Cloud-Native Application Protection Platform Market Report Scope & Overview:

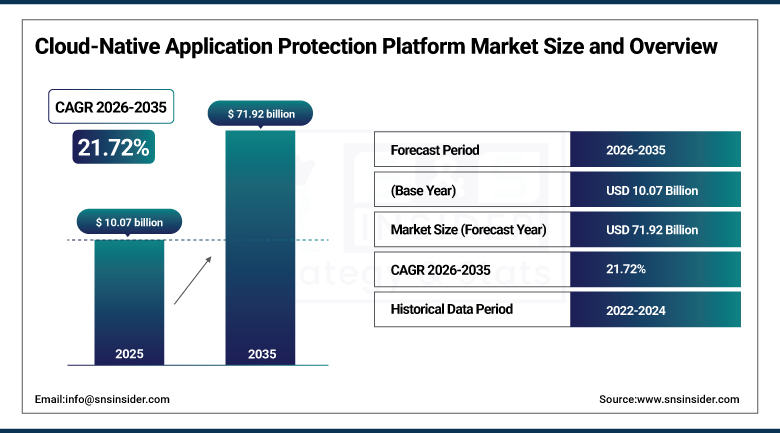

The Cloud-Native Application Protection Platform Market was valued at USD 10.07 Billion in 2025 and is expected to reach USD 71.92 Billion by 2035, growing at a CAGR of 21.72% from 2026 to 2035.

Cloud-native application protection platforms are unified security architectures that consolidate into a single integrated solution the security capabilities required to protect applications, workloads, data, and identities across cloud-native computing environments encompassing containers, Kubernetes orchestration, serverless functions, microservices, and the infrastructure-as-code configurations that define cloud resource deployments. The CNAPP category emerged from the recognition by enterprise security teams and cloud security researchers that the fragmented deployment of individually capable but unconnected point security tools, including separate cloud security posture management platforms, cloud workload protection products, cloud infrastructure entitlement management solutions, Kubernetes security posture management tools, and infrastructure-as-code scanners.

Palo Alto Networks released expanded Prisma Cloud AI-powered capabilities in November 2024 that integrated automated alert deduplication and AI-driven risk prioritisation across container security, cloud security posture management, and code security modules. The system's ability to correlate findings across previously separate Prisma Cloud modules and reduce alert volumes by greater than 60 percent while increasing the precision of critical risk identification addressed the alert fatigue problem that security teams at large enterprise customers identified as the primary operational barrier to effective CNAPP utilisation. The contextual risk graph connecting misconfigurations, vulnerable packages, exposed secrets, and runtime behaviours enabled security teams to prioritise the comparatively small number of exploitable risk combinations from the much larger number of individual findings that prior-generation tools produced in isolation.

Market Size and Forecast

-

Market Size in 2026E: USD 12.27 Billion

-

Market Size by 2035: USD 71.92 Billion

-

CAGR: 21.72% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Cloud-Native Application Protection Platform Market - Request Free Sample Report

Cloud-Native Application Protection Platform Market Trends

-

AI-powered risk analysis is enhancing CNAPP platforms by automating attack path mapping and prioritizing cloud-native security risks.

-

Shift-left security adoption is integrating CNAPP capabilities into CI/CD pipelines and infrastructure-as-code workflows to detect vulnerabilities before deployment.

-

Agentless CNAPP architectures are gaining traction by enabling rapid cloud visibility and security coverage without deploying endpoint agents.

-

Data Security Posture Management (DSPM) capabilities are expanding CNAPP functionality to protect sensitive cloud data across storage, databases, and data pipelines.

-

Zero Trust security integration is driving CNAPP evolution through identity-based access controls, continuous verification, and micro-segmentation for cloud-native environments.

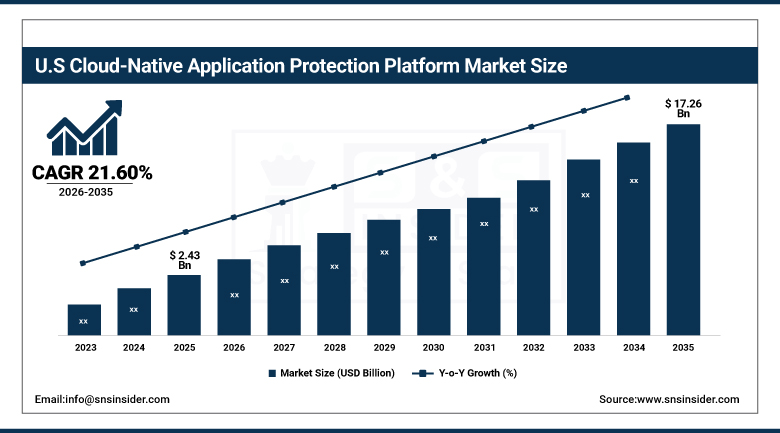

The U.S. Cloud-Native Application Protection Platform Market Outlook

The U.S. Cloud-Native Application Protection Platform Market was valued at approximately USD 2.43 Billion in 2025 and is expected to reach approximately USD 17.26 Billion by 2035, growing at a CAGR of approximately 21.60%.

The United States leads the global CNAPP market through the combination of the world's largest enterprise cloud infrastructure deployment base, the most rigorous cybersecurity regulatory environment whose compliance requirements create measurable ROI for comprehensive cloud-native security investment, and the domestic headquarters presence of CNAPP platform leaders including Palo Alto Networks, Wiz, CrowdStrike, and Microsoft whose product development, go-to-market strategies, and customer success programmes are concentrated in the United States. The Biden Administration's Executive Order on Improving the Nation's Cybersecurity in 2021 and the subsequent CISA directives establishing zero trust architecture requirements for federal agencies created public sector CNAPP demand while simultaneously signalling cybersecurity investment priority to private sector chief information security officers.

Wiz Inc. achieved a USD 500 million annual recurring revenue milestone in 2024 faster than any enterprise software company in history, reaching the threshold in less than five years from founding. The company's agentless cloud security approach that provides complete cloud asset inventory and risk assessment within hours of deployment without requiring agent installation across workloads was the commercial differentiator that enabled Wiz to displace established agent-based CWPP vendors at large enterprise and hyperscaler customers whose cloud environment scale made comprehensive agent deployment operationally impractical. Microsoft's USD 32 billion acquisition offer for Wiz in July 2024, though declined by Wiz management, validated CNAPP platform strategic value at the highest acquisition price ever offered for a cybersecurity company and accelerated competitive investment across the CNAPP vendor landscape.

Cloud-Native Application Protection Platform Market Segment Analysis

-

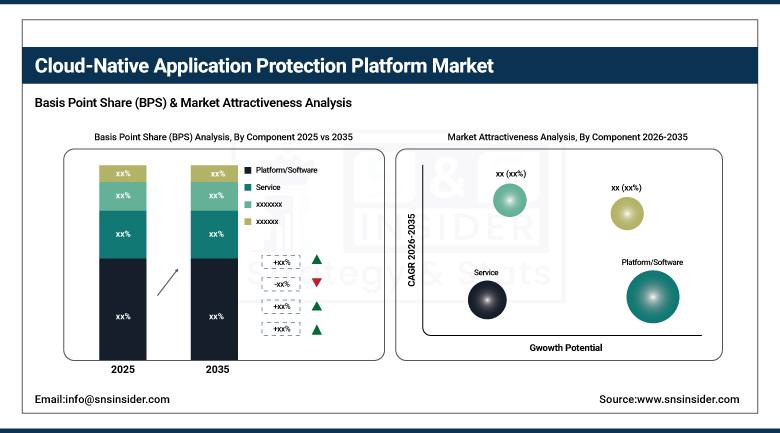

By Component, the platform/software segment dominated the CNAPP market with approximately 70.00% share in 2025, while the services segment is the fastest growing component during 2026 to 2035.

-

By Cloud Type, the hybrid cloud segment dominated the CNAPP market with approximately 80.00% projected share in 2025, while the public cloud segment is growing at the fastest rate during 2026 to 2035.

-

By Deployment, the SaaS segment dominated the CNAPP market with 61.70% share in 2025, while the PaaS-integrated segment is the fastest growing deployment model at a CAGR of 23.50%.

-

By Industry Vertical, the BFSI segment dominated the CNAPP market in 2025, while the healthcare & life sciences segment is the fastest growing vertical during 2026 to 2035.

By Component, software dominates, services grow fastest

Platform and software generated approximately 70.00% of CNAPP market revenue in 2025, reflecting the recurring licence and subscription revenue from CNAPP platform deployments at enterprise customers whose contractual terms range from one to three year agreements that create visible forward revenue under the SaaS and subscription delivery model that dominates CNAPP commercial packaging. The platform revenue concentration reflects the market dynamic in which large enterprises deploy comprehensive CNAPP platforms rather than individual modules, with annual contract values at Fortune 500 customers frequently exceeding USD 1 million when full platform capability including cloud security posture management, cloud workload protection, container security, and shift-left development security modules are included in a consolidated enterprise agreement.

Services are growing fastest as CNAPP platform complexity and the scarcity of certified cloud security professionals create strong demand for vendor professional services, managed detection and response services, and system integrator implementation support that collectively expand the addressable revenue opportunity per customer well beyond software licence value.

By Industry Vertical, BFSI dominates, healthcare grows fastest

BFSI retained the dominant industry vertical position in 2025, driven by the combination of the most stringent cloud security regulatory requirements of any industry sector, the highest data sensitivity of protected assets including customer financial data and transaction records whose exposure creates direct regulatory liability, and the most sophisticated cloud security investment culture among large financial institutions whose security operations teams have the expertise to deploy and operate comprehensive CNAPP platforms effectively.

Healthcare and life sciences is growing fastest as the progressive migration of electronic health records, clinical imaging, genomics data, and patient engagement applications to cloud environments creates growing HIPAA compliance and patient data protection obligations that CNAPP platforms are specifically positioned to satisfy. The healthcare sector's historically lagging cloud security maturity relative to financial services creates both greater urgency for remediation and larger commercial opportunity for CNAPP platform deployments that bring healthcare cloud environments to the protection standard that patient data sensitivity demands.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

27.84% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

24.73% |

|

Latin America |

Brazil |

43.84% |

North America Cloud-Native Application Protection Platform Market Insights

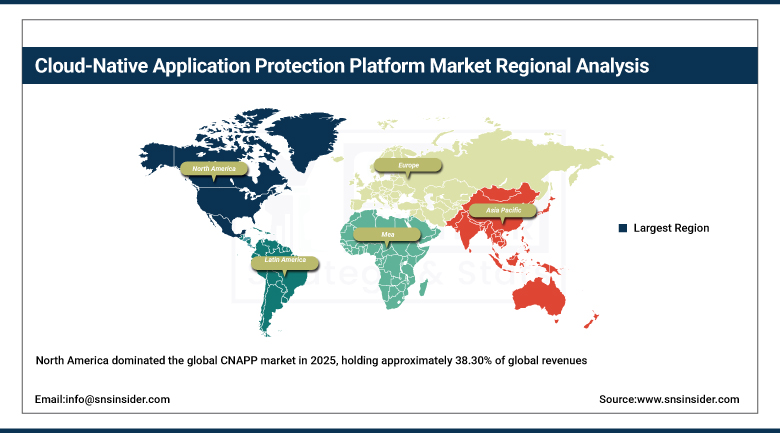

North America dominated the global CNAPP market in 2025, holding approximately 38.30% of global revenues. The United States accounts for approximately 84.73% of regional revenue through the world's largest enterprise cloud infrastructure deployment, the domestic headquarters of leading CNAPP vendors, and the most comprehensive cybersecurity regulatory compliance environment whose federal and state requirements create non-discretionary CNAPP investment mandates. The concentration of financial services, healthcare, technology, and government cloud deployments in the United States sustains the highest per-enterprise CNAPP platform value globally, where comprehensive multi-module deployments at major financial institutions and cloud providers generate annual contract values that significantly exceed equivalent deployments in other regions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cloud-Native Application Protection Platform Market Insights

GDPR's data protection obligations, which impose accountability for the security of personal data processed in cloud environments, create a compliance-driven CNAPP investment mandate across European enterprises whose data controller and processor obligations under the regulation require demonstrable cloud security controls. The EU's NIS2 Directive expanding cybersecurity requirements across critical infrastructure sectors and the DORA regulation imposing digital operational resilience requirements on financial services institutions each amplify cloud security investment obligations that CNAPP platforms are positioned to satisfy through their integrated compliance monitoring and evidence reporting capabilities. Germany, France, and the Netherlands lead European revenues through their concentration of financial services, technology, and critical infrastructure cloud deployments.

Asia Pacific Cloud-Native Application Protection Platform Market Insights

Asia Pacific is the fastest-growing regional CNAPP market, projected to expand at a CAGR of approximately 23.80% through 2035. China accounts for approximately 38.47% of Asia Pacific revenues through its large enterprise cloud adoption base, growing data security regulation under the Personal Information Protection Law and Cybersecurity Law, and significant domestic cloud deployment by financial services and technology companies whose workloads require cloud-native security frameworks. India, Japan, Singapore, South Korea, and Australia each contribute meaningful regional demand through growing cloud adoption in regulated industries and expanding cybersecurity regulatory frameworks that are progressively aligning with international cloud security standards.

MEA & Latin America Cloud-Native Application Protection Platform Market Insights

Middle East and Latin America represent growing CNAPP markets where cloud adoption acceleration and tightening cybersecurity regulatory requirements are creating expanding demand. The UAE leads MEA revenues at approximately 24.73% of the regional total through its advanced cloud infrastructure adoption, concentration of financial services and government cloud deployments, and National Cybersecurity Strategy requirements that mandate cloud security standards for critical national infrastructure operators. Saudi Arabia's increasing cloud adoption in NEOM and Vision 2030 digital transformation programmes creates growing CNAPP demand across both private and public sector cloud deployments. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its financial services sector's cloud-native modernisation, LGPD data protection compliance requirements, and growing technology sector cloud deployment.

Growth Drivers: Multi-cloud complexity creating security visibility gaps and regulatory compliance requirements imposing cloud security controls across financial services, healthcare, and critical infrastructure sectors

Enterprise multi-cloud architectures, in which organisations simultaneously deploy workloads across Amazon Web Services, Microsoft Azure, and Google Cloud Platform to avoid vendor lock-in and optimise workload placement, create security management complexity that single-cloud or on-premise security architectures were not designed to address. Each additional cloud environment introduces unique security configurations, identity management systems, billing models, and native security tooling whose integration into a coherent enterprise security posture requires cross-cloud normalisation, correlation, and policy enforcement capabilities that only platform-level CNAPP solutions can provide. Regulatory compliance frameworks imposing cloud security controls are expanding globally, with financial services regulation including Basel IV operational resilience requirements, healthcare HIPAA security rule updates, and critical infrastructure cybersecurity directives.

Restraints: Platform complexity and the requirement for skilled cloud security professionals to configure, operate, and respond to CNAPP alerts create deployment and operational barriers for mid-market enterprises and resource-constrained security teams.

CNAPP platforms in their full capability configuration generate contextual risk graphs, cloud asset inventories, runtime alerts, compliance findings, vulnerability reports, and shift-left code security findings whose aggregate information volume requires security analyst expertise to prioritise, investigate, and remediate effectively. Organisations whose security operations teams lack cloud-native expertise may find comprehensive CNAPP deployment creates alert volumes and operational requirements that exceed their response capacity, reducing the realised security benefit below the platform's theoretical protection capability. The global shortage of cloud security professionals with Kubernetes, container, and cloud infrastructure expertise creates a staffing constraint that limits effective CNAPP utilisation at organisations whose security teams were established for traditional on-premise security operations.

Opportunities: Managed CNAPP services and AI-automated remediation capabilities represent transformative commercial opportunities that extend CNAPP platform accessibility to the large mid-market enterprise segment

Managed CNAPP services delivered by cloud security managed service providers who operate the platform, triage alerts, investigate findings, and execute remediation on behalf of enterprise customers are creating a commercial model that extends comprehensive cloud-native protection to mid-market enterprises whose internal security teams lack the cloud expertise or capacity to operate full CNAPP platforms independently. The managed service model transforms CNAPP from a platform requiring substantial internal investment in tooling and expertise into a cloud security outcome delivered as a monthly subscription, aligning cost with security value in a model accessible to the much larger population of enterprises below the Fortune 1000 scale at which internal CNAPP operations become economically justifiable. AI-automated remediation capabilities that automatically remediate identified misconfigurations, rotate exposed credentials, and isolate compromised workloads without security analyst involvement.

Recent Developments:

-

2025: Wiz Inc. expanded its CNAPP platform with AI Security capabilities including detection of AI model exposure, training data access risks, and AI pipeline misconfigurations, addressing the rapidly emerging security requirements of enterprises deploying large language model and generative AI applications in cloud environments without established security frameworks.

-

2025: Trend Micro extended its partnership with Google Cloud to advance AI-driven cybersecurity, integrating Trend Micro Vision One Sovereign and Private Cloud with Google Cloud Assured Workloads to strengthen protection of data in public, hybrid, and air-gapped environments for regulated enterprise customers.

-

2024: Palo Alto Networks released AI-driven alert deduplication within Prisma Cloud that reduced alert volumes by over 60 percent while improving critical risk identification precision, directly addressing the alert fatigue problem that security teams identified as the primary operational barrier to effective CNAPP platform utilisation at enterprise scale.

Cloud-Native Application Protection Platform Market Key Players:

-

Palo Alto Networks Inc. (Prisma Cloud)

-

Wiz Inc.

-

Microsoft Corporation (Defender for Cloud)

-

Orca Security Ltd.

-

Check Point Software Technologies Ltd.

-

Fortinet Inc.

-

Zscaler Inc.

-

Tenable Holdings Inc.

-

Lacework Inc.

-

Trend Micro Inc.

-

Sysdig Inc.

-

Qualys Inc.

-

IBM Corporation

-

Forcepoint LLC

-

Radware Ltd.

-

Sophos Group PLC

-

Snyk Ltd.

-

Ermetic Ltd. (Tenable)

Cloud-Native Application Protection Platform Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.07 Billion |

| Market Size by 2035 | USD 71.92 Billion |

| CAGR | CAGR of 21.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Platform/Software, Services) • By Cloud Type (Public Cloud, Private Cloud, Hybrid Cloud) • By Deployment (SaaS, PaaS, IaaS) • By Industry Vertical (BFSI, Healthcare & Life Sciences, IT & Telecommunications, Retail & E-Commerce, Government, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Palo Alto Networks Inc. (Prisma Cloud), Wiz Inc., CrowdStrike Holdings Inc., Microsoft Corporation (Defender for Cloud), Orca Security Ltd., Check Point Software Technologies Ltd., Fortinet Inc., Zscaler Inc., Tenable Holdings Inc., Lacework Inc., Aqua Security Software Ltd., Trend Micro Inc., Sysdig Inc., Qualys Inc., IBM Corporation, Forcepoint LLC, Radware Ltd., Sophos Group PLC, Snyk Ltd., and Ermetic Ltd. (Tenable) |

Frequently Asked Questions

The primary growth factors are multi-cloud architecture adoption creating security visibility gaps that fragmented point tools cannot address, regulatory compliance requirements imposing cloud security controls across BFSI, healthcare, and critical infrastructure.

The Cloud-Native Application Protection Platform Market was valued at USD 10.07 Billion in 2025.

The Cloud-Native Application Protection Platform Market is expected to grow at a CAGR of 21.72% from 2026 to 2035.

Get in Touch