Data Center Generator Market Report Scope & Overview:

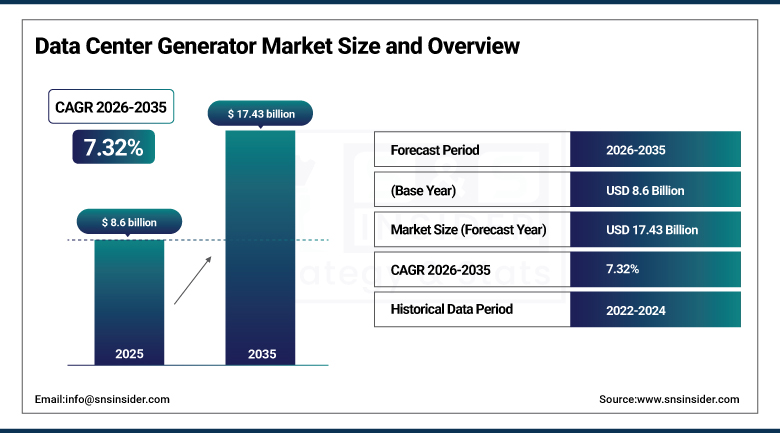

The Data Center Generator Market was valued at USD 8.6 billion in 2025 and is expected to reach USD 17.43 billion by 2035, growing at a CAGR of 7.32% from 2026-2035.

The data center generator market is growing owing to the rising requirement for reliable power supply in hyperscale and colocation data centers. Higher data traffic, cloud computing, artificial intelligence operations, and digitization trends are causing constant expansion in data centers around the world. Power outage concerns and the necessity for backup are fueling the adoption of generators in the sector. Edge data centers along with higher demands for uptime are expected to positively impact market performance.

According to the U.S. Department of Energy (DOE), data centers already consume about 1–2% of total global electricity demand, and in the U.S. alone, demand is projected to increase significantly as AI workloads accelerate, putting additional pressure on grid reliability and backup power systems.

Data Center Generator Market Size and Forecast

-

Data Center Generator Market Size in 2025: USD 8.6 Billion

-

Data Center Generator Market Size by 2035: USD 17.43 Billion

-

CAGR: 7.32% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Data Center Generator Market - Request Free Sample Report

Data Center Generator Market Trends

-

Increasing demand for reliable and uninterrupted power supply in hyperscale and colocation data centers.

-

Expansion of cloud services and digital transformation initiatives driving higher backup power requirements.

-

Growth in edge computing and modular data centers requiring flexible generator solutions.

-

Adoption of advanced diesel and gas generators with enhanced fuel efficiency and lower emissions.

-

Rising emphasis on power redundancy and resiliency to minimize costly downtime.

-

Integration of sustainable and low-carbon generator technologies in response to regulatory and ESG goals.

-

Increasing investments by cloud service providers and enterprises in robust power infrastructure.

-

Rising focus on predictive maintenance and smart generator monitoring systems for enhanced uptime.

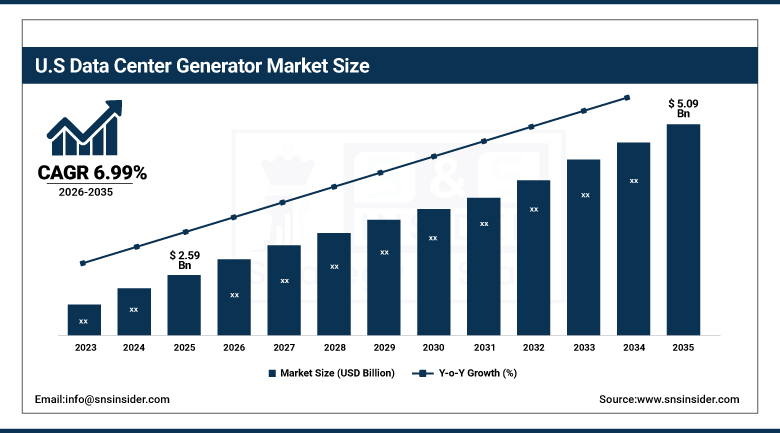

U.S. Data Center Generator Market was valued at USD 2.59 billion in 2025 and is expected to reach USD 5.09 billion by 2035, growing at a CAGR of 6.99% from 2026-2035.

In the United States, the data center generator market will grow because there is a growing need for power backup solutions owing to the expansion of data centers caused by cloud computing and AI services. The growing importance of reliability, concerns related to grid reliability, and energy-efficient generator technology will also boost market growth.

Data Center Generator Market Segment Highlights

-

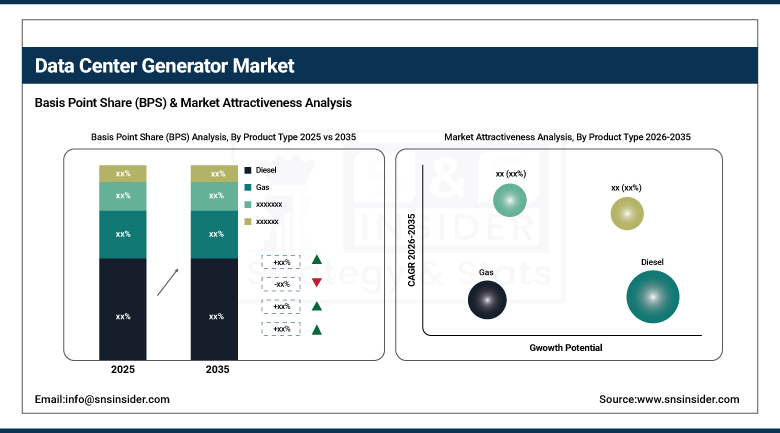

By Product Type, Diesel Generators segment dominated the Data Center Generator Market in 2025 with around 70% share; Gas Generators segment is the fastest growing during the forecast period.

-

By Capacity, Sub-1 MW Generators segment dominated the Data Center Generator Market in 2025 with around 54% share; 1–2 MW Generators segment is the fastest growing during the forecast period.

-

By Tier Standards, Tier III Data Centers segment dominated the Data Center Generator Market in 2025 with a significant share; Tier IV Data Centers segment is the fastest growing during the forecast period.

Data Center Generator Market Segment Analysis

By Product Type, Diesel Generators Lead While Gas Generators Gain Momentum

Diesel generators dominate the data center generator market share in 2025 owing to their excellent performance, fast startup, and reliability when specific loads are heavy. Diesel generators in hyperscale data centers are common to ensure uninterrupted uptime during power outages. Although environmentalists are pressurizing these companies to go green, their already established infrastructure and reliability will sustain high fuel demand. Their leadership will continue for several more years owing to their clean diesel technologies innovations.

The gas generators were expected to have the highest CAGR during the forecast period from 2026-2033 owing to their cost efficiency and environmental benefits over diesel generators. Their adoption would be increasingly growing owing to their adoption in sustainable data centers. Growing use of green infrastructure coupled with growing accessibility and affordability of natural gas would drive their growth especially among areas that have strict environmental rules.

By Capacity, Sub-1 MW Generators Dominate as 1–2 MW Segment Accelerates Growth

<1 MW Segment Captures the largest Market Share of Data Center Generators in the Prediction Period 2025 by Contributing 54%. The preference of these generators is because of their applicability to edge and small-midsize data centers located in urban areas and developing countries. The generators are cost-effective and compact in nature for low-power backup applications in minimum space. The increasing use of generators of less than 1 MW capacity will rise because of the expansion of the distributed IT infrastructure and micro data centers.

The 1 MW to 2 MW segment is anticipated to register the highest growth rate over the forecasted period, as these medium-sized enterprise data centers and colocation centers are likely to get installed within the same range of capacity. These generators deliver an optimal combination of performance and cost required for scalability in terms of IT infrastructure. It is expected to experience a phenomenally high growth rate owing to the growing need for modular data centers and hybrid clouds in the predicted period.

By Tier Standards, Tier III Data Centers Hold Majority Share, Tier IV Expands Rapidly

Tier III Data Center Generators led the data center generators market in 2025 and contributed a substantial revenue share because of their economical operation compared to Tier IV. These are highly prevalent in corporations and colocation services that are trying to balance out their costs with reliability. In the end, the rising demand for scalable and robust infrastructure owing to rapid digitalization will drive the adoption of Tier III systems in developed as well as developing regions.

Tier IV data center category will be growing at the fastest compound annual growth rate during the forecast period owing to their importance regarding mission criticality and a fault-tolerant design. This data center category is preferred by sectors such as banking, health care, and even the hyperscale cloud companies. The rise in the level of cybersecurity threats and the demand for service-level agreements will drive the adoption of this market in regions that value infrastructural reliability.

Data Center Generator Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

92.4% |

|

Europe |

United Kingdom |

25.3% |

|

Asia Pacific |

Australia |

9.8% |

|

Middle East & Africa |

UAE |

14.6% |

|

Latin America |

Brazil |

51.7% |

North America Data Center Generator Market Insights

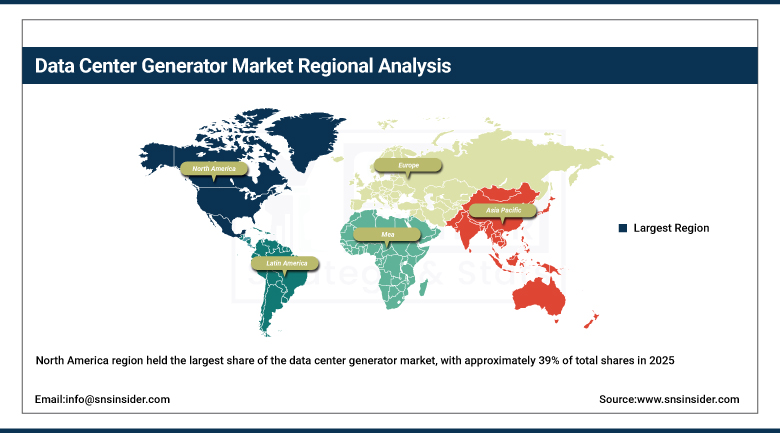

The North America region held the largest share of the data center generator market, with approximately 39% of total shares in 2025. The fast-growing trend of the construction of hyperscale data centers and colocation data centers is fueling the rise of the region’s dominance in the market. The rising adoption of cloud computing services, artificial intelligence, and digitalization is driving the demand for reliable power supply. The frequent power grid failures and weather extremities are also propelling the market towards reliability.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Data Center Generator Market Insights

The Asia-Pacific region is expected to grow at the fastest CAGR of 8.8% in the data center generator market owing to its fast digitalization and increase in cloud-based services. The rise in investment in hyperscale and edge data centers in emerging countries is contributing to the demand for backup power generators in this market. Factors like higher internet connectivity, rising data consumption, and usage of AI and IoT technologies are also supporting market growth. Moreover, government policies and investments from foreign players are helping in the expansion of this market.

Europe Data Center Generator Market Insights

The Europe data center generator market continues to experience robust growth, propelled by the rising need for dependable backup power among rapidly-growing cloud and colocation centers. The rising usage of digital solutions, artificial intelligence applications, and edge computing will improve infrastructure needs. Stringent environmental laws are prompting the use of fuel-efficient and gas-powered generators. Moreover, the growing trend of investing in sustainable data centers and upgrading existing data centers is further propelling the growth of the Europe data center generator market.

Middle East & Africa and Latin America Data Center Generator Market Insights

The data center generator market in Middle East & Africa and Latin America is developing consistently because of growing digitization, increased connectivity, and enhanced cloud computing. The deployment of hyperscale and colocation data centers is fueling the need for dependable backup generators. Power supply inconsistencies in some areas act as additional catalysts for generator usage. Moreover, efforts by governments to upgrade their digital infrastructure, coupled with foreign investments, are helping to develop the markets in these regions.

Data Center Generator Market Growth Drivers:

-

Growing Demand for Data Reliability Drives Surge in Backup Generator Investments

The increasing use of data worldwide and the increasing dependence on cloud computing technology have led to an increase in the need for high availability data centers. Backup generators are required in case there is no power supply for any prolonged period. With more businesses moving towards a multi-cloud environment and the Internet being used extensively with IoT and video streaming services, reliability has become crucial. Therefore, data center operators are investing heavily in diesel and gas generators in order to avoid downtime, which could lead to losses in revenue and disruptions in data transmission.

Data Center Generator Market Restraints:

-

Strict Environmental Regulations Curb Diesel Generator Adoption

The foremost restriction affecting the data center generator market is the strict regulatory measures in place regarding carbon emissions, particularly those generated by diesel generators. The shortages of conventional fossil fuel-based backup power generation facilities can be attributed to the push for alternative power sources. This is because companies will be faced with high costs when implementing the regulatory measures and hence they will need to come up with more efficient power generating units which may cost them more or get phased out. In addition, the increasing societal pressure against carbon footprints might make firms think twice about using diesel generators and hence limit their market expansion over the forecast period.

For instance, in 2023, the Indian government implemented the CPCB IV+ emission standards for diesel generators up to 800 kW, achieving a 90% reduction in particulate matter and nitrogen oxide emissions compared to previous norms.

Data Center Generator Market Opportunities:

-

Expansion of Hyperscale and Edge Data Centers Boosts Generator Demand

With the huge expansion of hyperscale data centers in the top cloud companies and the rapid rise of edge data centers for latency-sensitive applications, the development in the generator industry has a lot of potential in grabbing hold.' Backup power is critical for data centers that will have to rely on high reliability and scalability, along with modularity. Sectors that are planning to incorporate AI, 5G technology, and real-time data analysis are going to give rise to the need for distributed computing, hence requiring edge data centers that will in turn require robust back-up. In essence, the emerging environment will offer many opportunities to generators that provide efficient and environmentally friendly products.

Recent Developments:

-

In 2024, Caterpillar expanded its data center generator portfolio with enhanced fuel-efficient and low-emission diesel generator sets designed to meet stricter environmental regulations while maintaining high reliability.

-

In 2024, Generac expanded its commercial and industrial generator lineup to support modular data center deployments with improved remote monitoring and load management capabilities.

-

In 2025, Cummins introduced next-generation gas generator solutions optimized for data centers, focusing on lower carbon emissions and reduced operational costs.

Key Players

Some of the Data Center Generator Market Companies

-

Caterpillar Inc.

-

Cummins Inc.

-

Generac Power Systems, Inc.

-

Kohler Co. (Rehlko)

-

Rolls-Royce Power Systems (MTU Onsite Energy)

-

ABB Ltd.

-

Atlas Copco AB

-

Aggreko plc

-

HITEC Power Protection

-

Himoinsa

-

Aksa Power Generation

-

Mitsubishi Heavy Industries

-

INNIO Group

-

Deutz AG

-

Kirloskar Oil Engines Ltd.

-

Yanmar Holdings Co., Ltd.

-

Perkins Engines Company Limited

-

Wartsila Corporation

-

Doosan Portable Power

-

FG Wilson

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.6 Billion |

| Market Size by 2035 | USD 17.43 Billion |

| CAGR | CAGR of 7.32% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Diesel, Gas, Others) • By Capacity (<1 MW, 1–2 MW, >2 MW) • By Tier Standards (Tier I & II, Tier III, Tier IV) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Caterpillar Inc., Cummins Inc., Generac Power Systems, Inc., Kohler Co. (Rehlko), Rolls-Royce Power Systems (MTU Onsite Energy), ABB Ltd., Atlas Copco AB, Aggreko plc, HITEC Power Protection, Himoinsa, Aksa Power Generation, Mitsubishi Heavy Industries, INNIO Group, Deutz AG, Kirloskar Oil Engines Ltd., Yanmar Holdings Co., Ltd., Perkins Engines Company Limited, Wärtsilä Corporation, Doosan Portable Power, and FG Wilson. |

Frequently Asked Questions

Ans: North America dominated the Data Center Generator Market in 2025.

Ans: The Diesel Generators segment dominated the Data Center Generator Market in 2025.

Ans: Growing dependence on cloud computing and rising global data usage are increasing demand for high-availability data centers, driving strong investment in backup generators for uninterrupted operations.

Ans: The Data Center Generator Market was valued at USD 8.6 billion in 2025.

Ans: The Data Center Generator Market is expected to grow at a CAGR of 7.32% from 2026 to 2035.

Get in Touch