Cloud Microservices Market Report Scope & Overview:

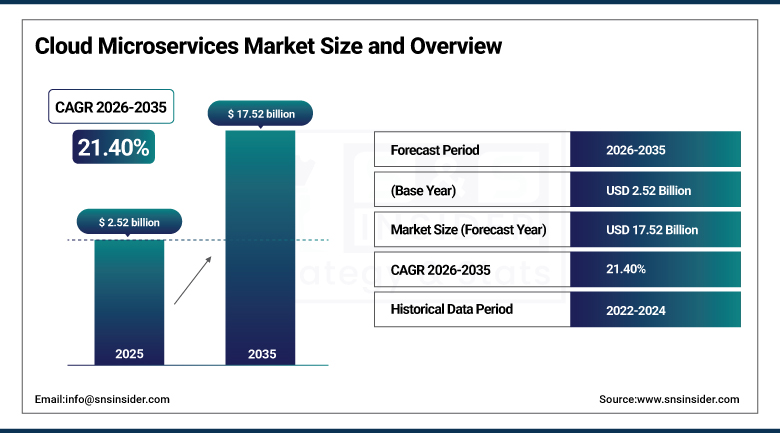

The Cloud Microservices Market was valued at USD 2.52 Billion in 2025 and is expected to reach USD 17.52 Billion by 2035, growing at a CAGR of 21.40% from 2026–2035.

In cloud microservices, an application is split into several smaller pieces that can be deployed independently and without any effect on other parts of the system. As a result, the development becomes faster, it becomes possible to deploy new features continuously, and companies get operational benefits in scaling particular modules according to real demand. Cloud platforms such as Amazon Web Services, Microsoft Azure, and Google Cloud Platform constantly offer advanced tools for implementing this architecture, while DevOps trends, CI/CD pipeline integration, and serverless technology encourage industries like BFSI, healthcare, retail, and telecom to adopt microservices to benefit from their scalability and real-time capabilities.

The Salesforce cloud-native microservices platform was unveiled in October 2024 in order to allow faster creation of applications. This tool makes possible the development of scalable applications with the use of a modular system, thus saving the company from time loss, and is one of the examples of how Salesforce improves its cloud service through the provision of more agile tools to its clients.

Market Size and Forecast

-

Market Size in 2026E: USD 3.06 Billion

-

Market Size by 2035: USD 17.52 Billion

-

CAGR: 21.40% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Cloud Microservices Market - Request Free Sample Report

Cloud Microservices Market Trends

-

Hybrid cloud adoption is accelerating as enterprises deploy microservices across public and private cloud environments to improve scalability, flexibility, and regulatory compliance.

-

Kubernetes and managed container orchestration platforms are simplifying large-scale microservices deployment, management, and application lifecycle automation.

-

Serverless computing is increasingly integrated with microservices architectures to optimize resource utilization, reduce operational costs, and accelerate application development.

-

AI-powered observability and monitoring platforms are enhancing performance management, anomaly detection, and troubleshooting across distributed microservices environments.

-

Service mesh technologies are improving secure service-to-service communication, traffic management, and policy enforcement in cloud-native microservices deployments.

U.S. Cloud Microservices Market Outlook

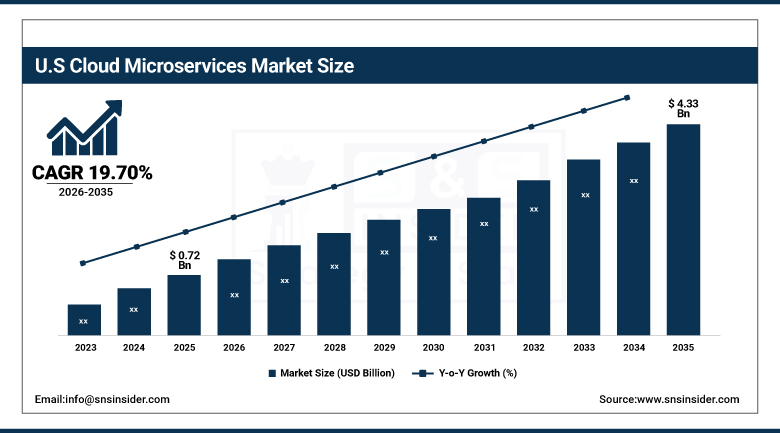

The U.S. cloud microservices market was valued at approximately USD 0.72 Billion in 2025 and is expected to reach approximately USD 4.33 Billion by 2035, growing at a CAGR of approximately 19.70%.

To achieve agility, scalability, and rapid deployment, U.S. organizations continue moving from monolithic architectures to microservices at a steady pace. This development is driven by increased use of the DevOps approaches, containers technologies like Docker and Kubernetes, and the constant necessity to achieve continuous integration and deployment. AWS, Microsoft Azure, Google Cloud, and other leading cloud vendors constantly improve the microservices offering in order to meet the needs of enterprise customers, which ensures the leadership of the U.S. market not only in size but also in technological advancement.

During the Google Cloud Next 2025 event held in April, Google introduced some notable improvements in Google Kubernetes Engine, which included the general availability of Cluster Director for GKE, and the introduction of Application Design Center and Cloud Hub. These application-focused solutions enable developers to design whole applications through canvas-based approach, create infrastructure as code, and monitor applications through a unified dashboard interface, in line with the trend in the industry towards higher level abstractions that facilitate the adoption of microservices architecture.

Cloud Microservices Market Segment Analysis

-

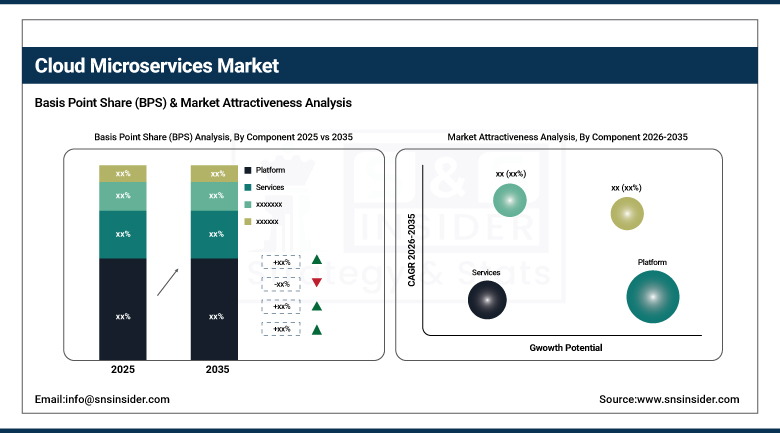

By Component, the platform segment dominated the cloud microservices market with a 64% revenue share in 2025, while the services segment is the fastest growing with a CAGR of approximately 24.6%.

-

By Deployment Mode, the hybrid segment dominated the cloud microservices market with a 50% revenue share in 2025, while the private segment is the fastest growing with a CAGR of approximately 22.9%.

-

By Enterprise Type, the large enterprises segment dominated the cloud microservices market with a 68% revenue share in 2025, while the SME segment is the fastest growing with a CAGR of approximately 24.7%.

-

By End-User, the IT & telecommunications segment dominated the cloud microservices market with a 28% revenue share in 2025, while the healthcare segment is the fastest growing with a CAGR of approximately 26.6%.

By Component, platform dominates, services grow fastest

The platforms segment was estimated to hold around 64% of the market in 2025 because the development tools and cloud-native platforms offer the necessary integrated ecosystem, which includes logging, container orchestration, API gateways, monitoring, and service discovery, for microservices to be operational. Increasing adoption of platforms based on Kubernetes, such as Red Hat OpenShift, AWS Fargate, and Microsoft Azure Kubernetes Service, further expedites application development and simplifies DevOps processes.

Among all segments, the services segment is witnessing the fastest growth at a projected CAGR of 24.6%, due to increasing demand for professional consultation, integration, and maintenance services. The enterprises are depending more and more on managed services, because they are using microservices architecture, and to support this process they need assistance with deployment, configuration of security, and lifecycle management, while cloud providers such as AWS and Google Cloud are offering services to manage containers and service meshes.

By Deployment Mode, hybrid dominates, private grows fastest

Deployment through the hybrid model has been leading the market since 2025 with a 50% revenue share because of the higher flexibility, control, and security it offers. There are many firms that have opted to adapt their cloud infrastructure into a hybrid cloud infrastructure that ensures they combine the benefits of flexibility from public clouds and the control provided by private clouds.

The private deployment model will have the highest growth rate in the coming years, and is expected to grow at an estimated compound annual growth rate (CAGR) of around 22.9%, owing to factors such as security, customization, and compliance requirements that favor the growth of this market segment. Enterprises dealing with confidential data, especially those from industries such as finance, healthcare, and government, are deploying their microservices in the private cloud.

By Enterprise Type, large enterprises dominate, SMEs grow fastest

Large companies were the dominant players in terms of revenue generation, accounting for 68% of the overall revenues, owing to their robust infrastructures, international reach, and focus on digital transformation. Such organizations require highly scalable, secure, and robust architectures that can support large application environments and cope with market dynamics by utilizing microservices for legacy system migration and fast deployment cycles.

Small and medium-sized enterprises represent the most rapidly growing category of businesses with a growth rate that is expected to grow at a CAGR of about 24.7% due to increased availability of affordable cloud infrastructure and innovations. Small and medium-sized enterprises are gradually shifting from the conventional monolithic architecture to more innovative microservices architecture in order to develop products quickly and be competitive in the market.

By End-User, IT & telecommunications dominates, healthcare grows fastest

With a market share of 28% in 2025, IT and telecommunication sector is dominant owing to significant usage of microservices architecture which provides scalability, flexibility, and resilience. With the advancement of digital transformation, the telecoms companies as well as IT firms are leveraging cloud microservices to modernize their existing system architectures and develop cloud native applications such as Ericsson and Nokia.

The healthcare sector represents the highest growing end-user segment, estimated to exhibit a CAGR of around 26.6% owing to factors like rising digitalization, patient-oriented approach, and the need for regulatory compliance. The use of cloud microservices offers healthcare providers agility to roll out services rapidly while ensuring interoperability along with facilitating telemedicine, EHRs, and mHealth solutions that rely on accessing specific patient information.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.0% |

|

Europe |

Germany |

23.0% |

|

Asia Pacific |

China |

39.0% |

|

Middle East & Africa |

UAE |

28.0% |

|

Latin America |

Brazil |

37.0% |

North America Cloud Microservices Market Insights

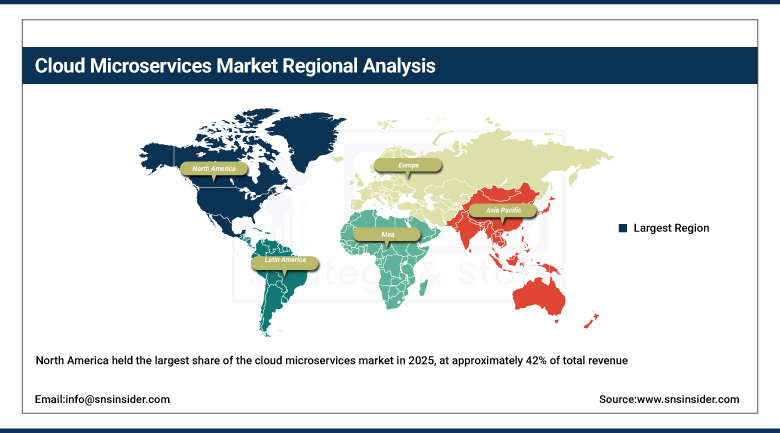

North America held the largest share of the cloud microservices market in 2025, at approximately 42% of total revenue, a leadership position built on the presence of major cloud providers including Amazon Web Services, Microsoft Azure, Google Cloud, and IBM Cloud. These major players provide powerful microservices frameworks and orchestration tools for industries including BFSI, healthcare, retail, and telecom.

The region's dominance is further reinforced by advanced IT infrastructure, strong adoption of DevOps practices, and widespread digital transformation initiatives across both large enterprises and growing mid-market companies. Continued investment in AI-driven observability tools and managed Kubernetes services keeps North America at the technical forefront of microservices architecture even as other regions grow faster in percentage terms.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cloud Microservices Market Insights

Europe remains a steady, technically capable cloud microservices market, shaped by strict data protection regulation and a strong base of enterprise software adopters across financial services, manufacturing, and telecommunications. Germany leads regional demand, drawing on its dense enterprise software user base and growing appetite for cloud-native application development.

The United Kingdom and France follow as significant secondary markets, where GDPR compliance requirements have pushed enterprises toward microservices platforms with strong built-in governance and data residency capabilities. This regulatory emphasis has made European deployments a proving ground for privacy-conscious microservices architectures increasingly valued in markets outside Europe as well.

Asia Pacific Cloud Microservices Market Insights

Asia Pacific represents the fastest-growing cloud microservices market, estimated to grow at a rate of about 24.6% through the forecast period. This growth is largely attributed to the growing pace of cloud adoption, thriving digital economies, and an increase in startups and SMEs across countries including China, India, Japan, and Southeast Asia.

More and more firms based out of countries like India and other nations in South East Asia are increasingly employing cloud-based computing platforms like Google Cloud Run and Azure Kubernetes Services in order to build their applications which can be scaled. This is additionally being driven by factors like an increasing tech-aware population and the growth in the IT outsourcing industry.

MEA & Latin America Cloud Microservices Market Insights

The Middle East and Africa remain an early-stage but developing cloud microservices market, led by the UAE's investment in digital government and financial services as part of its broader national digital transformation programs. Saudi Arabia, too, is on a parallel path where cloud native application development is linked to the economic diversification strategy, whereas South Africa plays a role of driving demand in the rest of Africa.

Latin America also shows stable adoption, headed by Brazil where financial institutions and retailers are adopting cloud microservices to handle growing transactions and to make applications scalable. Next in line in terms of adoption is Mexico, which is the second largest market in Latin America and backed by growing number of tech companies catering to North America.

Growth Drivers: Rising need for agile and scalable application development

Increased adoption of cloud technologies is leading to greater demand for more flexible, agile, and scalable application development, a significant factor driving growth in the cloud microservices market. In many cases, the traditional monolithic design of applications is not able to cope with modern requirements regarding scalability, speed of deployment, and agility, whereas cloud microservices architecture allows splitting applications into small independent units that can be scaled or updated without affecting the entire system.

The above modularity greatly boosts the productivity of firms, shortens the time to market, and supports principles of continuous delivery, hence making microservices most suitable for firms that have embraced DevOps and CI/CD principles. As firms strive to provide innovations and digital transformation services, especially in sectors such as BFSI, e-commerce, and healthcare, microservices become more and more popular.

Restraints: High complexity in managing distributed systems

The complexity of managing distributed systems remains a major constraint on cloud microservices market growth. Whereas monolithic models consist of one application or module that performs all functions, microservices architecture is made up of several services that run independently, making orchestration, monitoring, and debugging very difficult especially because different services can be coded using different programming languages.

Such intricacy leads to increased infrastructure costs and extended onboarding periods for the developers' team, with the main issues related to the guarantee of performance consistency, inter-services communication, and service-level data consistency. Implementation of security measures within such distributed and extensive environment is a whole new problem, and such obstacles are even more difficult to overcome for small companies with limited resources.

Opportunities: Growing adoption of DevOps and serverless computing

The growing adoption of DevOps culture and serverless computing in enterprises provides lucrative growth avenues in the cloud microservices market. The microservices architecture fits well with the DevOps paradigm, as it emphasizes both continuous integration and delivery as well as close cooperation between the development and operations teams, which enables DevOps teams to make changes and scale individual services independently.

There are architectures of serverless computing like AWS Lambda, Azure Functions, and Google Cloud Functions that provide the perfect platform for the execution of microservices without having to deal with any server infrastructure at all. As organizations begin to concentrate on innovation and improving interactions with their clients, there will be new frontiers that will be created through DevOps and serverless computing technologies when deploying microservices.

Recent Developments:

-

2024: In October 2024, Salesforce launched a new cloud-native microservices platform designed to streamline application development and deployment, using a modular architecture to enhance flexibility and reduce time-to-market for customers.

-

2025: At Google Cloud Next 2025 in April, Google announced major upgrades to Google Kubernetes Engine, including the general availability of Cluster Director for GKE and the launch of the Application Design Center and Cloud Hub for application-centric development.

-

2025: Throughout 2025, Google continued expanding GKE's AI infrastructure capabilities ahead of the platform's 10th anniversary, including GKE Inference Gateway and support for Kubernetes clusters scaling to 130,000 nodes for large-scale AI workloads.

Cloud Microservices Market Key Players

-

Amazon Web Services (AWS)

-

Microsoft Corporation

-

IBM Corporation

-

Salesforce, Inc.

-

F5, Inc.

-

Broadcom Inc.

-

Software AG

-

Google LLC

-

Red Hat, Inc.

-

VMware by Broadcom

-

Oracle Corporation

-

SAP SE

-

HashiCorp, Inc.

-

Docker, Inc.

-

Datadog, Inc.

-

Dynatrace, Inc.

-

New Relic, Inc.

-

MuleSoft (Salesforce)

-

Kong Inc.

-

Solo.io

Cloud Microservices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.52 Billion |

| Market Size by 2035 | USD 17.52 Billion |

| CAGR | CAGR of 21.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Platform, Services) • By Deployment Mode (Public, Private, Hybrid) • By Enterprise Type (Large Enterprises, SMEs) • By End-User (IT & Telecommunications, BFSI, Retail & Consumer Goods, Healthcare, Education, Media & Entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amazon Web Services (AWS), Microsoft Corporation, IBM Corporation, Salesforce, Inc., F5, Inc., Broadcom Inc., Software AG, Google LLC, Red Hat, Inc., VMware by Broadcom, Oracle Corporation, SAP SE, HashiCorp, Inc., Docker, Inc., Datadog, Inc., Dynatrace, Inc., New Relic, Inc., MuleSoft (Salesforce), Kong Inc., Solo.io |

Frequently Asked Questions

The Cloud Microservices Market was valued at USD 2.52 Billion in 2025.

North America dominated the Cloud Microservices Market in 2025 with approximately 42% market share.

The Cloud Microservices Market is expected to grow at a CAGR of 21.40% from 2026 to 2035.

Get in Touch