Compact Loader Market Report Scope & Overview:

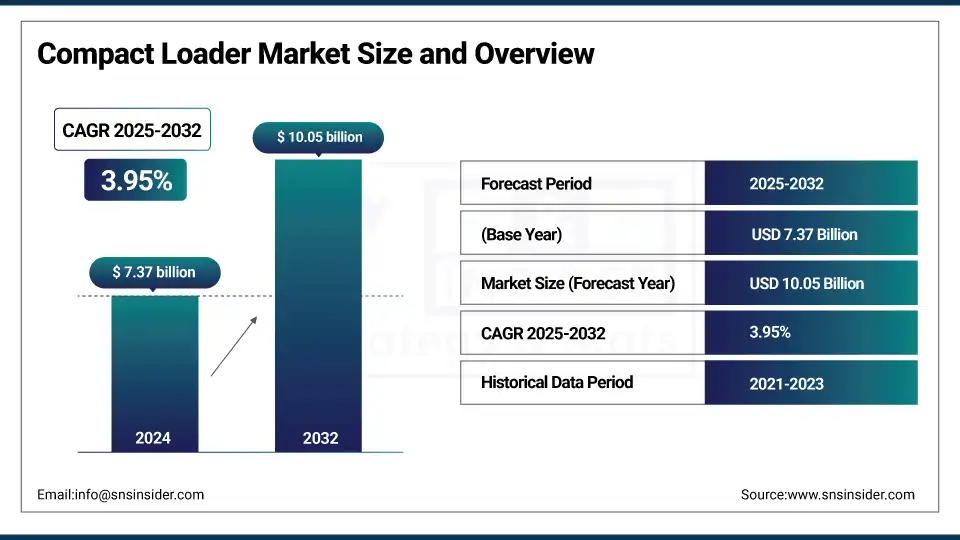

The Compact Loader Market size was valued at USD 7.37 billion in 2024 and is expected to reach USD 10.05 billion by 2032, growing at a CAGR of 3.95% over the forecast period of 2025-2032.

The global compact loader market is experiencing substantial growth due to increasing demand for compact construction machinery across various sectors. The market comprises two main segments, one in the compact wheel loaders industry and the compact track loader industry. Looking for compact wheel loaders that are easier to navigate, fuel efficient, and are simple to operate, these machines are often the choice for material handling, snow removal, and urban construction projects by the best progression of compact wheel loaders. On the other hand, compact track loaders trends are in greater traction, stability, and performance on soft or uneven ground. Some of the trends observed in the key compact loader market include the increasing adoption of electric and hybrid models, telematics, smart technologies, such as GPS, remote monitoring, and automation, coupled with increasing demand for productivity and safety.

To Get more information On Compact Loader Market - Request Free Sample Report

Furthermore, the increase in infrastructure development, urbanization, and the need for mechanization in agriculture and landscaping activities is expected to bolster the compact loader market growth. Additionally, the increasing trend of rental equipment among cost-sensitive contractors is supporting the growth of compact loaders. According to industry reports published in 2024, compact track loaders continue to be the fastest-growing segment, yet compact wheel loaders still make up the largest product segment. The expanding range of attachments, including augers, trenchers, and pallet forks, is also widening their operational capabilities, making them an indispensable component of modern equipment fleets.

In May 2025, Volvo Construction Equipment launched its new generation of wheel loaders, focusing on enhanced fuel efficiency, advanced telematics, and automated load assistance. These models offer improved hydraulic performance, reduced emissions, and lower maintenance needs. They are designed for construction, mining, and material handling applications, emphasizing sustainability and productivity.

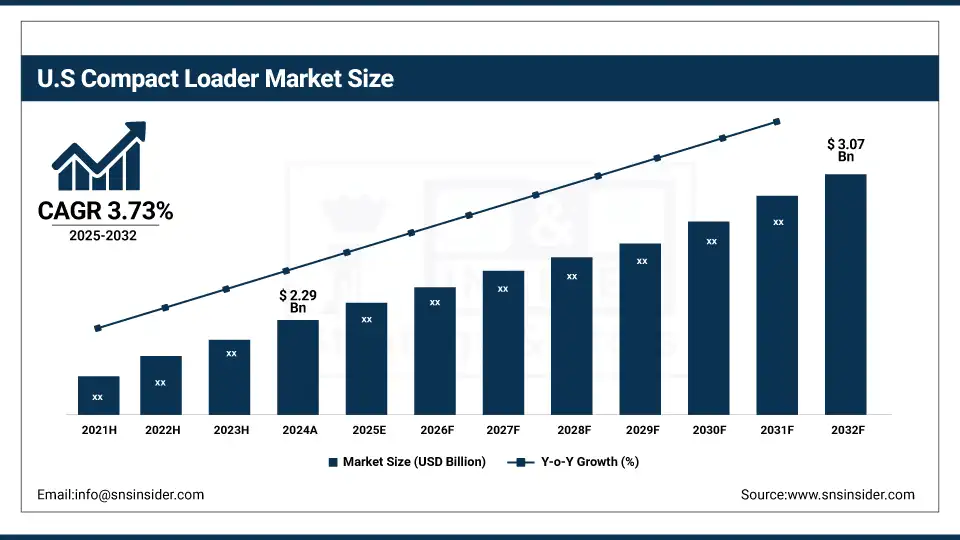

The U.S. leads the North America Compact Loader market, valued at USD 2.29 billion in 2024, projected to reach USD 3.07 billion by 2032, with a CAGR of 3.73%. Growth is driven by rising demand in the construction, agriculture, and landscaping sectors. Infrastructure investments and the adoption of advanced, fuel-efficient compact loaders further boost the market.

Compact Loader Market Dynamics:

Drivers

-

Technological Innovations and Telematics Drive Efficiency and Reliability in the Compact Loader Market

The compact loader market has been propelled by various technological and digital advancements, along with the rise in Internet of Things (IoT), telematics, GPS, and smart diagnostics systems. These solutions offer features like real-time monitoring, remote diagnostics, and predictive maintenance, resulting in reduced downtime and operational expenses. For example, telematics can track equipment performance, fuel efficiency, and location which can ultimately lead to better fleet management and productivity. Research shows that 60% of construction equipment owners currently use telematics for equipment monitoring. Some machines are also aided by more precise hydraulic systems and by automated controls that are helping the machines work with greater precision and improved fuel efficiency. To facilitate optimum working conditions, technology innovations like AI-powered maintenance alerts, along with automated safety systems integrated by several top manufacturers are likely to reduce wear & tear, save costs on equipment maintenance, maximize equipment lifespan, and reduce downtime–this makes these tech innovations imperative in compact loader operations.

Restraint

-

High Acquisition Costs Limit Compact Loader Adoption Among SMEs and Cost-Sensitive Regions

Compact loaders have prohibitively high initial acquisition costs, which is a key restraint, especially for small and medium-sized enterprises (SMEs), independent contractors, and small-scale farmers. These loaders are a high-capital product with prices normally ranging from USD 30,000 to USD 100,000 or more depending upon specification, attachments, and technology integrations. This expenditure is frequently unaffordable in emerging economies and dominion areas which have limited budgets. Aside from this, for many buyers in areas such as Southeast Asia, Latin America or even parts of Africa, affordability is also an issue, leading buyers to opt for renting versus outright purchasing. On top of which, the apparent ownership potential is also hampered by scarce or expensive financing options in some markets.

Compact Loader Market Segmentation Analysis:

By Product Type

The Wheel loaders segment dominated the market and accounted for 68% of the compact loader market share. It is sure to dominate because it is extremely versatile, easy to use, and found everywhere across industries from construction, landscaping, and agriculture. Wheel loaders also offer high travel speeds, better fuel efficiency and reduced maintenance in contrast to track loaders, which are better suited to heavy hauling and lifting where high traction and power are required, making it ideal for urban and other general-purpose work. They're tough enough for hard, paved surfaces and can also cope with many attachments, making them even more viable. Additionally, manufacturers continue to accumulate high end specifications with the wheel loader models, which supports their market leadership.

Track loaders represent the fastest-growing segment in the compact loader market, gaining popularity due to their superior traction and stability in challenging terrains. Wheeled TRUs are growing in popularity in agricultural, forestry, and construction applications as being ideal for use in soft, muddy, or uneven ground conditions which would result in a wheel loader becoming stuck. They also offer more lift capacity and also distribute weight, minimizing surface damage in softer grounds. As a result, the greater construction of infrastructure in more remote and difficult locations is stimulating a resurgence in track loader demand. Moreover, technological development such as enhanced undercarriage systems and improved comfort of the operator are providing them with a push for growth in the market.

By Source Type

Electric compact loaders are the dominant source type, accounting for 52% market share in 2024. Strict emissions regulations, soaring fuel prices, and increasing demand for cleaner equipment are making them the largest, Models powered by electricity have a host of advantages such as being quieter during operation, reduced maintenance costs and relatively reduced carbon emissions which makes them ideal for indoor use, urban sites or places with low noise level restrictions. Fueled further by government incentives and charging hardware. Moreover, adoption of advanced battery technology, which is improving performance as well as lowering lifecycle running cost of electric compact loaders, and becoming major growth driver of this market.

Hybrid compact loaders are emerging as the fastest-growing source segment in the market. The rapid development is largely because they embody the best of both diesel and electric systems, giving a mix of better fuel economy and lower emissions while maintaining performance. And with hybrid loaders offering a powerful, sustainable solution, it's easier than ever to make the switch. Compared to pure-electric versions, they offer longer working hours, and are also more fuel efficient than diesel units. Due to rising productivity demands in the construction and agricultural industries yet with a goal of greener options, technological innovation and regulation are inspiring adoption of hybrid compact loaders worldwide to provide a green hybrid option for customers where productivity has been maximised.

By Application

The construction sector dominated the compact loader market, holding a 32% share in 2024. Compact Loaders are popular for excavation, material handling, grading, and site preparation work in construction. Compact form factor and maneuverability, along with versatility to mount multiple tools, makes mini-excavators a workhorse at construction sites, notably in cities and tight areas. With demand for residential, commercial and infrastructure construction projects continuing to rise around the globe, compact loaders will be part of the construction landscape. In addition, by means of automation technologies, telematics, and fuel-efficient tech, manufacturers are adapting the form of loaders to be more appealing to construction.

Agriculture is recognized as the fastest-growing application segment in the compact loader market. Farmers and agricultural businesses are using compact loaders for livestock, feeding, land clearing and farm maintenance jobs. These loaders augment the productivity for farms and the requirement of agricultural machinery that add in efficiency & multipurpose functionality has uplifted the demand of this type of loader. Due to their space-efficient nature and functionality via interchangeable tools, they are one of the most versatile farm machines for modern agriculture systems. Furthermore, rising labor shortages as well as trend towards mechanized farming are stimulating the creation of compact loaders in agriculture, particularly in agro-business emerging countries.

Compact Loader Market Regional Outlook:

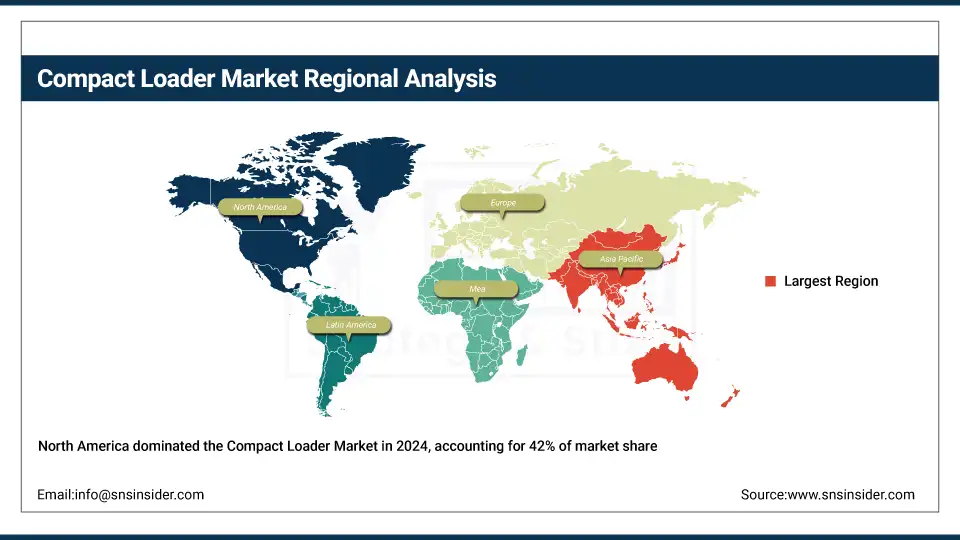

North America dominated the compact loader market in 2024, accounting for around 42% of the global share. This region is a leader in terms of construction machinery due to strong infrastructure development, high demand, and the presence of significant manufacturers. The primary drivers of contributions are robust investments in residential, commercial and municipal construction projects, led by the U.S. and Canada. In addition to this growing demand for compact loaders on rent is fuelling the market growth. These technologies include electric and hybrid compact loaders, part of the growing trend in the region to achieve sustainability goals and stringent emissions regulations, cementing North America as the industry front-leader.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe holds a significant share in the compact loader market, backed by rising demand across the construction, agriculture, and landscaping industries. Germany, France, and Italy lead the way in the development of automation-oriented and environmentally friendly machinery. The region's growth is also attributed to strong government support for green construction technologies, along with electrifying machinery. Meanwhile, European manufacturers are targeting small, low-emission loaders, designed for city building construction and renovation operations. Strict labor laws with high cost of hiring workers lead to demand for equipment in the country and thus drive market. All in all, Europe is always dominant with stable demand, since Europe is the first, that is always at the forefront in terms of efficiency, sustainability and safety at construction sites.

Asia-Pacific is emerging as the fastest-growing region in the compact loader market, fueled by rapid urbanization, industrialization, and government-led infrastructure projects. In China, India, and Southeast Asian countries, the need for compact, versatile equipment to serve space-constrained construction environments is rising. Growing residential and commercial property needs, road building, and mining are all boosting equipment sales. In addition, government policies to promote construction and mechanization in agriculture are also serving as growth drivers. Like other companies, they are also looking to expand their dealer network and offer cost-effective models according to the local needs. This immense synergy of economic development and urbanization cause Asia-Pacific to emerge as the fastest-growing market.

China dominates the Asia-Pacific Compact Loader market due to rapid urbanization and large-scale infrastructure projects. Continued strong growth is attributed to strong demand from the construction, agriculture, and landscaping sectors. Market growth is supplemented by government efforts related to smart cities and rural development.

Key Players in the Compact Loader Market are:

Compact loader companies are Komatsu Ltd., ASV, Gamzen, Volvo Construction Equipment, Kato Works Co. Ltd., Takeuchi Mfg. Co., Ltd., CNH Industrial N.V., Sany Heavy Industry Co., Ltd., Doosan Bobcat, Caterpillar Inc.

Recent Development:

-

In Feb 2025, Komatsu, a global leader in construction and mining equipment, unveiled a new 4-tonne skid steer loader and a 5-tonne compact track loader at Bauma 2025, the international trade fair for construction and infrastructure.

-

In April 2025, Volvo CE launched the first wave of its next-generation wheel loaders, beginning with five models spanning from the L150 to the L260. Engineered for maximum productivity, operator comfort, and safety, these new loaders feature advanced technologies and innovative service solutions.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 7.37 Billion |

| Market Size by 2032 | USD 10.05 Billion |

| CAGR | CAGR of 3.95% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Wheel Loader, Track Loader) • By Source Type (Diesel, Electric, Hybrid) • By Application (Construction, Landscaping, Agriculture, Forestry, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Komatsu Ltd., ASV, Gamzen, Volvo Construction Equipment, Kato Works Co. Ltd., Takeuchi Mfg. Co. Ltd., CNH Industrial N.V., Sany Heavy Industry Co. Ltd., Doosan Bobcat, Caterpillar Inc. |

Frequently Asked Questions

Ans: The North America region dominated the Compact Loader market in 2024.

Ans: The “Wheel loaders” segment dominated the Compact Loader market.

Ans: Technological Innovations and Telematics Drive Efficiency and Reliability in the Compact Loader Market

Ans: The Compact Loader market was USD 7.37 billion in 2024 and is expected to reach USD 10.05 billion by 2032.

Ans: The Compact Loader market is expected to grow at a CAGR of 3.95% from 2025-2032.

Get in Touch