Chemicals Digitalization Market Report Size:

Get More Information on Chemicals Digitalization Market - Request Free Sample Report

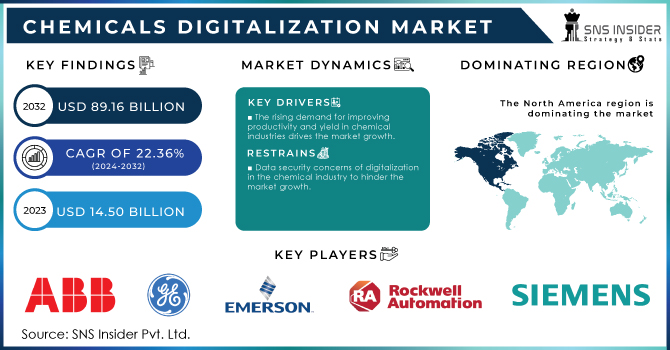

The Chemicals Digitalization Market Size was valued at USD 14.50 billion in 2023 and is expected to reach USD 89.16 billion by 2032 and grow at a CAGR of 22.36% over the forecast period 2024-2032.

Increasing adoption of data analytics, automation, and other technological advancements in business on a global scale has growing the demand for chemical digitalization market. Manufacturers in the chemicals sector benefit from increased digitalization in terms of customer satisfaction, manufacturing capacity, and competitiveness which drive the market growth.

In April 2024, Hitachi Energy announced to its increase its global transformer manufacturing by spending an USD 1.5 billion. This investment span across Europe, Asia, and North America.

Digital twin in chemicals can be a game-changer in this pursuit by optimizing resource usage, minimizing waste, and enhancing safety measures. With these driving forces and government support for research and development in digital manufacturing processes, the chemicals digitalization market is poised for a prosperous future.

The demand for more efficient and continuous manufacturing techniques, the use of cutting-edge digital technology, and improved batch production scheduling are some of the factors propelling the expansion of the digital chemicals market. Moreover, the demand for specialty chemical digitalization globally is forecasted to rise as a result of the substantial increase being seen by a number of end-user industries within the chemical digitalization industry in the region, including water treatment, cars, electronics, and personal care items.

In the chemical industry, digitalization is a revolution in progress such as, data and analytics are the key source, of uncovering opportunities for improvement. Manual tasks are on the endangered list as automation takes the wheel, supercharging productivity. Digitalization fosters a collaborative ecosystem with industry partners, suppliers, and customers. Sharing data, knowledge, and resources through digital platforms fuels innovation and ignites the engine of progress. The verdict is clear – digitalization is a transformative force for the chemical industry.

Market Dynamics

Drivers

-

The rising demand for improving productivity and yield in chemical industries drives the market growth.

Chemical companies are locked in a constant battle to maximize output and efficiency. This relentless pursuit of enhanced productivity and yield is a critical factor driving the surging growth of the chemical’s digitalization market. By deploying digital tools and technologies, chemical companies can unlock substantial gains in these areas. Data analytics and automation act as powerful weapons in this arsenal, identifying areas for improvement and streamlining operations. This translates to churning out more product in less time, or extracting a greater percentage of the desired product from a chemical reaction. In essence, digitalization empowers chemical companies to achieve greater output while optimizing resource consumption, fueling the market's impressive growth trajectory.

-

Rapidly increasing advanced digital technologies and innovation in the market has been drive the market growth.

The chemicals digitalization market is on a tear, propelled by the immediate pace of innovation in advanced new technologies in chemical and the relentless march of ingenuity within the industry. a constant stream of cutting-edge tools is flooding the market, empowering chemical companies with an ever-expanding toolkit to outmaneuver inefficiency. from the strategic deployment of artificial intelligence to the integration of machine learning and the internet of things (iot), these technologies are revolutionizing the way chemicals are produced. but the plot thickens. the market itself is a crucible of creativity, where companies are constantly forging new pathways to exploit the potential of these digital advancements. this symbiotic relationship between powerful instruments and ingenious applications is propelling the chemicals digitalization market towards a prosperous future.

Restrain

-

Data security concerns of digitalization in the chemical industry to hinder the market growth

Digital transformation in the chemical industry has opportunities but have lots of challenge. As chemical plants become data repositories overflowing with confidential formulas, intricate production processes, and potentially sensitive customer information, they morph into a tempting target for cybercriminals. These digital adversaries may launch cyberattacks to steal this valuable data, fueling industrial espionage and crippling a competitor's edge. In essence, the data that fuels the efficiency gains of digitalization also presents a security minefield that chemical as a service companies must skillfully disarm.

Market Segmentation

By Product

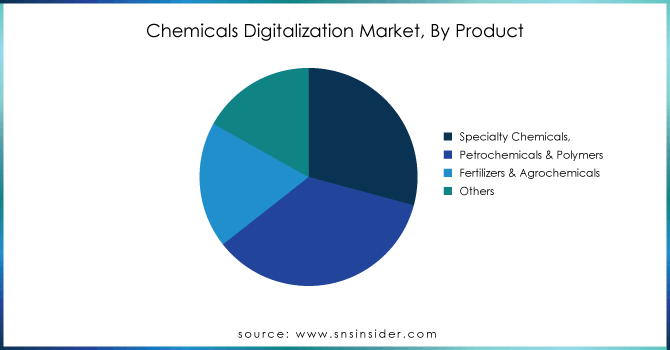

The petrochemicals & polymers held the largest market share approx. 35.20% in Product segment in 2023. Due to many industries including plastics, packaging, clothing, electronics, medical devices and detergents, rely heavily on these products. Most beverages and personal hygiene products are packaged in polyethylene terephthalate (PET) bottles, which are made from ethylene and paraxylene Also, the automotive industry relies heavily on polymers and plastics for lightweight, supply fuel efficiency and reduced emissions.

The specialty chemicals segment covers a wide range of products, including adhesives and coatings, agricultural chemicals, construction and electronic chemicals, flavours and fragrances, polymers, and catalysts, etc. These chemicals are used to provide durability, performance and excellent aesthetics. They are also used in a variety of applications to provide specific applications in infrastructure.

Get Customized Report as per your Business Requirement - Request For Customized Report

By Process

The manufacturing segment hold the largest revenue share in chemicals digitalization market in 2023. Digitalization is essential for increasing productivity, assuring product quality, and streamlining industrial processes. It may improve production parameters, cut waste, and boost overall productivity by implementing modern process control systems and real-time monitoring.

The R&D program segment of the global chemical labelling market focuses on innovation, product development and enhancement of existing chemical products. Digitization has transformed R&D through the use of virtual simulations, data analysis and machine learning algorithms. Computer-aided design and computer-aided engineering enable researchers to model and simulate chemical reactions, predict product performance, and optimize products before manufacturing physical testing.

Chemicals Digitalization Market Regional Analysis

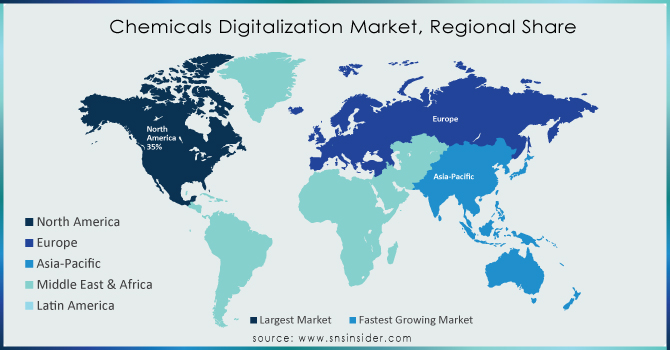

North America dominated the market and held the largest market share approx. 35.00% and is forecasted to grow at the quickest CAGR of 22.50% throughout the course of the forecast period. The region is known for its advanced technological infrastructure, strong research and development and strong pharmaceutical industry. Companies in North America are leading digital efforts, using technologies such as AI, IoT and data analytics to streamline processes, improve manufacturing efficiencies and improve supply chain management. Moreover, adoption of digital solutions in areas such as precision agriculture where farmers are leveraging data-driven insights to optimize crop production and resource utilization.

Europe held the second largest market in the chemical digitalization market. The facility is known for its emphasis on sustainability and environmental standards, as well as a strong pharmaceutical industry. The digitization of Europe drives efficiency and innovation across a range of medicines. This is primarily due to digital advances in areas such as green technology and sustainable medicine, which use digital to improve sustainable development and reduce negative impacts on the environment do UK businesses use digital technologies to enhance productivity, streamline supply chains and improve product quality.

Key Players

ABB Ltd., General Electric, Emerson Electric, Rockwell Automation, Siemens AG, Yokogawa Electric Corporation, Honeywell International, Mitsubishi Chemical Group Corporation, Solvay, Henkel Adhesives and others.

Recent Development:

-

In December 2023, Henkel Adhesives partnered with Tata Consultancy Services To boost efficiency, Henkel is standardizing ordering across subsidiaries and optimizing customer service processes.

-

In July 2023, Reliance Industries Limited signed the agreement with Brookfield Infrastructure and to invest in setting up and developing data centers around India.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 14.50 billion |

| Market Size by 2032 | US$ 89.16 Billion |

| CAGR | CAGR of 22.36 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Specialty Chemicals, Petrochemicals & Polymers, Fertilizers & Agrochemicals, and Others) •By Process (Manufacturing, R&D, Procurement, Supply Chain & Logistics, and Packaging) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB Ltd., General Electric, Emerson Electric, Rockwell Automation, Siemens AG, Yokogawa Electric Corporation, Honeywell International, Mitsubishi Chemical Group Corporation, Solvay, Henkel Adhesives and others. |

| Key Drivers | • The rising demand for improving productivity and yield in chemical industries drives the market growth |

| RESTRAINTS | • Data security concerns of digitalization in the chemical industry to hinder the market growth |

Frequently Asked Questions

The U.S. led the Chemicals Digitalization Market in North America region with highest revenue share in 2023.

Factor such as, data security concerns of digitalization in the chemical industry to hinder the market growth

The petrochemicals & polymers will grow rapidly in the Chemicals Digitalization Market from 2024-2032.

The expected CAGR of the global Chemicals Digitalization Market during the forecast period is 22.36%.

The Chemicals Digitalization Market was valued at USD 14.50 billion in 2023.

Get in Touch