Construction Robots Market Report Scope & Overview:

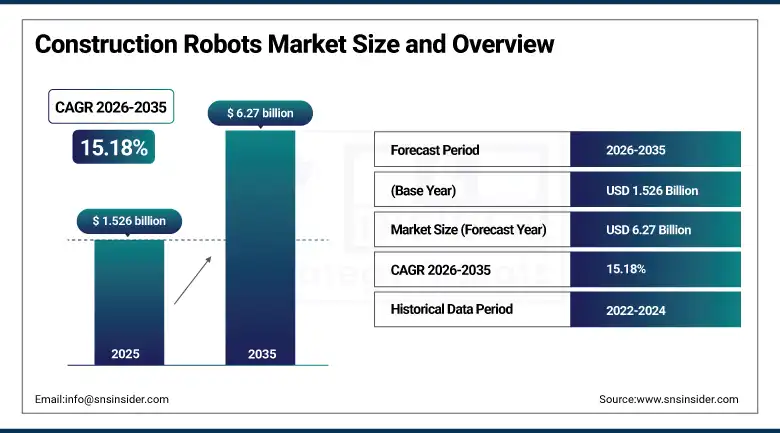

The Construction Robots Market was valued at USD 1.526 billion in 2025 and is expected to reach USD 6.27 billion by 2035, growing at a CAGR of 15.18% from 2026–2035.

The global construction robots market is experiencing unprecedented commercial growth as the integration of advanced robotics, artificial intelligence, machine learning, and precision sensor technologies into construction workflows is systematically addressing the most persistent structural challenges of the construction industry: chronic skilled labour shortages, escalating labour costs, inconsistent workmanship quality, unacceptable rates of fatal and serious workplace accidents, and the inability of conventional manual construction methods to meet the accelerating pace and quality standards that modern infrastructure and building programmes demand. Construction robots encompass a diverse and rapidly expanding portfolio of automated systems including demolition robots that safely break apart concrete structures without exposing human workers to collapse, vibration, and dust hazards; bricklaying and masonry robots that achieve consistent mortar joint quality and placement accuracy at speeds unachievable by human masons; concrete printing robots that fabricate complex architectural forms through layered concrete deposition; welding robots that deliver consistent weld quality across structural steel connections; and inspection drones that provide comprehensive site monitoring through aerial photography, LiDAR scanning, and thermal imaging. The construction robots market benefits from the simultaneous acceleration of urbanisation in emerging economies demanding unprecedented construction output, and the construction industry's labour crisis in developed economies where an ageing craft workforce is not being replaced by younger workers at rates sufficient to maintain project delivery capacity.

January 2025's Brokk Inc. appointment as North American distributor for Darda and Komatsu's CES 2025 showcase of its innovative lunar construction excavator and underwater construction robot demonstrate that the construction robotics innovation ecosystem is advancing simultaneously on multiple fronts: commercial market development through expanded distribution partnerships and breakthrough technology demonstrations that expand construction robot application boundaries beyond terrestrial projects.

Market Size and Forecast

-

Market Size in 2026E: USD 1.76 Billion

-

Market Size by 2035: USD 6.27 Billion

-

CAGR (2026–2035): 15.18%

-

Fastest Growing Market: Asia Pacific

-

Largest Market: North America

To Get more information On Construction Robots Market - Request Free Sample Report

Construction Robots Market Trends

-

Rapid advancement of AI-powered construction robot navigation and task execution systems, where machine learning algorithms trained on construction site sensor data enable robots to adaptively execute complex tasks in the unstructured, dynamically changing environments that distinguish construction sites from the controlled factory floors where industrial robots have traditionally operated.

-

Growing development of collaborative construction robots (cobots) designed to work safely alongside human construction workers without the physical barriers required by conventional industrial robots, enabling hybrid human-robot construction workflows where robotic systems handle the most physically demanding, repetitive, and hazardous tasks while skilled human workers perform the judgement-intensive coordination and quality assurance functions.

-

Accelerating adoption of construction drones for site monitoring, progress tracking, and aerial inspection functions that provide project managers with real-time documentation of construction progress, structural condition, and safety compliance status across large construction sites without requiring manual inspection from elevation-exposed positions.

-

Rising investment in modular and prefabrication construction techniques that are inherently more robotics-compatible than traditional site-assembled construction, where standardised component manufacturing in controlled factory environments enables higher robot utilisation rates and more consistent automated assembly quality than variable on-site conditions allow.

-

Growing integration of construction robots with Building Information Modelling data streams, where robots access digital building models to guide precise component placement, structural inspection, and as-built documentation that creates a continuous feedback loop between design intent and physical construction reality.

The U.S. Construction Robots Market Size Outlook

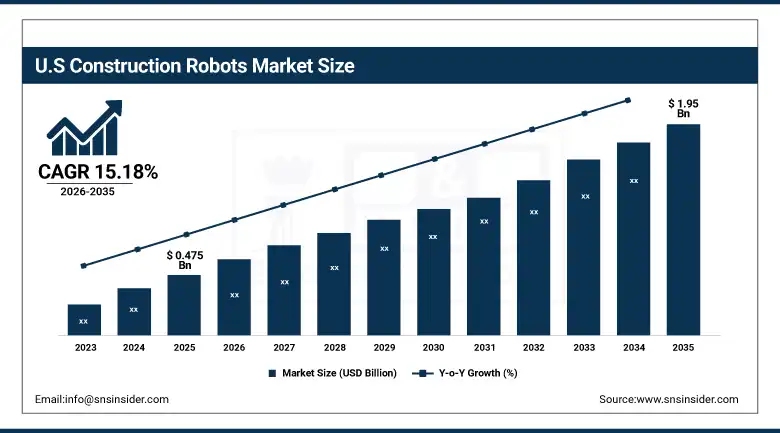

The U.S. Construction Robots Market was valued at approximately USD 0.475 billion in 2025 and is expected to reach approximately USD 1.95 billion by 2035, growing at a CAGR of 15.18% during 2026–2035.

The United States leads the North American construction robots market as the world's most commercially advanced construction technology adoption environment, driven by the acute construction labour shortage across all trade categories that the U.S. Bureau of Labor Statistics estimates at over 600,000 unfilled construction job openings, creating the strongest economic imperative for construction robot adoption of any national market. The Bipartisan Infrastructure Law's multi-year construction programme creating extraordinary demand for construction workforce capacity combined with insufficient workforce supply is the most commercially compelling demand driver for construction robot adoption in the history of the U.S. construction industry. Technology companies including Built Robotics, Dusty Robotics, Trimble, and Scaled Robotics are commercialising construction robot products targeting the specific U.S. construction workflow patterns and safety requirements that define the world's largest national construction robot market.

January 2025's Komatsu CES 2025 showcase of construction robots for extreme applications including lunar surface and underwater construction demonstrates that the leading construction equipment manufacturers are investing in robotics capabilities that extend well beyond conventional construction applications, creating platform technologies applicable across the full spectrum of built environment creation from conventional commercial construction through the most technically demanding frontier infrastructure applications, sustaining long-term product development investment that benefits the broader construction robot commercial market.

Construction Robots Market Segment Analysis

-

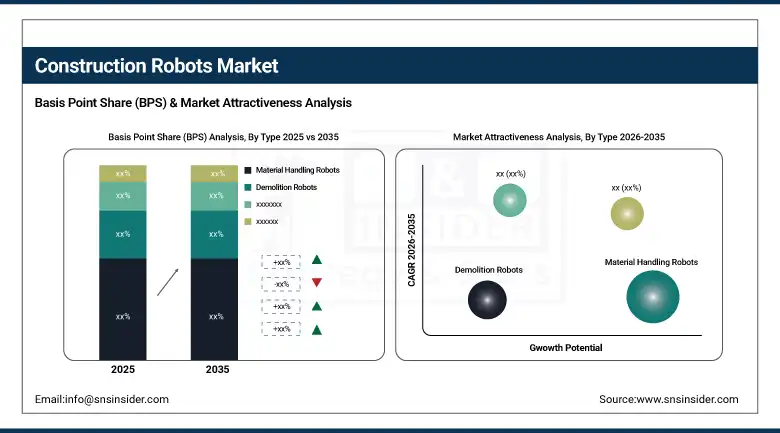

By Type, material handling robots dominated with approximately 35% market share in 2025; demolition robots are the fastest-growing type at approximately 26.53% CAGR.

-

By Autonomy Level, semi-autonomous robots dominated with approximately 58% market share in 2025; fully autonomous robots are growing fastest at approximately 18.24% CAGR.

-

By Application, industrial dominated with approximately 43% of revenues in 2025; residential is the fastest-growing application at approximately 18.64% CAGR.

By Type, material handling dominates, demolition is expected to grow fastest

Material Handling Robots retained the dominant type position with approximately 35% of the construction robots market in 2025, reflecting their universal applicability across every construction site category where the transportation, lifting, and precise placement of heavy and awkward building materials including concrete elements, steel sections, prefabricated components, and building materials constitutes one of the most labour-intensive, physically hazardous, and time-consuming activities in the entire construction process. Automated material handling robots address both the labour scarcity challenge and the workplace safety imperative simultaneously, removing the lifting injury, musculoskeletal strain, and accident risk from material handling tasks that are among the most common causes of construction worker injuries and fatalities globally.

Demolition Robots are the fastest-growing construction robot type at approximately 26.53% CAGR through 2035, driven by the extraordinary commercial and safety value proposition of remote-controlled and increasingly autonomous demolition robots in urban building removal, concrete breaking, and hazardous structure deconstruction applications where human demolition worker exposure to collapse, vibration, silica dust, and toxic material hazards is progressively unacceptable under tightening occupational health and safety regulations. Brokk Inc.'s expanded North American distribution and product portfolio demonstrates the growing commercial market for professional demolition robot equipment across the U.S. and Canadian construction markets.

By Application, industrial dominates, residential is expected to grow fastest

Industrial retained the dominant application position with approximately 43% of the construction robots market in 2025, reflecting the concentration of the highest-value and most technically demanding construction robot applications in large-scale factory, warehouse, power plant, and data centre construction where project scale, quality requirements, and construction timelines create compelling economic cases for robotics investment. Industrial construction projects' scale provides the volume of repetitive tasks, standardised components, and extended construction duration that justify the capital investment in specialised construction robots whose unit economics improve rapidly at higher utilisation rates.

Residential is the fastest-growing application segment at approximately 18.64% CAGR through 2035, driven by the global housing shortage creating extraordinary pressure to increase residential construction output at lower cost and with fewer skilled workers than conventional construction methods require. Construction robotics systems including Hadrian X's automated bricklaying robot and various concrete wall printing systems capable of fabricating complete residential structures through automated concrete extrusion demonstrate the emerging technology platforms that could transform residential construction productivity from the current labour-intensive artisanal model toward a more automated, reproducible, and scalable construction model.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82% |

|

Asia Pacific |

Japan |

35% |

|

Europe |

Germany |

29% |

|

Middle East & Africa |

UAE |

27% |

|

Latin America |

Brazil |

43% |

North America Construction Robots Market Insights

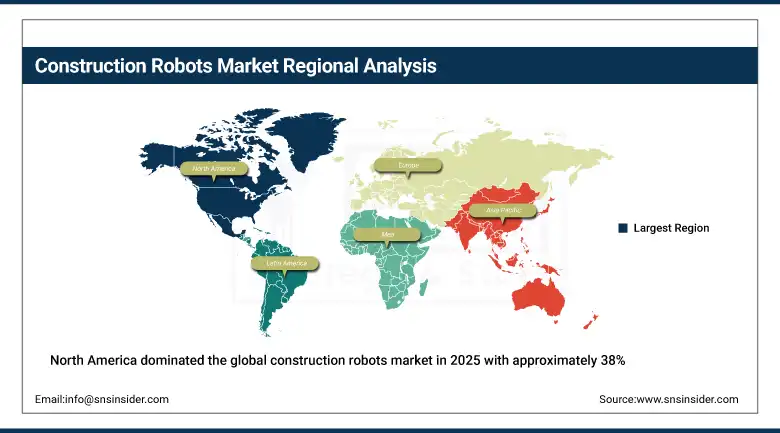

North America dominated the global construction robots market in 2025 with approximately 38% of revenues, led by the United States at approximately 82% of North American revenues. U.S. market leadership is driven by the most acute construction labour shortage, the highest construction robot technology adoption rate, the largest commercial construction robot company ecosystem including Built Robotics, Dusty Robotics, and Trimble Robotics, and the Bipartisan Infrastructure Law creating extraordinary construction demand that amplifies the labour gap driving robot adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Construction Robots Market Insights

Europe is a sophisticated construction robot market driven by Germany's precision engineering culture enabling advanced construction robot product development, the UK's smart construction programme driving adoption across public infrastructure projects, and EU-wide construction safety regulations creating compliance-driven demand for robotic solutions that reduce worker hazard exposure in demolition and concrete work applications.

Asia Pacific Construction Robots Market Insights

Asia Pacific is the fastest-growing regional construction robot market, driven by rapid urbanisation in China, India, and Southeast Asia creating extraordinary construction output requirements, Japan's advanced robotics culture and severe construction labour shortage driving world-leading construction robot technology development at companies including Komatsu, Shimizu, and Kajima, and South Korea's government-supported smart construction technology programme accelerating construction robot adoption across major construction companies.

Latin America and MEA Construction Robots Market Insights

Latin America and MEA are growing construction robot markets driven by large-scale infrastructure investment programmes creating construction output requirements that exceed available skilled labour supply. UAE and Saudi Arabia's NEOM and Vision 2030 megaproject construction programmes are creating substantial construction robot adoption in the Gulf region, while Brazil and Mexico's growing construction industries are beginning to adopt robotic systems for the most hazardous and labour-intensive construction tasks.

Market Dynamics

Growth Drivers: Global construction labour shortage and AI integration expanding robot capability and commercial viability across construction applications

The primary structural growth driver for the construction robots market is the global construction industry's deepening skilled labour crisis, where demographic ageing of the existing construction workforce combined with declining interest among younger workers in physically demanding construction careers is creating a structural workforce deficit that no amount of wage increase can fully resolve in the near term, making robotic automation the only technically viable pathway to maintaining construction output at the volumes that urbanisation, infrastructure investment, and residential demand programmes require.

The January 2025 Brokk and Darda North American distribution partnership and Komatsu's CES 2025 construction robot showcases collectively confirm that both the commercial distribution infrastructure and the technology innovation pipeline supporting the construction robots market are advancing simultaneously, creating the market development conditions that sustain the market's 15.18% CAGR through the 2026 to 2035 forecast period as robot capabilities progressively expand the range of construction tasks addressable by automation.

Restraints: High initial capital investment, complex unstructured construction site environments, and regulatory frameworks lagging behind robot capabilities

A significant restraint on the construction robots market is the high initial capital cost of professional construction robot systems, where demolition robot platforms, bricklaying robots, and autonomous material handling systems command purchase prices of USD 100,000 to USD 500,000 or more per unit that require substantial construction project scale and robot utilisation rates to justify through productivity improvement return on investment. The inherent complexity and variability of construction site environments, where changing layouts, irregular surfaces, weather exposure, and simultaneous multi-trade activity create dynamic conditions that challenge even advanced robot navigation and task execution systems, limit the range of construction applications where current robot technology achieves consistent performance competitive with skilled human workers.

Opportunities: Modular and prefabrication construction integration, infrastructure inspection automation, and emerging market construction robot adoption

The rapid growth of modular and prefabrication construction techniques that perform component manufacturing in controlled factory environments represents the most immediately robot-compatible construction market expansion, where standardised factory conditions enable industrial robot deployment from automotive manufacturing with minimal adaptation and demonstrate construction robot economics at scales and quality standards impossible on conventional construction sites. Construction infrastructure inspection automation through drone surveys, robotic structural inspection systems, and LiDAR-based as-built documentation represents a large and rapidly growing construction robot application category where the safety, cost, and quality advantages of robotic inspection over manual high-elevation and confined-space inspection are commercially compelling across bridge, tunnel, high-rise, and industrial facility maintenance markets.

Recent Developments:

-

2026: Brokk AB launched the upgraded Brokk 110+ and 130+ demolition robots in 2026 with SmartPower+ technology to improve efficiency, reliability, and remote-controlled demolition performance.

-

2026: Komatsu Ltd. expanded deployment of Intelligent Machine Control (IMC) 3.0 autonomous excavation technologies in 2026 to enhance precision, automation, and productivity in construction operations.

-

2026: Built Robotics Inc. continued expanding autonomous heavy equipment solutions in 2026, focusing on AI-enabled excavation and earthmoving systems for infrastructure and utility construction projects.

Construction Robots key players are:

-

Brokk AB

-

Komatsu Ltd.

-

Built Robotics Inc.

-

Dusty Robotics Inc.

-

Trimble Inc.

-

Boston Dynamics Inc.

-

Fanuc Corporation

-

KUKA AG

-

Yaskawa Electric Corporation

-

Shimizu Corporation

-

Kajima Corporation

-

Fastbrick Robotics (FBR Ltd.)

-

Construction Robotics LLC

-

Husqvarna Group

-

Hilti Group

-

Ekso Bionics Holdings Inc.

-

Advanced Construction Robotics Inc.

-

Scaled Robotics SL

-

Cazza Technologies Inc.

-

Caterpillar Inc.

Construction Robots Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.526 Billion |

| Market Size by 2035 | USD 6.27 Billion |

| CAGR | CAGR of 15.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Demolition Robots, Bricklaying Robots, Concrete Robots, Welding Robots, Inspection Robots, Material Handling Robots, Drones and Aerial Robots, Others) • By Autonomy Level (Semi-Autonomous, Fully Autonomous) • By Application (Residential, Commercial, Industrial, Infrastructure, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Brokk AB, Komatsu Ltd., Built Robotics Inc., Dusty Robotics Inc., Trimble Inc., Boston Dynamics Inc., Fanuc Corporation, KUKA AG, Yaskawa Electric Corporation, Shimizu Corporation, Kajima Corporation, Fastbrick Robotics (FBR Ltd.), Construction Robotics LLC, Husqvarna Group, Hilti Group, Ekso Bionics Holdings Inc., Advanced Construction Robotics Inc., Scaled Robotics SL, Cazza Technologies Inc., Caterpillar Inc. |

Frequently Asked Questions

Residential is the fastest-growing application at approximately 18.64% CAGR.

Material handling robots dominated with approximately 35% of revenues in 2025.

The global construction industry's deepening skilled labour crisis where demographic ageing of the construction workforce and declining younger worker interest in construction.

The construction robots market was valued at USD 1.526 billion in 2025.

The construction robots market is expected to grow at a CAGR of 15.18% from 2026 to 2035.

Get in Touch