Contract Management Software Market Report Scope & Overview:

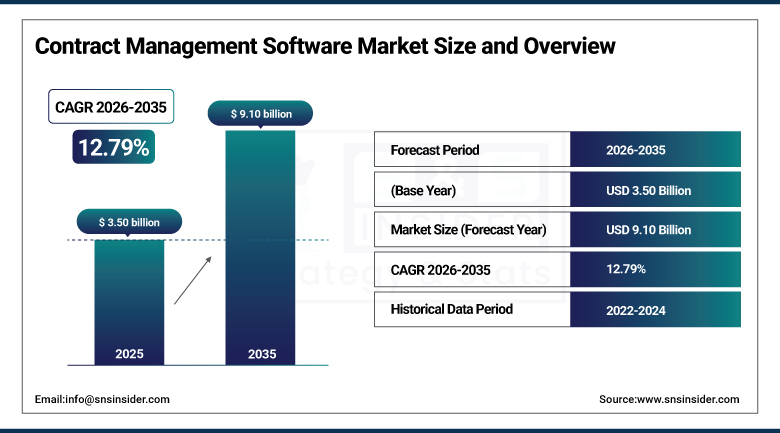

The Contract Management Software Market was valued at USD 3.50 Billion in 2025 and is expected to reach USD 9.10 Billion by 2035, growing at a CAGR of 12.79% from 2026 to 2035.

This report provides a detailed analysis of the Contract Management Software Market, presenting key statistical insights. It highlights how feature utilization patterns have evolved, with increasing adoption of AI based contract analytics, automated approval workflows, and obligation tracking functionalities. The market continues to see strong uptake from end user industries such as BFSI, healthcare, and IT, driven by rising regulatory demands, complex contract volumes, and the need for operational transparency. Integration capabilities with enterprise systems like ERP, CRM, and procurement platforms have become a critical purchase criterion as businesses seek unified data visibility and process automation. The latest edition introduces emerging trends such as generative AI powered contract drafting, predictive obligation management, and ESG clause monitoring tools, reflecting the market's shift toward intelligent, context aware contract lifecycle management solutions.

In 2024, DocuSign Inc. launched DocuSign Maestro, a no code workflow builder that enables enterprises to automate complex multi party agreement processes without requiring developer resources. The product launch reflects the growing commercial direction of contract management software toward democratized automation, where business users in legal, procurement, and finance teams can configure sophisticated workflow automations independently, reducing the IT dependency that has historically constrained contract process improvement initiatives in large and mid market enterprise environments.

Market Size and Forecast

-

Market Size in 2026E: USD 3.95 Billion

-

Market Size by 2035: USD 9.10 Billion

-

CAGR: 12.79% from 2026 to 2035

-

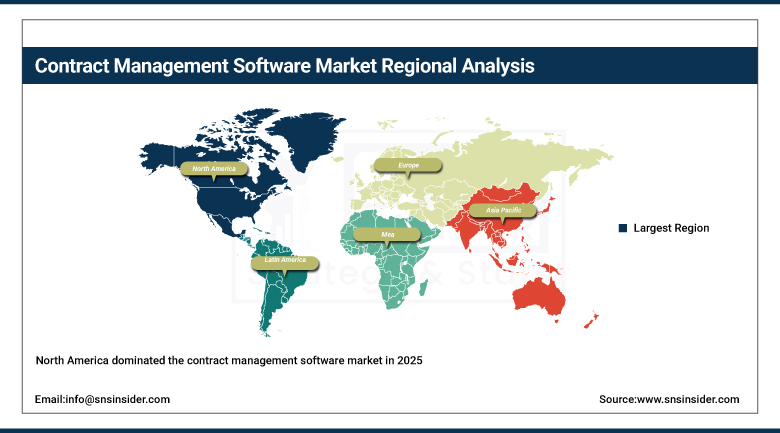

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Contract Management Software Market - Request Free Sample Report

Contract Management Software Market Trends

-

Increasing adoption of AI based contract analytics, automated approval workflows, and obligation tracking is transforming contract lifecycle management from a manual administrative function into a strategic enterprise capability.

-

Generative AI integration in contract drafting tools is enabling faster clause suggestion, risk identification, and template generation, materially reducing the time that legal teams spend on routine contract creation tasks.

-

Rising demand for contract management software with ERP, CRM, and procurement platform integration capability is reshaping purchase criteria as enterprises prioritize end to end data visibility over standalone contract management functionality.

-

Growing focus on ESG clause monitoring and regulatory reporting within contract management platforms reflects the expanding scope of contract obligations that enterprises must systematically track across their counterparty relationships.

-

Expansion of cloud based contract management software is reducing barriers to adoption for SMEs, with subscription pricing and rapid deployment enabling smaller organizations to access enterprise grade contract lifecycle management capability.

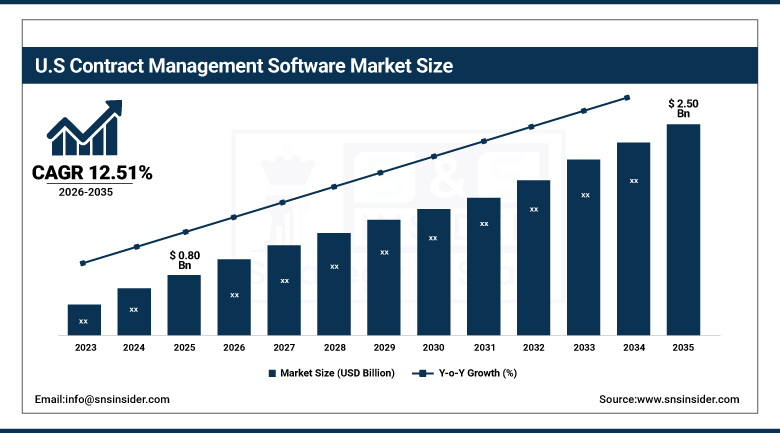

U.S. Contract Management Software Market Outlook

The U.S. Contract Management Software Market was valued at approximately USD 0.80 Billion in 2023 and is expected to reach approximately USD 2.50 Billion by 2032, growing at a CAGR of approximately 12.51%.

This growth is driven by increasing demand for process efficiency and automation, as well as rising The growth of this industry is due to the growing demand for process efficiency and automation and investment in next-generation technologies. In the US market, the high density of technology adopters in BFSI, healthcare, IT, and manufacturing industries, whose complex contract volumes and regulatory compliance needs drive structural demand for automated contract lifecycle management. There have been reports from organizations of a 30 to 40% reduction in the contract turnaround time after adopting the software, providing the companies with the quantifiable return on investment in making enterprise procurement decisions.

In 2023, Icertis increased the functionality of their Icertis Contract Intelligence platform through the use of generative AI features, including contract data extraction and risk analysis, allowing enterprise users to automatically process large volumes of contracts without manual intervention. The addition of the new capabilities highlights the commercial success of the generative AI adoption in enterprise contract management, where the need for structured data extraction from unstructured legacy contracts brings immediate productivity gains.

Contract Management Software Market Segment Analysis

-

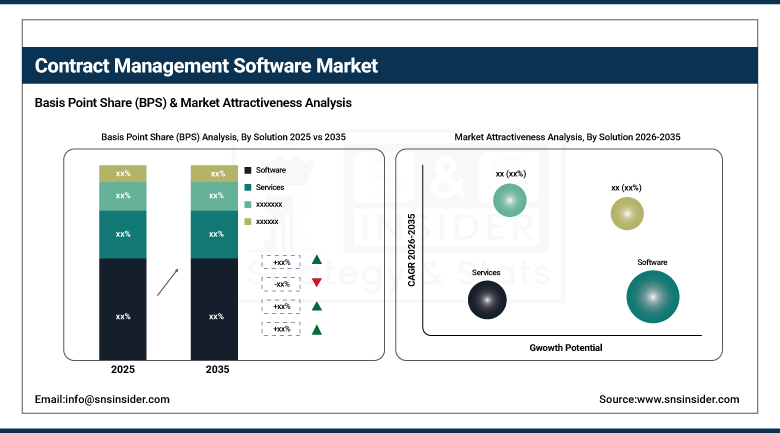

By Solution, the Software segment dominated the Contract Management Software Market with approximately 69.00% share in 2025, while the Services segment is the fastest growing.

-

By Business Function, the Procurement segment dominated the Contract Management Software Market with approximately 28.00% share in 2025, while the HR segment is the fastest growing.

-

By Enterprise Size, the Large Enterprises segment dominated the Contract Management Software Market with approximately 66.00% share in 2025, while the SMEs segment is the fastest growing.

-

By Industry, the Services Industry segment dominated the Contract Management Software Market with approximately 26.00% share in 2025, while the Public Sector segment is the fastest growing.

By Solution, software dominates, services grow fastest

Software emerged as the largest revenue generator in the contract management software market in 2025 with a share of 71%, attributable to its capability to automate complicated processes, enhance contract visibility, and reduce chances of human error. The increasing demand for intelligent applications, which include automatic clause recognition, risk identification, and predictive obligations, has been responsible for the widespread adoption of the software in BFSI, healthcare, IT, and manufacturing industries. Cloud-based and on-premises software solutions offer flexibility and scalability to both large enterprises and SMEs. In light of increased compliance and digitalization requirements, the segment is likely to continue its dominance during the forecast period through continuous innovation of platforms with the help of generative AI and workflow automation features.

The Services segment is expected to register the fastest CAGR during the forecast period, driven by the increasing demand for implementation, customization, integration, and managed services. As organizations deploy more sophisticated contract management platforms that must integrate with ERP, CRM, and procurement systems, the need for professional implementation expertise and ongoing optimization support grows correspondingly. Each large enterprise whose contract management transformation requires multi system integration, legacy data migration, and change management support creates services engagement whose scope sustains the segment's accelerating commercial growth trajectory throughout the forecast period.

By Enterprise Size, large enterprises dominate, SMEs grow

In 2025, large enterprises made up the major portion of the contract management software market in terms of revenue, with over 60%, due to the complexity of their contract management processes involving multiple departments in several geographical locations. The need for automation, compliance monitoring, and integration is critical to such enterprises due to the complex nature of the work. In large enterprises, managing tens of thousands to hundreds of thousands of contracts becomes necessary, which makes the implementation of software tools mandatory for them to make sure everything goes smooth. Every single large enterprise that needs to invest in structured contract management software for its compliance and operation reasons contributes to the strong market position of this segment.

SMEs account for a growing and increasingly commercially significant share of the contract management software market as the availability of cost effective, cloud based solutions progressively lowers the barrier to adoption. SMEs seek simplified contract workflows, affordable pricing models, and user friendly interfaces to improve efficiency and stay competitive. The availability of subscription based SaaS contract management tools from vendors including Zoho, PandaDoc, and HubSpot has created structured SME market access that compounds with the growing awareness among smaller businesses of the operational risks and inefficiencies associated with manual contract management processes.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Contract Management Software Market Insights

North America dominated the contract management software market in 2025, driven by the presence of established software vendors, high technology adoption rates, and strong regulatory compliance requirements across BFSI, healthcare, and government sectors. The United States accounts for approximately 87.4% of North American revenues through DocuSign, Icertis, SAP Ariba, and other major platform operators whose combined commercial leadership defines global contract management technology standards.

Canada contributes complementary North American revenue through its growing enterprise software adoption and increasing regulatory complexity across financial services and healthcare sectors that create structured contract management software demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Contract Management Software Market Insights

Europe has an advanced technology market for contract management software in which GDPR regulations and EU regulatory changes drive the formation of institutional demand for contract management systems that provide good data governance and audit trail functions. Germany makes up about 22.3% of the European revenue from its well-established enterprise software adoption in automotive, manufacturing, and financial services industries.

Other important second-tier markets are the United Kingdom and France where their well-established financial services industries and public sector digital transformations drive procurement. The European headquarters of SAP and other enterprise software providers make up the commercial supply side of the region.

Asia Pacific Contract Management Software Market Insights

Asia Pacific is expected to register the fastest CAGR during the forecast period, driven by rapid digital transformation, increasing cloud adoption, and growing regulatory complexity across BFSI, manufacturing, and government sectors in China, India, and Southeast Asia. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary enterprise software market scale and government driven digital economy investment.

India represents the most commercially dynamic emerging market within Asia Pacific where the country's growing IT services sector, expanding enterprise software adoption, and increasing regulatory compliance requirements are driving above average regional contract management software procurement growth.

MEA & Latin America Contract Management Software Market Insights

The UAE generates the most revenue within MEA due to growth in its financial services sector and investments in digitization for the purposes of contract management systems implementation. The vision of 2030 and the resulting digital economy initiatives as well as the increased regulation within Saudi Arabia further contribute to regional demand. Brazil is the leading generator of revenues within Latin America due to a large share of financial services and manufacturing sector that requires contract lifecycle management solutions. México and Argentina will support the market development until 2035.

Growth Drivers: Contract automation demand and AI-powered analytics adoption

With the rise in complexity of business contracts and the stringent regulatory requirements in industries like BFSI, healthcare, and IT, there has been a growing need for advanced contract management solutions. This has led many organizations to deploy software applications that can offer process automation capabilities for activities like contract drafting, approvals, and renewals. With the rising amount of transaction data and the need for real time compliance and risk management, in order to avoid any financial or legal liabilities, there is a move towards structured procurement in enterprise and mid-market segments.

Cloud-based delivery of these applications and the use of AI powered analytics is becoming more prevalent with the benefits of scalability and intelligence that come with these technologies. With the advent of AI in contract management software solutions, there has been a shift in the way enterprises manage their contracts, and the various capabilities that are powered by AI like automatic contract drafting, clause extraction, risk identification, and obligation management have brought about greater efficiency in operations.

Restraints: High implementation costs and integration complexity

Despite the many advantages of using contract management software in an organization, its implementation is a major challenge since there are up-front costs involved. The first major challenge of implementing contract management software is that it should integrate with the standard enterprise system, such as ERP, CRM and procurement systems, which could be highly challenging and involves high IT cost and customization. The process of migration of data from legacy systems as well as data security during integration requires high efforts and investments.

Some firms find resistance to change by their legal and procurement team that prefers working using manual and semi-automated systems. This could be a major barrier to the success rate of the implementation process. This results into delayed return on investment and discourages implementation in organizations with limited IT capability.

Opportunities: Generative AI and ESG compliance monitoring

Inclusion of artificial intelligence and predictive analytics in contract management systems offers an immense opportunity of growth. Automated drafting of contracts, clause extraction, risk detection, and prediction of obligations using AI features have brought about a revolutionary change in the way businesses manage their contracts in large numbers. These tools not only make the processes more efficient but also give insight into the performance of the contract, possible risks, and compliance issues.

Using AI technologies to monitor ESG clauses and prepare reports can add value strategically to the portfolio of the contracts. The move towards smart and automated contract management will create revenues and operational efficiencies for software providers and businesses at the same time. Each business with the requirement to keep its sustainability commitments and monitor ESG clauses in contracts of suppliers and customers will generate structured procurements for contract management software with ESG clause monitoring.

Recent Developments:

-

2024: DocuSign Inc. launched DocuSign Maestro in 2024, a no code workflow builder that enables enterprises to automate complex multi party agreement processes without requiring developer resources.

-

2023: Icertis expanded its Icertis Contract Intelligence platform in 2023 with new generative AI capabilities for contract data extraction and risk analysis, enabling enterprise customers to process large contract repositories automatically.

-

2024: SAP SE expanded its SAP Ariba contract management module in 2024 with enhanced AI powered clause analysis and ESG compliance tracking capabilities targeting enterprise procurement customers.

-

2023: Conga expanded its Conga Contracts platform in 2023 with new generative AI drafting and negotiation assistance tools, targeting legal and sales teams seeking to reduce contract cycle time.

-

2024: Coupa Software expanded its contract management capabilities in 2024 with enhanced spend analytics integration and AI powered obligation management features targeting enterprise procurement leaders.

Contract Management Software Market Key Players

-

DocuSign Inc.

-

SAP SE (SAP Ariba)

-

Conga Corporation

-

Coupa Software Inc.

-

Oracle Corporation

-

Salesforce Inc. (Apttus)

-

Agiloft Inc.

-

Ironclad Inc.

-

ContractSafe LLC

-

Procore Technologies Inc.

-

Juro Ltd.

-

Zoho Corporation

-

Concord Worldwide Inc.

-

Lexion Inc.

-

Evisort Inc.

-

Linkando GmbH

-

Oneflow AB

-

Symfact AG

Contract Management Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.50 Billion |

| Market Size by 2035 | USD 9.10 Billion |

| CAGR | CAGR of 12.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Solution (Software and Services) • by Business Function (Finance, Procurement, Sales & Marketing, Operations, HR, and IT) • by Enterprise Size (SMEs and Large Enterprises) • by Industry (Manufacturing & Resources, Distribution Services, Services Industry, Public Sector, and Infrastructure) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | DocuSign Inc., Icertis Inc., SAP SE (SAP Ariba), Conga Corporation, Coupa Software Inc., Oracle Corporation, Salesforce Inc. (Apttus), Agiloft Inc., Ironclad Inc., ContractSafe LLC, Procore Technologies Inc., Juro Ltd., Zoho Corporation, PandaDoc Inc., Concord Worldwide Inc., Lexion Inc., Evisort Inc., Linkando GmbH, Oneflow AB, Symfact AG |

Frequently Asked Questions

North America dominated the Contract Management Software Market in 2025, while Asia Pacific is expected to register the fastest CAGR through 2035.

The Contract Management Software Market is expected to grow at a CAGR of 12.79% from 2026 to 2035.

The Contract Management Software Market was valued at USD 3.50 Billion in 2025.

The increasing complexity of business contracts alongside stringent regulatory requirements across BFSI, healthcare, and IT driving demand for advanced automation of contract processes, and the integration of AI and predictive analytics within contract management platforms transforming how enterprises handle large contract volumes with intelligent drafting, risk flagging, and obligation management.

Get in Touch