Cold Flow Improver Market Report Scope & Overview:

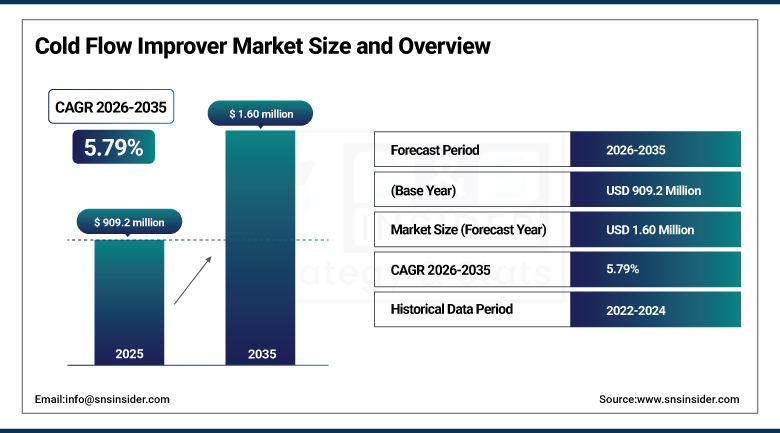

The Cold Flow Improver Market was valued at USD 909.2 Million in 2025 and is expected to reach USD 1.60 Billion by 2035, growing at a CAGR of 5.79% from 2026–2035.

The global cold flow improver market is advancing as the fuel additives sector addresses the critical operational challenge of wax crystallization in petroleum distillate fuels at low temperatures, where paraffin wax precipitates from diesel, lubricating oil, aviation fuel, and marine fuel create filter plugging, pour point elevation, and engine starting failures that cold flow improver polymers prevent by modifying wax crystal morphology to maintain fuel fluidity at temperatures below the cloud point. Cold flow improvers encompass ethylene vinyl acetate copolymers, polyalkyl methacrylates, polyalpha olefins, and polyacrylate chemistries whose backbone polymer structure, side chain length, and molecular weight distribution determine their effectiveness in specific fuel grade and operating temperature combinations.

In April 2023, Afton Chemical launched GreenClean 3, its most recent diesel fuel additive innovation combining cold flow improvement with advanced detergent technology for heavy-duty fleet and off-road vehicles equipped with the latest engine and emission control systems. The multifunctional formulation demonstrated the commercial direction of cold flow improver development toward performance packages combining wax crystal modification with deposit control, lubricity enhancement, and cetane improvement within a single treatment chemistry whose operational convenience and cost efficiency versus multi-additive programmes create specification preference among fleet operators managing diverse vehicle populations.

Market Size and Forecast

-

Market Size in 2026E: USD 961.7 Million

-

Market Size by 2035: USD 1.60 Billion

-

CAGR: 5.79% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Cold Flow Improver Market - Request Free Sample Report

Cold Flow Improver Market Trends

-

Biodiesel blending mandate expansion is creating growing cold flow improver demand as bio-blends exhibit higher cloud points than petroleum diesel.

-

Multifunctional additive package development combining cold flow improvement with detergency, lubricity, and corrosion inhibition is replacing multi-additive approaches.

-

Bio-based cold flow improver development using plant-derived polymer backbones is progressing under sustainable fuel additive research programmes.

-

Aviation fuel cold flow improver specification is tightening as advanced aircraft engines require tighter thermal stability and wax inhibition performance.

-

Marine fuel low-sulphur regulation compliance is driving cold flow improver adoption in VLSFO blends whose paraffinic content creates elevated cloud points.

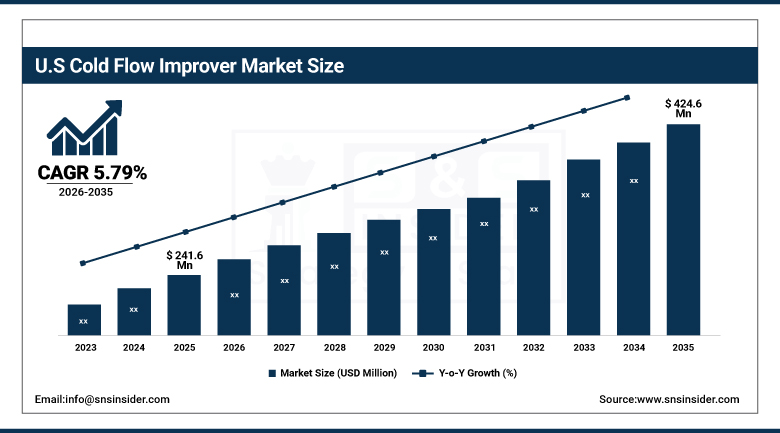

The U.S. Cold Flow Improver Market Outlook

The U.S. cold flow improver market was valued at approximately USD 241.6 Million in 2025 and is expected to reach approximately USD 424.6 Million by 2035, growing at a CAGR of approximately 5.79%.

The United States leads North American cold flow improver revenues through its large commercial diesel fleet operating in northern states’ extreme winter temperatures, the expanding renewable diesel and biodiesel mandate creating higher-cloud-point fuel blends requiring systematic additive treatment, and the petroleum refining sector’s additive specification for winter diesel operability. BASF, Afton Chemical, and Innospec sustain U.S. market leadership through their comprehensive cold flow improver portfolios validated across commercial fleet diesel specifications.

In 2024, BASF SE expanded its Keroflux cold flow improver product range with new polymer grades optimized for high-blend renewable diesel and hydrotreated vegetable oil mixtures, providing effective wax modification in HVO and FAME biodiesel blends whose branched paraffinic composition creates different cloud point and wax crystal morphology characteristics requiring specifically engineered polymer structures compared to conventional petroleum diesel cold flow improver chemistries.

Cold Flow Improver Market Segment Analysis

-

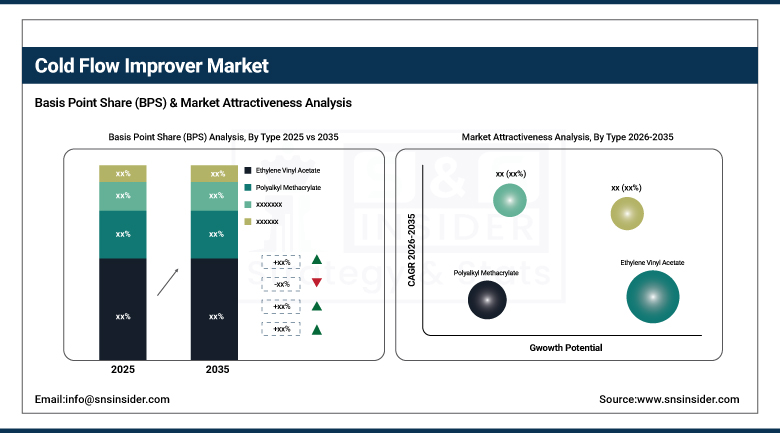

By Type, ethylene vinyl acetate (EVA) segment dominated the cold flow improver market with approximately 37.4% share in 2025, while polyalkyl methacrylate is growing for premium lubricating oil and aviation applications.

-

By Application, diesel fuel segment dominated the cold flow improver market with approximately 52% share in 2025, while aviation fuel is the fastest growing application driven by aerospace cold weather reliability requirements.

-

By End Use Industry, automotive segment dominated the cold flow improver market with the largest share in 2025, while the automotive segment is also the fastest growing at approximately 6.2% CAGR through commercial fleet expansion in cold climate markets.

By Type, EVA dominates, polyalkyl methacrylate grows for premium applications

Ethylene vinyl acetate retained the dominant type position with approximately 37.4% of the cold flow improver market in 2025. Its commercial primacy reflects the EVA copolymer’s optimal balance of wax crystal modification effectiveness, broad compatibility across diesel fuel grades, cost-efficient production from widely available ethylene and vinyl acetate monomer feedstocks, and the extensive field performance validation database accumulated across decades of commercial diesel fuel treatment in cold climate markets globally. EVA cold flow improver’s mechanism of wax crystal nucleation modification, where the polymer’s polar vinyl acetate groups associate with wax crystal surfaces during nucleation to limit crystal growth into the large plate structures that block fuel filters, creates effective filterability improvement across the cloud point to cold filter plugging point temperature range that defines diesel fuel cold weather operability.

Polyalkyl methacrylate is growing for premium applications because PAMA’s superior performance in both pour point depressant and wax crystal morphology modification roles creates dual-function additive capability whose single-chemistry treatment improves multiple cold flow properties simultaneously in lubricating oil and aviation fuel applications whose more demanding performance specifications exceed EVA’s capabilities in the lower temperature ranges and narrower cold flow property windows that premium applications require. Each new aviation fuel specification round that tightens JFTOT thermal stability and cold flow performance requirements creates PAMA demand for aviation fuel treatment above standard EVA capability.

By Application, diesel dominates, aviation fuel grows fastest

Diesel fuel retained the dominant application position with approximately 52% of the cold flow improver market in 2025. The commercial transportation sector’s diesel consumption volume across long-haul trucking, regional distribution logistics, construction and mining equipment, agricultural machinery, and stationary diesel generation creates the world’s largest petroleum distillate demand whose cold climate operability creates systematic cold flow improver treatment requirement across every winter diesel blend pool in cold climate markets. Each percentage point of global diesel consumption represents cold flow improver procurement from the world’s largest fuel additive application, creating a commercial base whose aggregate scale substantially exceeds all alternative cold flow improver applications combined.

Aviation fuel is growing fastest because the aerospace sector’s cold flow performance requirements are among the most stringent of any petroleum distillate application, where aircraft fuel system operability at altitudes where fuel temperatures drop to minus 40 to minus 60 degrees Celsius creates extreme cold flow performance demands that aviation fuel cold flow improvers must satisfy without compromising thermal stability, combustion quality, or safety specifications. Each new aircraft engine design whose fuel system thermal management creates different fuel temperature profiles and filter sizing creates new cold flow improver performance validation requirements.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

22.8% |

|

Latin America |

Brazil |

43.8% |

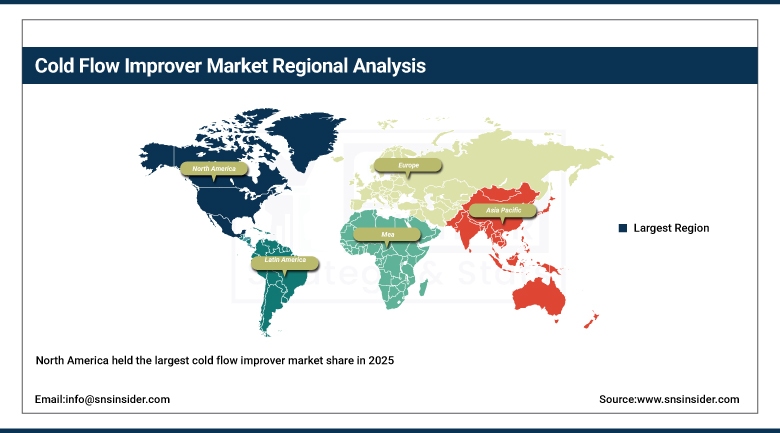

North America Cold Flow Improver Market Insights

North America held the largest cold flow improver market share in 2025, accounting for approximately 35% of global revenue, driven by its extreme winter temperatures across the northern United States and Canada creating diesel cold flow treatment requirements, the world’s largest commercial trucking fleet’s winter diesel procurement, and the renewable fuel standard’s biodiesel blending mandate creating high-cloud-point blends requiring systematic additive treatment. The United States accounts for approximately 82.5% of North American revenues through its large petroleum refining sector’s additive specification.

Canada contributes supplementary North American revenues through its extreme northern climate’s diesel fuel cold flow treatment requirements, the oil sands sector’s large diesel consumption in surface mining operations, and the agricultural sector’s winter diesel treatment for farm equipment operation at temperatures where unaddressed diesel would gel without cold flow improver treatment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cold Flow Improver Market Insights

Europe is a significant cold flow improver market where cold continental winters in Germany, Poland, Scandinavia, and Eastern Europe create seasonal diesel cold flow treatment requirements, the automotive aftermarket’s consumer diesel additive products, and the transition toward higher biodiesel blend rates under the RED III renewable fuel directive creating above-baseline cold flow improver demand. Germany accounts for approximately 24.6% of European revenues through its large automotive, trucking, and industrial diesel consumption.

Scandinavian countries’ extreme cold climate diesel requirements, Poland and Czech Republic’s large commercial trucking sector’s winter fuel treatment, and the European aviation sector’s Jet A-1 cold flow improver specification collectively sustain European market development. European bio-based cold flow improver research and development investment reflects the EU’s chemical innovation funding priorities for sustainable fuel additive technologies.

Asia Pacific Cold Flow Improver Market Insights

Asia Pacific is the fastest-growing regional cold flow improver market, driven by China’s large northern provincial diesel consumption in regions experiencing harsh winters, the expanding Indian commercial vehicle fleet’s diesel treatment requirements in Himalayan and northern plain regions, and the growing aviation industry’s aviation fuel cold flow specification adoption. China accounts for approximately 44.8% of Asia Pacific revenues through its large commercial diesel vehicle fleet and the petroleum refinery sector’s fuel additive specification.

India’s growing commercial vehicle fleet and expanding diesel consumption in cold northern states, South Korea’s sophisticated petrochemical industry’s cold flow additive manufacturing, and Japan’s cold climate diesel treatment requirements in Hokkaido and northern Honshu collectively sustain Asia Pacific’s fastest-growing regional trajectory. The progressive adoption of biodiesel blending mandates across Asian markets is creating additional cold flow improver procurement needs.

MEA & Latin America Cold Flow Improver Market Insights

Saudi Arabia leads MEA revenues through its large petroleum refinery sector’s fuel additive specification, the aviation sector’s substantial Jet A-1 fuel cold flow treatment requirement at its world-class international airports, and the industrial and mining diesel consumption in higher-altitude regions with cooler temperatures. Refinery-gate additive treatment creates structured procurement above consumer market demand.

Brazil leads Latin American revenues through its large commercial vehicle fleet’s winter fuel treatment in southern states, the growing biodiesel blending mandate’s B15 blend’s elevated cloud point creating systematic cold flow improver requirement in cooler months, and the petroleum refining sector’s additive specification at Petrobras refineries. Mexico and Argentina contribute growing secondary demand through their commercial vehicle fleets and petroleum sector.

Market Dynamics

Growth Drivers: Biodiesel blending mandate expansion creating higher cloud point fuel blends requiring systematic cold flow improver treatment

The cold flow improver market’s most commercially significant growth driver is the global expansion of biodiesel and renewable fuel blending mandates, where fatty acid methyl ester biodiesel’s saturated long-chain fatty acid composition creates cloud points substantially higher than petroleum diesel equivalents, requiring proportionally greater cold flow improver treatment at equivalent winter operability performance. Each percentage point increase in mandatory biodiesel blending, from EU’s B7 baseline toward RED III’s 2030 targets, creates proportional cold flow improver demand whose commercial scale grows with each blend rate increase. HVO hydrogenated vegetable oil renewable diesel’s branched paraffinic composition creates different but equally challenging cold flow properties requiring purpose-engineered polymer additive treatment.

The commercial transportation sector’s continuous growth in cold climate markets, where logistics fleet expansion in northern North America, Northern Europe, and northern China creates above-baseline diesel demand in regions whose winter temperatures require systematic cold flow treatment, sustains the automotive and transportation end-use segment’s commercial leadership. Each additional truck route expansion into colder regions and each new commercial fleet procurement of vehicles requiring winter diesel operability creates incremental cold flow improver treatment demand whose aggregate across global fleet growth rates creates the market’s reliable baseline growth trajectory.

Restraints: Electric vehicle adoption reducing diesel consumption and warm climate market growth creating below-average cold flow improver demand

The progressive global electrification of light commercial and passenger vehicles, where EV penetration rate growth reduces petrol and diesel fuel demand from the passenger vehicle sector, creates a structural headwind for cold flow improver market growth whose diesel consumption base is progressively eroding in regions where passenger vehicle electrification is most advanced. Each percentage point of European or North American passenger vehicle fleet electrification that reduces diesel consumption creates proportional cold flow improver volume demand reduction that partially offsets the commercial vehicle and industrial sector’s growing diesel cold flow improver requirement.

Cold flow improver market demand in warm climate markets including tropical Asia, sub-Saharan Africa, and equatorial Latin America, where ambient temperatures remain above diesel cloud point year-round, creates geographic growth limitations that constrain addressable market expansion to cold climate markets. The market’s concentration in cold winter regions creates seasonal procurement patterns whose revenue seasonality makes annual volume forecasting and production planning more complex than year-round specialty chemical markets.

Opportunities: Marine VLSFO cold flow treatment and bio-based additive development creating premium cold flow improver market expansion

Marine fuel’s IMO 2020 very low sulphur fuel oil mandate’s creation of VLSFO blends from paraffinic components whose higher cloud points than conventional high-sulphur fuel oil create cold flow challenges in polar and northern shipping routes represents a growing cold flow improver application category. Each VLSFO blend whose pour point or cloud point creates operability risk in Arctic shipping lanes, North Sea winter operations, or high-latitude port berthing creates marine cold flow improver procurement whose commercial scale grows with VLSFO consumption volume.

Bio-based cold flow improver development using plant-derived polymer backbones including vegetable oil-derived polyalkyl methacrylates and fermentation-derived polyols represents a sustainable product innovation category whose successful performance validation at competitive economics creates commercial opportunity in markets where bio-based content certification creates procurement specification advantage. Each bio-based cold flow improver that achieves equivalent petroleum diesel performance at cost-competitive economics creates a certified sustainable chemistry product whose environmental credentials support petroleum refiner sustainability reporting.

Recent Developments:

-

2024: BASF SE expanded its Keroflux cold flow improver range with new polymer grades optimized for high-blend renewable diesel and HVO mixtures, addressing the different wax crystal morphology of branched paraffinic biofuel blends that conventional EVA-based additives address less effectively.

-

2023: Afton Chemical launched GreenClean 3, a multifunctional diesel additive combining cold flow improvement with advanced detergent technology for heavy-duty fleet vehicles with modern emission control systems, expanding beyond single-function cold flow improver chemistry.

-

2023: Clariant AG introduced new winter diesel additive packages incorporating its DigiFlow cold flow improver platform with digital dosing optimization capability, enabling fuel distributors to automatically adjust additive treat rates based on real-time ambient temperature and blend composition data.

Cold Flow Improver Market Key Players are:

-

BASF SE

-

Evonik Industries AG

-

Clariant AG

-

Afton Chemical Corporation

-

The Lubrizol Corporation

-

Infineum International Limited

-

Innospec Inc.

-

Baker Hughes Company

-

Dorf Ketal Chemicals India Pvt. Ltd.

-

Chevron Oronite Company LLC

-

Croda International PLC

-

LANXESS AG

-

Akzo Nobel N.V.

-

SI Group Inc.

-

Ecolab Inc.

-

Momentive Performance Materials Inc.

-

Haltermann Carless GmbH

-

Eastern Petroleum Pvt. Ltd.

-

Polimeri Europa SpA (Versalis)

-

Rocanda Enterprises Ltd.

Cold Flow Improver Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 909.2 Million |

| Market Size by 2035 | USD 1.60 Billion |

| CAGR | CAGR of 5.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Ethylene Vinyl Acetate, Polyalkyl Methacrylate, Polyalpha Olefin, Polyacrylate, Others) • By Application (Diesel Fuel, Lubricating Oil, Aviation Fuel, Marine Fuel, Others) • By End Use Industry (Automotive, Aerospace & Defense, Marine, Industrial, Agriculture, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Evonik Industries AG, Clariant AG, Afton Chemical Corporation, The Lubrizol Corporation, Infineum International Limited, Innospec Inc., Baker Hughes Company, Dorf Ketal Chemicals India Pvt. Ltd., Chevron Oronite Company LLC, Croda International PLC, LANXESS AG, Akzo Nobel N.V., SI Group Inc., Ecolab Inc., Momentive Performance Materials Inc., Haltermann Carless GmbH, Eastern Petroleum Pvt. Ltd., Polimeri Europa SpA (Versalis), and Rocanda Enterprises Ltd. |

Frequently Asked Questions

The Cold Flow Improver Market was valued at USD 909.2 Million in 2025.

Biodiesel blending mandate expansion creating higher cloud point fuel blends requiring systematic additive treatment, and commercial transportation fleet growth in cold climate markets, marine VLSFO cold flow challenges are the primary growth factors.

The Diesel Fuel segment dominated the Cold Flow Improver Market with approximately 52% share in 2025.

North America dominated the Cold Flow Improver Market in 2025.

Get in Touch