Construction Materials Market Report Scope and Overview:

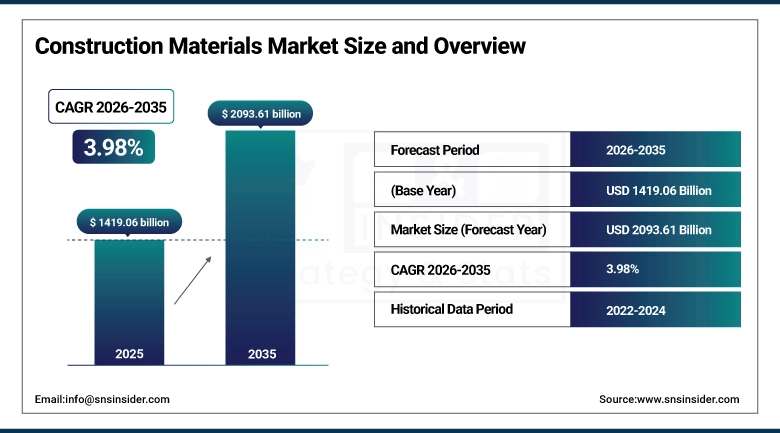

The Construction Materials Market was valued at USD 1,419.06 billion in 2025 and is expected to reach USD 2,093.61 billion by 2035, growing at a CAGR of 3.98% from 2026-2035.

Construction Materials Market is growing steadily due to increased investments in infrastructure construction and residential and commercial buildings construction in developed countries as well as developing economies. Construction materials can be defined as various raw materials needed for the construction process and include aggregates such as sand, gravel, crushed stones; binders such as cement, lime; masonry products such as bricks, blocks; structural metals like steel and aluminum; and special construction materials used for insulation, finishing, and waterproofing. The demand for the mentioned construction materials depends on the level of construction activities, which are affected by demographic factors like population growth, urbanization rates, and governmental spending in infrastructure projects and private investors' involvement in real estate constructions.

The growing market can be explained by an increased demand for more resistant and high-quality materials that are able to comply with modern structural and environmental requirements and certifications. Manufacturers strive to meet environmental regulations and circular economy demands and are introducing innovative low-carbon cement solutions and recycled aggregates as well as high-efficiency insulation solutions for masonry materials. The combination of increased demand for infrastructure renovation in mature economies and construction activities in developing countries creates a solid demand base throughout the forecast period.

Construction Materials Market Size and Forecast

-

Market Size in 2025: USD 1,419.06 Billion

-

Market Size by 2035: USD 2,093.61 Billion

-

CAGR: 3.98% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Construction Materials Market - Request Free Sample Report

Construction Materials Market Trends

-

The increase in infrastructure spending among governments in Asia-Pacific, the Middle East, and Latin America regions creates long-term demand forecasts for construction aggregates, cement, and structural metals, with government infrastructure development initiatives, such as the construction of roadways, railways, seaports, and urban transit systems ensuring long-term demand forecasts for construction material supplies, which are independent of market cycles and influenced by the private sector.

-

Increasing trends toward low carbon and sustainable cementitious construction material usage include the use of blended cement using fly ash, ground granulated blast furnace slag, and calcined clay clinker substitutes that have been specified in major infrastructure and commercial construction projects in Europe and North America.

-

Pre-fabricated and modular building methods increase the demand for pre-cast concrete, steel precast structural systems, and modular metal framing systems and reduce on-site aggregate and wet cement usage due to their factory-manufactured properties.

-

The growing trend of reusing and recycling construction materials for reuse includes recycled concrete, asphalt, bricks, masonry blocks, wood products, and metals that will be specified in construction projects across European member states, with regulations requiring a certain percentage of recycled content in all government-funded construction infrastructure projects.

-

Digital construction platforms and building information modeling integration are improving construction material planning accuracy, reducing waste generation on project sites, and creating more predictable procurement volumes for material suppliers, while also enabling tighter supply chain coordination between materials producers, distributors, and construction contractors.

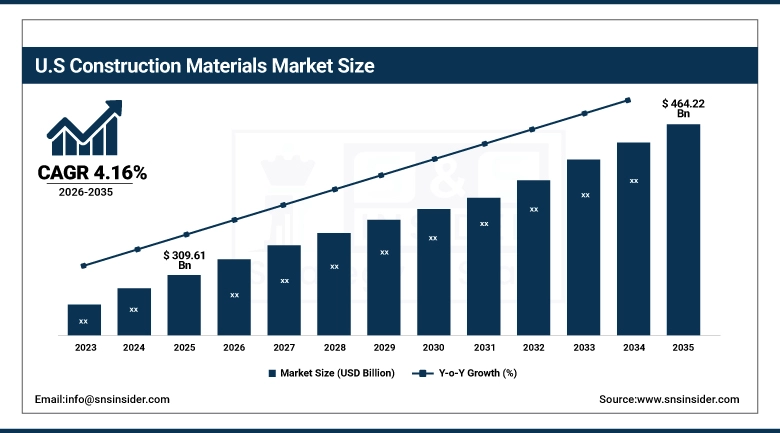

U.S. Construction Materials Market was valued at USD 309.61 billion in 2025 and is expected to reach USD 464.22 billion by 2035, growing at a CAGR of 4.16%.

US Construction Material Market represents the biggest domestic market in North America, fueled by massive government spending on infrastructure via the Infrastructure Investment and Jobs Act, the active process of building residential structures due to unrelenting housing demand in important metropolitan areas and suburbs, and the development of commercial and industrial properties within growth centers in the Sun Belt and Mountain West zones. Aggregates and cement account for the biggest material volumes used domestically, while the major buyers for commodity construction materials include ready-mix concrete makers, precast manufacturers, and road construction contractors.

Construction Materials Market Segment Analysis

-

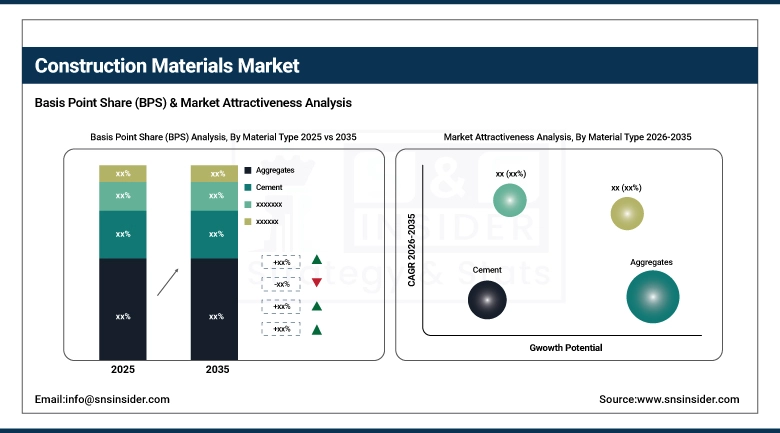

By Material Type, Aggregates dominated with ~29.10% share in 2025; Aggregates is also the fastest-growing material type segment with a CAGR of 5.70%.

-

By End-User, Infrastructure dominated with ~44.18% share in 2025; Residential is the fastest-growing end-user segment with a CAGR of 4.72%.

By Material Type: Aggregates dominate, Cement second largest by value

Aggregates held approximately 29.10% of the Construction Materials Market in 2025 is projected to grow at the fastest CAGR of 5.70% among all material types through the forecast period. Aggregates including crushed stone, sand, and gravel serve as the foundational volumetric component of concrete, asphalt pavement, and drainage infrastructure, making them the highest-consumption construction material by tonnage in virtually every country. The direct correlation between aggregate demand and infrastructure construction activity—particularly road building, highway resurfacing, bridge reconstruction, and rail bed preparation—ties aggregate market growth closely to government capital spending programs, which are expanding across Asia Pacific, the Middle East, and North America through the forecast period.

By End-User: Infrastructure dominates, Residential second largest

The Infrastructure end-user segment dominated the Construction Materials Market with approximately 44.18% share in 2025. Infrastructure construction encompasses road and highway networks, bridges and tunnels, rail systems, airports, ports, water and wastewater treatment facilities, energy generation and transmission infrastructure, and telecommunications network buildout, all of which are intensive consumers of aggregates, cement, structural steel, and specialty construction materials. Government infrastructure programs across Asia Pacific, the Middle East, North America, and Europe are providing multi-year funded demand pipelines that support material procurement planning and supply chain investment by major construction material producers.

The Residential end-user segment, is projected to grow at the fastest CAGR of 4.72% through the forecast period, driven by population growth, household formation rates, urbanization in developing economies, and housing stock renewal in mature markets. Residential construction material demand spans foundation aggregates and concrete, structural masonry and framing systems, roofing materials, and finishing products across a broad range of dwelling types from single-family detached homes to high-density urban apartment towers. Housing shortfalls in major urban markets across North America, Europe, India, and Southeast Asia are sustaining residential construction activity at levels that support consistent material demand growth above the broader economic growth rate in many geographies.

Construction Materials Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

79% |

|

Europe |

Germany |

23% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

Saudi Arabia |

29% |

|

Latin America |

Brazil |

47% |

North America Construction Materials Market Insights

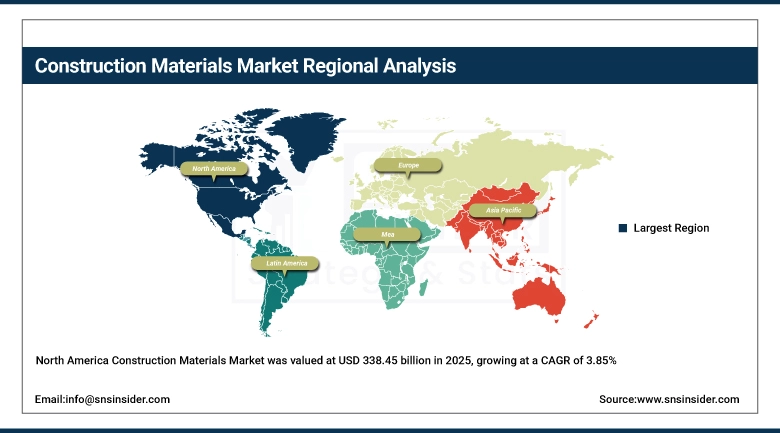

The North America Construction Materials Market was valued at USD 338.45 billion in 2025, growing at a CAGR of 3.85%, with the United States representing the dominant national market. Federal infrastructure investment through multi-year legislative funding programs, sustained residential construction demand driven by persistent housing shortfalls in major metropolitan areas, and active industrial and data center construction programs are collectively sustaining construction material demand across aggregate, cement, metal, and specialty product categories. Canada contributes a meaningful secondary market volume supported by urban residential construction in Toronto, Vancouver, and Montreal, ongoing northern resource extraction facility construction, and federal infrastructure co-investment programs with provincial governments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Construction Materials Market Insights

The Europe Construction Materials Market was valued at USD 275.58 billion in 2025, growing at a CAGR of 3.42%, with Germany, France, the United Kingdom, and Nordic countries as the primary national markets. European construction material demand is supported by ongoing residential renovation programs responding to EU energy efficiency directives that require thermal upgrading of existing building stock, infrastructure maintenance and modernization investment by national governments, and sustained commercial construction activity in major urban centers. The European Green Deal and Fit for 55 legislative framework are driving significant reformulation investment by cement producers, aggregate processors, and steel manufacturers operating in the region to meet embodied carbon reduction requirements being introduced in green building certification standards and public procurement specifications.

Asia Pacific Construction Materials Market Insights

Asia Pacific is the largest and fastest-growing regional Construction Materials Market projected to grow at a CAGR of 5.21%—the highest among all regions. China is the dominant national market, accounting for the majority of regional cement and aggregate consumption through a construction program of infrastructure, residential, and commercial development that remains the largest in the world by volume despite a moderation in residential property market activity. India is the fastest-growing national market within Asia Pacific, driven by the National Infrastructure Pipeline program targeting multi-trillion rupee investment in roads, rail, airports, and urban infrastructure over a ten-year horizon, alongside a housing construction program supporting demand for cement, aggregates, and masonry materials across both urban and rural construction contexts.

Latin America Construction Materials Market Insights

Latin America Construction Materials Market was headed by Brazil, Mexico, Colombia, and Peru. In terms of national market size, Brazil accounted for the largest national market owing to its large domestic cement production capacity, domestic construction of residential buildings via affordable housing initiatives of the government, and construction of road networks and ports. Mexico was witnessing an increase in its requirement of construction materials on account of housing construction within the nation, establishment of industries in manufacturing hubs in connection with the supply chains for USMCA, and the urban infrastructure initiatives being carried out in cities such as Mexico City, Guadalajara, and Monterrey.

Middle East & Africa Construction Materials Market Insights

Middle East & Africa Construction Materials Market The Gulf Cooperation Council (GCC) nations such as Saudi Arabia, the United Arab Emirates, and Qatar continue to have high consumption of construction materials due to massive investments in infrastructure and urban development projects that fit within their plans for economic diversification, as evidenced by the Saudi Arabia Vision 2030 plan, which happens to be one of the biggest investment plans in the world for construction. In sub-Saharan Africa, the need for construction materials continues to rise, albeit from a lower base but at an increasingly rapid pace owing to urbanization, rising populations, and higher government spending on infrastructure in countries like Nigeria, Ethiopia, Kenya, and Ghana.

Market Growth Drivers:

-

Government infrastructure investment programs and urbanization-driven residential construction sustaining structural demand growth across construction material categories

In the market for construction materials, there are several structural drivers which make up the backbone of demand, acting alongside each other in a manner which is largely independent of one another. These include government-led infrastructure projects which involve lengthy contracts for the purchase of aggregate materials, cement, and steel; and construction work carried out by the private sector due to increases in the population and affordability measures implemented on houses. This ensures that the market is more resistant to economic cycles than purely commercial or industrial construction use, as infrastructure purchases remain consistent throughout economic downturns, thereby balancing the sharp decline in private demand.

Market Restraints:

-

Carbon regulation pressure on cement and steel production and raw material supply constraints creating cost and availability challenges

Construction material suppliers are under considerable cost pressure due to the introduction of carbon taxes, cap-and-trade systems, and environmental regulations that affect the economics of producing cement, steel, and aggregates. Cement manufacturers contribute around 7-8% of worldwide CO2 emissions and thus are targeted by decarbonization policies in Europe and becoming so in North America and Asia Pacific, which requires costly investments in carbon capture, alternative fuel utilization, and clinker substitutions to produce their goods compared to traditional methods. The aggregate industry also suffers from permitting and quarries restrictions, as land use conflicts, conservation requirements, and transport issues limit the expansion of extraction locations near urban markets for construction materials.

Market Opportunities:

-

Low-carbon material innovation, emerging market infrastructure investment, and circular economy material recovery creating long-term growth opportunities

The development of low-carbon construction materials is an important area of product innovation potential for cement manufacturers, aggregates producers, and steel makers, as the growing emphasis on green building rating programs, sustainable government procurement practices, and company pledges to reduce the carbon intensity of their real estate portfolios have created a premium market for certified low-carbon construction materials. Materials such as supplementary cementitious materials, green steel made through renewable electricity-powered electric arc furnace operations, and recycled aggregate materials that meet carbon intensity certification criteria are gaining increased access to procurement funding at contracting firms targeting lower levels of embodied carbon intensity. Growth in emerging market infrastructure investments in Sub-Saharan Africa, South Asia, and Southeast Asia are the highest volume construction material market opportunities, as emerging market infrastructure investment rates rise to levels seen in developed nations.

Recent Developments:

-

2025: LafargeHolcim (Holcim Group) introduced its ECOPact range of concrete products in 12 new domestic markets, increasing its global presence from 43 to 55 countries and providing a standardized range of products which offer 30-90% lower carbon footprint per cubic meter compared to traditional concrete product mixes, resulting in the sale of more than 10 million cubic meters of ECOPact products three years after launch.

-

2025: Vulcan Materials Company, the largest aggregates supplier in the United States, completed a USD 1.05 billion acquisition of a regional competitor involved in aggregates mining in the southeastern part of the U.S., increasing its aggregate reserves by 1.4 billion metric tons in Florida, Georgia, and Tennessee, where growth prospects in construction infrastructure and residential projects are anticipated during the coming decade.

Construction Materials Market Key Players

Some of the Construction Materials Market Companies

-

Holcim Group (LafargeHolcim)

-

HeidelbergCement AG (Heidelberg Materials)

-

CRH plc

-

Vulcan Materials Company

-

Martin Marietta Materials, Inc.

-

CEMEX S.A.B. de C.V.

-

Saint-Gobain S.A.

-

Wienerberger AG

-

ArcelorMittal

-

Nucor Corporation

-

Boral Limited

-

James Hardie Industries plc

-

Compagnie de Saint-Gobain

-

USG Corporation (Knauf Group)

-

Summit Materials, Inc.

-

Eagle Materials Inc.

-

Sika AG

-

GCP Applied Technologies (Saint-Gobain)

-

Kingspan Group plc

-

UltraTech Cement Limited

Construction Materials Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,419.06 Billion |

| Market Size by 2035 | USD 2,093.61 Billion |

| CAGR | CAGR of 3.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Aggregates, Cement, Bricks and Blocks, Metals, Others) • By End-User (Infrastructure, Residential, Commercial, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Holcim Group, HeidelbergCement AG (Heidelberg Materials), CRH plc, Vulcan Materials Company, Martin Marietta Materials Inc., CEMEX S.A.B. de C.V., Saint-Gobain S.A., Wienerberger AG, ArcelorMittal, Nucor Corporation, Boral Limited, James Hardie Industries plc, Compagnie de Saint-Gobain, USG Corporation (Knauf Group), Summit Materials Inc., Eagle Materials Inc., Sika AG, GCP Applied Technologies (Saint-Gobain), Kingspan Group plc, UltraTech Cement Limited. |

Frequently Asked Questions

Asia Pacific is expected to grow at the fastest CAGR of 5.21% in the Construction Materials Market.

Infrastructure dominated with approximately 44.18% share in 2025.

Aggregates dominated with approximately 29.10% share in 2025.

The Construction Materials Market was valued at USD 1,419.06 Billion in 2025.

The Construction Materials Market is expected to grow at a CAGR of 3.98% from 2026 to 2035.

Get in Touch