Compound Semiconductor Market Report Scope & Overview:

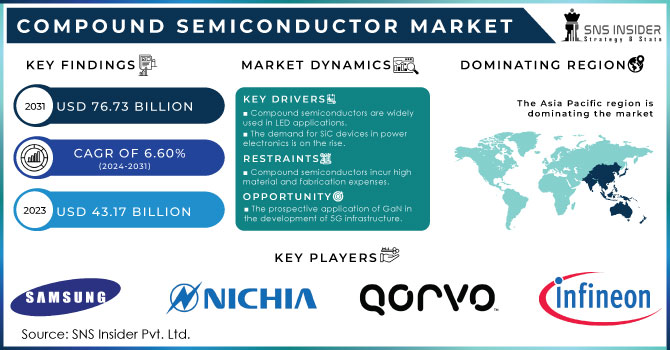

The Compound Semiconductor Market Size was valued at USD 43.17 billion in 2023 and is expected to reach USD 76.73 billion by 2032 and grow at a CAGR of 6.60% over the forecast period 2024-2032.

The compound semiconductor market has improved substantially in the last years based on the rising need for high-performance devices within telecommunications, automotive, and consumer electronics. Compound semiconductors such as gallium arsenide, gallium nitride, indium phosphide, and others have been developed to replace silicon semiconductors. They have shown better performance than silicon semiconductors offering higher electron mobility, temperature resistance, and efficiency of devices within the high-frequency sector. This includes 5G networks, satellite communications, ADAS, and many other aspects. The arrival of the 5G and the future 6G networks is driving the market to new heights. The 5G devices should exceed the mark of 14.4 billion, due to the rise of the use of smartphones. There is a growing need for Gallium Nitride-based RF devices because they provide better performance at higher frequencies. Moreover, gallium nitride-based solutions are in demand due to the development of the consumer electronics market, which nowadays is focused on quicker recharging and a smaller form factor.

Get more information on Compound Semiconductor Market - Request Sample Report

Innovations in LED and laser technologies for displays and lighting are also creating new opportunities within the market. Compound semiconductors are materials that like pure elements can control the flow of electricity very precisely. However, compound semiconductors involve two or more elements combined. Thus, in a light-emitting diode, when the electric current flows through the compound semiconductor, it makes the energy want to leave as light. According to Warehouse-Lighting, by 2030, with a forecast of up to 87%-unit share of lighting sources, these devices are going to replace all other options rapidly. The driving force behind this transition is to comprise both economic and environmental benefits. For instance, it requires up to 75% less energy than glowing bulbs and can save consumers a significant amount of money in the long run, even those who cannot afford their higher cost compared to standard models. The commercial sector, which has only 13% of lighting options offered by the chosen technology, is the best example. More specifically, conventional fluorescent lights used in linear fittings are expected to be replaced.

MARKET DYNAMICS:

Drivers

- Compound semiconductors are widely used in LED applications.

LED is a thin form of a light-emitting diode and this technology is the most excellent replacement for IoT in which tiny light sources can convert electricity into visible light. A semiconductor is a compound material having an electrical conductivity ranging between the conductors of metals and insulators like plastics This conductivity can be modified through doping by adding impurities. Compound semiconductors are made by combining two elements or more. The major forms of lifetime compound semiconductors are indium and gallium. The compound semiconductors have formations that enable them to emit useful light. Their suggestions are used directly to emit lights as they result at the LED junction. They can emit light and also can convert to form light energy. Cree is a company that uses silicon carbide and produces LED chips. Silicon carbide compound semiconductor allows this companies LEDs to be operated at high temperatures due to its extreme intensity. It is suitable for various vehicles like the headlamps and home lightening since heat is always expected in cold rooms.

- The demand for SiC devices in power electronics is on the rise.

SiC devices are characterized by having ten times more breakdown electric field strength and three times the thermal conductivity than silicon-based components. This one-of-a-kind characteristic simplifies the cost and complexity of the devices, improves reliability, and makes SiC devices ideal for various high-voltage applications, such as solar inverters, power supplies, wind turbines, and other applications. The demand for power electronics also shifts the demand for SiC power devices due to their beneficial properties and applications. Power electronics are a crucial tool in controlling and converting electric power effectively. Moreover, a growing demand for power electronics in various sectors, such as aerospace, medical, and defense, is another important factor influencing the demand for SiC power devices.

- The prospective application of GaN in the development of 5G infrastructure.

Efficiency, performance, and value are crucial requirements for 5G wireless base stations. GaN solutions play a pivotal role in fulfilling these requirements. Compared to diffused metal-oxide-semiconductor (LDMOS), GaN-on-SiC offers substantial improvements in efficiency and performance for 5G base stations. Additionally, GaN-on-SiC provides benefits such as enhanced thermal conductivity, heightened robustness and reliability, improved efficiency at higher frequencies, and comparable performance in a smaller-sized MIMO array. The integration of GaN technology in power amplifiers for all transmission cells in the network, including micro, macro, pico, and femto/home routers, is anticipated to have a significant impact on the deployment of next-generation 5G networks.

Restraints

- Compound semiconductors incur high material and fabrication expenses.

The primary obstacle to the growth of the compound semiconductor market stems from the substantial expenditure involved throughout the industry's supply chain processes. The total average expenditure per compound semiconductor device, encompassing both upstream and downstream expenditures, significantly exceeds that of pure silicon semiconductor devices. This discrepancy arises due to the complexity and novelty of all processes involved, necessitating advanced technologies and costly state-of-the-art equipment. Furthermore, there is a lack of familiarity and expertise among engineering professionals and executives within the compound semiconductor industry regarding manufacturing processes. Additionally, the commercial synthesis of compound semiconductors in high-temperature environments results in higher costs compared to the easily extractable silicon raw material obtained from naturally occurring silica. Moreover, factors such as fewer foundry and fab facilities and the absence of advanced technology-based equipment in final phases like assembly, testing, and packaging contribute to higher costs.

- The design complexity of compound semiconductors.

Designing compound semiconductor devices involves a high degree of complexity. The primary challenge for designers lies in achieving enhanced efficiency while simultaneously minimizing costs and simplifying the structure. Additionally, the diverse requirements of various applications further compound the design complexities of power and RF devices. The rise in efficiency extends the operating time of battery-powered products, thereby reducing the electricity consumption of wireless base stations and similar applications.

MARKET SEGMENT:

By Decomposition Technology

- Chemical Vapor Deposition (CVD)

- Molecular Beam Epitaxy

- Hydride Vapor Phase Epitaxy (HVPE)

- Ammonothermal

- Liquid Phase Epitaxy

- Atomic Layer Deposition (ALD)

- Others

By Type

- Gallium Nitride (GaN)

- Gallium Arsenide (GAAS)

- Silicon Carbide (SiC)

- Indium phosphide (INP)

- Silicon germanium (SIGE)

- Gallium phosphide (GAP)

- Others

GaN will continue to dominate the compound semiconductor market in 2023 with a market share of more than 39.78%. GaN has a high bandgap, which is suitable for high breakdown voltage and low conduction resistance. These properties of the GaN enable high-speed switching and miniaturization. Whereas, the silicon devices need a broader chip area to lower the on-resistance. In addition, GaN devices are small, which allows better high-resolution and also helps to perform high-speed switching, high electron mobility and density, and enabling miniaturization in a better way.

BY PRODUCT

- LED

- RF Devices

- Optoelectronics

- Power Electronics

The power electronics segment became the leading segment in the compound semiconductors market and holds the highest market share of over 40.99% in 2023. The adoption of smart home appliances and the purchase of advanced consumer electronics are likely to facilitate the demand for power electronics modules. GaN has become an essential component for power electronics and is increasingly being implemented by companies in delivering effective solutions to their clients. Wireless consumer electronics such as smartphones, tablets, and intelligent wearables have been experiencing advanced performance as a result of GaN technologies.

BY APPLICATION

-

General Lighting

-

Military, Defense, and Aerospace

-

Power Supply

-

Commercial

-

Consumer Devices

-

Telecommunication

-

Automotive

-

Datacom

-

Consumer Display

-

Others

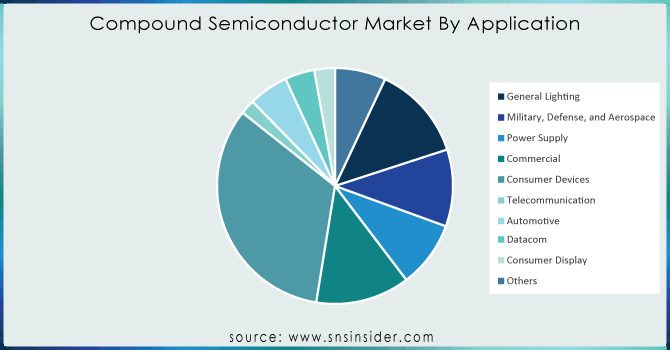

Increased usage of GaAs, GaN, InP, and SiGe compound semiconductors make telecommunication the leading application segment of the compound semiconductor market, with a market share of more than 33.12% in 2023. The telecommunication application market is being fueled by the opportunity created by the 5G technology for compound semiconductors for telecom.

Get Customized Report as per your Business Requirement - Request For Customized Report

REGIONAL ANALYSIS:

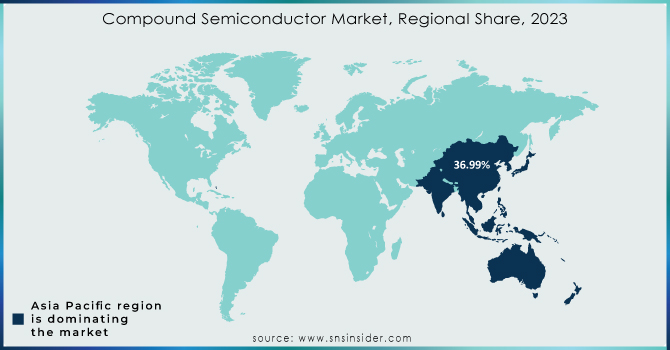

In 2023, Asia Pacific dominated the market with a share of above 36.99%, due to extensive product penetration and rise in the consumer electronics manufacturing sector. The region is poised to continue growing due to rapid urbanization and rising disposable income, which are expected to sustain the upward trend in the consumer electronics sector. In addition, the region displays the highest growth potential for advanced technologies, and shifting consumer preference toward smart, and innovative products is further expected to increase regional growth both currently and in the foreseeable future.

North America is poised to experience the fastest CAGR during the forecast period. The market growth is driven by robust demand in the end-use sectors in the United States, Canada, and Mexico. Further, with the capacity expansion market entry, growth, and acquisition, foreign manufacturers make an entry into the highly dynamic market set to cater to the rising demand.

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of the Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

KEY PLAYERS:

The key players in the compound semiconductor market are Nichia Corporation, Samsung Electronics, NXP Semiconductor, Infineon Technologies, Taiwan Semiconductor, QORVO, CREE, Renesas Electronics Corporation, Stmicroelectronics, Texas Instruments Incorporated, OSRAM AG, Skyworks, Wolfspeed Inc., GaN Systems, Canon Inc., Infineon Technologies AG, Mitsubishi Electric & Other.

RECENT DEVELOPMENT

- In June 2023, India reopened the application window for government incentives for companies interested in developing semiconductor manufacturing, including compound semiconductors.

- In May 2024, Australian firm Silanna UV announced the launch of far-UVC. Proximity Exposure Module, using compound semiconductors in advanced disinfectant technology.

- In February 2024, Innoscience unveiled a family of integrated GaN devices that combine a variety of functions in the same package, providing a simple power electronics design.

- In February 2024, Sivers Semiconductors introduced the new RF-LDM-10 range of 2 490-2 690 MHz low-RF 5G modules to showcase the growing affordable production of compound semiconductor technology for the next generation of wireless telecommunications.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 43.17 Billion |

| Market Size by 2032 | US$ 76.73 Billion |

| CAGR | CAGR of 6.60% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments |

|

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Nichia Corporation, Samsung Electronics, NXP Semiconductor, Infineon Technologies, Taiwan Semiconductor, QORVO, CREE, Renesas Electronics Corporation, Stmicroelectronics and Texas Instruments Incorporated, OSRAM AG, Skyworks, Wolfspeed Inc., GaN Systems, Canon Inc., Infineon Technologies AG, Mitsubishi Electric |

| Key Drivers |

|

| RESTRAINTS |

|

Frequently Asked Questions

Asia Pacific will be the dominating region in the Compound Semiconductor Market in 2023.

The telecommunication segment by application is dominating the Compound Semiconductor Market.

The rise in the application of LED and demand for SiC devices in power electronics raises the growth of the Compound Semiconductor Market.

The Compound Semiconductor Market size was USD 43.17 billion in 2023 and is expected to Reach USD 76.73 billion by 2032.

The Compound Semiconductor Market is expected to grow at a CAGR of 6.60%.

Get in Touch