in artificial intelligence, cloud and cognitive solutions, and healthcare analytics. IBM deploys its Watson Health artificial intelligence platform for providing data-driven insights, predictive analytics, and evidence-based recommendations for clinicians in use cases across the clinical decision support systems market. With robust big data integration, machine learning, and healthcare interoperability, it aids in enhancing clinical outcomes and operational efficiency. IBM's position in the CDSS space is bolstered by persistently innovative AI investments and strategic partnerships with healthcare providers.

-

In March 2025, IBM Corporation expanded its AI-driven healthcare analytics capabilities by enhancing its Watson-based clinical decision tools, improving real-time patient data analysis and supporting more accurate and personalized treatment decisions across healthcare systems.

Oracle is a top global cloud infrastructure provider and healthcare IT solutions vendor with a primary focus in electronic health records and data management systems. Oracle focuses on integrating advanced analytics and cloud-based platforms to create a connected environment that aligns seamlessly with clinical workflows to aid clinical decision support systems in the market. Acquisitions of healthcare IT platforms have helped it provide CDSS solutions to customers reliably, at scale and interoperably. Oracle's focus on secure data management and cloud transformation enables its growing presence in digital healthcare ecosystems.

-

In February 2025, Oracle enhanced its cloud-based healthcare platform by integrating advanced clinical decision support capabilities, enabling improved interoperability, real-time insights, and more efficient patient data management for healthcare providers.

Clinical Decision Support Systems Market Key Players:

-

IBM Corporation

-

Oracle

-

Koninklijke Philips

-

McKesson Corporation

-

Siemens Healthineers GmbH

-

Wolters Kluwer

-

Allscripts Healthcare

-

Agfa-Gevaert Group

-

athenahealth, Inc.

-

NextGen Healthcare Inc.

-

Aidoc

-

Navina

-

Tebra

-

Medidata Solutions

-

Corti

-

DreaMed Diabetes

-

Bingli

-

SOAP, Inc.

-

Included Health

-

Accolade

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.62 Billion |

| Market Size by 2035 | USD 15.79 Billion |

| CAGR | CAGR of 10.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component: (Hardware, Software, Services) • By Delivery Mode: (On-Premise, Cloud-Based, Web-Based) • By Application: (Clinical Decision Support, Drug Allergy Alerts, Clinical Guidelines) • By End User: (Hospitals, Clinics, Diagnostic Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Oracle, Koninklijke Philips, McKesson Corporation, Siemens Healthineers GmbH, Wolters Kluwer, Allscripts Healthcare, Agfa-Gevaert Group, Athenahealth, Inc., NextGen Healthcare Inc., Aidoc, Navina, Tebra, Medidata Solutions, Corti, DreaMed Diabetes, Bingli, SOAP, Inc., Included Health, Accolade |

Frequently Asked Questions

The Clinical Decision Support Systems Market is expected to grow at a CAGR of 10.84 % during 2026–2035.

The Clinical Decision Support Systems Market size was valued at USD 5.62 Billion in 2025 and is projected to reach USD 15.79 Billion by 2035.

The key drivers of the Clinical Decision Support Systems Market include increasing adoption of digital healthcare solutions, rising integration of AI and data analytics for accurate clinical decision-making, growing prevalence of chronic diseases, supportive government initiatives, and the need to improve patient outcomes and reduce medical errors.

The Software segment dominated the Clinical Decision Support Systems Market during the projected period.

North America dominated the Clinical Decision Support Systems Market in 2025.

Get in Touch