Coffee Pods Market Report Scope & Overview:

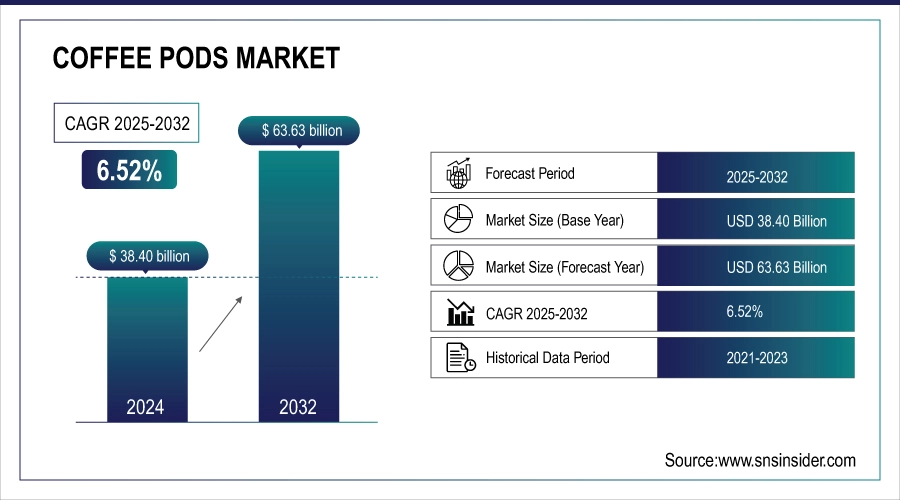

The Coffee Pods market size was valued at USD 38.40 billion in 2024 and is expected to reach USD 63.63 billion by 2032, growing at a CAGR of 6.52% over the forecast period of 2025-2032.

The coffee pods market continues to evolve as convenience, sustainability, and premium-at-home experiences drive product innovation. Compostable and plastic-free pods, in-capsule recycling, and single-origin premium lines are accelerating category diversification. Major coffee pod companies are launching circularity programs and private-label partnerships, while retailers expand assortment and subscription models. Initiatives such as Nespresso’s home-compostable capsule and Keurig’s k-rounds and k-cycle recycling support steady premiumization and convenience-led purchasing, fueling coffee pods market growth.

Supply resilience, regulatory changes, and consumption trends further influence the market. The International Coffee Organization estimated world coffee consumption at 177 million bags for 2023/24, highlighting strong demand. Meanwhile, EU deforestation regulations and Nestlé’s Nespresso sales of 3.1 billion Swiss francs in the first half of 2024 emphasize policy and corporate signals that impact coffee pods market analysis and strategy decisions.

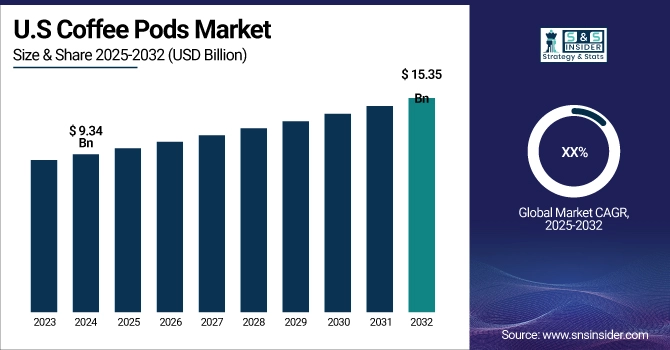

The U.S. leads this growth, holding a market share of around 79% and with a market size of USD 9.34 billion in 2024 and is projected to have a market size of USD 15.35 billion by 2032, with extensive use of coffee pod machines in households, supported by the National Coffee Association reporting a 60% rise in single-serve coffee consumption. Canada also shows robust market growth fueled by eco-friendly coffee packaging initiatives and expanding specialty coffee cafes.

Market Dynamics:

Drivers:

-

Rising consumer preference for Single-Serve Coffee Pods enhances market convenience and freshness

Consumers increasingly favor single-serve coffee pods for their convenience and ability to preserve coffee freshness. According to the National Coffee Association USA, over 60% of coffee drinkers prefer single-serve formats due to quick preparation and minimal waste. This demand pushes innovation in pod technology, expanding the Single-Serve Coffee Pods segment. Industry leaders like Nespresso continue launching new pod varieties, reflecting ongoing Coffee Pods Market Growth influenced by changing consumer lifestyles. This shift drives broader adoption globally and increases market penetration.

-

Expansion of Compostable Coffee Pods reflects sustainability trends in packaging

Sustainability efforts are driving demand for compostable coffee pods as consumers and governments push for eco-friendly packaging. The U.S. Environmental Protection Agency reported a 30% increase in composting initiatives since 2020, highlighting waste reduction priorities. Nestlé and Keurig have introduced certified Compostable Coffee Pods to align with environmental regulations and consumer preferences. This transition fosters innovation in biodegradable materials, positively affecting the Coffee Pods Market Size and encouraging adoption among eco-conscious consumers worldwide.

Restraints:

-

Limited compatibility of coffee capsules with multiple brewing machines restricts consumer choice

The fragmented nature of coffee machine compatibility limits the usability of many coffee capsules, frustrating consumers and restricting market potential. A Consumer Reports survey showed 40% of pod users experience compatibility issues, impacting satisfaction and repeat purchases. This lack of standardization in pod design inhibits the Coffee Pods Market Size by reducing cross-brand adoption. Brands are investing in proprietary systems, which, though profitable, limit consumer flexibility and slow broader market penetration for coffee capsules overall.

Segmentation Analysis:

By Category

Caffeinated held a dominant coffee pods market share of 70.20% in 2024 due to global consumption patterns favoring caffeine and premium blends. Leading brands like nespresso emphasize caffeinated pods, which align with consumer cultural habits and preferences. The international coffee organization confirms steady demand for caffeinated coffee worldwide. This dominance is reinforced by innovation in flavors and variety, securing caffeinated pods as the preferred choice in the coffee pods market for daily consumers.

Decaffeinated is the fastest growing with the highest CAGR of 6.61% during the forecast period over 2025 to 2032, driven by health-conscious consumers and regulatory influences. The us food and drug administration highlights increased demand for decaf products among sensitive populations. Major players like starbucks and keurig are expanding decaffeinated pod offerings with improved flavor profiles, encouraging adoption and boosting growth within the coffee pods market segment.

By Product Type

Hard/capsule pods held a dominant coffee pods market share of 63.90% in 2024 due to their convenience, compatibility, and variety. Plastic capsules dominate this subsegment by offering affordability and wide machine compatibility. Keurig and Nespresso’s innovation in plastic capsules has expanded consumer options, increasing adoption in homes and offices. The Specialty Coffee Association reports that single-serve convenience drives consumer preference, sustaining hard capsules’ leadership in the coffee pods market.

However, hard/capsule pods are the fastest growing with the highest CAGR of 6.46% during the forecast period from 2025 to 2032, driven by rising demand for compostable capsules. Environmental regulations like the EU packaging waste directive encourage eco-friendly alternatives. Companies such as Lavazza and Keurig are expanding compostable coffee pods lines to meet consumer sustainability expectations, which accelerates growth in this segment and supports the coffee pods market’s evolving eco-conscious trends.

By Flavor

Chocolate held a dominant coffee pods market share of 35.20% in 2024 due to consumer preference for indulgent, dessert-like coffee experiences. Brands like Lavazza and Nespresso lead with chocolate-flavored offerings, supported by Specialty Coffee Association data showing rising flavored pod demand. Continuous innovation and marketing have solidified chocolate pods as a favorite, driving their strong position within the coffee pods market’s flavor segment by appealing to a broad consumer base seeking variety and taste richness.

Vanilla is the fastest-growing with the highest CAGR of 7.15% during the forecast period from 2025 to 2032, driven by rising consumer interest in aromatic, subtle coffee flavors. The U.S. Department of Agriculture notes vanilla’s increasing presence in specialty coffee products. Companies like Keurig and Starbucks actively promote vanilla-flavored pods, responding to consumer demand for sophisticated varieties, thus accelerating growth and expanding the coffee pods market’s flavor diversity.

By Coffee Type

Blended coffee held a dominant coffee pods market share of 54.00% in 2024 due to its balanced flavor, consistency, and broad appeal. Industry leaders like Starbucks and JDE Peet’s prioritize blended pods to capture wide consumer segments. The International Coffee Organization highlights blended coffee’s popularity as a key driver of global consumption. This segment’s dominance reflects consumer preference for reliable taste and cost-effective options within the coffee pods market.

Specialty coffee is the fastest-growing segment with the highest CAGR of 6.76% during the forecast period from 2025 to 2032, driven by rising demand for unique single-origin and artisanal brews. Research from the Specialty Coffee Association shows consumers seeking premium, traceable coffee experiences. Companies like Blue Tokai and Nespresso invest in specialty pods to meet evolving tastes, fueling segment growth and increasing coffee pods market value.

By End Use

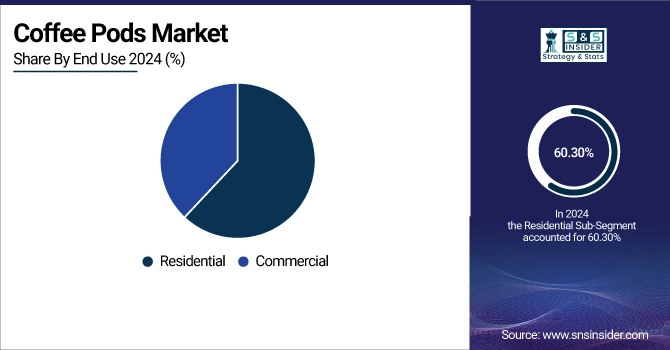

Residential held a dominant coffee pods market share of 60.30% in 2024 due to increase at-home coffee consumption fueled by remote work trends. The national coffee association reports growing home brewing habits supported by compact coffee machines compatible with pods. This residential preference drives product innovation and targeted marketing, securing its leading role in the coffee pods market through convenience and customization for individual consumers.

Commercial is the fastest growing with the highest CAGR of 6.59% during the forecast period over 2025 to 2032, driven by adoption in offices, cafes, and hotels. Workplace wellness initiatives and sustainability policies encourage pod usage. The specialty coffee association highlights increased demand for consistent, quality coffee in commercial settings, supporting growth in this segment and transforming the coffee pods market’s application landscape.

By Distribution Channel

B2c held a dominant coffee pods market share of 61.60% in 2024 due to the increasing popularity of grocery stores, supermarkets, and online direct-to-consumer channels. Online retail platforms like amazon and Walmart have enhanced accessibility, while consumer preference for at-home brewing continues to grow. According to the National Coffee Association, convenience and variety drive b2c segment dominance, reinforcing its position in the coffee pods market through expansive distribution and targeted marketing strategies.

B2b is the fastest-growing segment with the highest CAGR of 6.59% during the forecast period from 2025 to 2032, driven by expanding demand from cafes, hotels, and offices. Institutional buyers favor bulk purchases and premium coffee pods, supported by innovations in single-serve commercial machines. Workplace wellness programs and sustainability goals encourage office adoption. Specialty coffee association reports increased commercial pod usage, accelerating growth, and transforming the coffee pods market’s distribution dynamics.

Regional Analysis:

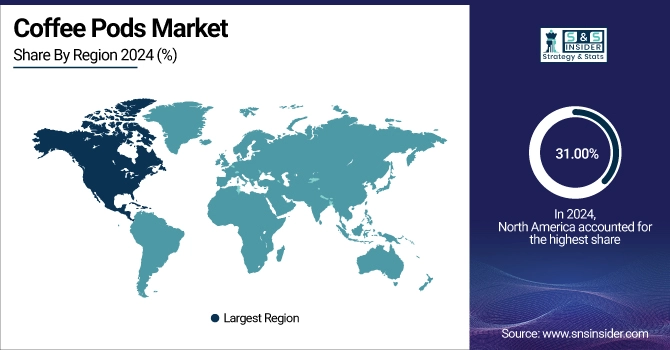

North America is the second-dominating region in the coffee pods market, holding a significant market share of 31.00%. This prominence is driven by widespread adoption of home brewing coffee trends and premium coffee products among consumers seeking convenience and quality.

Europe dominates the coffee pods market with a market share of 37.50%, owing to strong consumer preference for premium coffee products and stringent sustainability regulations that promote eco-friendly coffee packaging. Countries like Germany, Italy, and France lead the region, with Italy’s rich coffee culture bolstering capsule demand. The European Coffee Federation highlights increasing use of advanced coffee pod machines and growing environmental consciousness, further reinforcing Europe’s leadership. This mix of tradition and innovation drives continuous coffee pods market growth.

Asia Pacific is the fastest-growing region with the highest CAGR of 6.95%, propelled by rising disposable incomes, urbanization, and expanding home brewing coffee trends. China and India, with growing middle-class populations, are key contributors, adopting premium coffee products and modern coffee pod machines. Government initiatives supporting sustainable packaging encourage eco-friendly coffee packaging adoption. The Asia Pacific Coffee Association notes a surge in coffee culture, which underpins robust coffee pods market growth during the forecast period.

Key Players:

The major coffee pods market competitors include Blasercafé AG, Blue Tokai Coffee Roasters, Caffe Borbone S.r.l., Coffeeza, Difference Coffee Company, Dolce Gusto (Nestlé), Gruppo Gimoka S.p.A., Gruppo Izzo S.r.l., Illycaffè S.p.A., JDE Peet’s (Jacobs Douwe Egberts B.V.), Keurig Dr Pepper Inc. / Keurig Green Mountain Inc., Kimbo S.p.A., Labcaffè S.r.l., Lavazza Group (Luigi Lavazza S.p.A.), Nestlé S.A., Nespresso (Nestlé), Procaffé S.p.A., Segafredo Zanetti S.p.A., The J.M. Smucker Company, and The Kraft Heinz Company.

Recent Developments:

-

In March 2025, Nespresso opened its first boutique in New Delhi, entering the Indian market, planning expansion in metros, and increasing local coffee sourcing to support farmers and meet growing demand.

-

In April 2024, NatureWorks launched compostable coffee pods compatible with Keurig brewers, made from Ingeo PLA biopolymer, promoting sustainability while maintaining high-quality brewing performance and commercial production capabilities.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 38.40 billion |

| Market Size by 2032 | USD 63.63 billion |

| CAGR | CAGR of 6.52% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Category (Caffeinated, and Decaffeinated) •By Product Type (Soft Pods [Paper Filter Pods, and Mesh Filter Pods], Hard/Capsule pods [Plastic Capsules, Aluminum Capsules, and Compostable Capsules]) •By Flavor (Caramel, Chocolate, Hazelnut, Vanilla, and Others) •By Coffee Type (Single-Origin Coffee, Blended Coffee, and Specialty Coffee) •By End Use (Commercial, and Residential) •By Distribution Channel (B2B [Cafes, Hotels & Restaurants, Offices, Bakeries and coffee shops, and Others), B2C (Grocery Stores/Supermarkets, Hypermarkets, Convenience Stores, Online Retailers, Online Direct-to-Consumer (DTC), and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Blasercafé AG, Blue Tokai Coffee Roasters, Caffe Borbone S.r.l., Coffeeza, Difference Coffee Company, Dolce Gusto (Nestlé), Gruppo Gimoka S.p.A., Gruppo Izzo S.r.l., Illycaffè S.p.A., JDE Peet’s (Jacobs Douwe Egberts B.V.), Keurig Dr Pepper Inc. / Keurig Green Mountain Inc., Kimbo S.p.A., Labcaffè S.r.l., Lavazza Group (Luigi Lavazza S.p.A.), Nestlé S.A., Nespresso (Nestlé), Procaffé S.p.A., Segafredo Zanetti S.p.A., The J.M. Smucker Company, and The Kraft Heinz Company |

Frequently Asked Questions

Europe leads with 37.5% market share, followed by North America at 31%, driven by premium coffee culture and sustainability trends.

Hard/capsule pods dominate due to convenience and compatibility, with plastic and compostable capsules leading innovation.

Sustainability pushes adoption of compostable coffee pods and eco-friendly packaging, supported by regulations and consumer eco-awareness globally.

Demand is driven by convenience, single-serve preferences, premium home brewing trends, and sustainability initiatives promoting compostable coffee pods.

The coffee pods market was valued at USD 38.40 billion in 2024 and is projected to grow steadily due to rising demand and innovation through 2032.

Get in Touch