Connected Enterprise Market Report Scope & Overview:

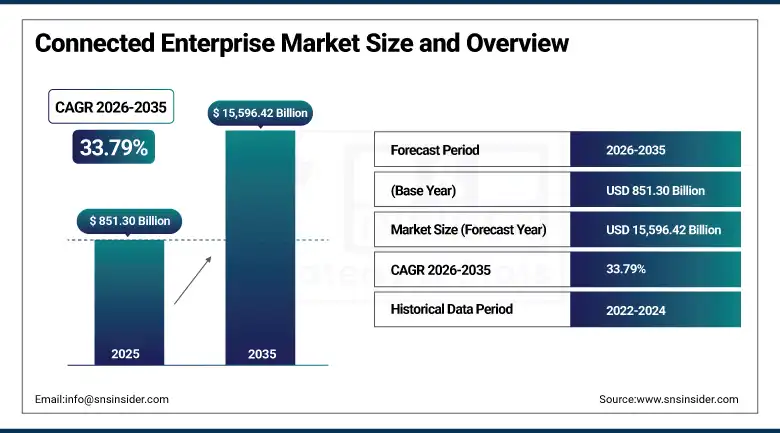

The Connected Enterprise Market was valued at USD 851.30 Billion in 2025 and is expected to reach USD 15,596.42 Billion by 2035, growing at a CAGR of 33.79% from 2026–2035.

The global connected enterprise market is growing at an exceptional and transformative pace. A connected enterprise is a fully integrated digital organisations where all processes, people, machines, and systems are interconnected through IoT platforms, cloud computing, AI analytics, edge computing, and 5G connectivity. The market is driven by the increasing integration of IoT and automation that enhances efficiency and reduces costs, the rise of 5G that accelerates adoption by enabling faster data processing and low-latency industrial automation applications. Adoption of connected enterprise solutions varies by industry with manufacturing, healthcare, and retail leading due to IoT integration and automation requirements.

In 2024, Siemens launched its Xcelerator connected enterprise platform with enhanced AI-powered digital twin capabilities, integrating real-time production data from shop-floor IoT sensors with cloud-based simulation. The platform creates a continuously updated digital replica of the entire manufacturing system whose operational intelligence reduces production downtime, accelerates new product introduction, and enables sustainable manufacturing optimization.

Market Size and Forecast

-

Market Size in 2026E: USD 1,139.25 Billion

-

Market Size by 2035: USD 15,596.42 Billion

-

CAGR: 33.79% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Connected Enterprise Market - Request Free Sample Report

Connected Enterprise Market Trends

-

Generative AI integration with connected enterprise platforms is enabling autonomous decision-making, predictive maintenance, and intelligent enterprise-wide operational optimization.

-

Industrial metaverse adoption combining digital twins, AR/VR, and real-time sensor data is improving remote collaboration, training, and facility management.

-

Edge computing deployment is increasing to support low-latency analytics, real-time control, and secure processing of industrial IoT data.

-

Cybersecurity is becoming a core component of connected enterprise architectures as IT/OT convergence expands organizational attack surfaces.

-

Sustainability-focused connected enterprise solutions are enabling real-time monitoring of energy use, emissions, water consumption, and resource efficiency.

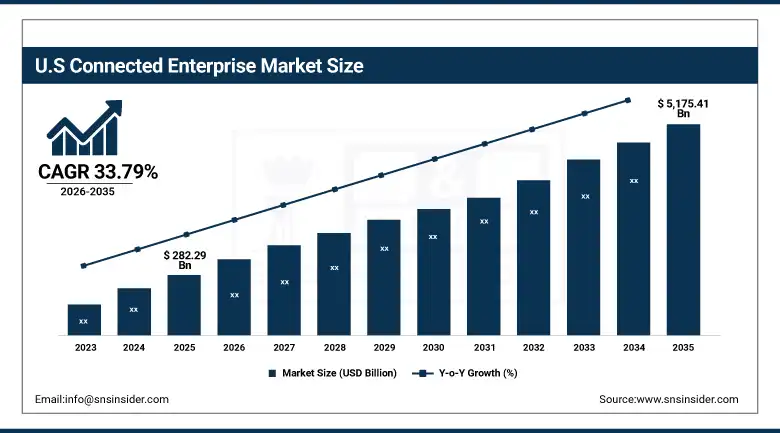

The U.S. Connected Enterprise Market Outlook

The U.S. Connected Enterprise Market was valued at approximately USD 282.29 Billion in 2025 and is expected to reach approximately USD 5,175.41 Billion by 2035, growing at a CAGR of approximately 33.72%.

The U.S. is the world’s most commercially sophisticated connected enterprise market within North America’s dominant revenue position. Microsoft Azure’s industrial IoT, AWS IoT Greengrass, Cisco’s industrial networking, Rockwell Automation’s FactoryTalk, and Siemens’ U.S. operations collectively define the North American connected enterprise commercial and technology landscape. The advanced U.S. manufacturing sector’s Industry 4.0 investment, the healthcare system’s digital patient monitoring adoption, and the retail sector’s supply chain visibility digitalization create the world’s most commercially diverse connected enterprise demand environment.

Rockwell Automation expanded its FactoryTalk Design Studio connected enterprise platform with enhanced cloud-native remote access capabilities, enabling engineers at geographically distributed manufacturing facilities to collaboratively design, deploy, and monitor industrial control system programmes from a unified cloud interface. The expansion reflects the commercial recognition that manufacturing’s progressive globalization and the engineering talent shortage’s geographic constraint create commercial motivation for cloud-connected control system engineering tools.

Connected Enterprise Market Segment Analysis

-

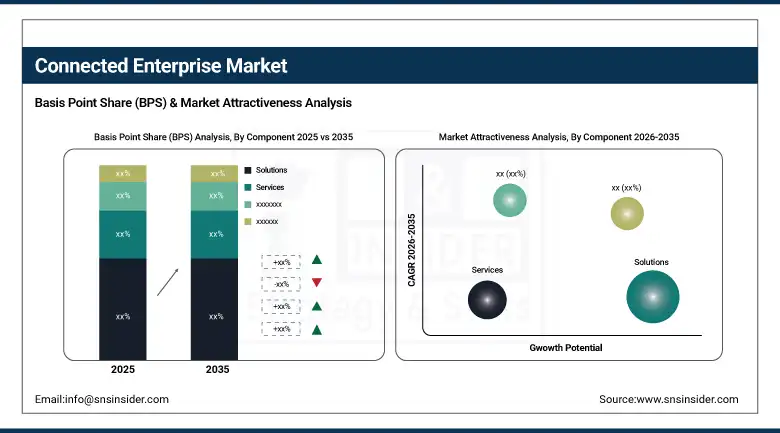

By Component, the solutions segment dominated the market with approximately 46% share in 2025, while the services segment is the fastest growing.

-

By Deployment, the cloud segment dominated the market with approximately 62% share in 2025, while the on-premise segment is the fastest growing.

-

By Enterprise Size, the large enterprise segment dominated the market with approximately 68% share in 2025, while the small & medium enterprises segment is the fastest growing.

-

By End User, the manufacturing segment dominated the market with approximately 28% share in 2025, while the healthcare segment is the fastest growing.

By Component, solutions dominate, services grow fastest

Solutions retained the dominant component position with approximately 46% of the connected enterprise market in 2025. Connected enterprise solutions’ commercial primacy reflects the foundational technology deployment requirement that every connected enterprise programme requires before services can create value. IoT platforms that aggregate device data, AI analytics engines that extract operational insights, digital twin software that creates virtual operational replicas, and enterprise integration middleware that connects operational technology with information technology collectively constitute the solution portfolio whose procurement defines the majority of connected enterprise commercial investment.

Services are the fastest-growing component because connected enterprise implementation’s technical complexity, the OT/IT convergence programme’s organizational change management requirement, and the ongoing managed connectivity service model’s commercial accessibility create growing services procurement that exceeds solution licensing growth rates. Each enterprise that deploys connected enterprise solutions creates implementation consulting demand, and each organization that lacks the internal expertise to operate and optimize its connected enterprise infrastructure creates managed services procurement whose recurring revenue compounds with programme expansion.

By End User, manufacturing dominates, healthcare grows fastest

Manufacturing retained the dominant end-user position with approximately 28% of the connected enterprise market in 2025. The manufacturing sector’s adoption of Industry 4.0 technologies—connecting production equipment, quality systems, supply chain visibility platforms, and worker productivity tools in unified digital environments—creates the most commercially concentrated and highest-value connected enterprise procurement of any industry vertical. Each smart factory initiative creates IoT sensor deployment, edge computing infrastructure, cloud analytics platform subscription, and digital twin programme investment.

Healthcare is the fastest-growing end user because the convergence of connected medical devices, remote patient monitoring, clinical workflow automation, and healthcare operational analytics is creating multiple simultaneous above-average growth vectors within a single industry vertical. Hospital IoT’s real-time patient location, medical equipment utilization monitoring, and environmental condition sensing create facility management connectivity investment that compounds with clinical connected device deployment.

By Deployment, cloud dominates, on-premise grows for regulated sectors

Cloud deployment retained the dominant position with approximately 62% of the connected enterprise market in 2025. Cloud-delivered connected enterprise infrastructure’s scalability advantage creates natural specification preference for organisations whose connected device deployment scale is uncertain during initial programme planning. Cloud platform’s continuous AI model update capability, global multi-site connectivity, and collaboration enablement across geographically distributed operations create commercial advantages that on-premise alternatives cannot match without significantly higher capital infrastructure investment.

On-premise deployment is the fastest-growing for regulated industries where classified government operations, financial trading system data sovereignty, and critical infrastructure OT network security management create mandatory local processing requirements whose compliance motivation sustains capital infrastructure investment independently of cloud alternative cost comparison. Each regulated enterprise that cannot transit operational technology data through public cloud infrastructure creates on-premise connected enterprise architecture investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Connected Enterprise Market Insights

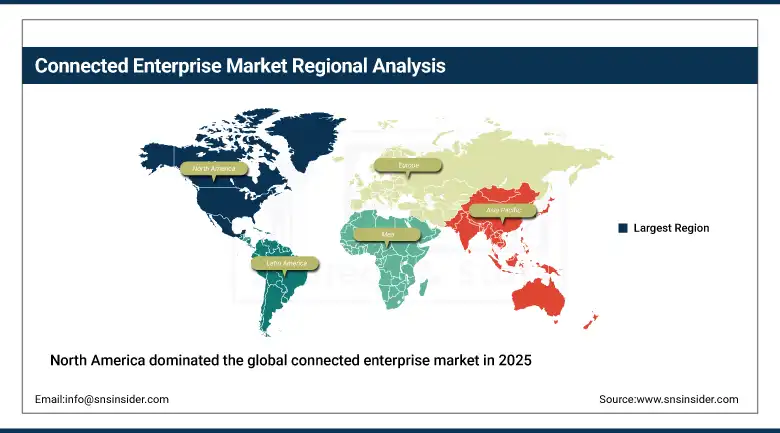

North America dominated the global connected enterprise market in 2025 with the highest investment in IoT integration and automation. The United States accounts for approximately 87.4% of North American revenues through Microsoft, AWS, Cisco, Rockwell Automation, and Siemens’ commercial dominance whose combined portfolio defines the connected enterprise technology standard. The advanced manufacturing sector’s Industry 4.0 investment, the healthcare system’s digital transformation, and the commercial real estate sector’s smart building adoption collectively create the world’s most commercially diverse connected enterprise procurement environment.

Canada contributes approximately 12.6% of North American revenues through its manufacturing sector’s automation investment, the natural resources industry’s remote monitoring adoption, and the healthcare system’s digital patient care connectivity programme.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Connected Enterprise Market Insights

Europe is a technically sophisticated connected enterprise market where EU Industry 5.0 framework, GDPR’s data governance requirements creating on-premise deployment motivation, and Siemens’ and SAP’s European commercial leadership create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its world-class manufacturing sector’s Industrie 4.0 investment, SAP’s enterprise platform integration, and Siemens’ Xcelerator commercial operations.

The United Kingdom, France, and the Netherlands are significant secondary markets where manufacturing digitalization, healthcare system connectivity, and financial services digital infrastructure create consistent connected enterprise procurement that compounds with each country’s digital transformation investment pace.

Asia Pacific Connected Enterprise Market Insights

Asia Pacific is the fastest-growing regional connected enterprise market, driven by China’s Made in China 2025 initiative’s smart manufacturing investment, Japan’s Society 5.0 framework’s connected society vision, India’s manufacturing sector’s digital transformation, and South Korea’s smart factory programme. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary industrial IoT deployment scale, the government’s smart city connectivity investment, and the manufacturing sector’s systematic robotics and automation integration.

India represents the most commercially dynamic emerging market within Asia Pacific where the government’s Production Linked Incentive scheme is creating manufacturing sector digital investment that creates above-average first-time connected enterprise procurement, and the rapidly growing digital economy creates connected enterprise demand across retail, healthcare, and financial services.

MEA & Latin America Connected Enterprise Market Insights

UAE leads MEA revenues at approximately 38.4% through its UAE Vision 2031’s smart economy investment, the manufacturing sector’s Industry 4.0 adoption, and the smart city Dubai initiative’s connected infrastructure creating structured connected enterprise procurement. Brazil leads Latin American revenues at approximately 44.2% through its manufacturing sector’s automation investment, the financial services industry’s digital transformation, and the healthcare system’s connected patient monitoring adoption.

Saudi Arabia’s Vision 2030 and NEOM’s smart city development create significant MEA secondary market procurement whose connected enterprise infrastructure investment reflects the extraordinary scale of Saudi Arabia’s digital economy programme ambition.

Market Dynamics

Growth Drivers: Industry 4.0 adoption creating manufacturing connectivity demand and 5G enabling ultra-low-latency industrial applications

Industry 4.0’s systematic adoption across global manufacturing is the connected enterprise market’s most commercially certain structural growth driver. Each manufacturing facility that progresses from traditional operation toward smart factory connectivity creates IoT platform, edge computing, digital twin, and AI analytics procurement whose combined per-facility investment creates commercial relationships that sustain multi-year programme expansion. The World Economic Forum’s Lighthouse manufacturing network, which certifies facilities that demonstrate Industry 4.0 leadership, creates peer benchmarking whose competitive manufacturing efficiency pressure sustains global Industry 4.0 investment that creates connected enterprise demand.

5G’s progressive commercial network deployment is creating the connectivity infrastructure whose ultra-low latency, high bandwidth, and massive device density capabilities enable connected enterprise applications that 4G and Wi-Fi alternatives cannot support. Each 5G private network deployment in a manufacturing facility creates industrial IoT connectivity whose real-time closed-loop control, AR-guided assembly, and AGV fleet coordination create operational efficiency improvements whose commercial measurement sustains connected enterprise investment.

Restraints: OT/IT cybersecurity convergence complexity and data sovereignty regulation constraining cloud deployment

OT/IT network convergence’s creation of bi-directional connectivity between previously isolated operational technology and enterprise information technology creates cybersecurity attack surface expansion whose management requires specialized industrial cybersecurity expertise whose scarcity creates implementation barriers. Each industrial network that connects previously air-gapped control systems to enterprise IT infrastructure creates security vulnerability whose exploitation potential creates risk management investment requirement proportional to the connected enterprise programme’s operational criticality.

Data sovereignty regulation in multiple jurisdictions creates cloud deployment constraints that require geographic data residency compliance whose engineering complexity increases connected enterprise architecture cost and limits the global cloud platform procurement consolidation that IT cost optimization programmes target.

Opportunities: Industrial metaverse applications and SME cloud-delivered connected enterprise democratization

Industrial metaverse applications combining digital twin, augmented reality, and connected sensor data represent the most commercially innovative connected enterprise capability direction whose immersive operational visualization creates new workforce productivity, remote expert collaboration, and facility management applications. Each industrial metaverse application that demonstrates measurable operational improvement creates adoption motivation that sustains premium technology investment. Siemens’ Xcelerator and Microsoft’s Azure Digital Twins collectively demonstrate the commercial ecosystem whose maturation creates industrial metaverse adoption at enterprise scale.

SME connected enterprise democratization through cloud SaaS delivery represents the most commercially scalable volume growth opportunity whose addressable market substantially exceeds the large enterprise segment by participant count.

Recent Developments:

-

2024: Siemens advanced its Xcelerator platform through expanded digital twin and industrial metaverse capabilities for connected manufacturing environments.

-

2024: Cisco expanded industrial networking and cybersecurity offerings designed to secure large-scale IT/OT converged enterprise infrastructures.

-

2024: Honeywell enhanced industrial digitalization platforms with AI-enabled predictive maintenance and asset performance optimization capabilities.

Connected Enterprise Market key players are:

-

Microsoft Corporation (Azure IoT)

-

Amazon Web Services (AWS IoT)

-

Siemens AG (Xcelerator)

-

Rockwell Automation Inc.

-

Cisco Systems Inc.

-

SAP SE

-

IBM Corporation

-

Honeywell International Inc.

-

General Electric (GE Digital)

-

PTC Inc.

-

Schneider Electric SE

-

ABB Ltd.

-

Emerson Electric Co.

-

Bosch Connected Industry

-

Hitachi Vantara

-

Oracle Corporation

-

Zebra Technologies Corporation

-

Ericsson AB

-

Nokia Corporation

-

Huawei Technologies Co., Ltd.

Connected Enterprise Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 851.30 Billion |

| Market Size by 2035 | USD 15,596.42 Billion |

| CAGR | CAGR of 33.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (Cloud, On-Premise, Hybrid) • By Enterprise Size (Large Enterprise, Small & Medium Enterprises) • By End User (Manufacturing, Healthcare, Retail & E-Commerce, Transportation & Logistics, Energy & Utilities, BFSI, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation (Azure IoT), Amazon Web Services (AWS IoT), Siemens AG (Xcelerator), Rockwell Automation Inc., Cisco Systems Inc., SAP SE, IBM Corporation, Honeywell International Inc., General Electric (GE Digital), PTC Inc., Schneider Electric SE, ABB Ltd., Emerson Electric Co., Bosch Connected Industry, Hitachi Vantara, Oracle Corporation, Zebra Technologies Corporation, Ericsson AB, Nokia Corporation, Huawei Technologies Co., Ltd. |

Frequently Asked Questions

The Connected Enterprise Market is expected to grow at a CAGR of 33.79% from 2026 to 2035.

The Connected Enterprise Market was valued at USD 851.30 Billion in 2025.

Increasing integration of IoT and automation enhancing operational efficiency and reducing costs across manufacturing, healthcare, and retail industries.

Solutions dominated the market with approximately 46% share in 2025, while the Services segment is the fastest growing.

North America dominated the market in 2025.

Get in Touch