Copper Foil Market Report Scope & Overview:

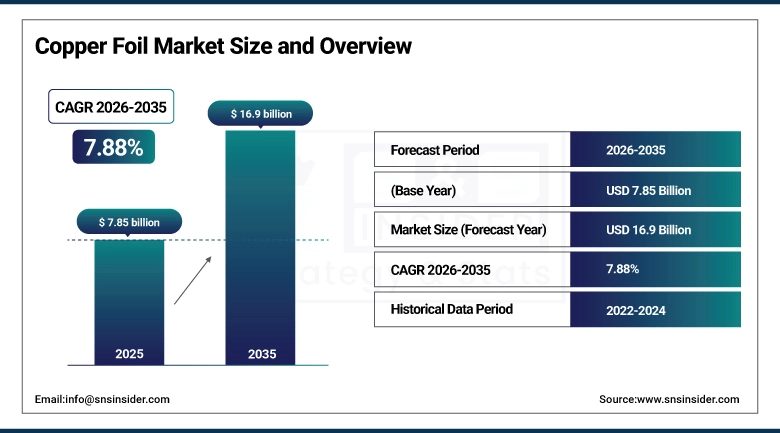

The Copper Foil Market was valued at USD 7.85 billion in 2025 and is expected to reach USD 16.9 billion by 2035, growing at a CAGR of 7.88% from 2026–2035.

Copper Foil is known to be the thin, flat metal sheet comprising mostly of pure copper and is one of the most critical parts in the construction of printed circuit boards (PCB). Copper foil is also used as the anode material of lithium ion batteries. Copper foil is known for its excellent electrical conductivity, thermal resistance, ductile nature, and thinness in manufacture, making it indispensable for both electronic applications and battery technology. The industry is witnessing healthy growth owing to two mega trends; first, is the ongoing trend towards electrification of transport worldwide, requiring vast amounts of copper foils in the manufacturing of EV battery cells, and secondly is the widespread usage of electronics, requiring high-quality copper foils in their PCBs. Ultra-Thin copper foil ranging from 4.5 to 12 microns in thickness, is considered one of the most valuable kinds of copper foils.

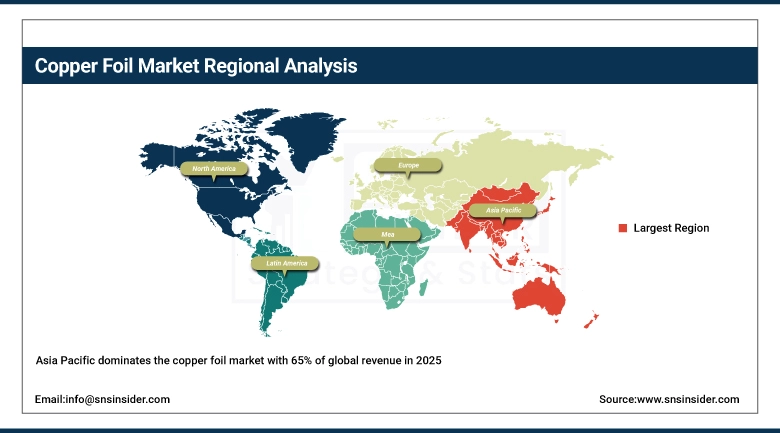

Asia-Pacific holds the major market share in copper foil with a percentage of 65% of the entire globe in 2024, whereby China, South Korea, Japan, and Taiwan hold the lion’s share when it comes to both manufacturing and consumption. It is important to note that China being the world’s leading market in electric vehicles and PCB manufacturer makes it the key player in the value chain.

The transition to ultra-thin copper foil below 6 micrometers is becoming a competitive battleground among global producers. Thinner foil increases the energy density of lithium-ion battery cells by allowing more active electrode material per unit volume, which is critical for extending EV range. Japanese producers including Furukawa Electric and Mitsui Mining & Smelting and Korean producers including SKC are competing intensely on ultra-thin foil quality and production scale.

Market Size and Forecast

-

Market Size in 2025: USD 7.85 Billion

-

Market Size by 2035: USD 16.9 Billion

-

CAGR: 7.88% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Copper Foil Market - Request Free Sample Report

Market Trends

-

EV battery gigafactory construction driving unprecedented demand for ultra-thin copper foil as the critical anode current collector.

-

Ultra-thin copper foil development below 6 micrometers enabling higher energy density battery cells for next-generation EVs.

-

Increased adoption of 5G networks and expansion of AI servers boosting the need for high-quality PCB copper foil.

-

The IRA domestic content provisions within the United States encouraging copper foil manufacturing domestically.

-

Copper foil recycling and sustainability becoming popular owing to battery makers’ efforts toward circular supply chains.

-

The use of advanced surface treatments decreasing losses during the transmission process of high-frequency PCB copper foil.

-

Solid-state batteries opening new avenues for copper foils due to advancements in battery cell design.

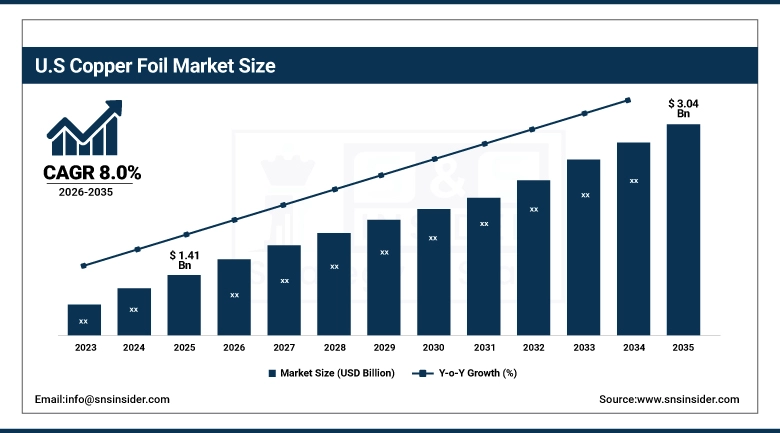

U.S. Copper Foil Market was valued at USD 1.41 billion in 2025 and is expected to reach USD 3.04 billion by 2035, at a CAGR of 8.0% from 2026 to 2035.

The U.S. copper foil market is growing at the fastest regional CAGR globally, driven by the rapid expansion of domestic EV battery manufacturing—the Inflation Reduction Act's domestic content requirements for battery tax credits are incentivizing domestic copper foil production for the first time. Major gigafactories from LG Energy Solution, Samsung SDI, Panasonic, and domestic battery manufacturers are establishing U.S. production that will create sustained domestic copper foil demand. The sophisticated U.S. PCB industry for military, aerospace, and high-end computing applications also sustains a premium domestic market.

Lotte Energy Materials (formerly Iljin Materials) secured an exclusive copper foil supply contract with StarPlus Energy's Indiana battery plant—a joint venture between Samsung SDI and Stellantis—representing exactly the kind of IRA-driven supply chain localization that is reshaping North America's copper foil demand landscape. As more gigafactories come online across the U.S., domestic copper foil supply will need to develop proportionally.

Copper Foil Market Segment Insights

-

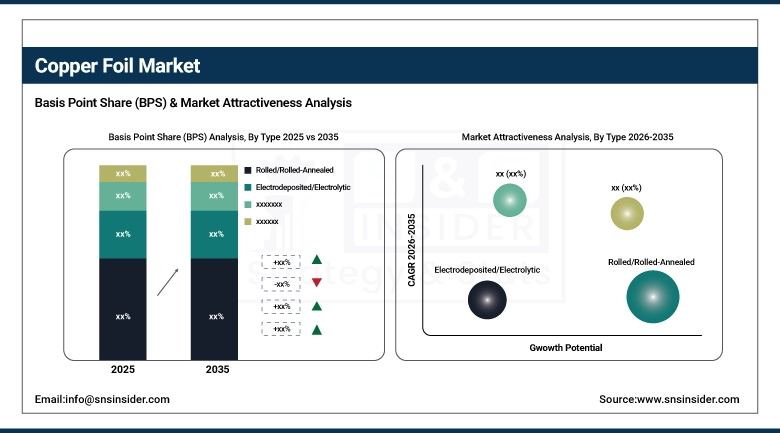

Based on Type, Rolled copper foil held 58% share in 2025 for flexibility-critical applications; Electrodeposited is growing fastest for high-volume battery production.

-

Based on Thickness, Standard thickness foils lead by volume; Ultra-Thin is the highest-value and fastest-growing segment for EV battery energy density.

-

Based on Application, Circuit Boards/PCBs held ~45% share as the established largest market; Li-Ion Batteries/EVs is growing fastest and will surpass PCBs in revenue.

Market Segment Analysis

By Type: Rolled/Rolled-Annealed dominates (58% share), Electrodeposited/Electrolytic Fastest Growing CAGR

Rolled copper foil is produced by mechanically rolling copper sheets through successive cold-rolling operations to progressively reduce thickness. The resulting foil has superior ductility and flexibility compared to electrodeposited alternatives because the rolling process aligns the copper crystal grain structure longitudinally. This flexibility makes rolled copper foil the preferred choice for flexible printed circuit boards (FPCBs) used in smartphones and wearables, high-frequency PCB applications where the smooth surface enables lower transmission loss, and battery applications requiring resistance to repeated bending stress.

Electrodeposited (ED) copper foil is produced by electrochemically depositing copper onto a rotating drum cathode from a copper sulfate electrolyte solution. The drum is peeled and the resulting foil has a very uniform thickness, fine grain structure, and excellent bonding surface for lamination to PCB substrates and battery electrode coatings. ED copper foil is the dominant format for high-volume PCB and lithium-ion battery manufacturing because it can be produced continuously at very high speeds in thicknesses as low as 4.5 micrometers. Advances in ED foil production technology are enabling thinner, stronger foil with controlled surface roughness profiles for different application requirements.

By Thickness: Ultra-Thin (≤12μm) dominates and fastest growing CAGR

Ultra-thin copper foils at 12 micrometers or below are the highest-value, fastest-growing segment of the copper foil market. In EV battery applications, thinner foil (as low as 4.5-6 micrometers) increases the energy density of battery cells by allowing more active electrode material per unit cell volume—critical for extending vehicle range without increasing battery weight. In PCB applications, ultra-thin foil enables finer circuit traces needed for high-density interconnect (HDI) PCBs in compact smartphones and advanced computing hardware. The technical difficulty of producing ultra-thin foil without defects and the specialized equipment required create significant barriers to entry and support premium pricing for leading producers.

By Application: Circuit Boards/PCBs (~45% share) dominates, Li-Ion Batteries/EVs Fastest Growing CAGR

PCB Copper Foil is the traditional largest application for copper foil, forming the backbone of almost all electronic devices. The PCB Copper Foil forms the conductive traces that connect electronic parts. The global PCB industry will grow along with the electronics industry, especially in cases where the PCBs are used for HDI or Multilayer applications in 5G base stations, AI accelerator cards, automotive electronics, and other medical applications.

The manufacture of Lithium-ion batteries is the fastest-growing segment for copper foil due to the global electrification of vehicles which will increase demand for copper foil at unprecedented rates. The Copper foil forms the anode current collector for all Lithium-ion battery cells, which is then bound with Graphite active material to form the negative electrode of the battery.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

78% |

|

Europe |

Germany |

32% |

|

Asia Pacific |

China |

58% |

|

Middle East & Africa |

UAE |

37% |

|

Latin America |

Brazil |

49% |

Asia Pacific Copper Foil Market Insights

Asia Pacific dominates the copper foil market with 65% of global revenue in 2024. China is the world's largest copper foil producer and consumer, home to CATL, BYD, and dozens of copper foil manufacturers. South Korea's Lotte Energy Materials (formerly Iljin Materials) and SKC are global leaders in ultra-thin battery copper foil. Japan's Furukawa Electric and Mitsui Mining & Smelting are dominant in high-end rolled copper foil for FPC and specialty PCB applications. Taiwan's Chang Chun Group serves the PCB supply chain for Taiwanese and global electronics manufacturers.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Copper Foil Market Insights

North America is the fastest-growing copper foil region, driven by IRA-incentivized EV battery gigafactory investment across the U.S. The domestic EV battery supply chain is being built from scratch, creating demand for domestic or near-sourced copper foil for the first time. American copper producers are evaluating copper foil production investments while Korean and Japanese producers are establishing U.S. manufacturing through partnerships and greenfield investments. The U.S. aerospace, defense, and high-end computing PCB market also sustains premium copper foil demand.

Europe Copper Foil Market Insights

Europe is an important market for copper foils due to German electric vehicle (EV) manufacturing, advanced electronics, and increasing renewable energy storage systems installations. Gigafactories in Germany and Sweden from Volkswagen, CATL, and Northvolt have generated new copper foil demand in Europe. Circuit Foil Luxembourg (Doosan) and Wieland Group cater to European printed circuit board (PCB) manufacturers. The EU Battery Regulation's focus on carbon emissions and supply chain transparency is redefining European copper foil procurement practices towards low-emission production.

Middle East & Africa and Latin America Copper Foil Market Insights

The Middle Eastern copper foil market is in its infancy but expanding due to electronics assembly facilities in UAE and Israel. Data center expansion in the region is generating PCB demand. African copper ore (mining in Democratic Republic of Congo, Zambia, South Africa) mining is aiding the supply chain although copper foil manufacturing in the downstream market is predominantly Asian. North African electronics manufacturing for the European market is generating additional copper foil demand in the region.

Latin America is one of the emerging copper foil markets, with Brazil and Mexico being the main consuming nations. The need for copper foils arises due to Mexico's manufacturing of electronic circuits for use by Original Equipment Manufacturers (OEMs). Brazil’s emergence as an automobile manufacturer for electric vehicles is also driving demand for copper foils. In Chile, being the largest producer of copper, copper foil manufacturing presents itself as a good opportunity.

Market Growth Drivers

EV battery demand and PCB proliferation are the dual structural growth drivers

The electrification of global transportation is the most significant driver of copper foil market growth, creating demand for copper foil at a scale that will dwarf all previous growth drivers. EV battery cell manufacturing requires precision copper foil at 6-12 micrometers thickness in enormous quantities—a single gigafactory producing 50 GWh of cells annually consumes thousands of metric tonnes of copper foil. Simultaneously, the continued growth of electronics including 5G infrastructure, AI computing, and consumer devices maintains steady PCB copper foil demand. These two demand streams are growing in parallel, providing diversified market support.

The IRA's domestic content requirements for the clean vehicle tax credit are creating a structural shift in North American copper foil sourcing. Batteries must contain increasing proportions of North American-produced components to qualify for the full tax credit, making domestic copper foil supply a competitive necessity for battery manufacturers serving the U.S. auto market. This policy effect is triggering significant copper foil manufacturing investment in North America that will permanently reshape the regional market.

Market Restraints

Copper price volatility and high capital intensity of ultra-thin foil production create supply challenges

Copper is a commodity metal that is affected by cycles in its pricing because of macroeconomic conditions around the world, mining considerations, and speculation. High prices of copper reduce the profit margins in producing copper foils and may cause complications in fulfilling supply contracts. The production of very thin copper foils relies on sophisticated equipment using electroplating technology that can produce sheets with a consistent thickness of 4-6 micrometers without any imperfections. These machines are expensive and take a long time to be delivered, making it hard to expand production when demand increases.

Market Opportunities

Solid-state batteries and 5G/AI infrastructure create premium copper foil opportunities

Solid-state battery development represents a significant opportunity for advanced copper foil producers because solid-state cell designs may require thinner, more precisely controlled copper foil than current lithium-ion technology. Companies that establish ultra-thin foil production capabilities now will be positioned to serve next-generation solid-state battery manufacturers. The buildout of 5G millimeter-wave infrastructure and AI data center network equipment requires ultra-low-loss PCB copper foil with engineered surface profiles that minimize transmission loss—a premium product segment that commands significantly higher pricing than standard PCB copper foil.

Recent Developments

-

2026: Freeport-McMoRan emphasized the robust long-term demand for copper due to the growing requirement of electrification and artificial intelligence infrastructures. Freeport-McMoRan has started increasing its projects for recovering and mining copper due to increased demand from industries.

-

2026: BHP and Lundin Mining expanded investment in Argentina’s Vicuña copper district to around USD 800 million. This project would support the long-term copper supply growth for rising global demand from electrification, AI data centers, and energy transition sectors.

-

2026: Mitsui Kinzoku announced a 12% price increase for its MicroThin copper foil products due to rising raw material and labor costs. The move reflects strong demand from PCB and AI-driven electronics applications, tightening global supply conditions.

Copper Foil Market Key Players

Some of the companies in the Copper Foil Market:

-

Lotte Energy Materials

-

SKC Nexilis

-

Furukawa Electric Co. Ltd.

-

Mitsui Mining & Smelting Co. Ltd.

-

JX Advanced Metals

-

Chang Chun Petrochemicals Co. Ltd.

-

Circuit Foil Luxembourg

-

Nippon Denkai Ltd.

-

Targray Technology International

-

Panasonic Holdings Corporation

-

ILJIN Materials Co. Ltd.

-

LS Mtron Ltd.

-

Nan Ya Plastics Corporation

-

Kingboard Copper Foil Holdings Limited

-

Fukuda Metal Foil & Powder Co. Ltd.

-

Jiayuan Technology

-

Tongling Nonferrous Metals Group

-

Guangdong Jia Yuan Technology

-

Shengda Group

-

Hindalco Industries Ltd.

Copper Foil Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.85 Billion |

| Market Size by 2035 | USD 16.9 Billion |

| CAGR | CAGR of 7.88% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Rolled/Rolled-Annealed, Electrodeposited/Electrolytic) • By Thickness (Standard [>18μm], Ultra-Thin [≤12μm], Others) • By Application (Circuit Boards/PCBs, Li-Ion Batteries/EVs, Consumer Electronics, Industrial, Solar & Renewable Energy, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lotte Energy Materials, SKC Nexilis, Furukawa Electric Co. Ltd., Mitsui Mining & Smelting Co. Ltd., JX Advanced Metals, Chang Chun Petrochemicals Co. Ltd., Circuit Foil Luxembourg, Nippon Denkai Ltd., Targray Technology International, Panasonic Holdings Corporation, ILJIN Materials Co. Ltd., LS Mtron Ltd., Nan Ya Plastics Corporation, Kingboard Copper Foil Holdings Limited, Fukuda Metal Foil & Powder Co. Ltd., Jiayuan Technology, Tongling Nonferrous Metals Group, Guangdong Jia Yuan Technology, Shengda Group, Hindalco Industries Ltd. |

Frequently Asked Questions

Ans: Asia Pacific leads with 65% market share; North America is the fastest-growing region driven by IRA-incentivized EV battery gigafactory investment.

Ans: Rolled copper foil holds 58% market share for flexibility-critical PCB and FPC applications; Electrodeposited is growing fastest for high-volume battery production.

Ans: Li-Ion Battery/EV applications are growing fastest, driven by the global EV transition creating massive demand for copper foil as the anode current collector.

Ans: The Copper Foil Market was valued at USD 7.85 billion in 2025.

Ans: The Copper Foil Market is expected to grow at a CAGR of 7.88% from 2026 to 2035.

Get in Touch