Corrosion Monitoring Market Report Scope & Overview:

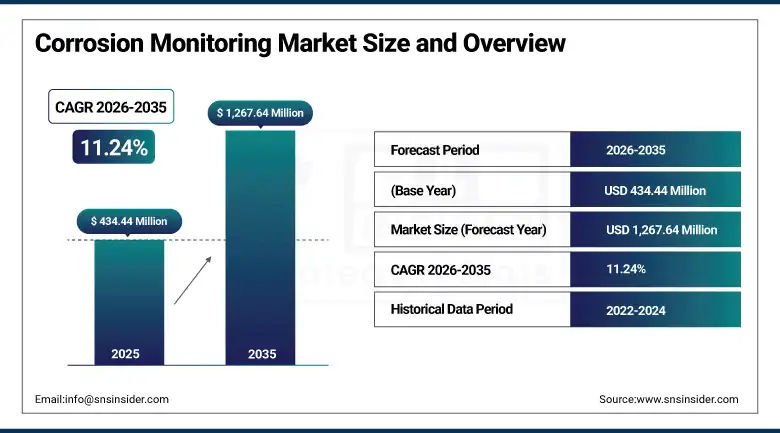

The Corrosion Monitoring Market was valued at USD 434.44 Million in 2025 and is expected to reach USD 1,267.64 Million by 2035, growing at a CAGR of 11.24% from 2026–2035.

The global corrosion monitoring market is witnessing significant expansion, driven by the escalating need for predictive maintenance and asset integrity management across process-intensive industries. Corrosion monitoring encompasses the continuous or periodic assessment of corrosion activity in industrial equipment, pipelines, pressure vessels, storage tanks, and structural assets. Industries including oil and gas, chemical processing, power generation, and marine are increasingly adopting advanced corrosion monitoring solutions to prevent catastrophic equipment failures and ensure operational safety. The market is propelled by regulatory safety mandates, ageing infrastructure requiring enhanced monitoring intensity, and the progressive adoption of IIoT-connected corrosion sensors that enable real-time remote monitoring and predictive maintenance integration in asset integrity management programmes.

In March 2024, RPA's Anticorrosion Paint Meetings 2025 showcased 85 exhibitors presenting the latest advancements in industrial anti-corrosion coatings and monitoring technologies, featuring expert-led discussions on decarbonization and sustainable corrosion management practices. The event reflects the commercial momentum of corrosion monitoring technology development whose convergence with sustainable industrial operations is creating demand for lower-impact monitoring solutions that satisfy both asset integrity and environmental performance objectives simultaneously.

Market Size and Forecast

-

Market Size in 2026E: USD 483.24 Million

-

Market Size by 2035: USD 1,267.64 Million

-

CAGR: 11.24% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

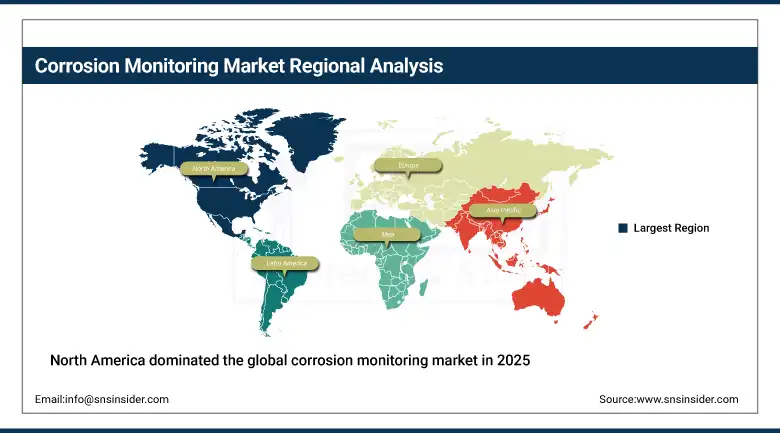

Largest Region: North America

To Get more information On Corrosion Monitoring Market - Request Free Sample Report

Corrosion Monitoring Market Trends

-

IIoT-connected corrosion sensors enable real-time remote monitoring of pipelines and tanks, eliminating manual coupon retrieval and analysis processes.

-

AI and machine learning in corrosion platforms enable predictive modelling, helping operators anticipate corrosion progression and prevent failures early.

-

Non-intrusive ultrasonic corrosion monitoring allows continuous thickness measurement without shutdowns, improving operational efficiency and safety significantly.

-

Hydrogen embrittlement monitoring is rising due to hydrogen economy expansion, requiring specialized corrosion tracking in pipelines and pressure vessels.

-

Digital twin integration with corrosion data enables virtual asset modelling, improving remaining life prediction and inspection planning accuracy.

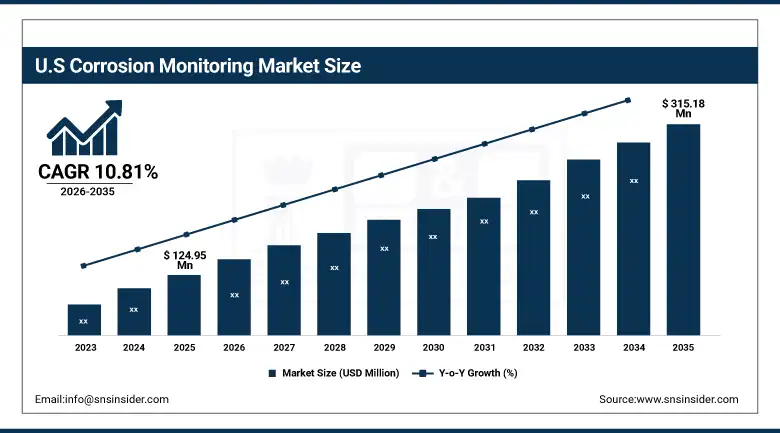

The U.S. Corrosion Monitoring Market Outlook

The U.S. Corrosion Monitoring Market was valued at approximately USD 124.95 Million in 2025 and is expected to reach approximately USD 315.18 Million by 2035, growing at a CAGR of approximately 10.81%.

The U.S. is the most commercially significant corrosion monitoring market within North America's dominant regional revenue position. Emerson Electric's Roxar corrosion monitoring systems, Honeywell's asset integrity solutions, Baker Hughes' pipeline integrity technologies, MISTRAS Group's inspection services, and Cosasco's corrosion probe and coupon systems collectively define the domestic commercial landscape. The ageing U.S. oil and gas pipeline infrastructure, the chemical manufacturing sector's asset integrity compliance requirements, and the power generation industry's boiler and heat exchanger monitoring programmes create structured institutional corrosion monitoring procurement. The U.S. Department of Transportation's Pipeline and Hazardous Materials Safety Administration's integrity management regulations create compliance-driven monitoring investment across the approximately 3.3 million miles of U.S. pipeline network.

In 2024, Emerson Electric expanded its Roxar Corrosion Monitoring System portfolio with new multi-point wireless sensor nodes capable of transmitting real-time corrosion rate data from multiple pipeline monitoring locations to a centralised asset integrity dashboard without requiring wired connection installation. The product innovation addresses the commercial barrier of wired sensor installation cost in remote pipeline environments where cable routing across long pipeline segments creates disproportionate installation investment relative to the monitoring hardware cost.

Corrosion Monitoring Market Segment Analysis

-

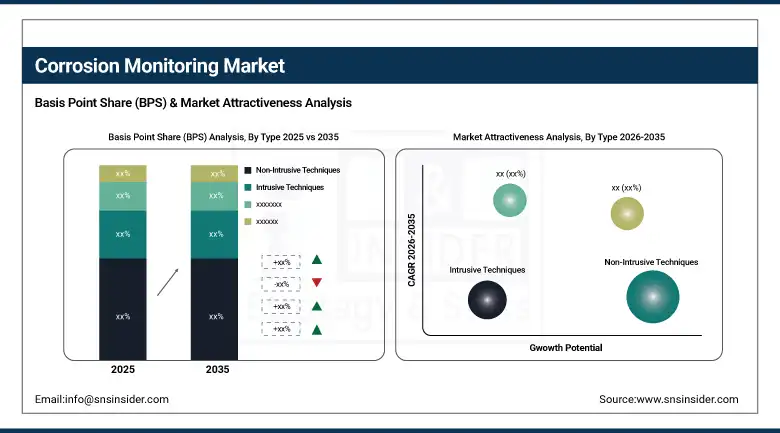

By Type, the non-intrusive techniques segment dominated the corrosion monitoring market with approximately 64% share in 2025, while the intrusive techniques segment is the fastest growing.

-

By Technique, the electrical resistance segment dominated the corrosion monitoring market with approximately 25% share in 2025, while the ultrasonic thickness measurement segment is the fastest growing.

-

By Probe Type, the electro-chemical segment dominated the corrosion monitoring market with approximately 42% share in 2025, while the electrical segment is the fastest growing.

-

By End User, the oil & gas segment dominated the corrosion monitoring market with approximately 32% share in 2025, while the chemical & petrochemical segment is the fastest growing.

By Type, non-intrusive dominates, intrusive grows fastest

Non-intrusive corrosion monitoring techniques retained the dominant type position with approximately 64% of the corrosion monitoring market in 2025. Their commercial primacy reflects the operational safety and productivity advantage that process-independent monitoring capability provides for asset operators whose production continuity creates financial motivation to avoid the process shutdown and depressurization that intrusive probe installation requires. Non-intrusive ultrasonic thickness measurement whose clamped or bonded transducers monitor wall thickness from external surfaces without fluid contact, acoustic emission monitoring whose passive sensor arrays detect corrosion-induced acoustic events, and guided wave ultrasonics whose long-range screening capability covers extensive pipeline lengths from single access points collectively sustain non-intrusive monitoring's dominant commercial position.

Intrusive techniques are the fastest-growing type because the established electrochemical and electrical resistance probe technologies' proven accuracy for direct corrosion rate measurement in process fluids creates structured installation demand in new facility construction and planned maintenance outage retrofit programmes. Each refinery turnaround and plant shutdown creates an intrusive probe installation opportunity whose scheduling during planned maintenance minimizes the production impact that continuous operation precludes. The growing awareness of corrosion monitoring value in chemical and petrochemical processing, where complex fluid corrosivity creates asset integrity risk that non-intrusive external monitoring cannot fully characterize, creates above-average intrusive probe system procurement.

By Technique, electrical resistance dominates, ultrasonic grows fastest

Electrical resistance retained the dominant technique position with approximately 25% of the corrosion monitoring market in 2025. The ER probe's commercial primacy reflects its versatility across both aqueous and non-aqueous environments, its ability to provide continuous corrosion rate measurement without process fluid conductivity requirement, and its established technology base whose operational simplicity and interpretation straightforwardness create specification preference across oil and gas and chemical processing applications. Each pipeline corrosion monitoring programme, each tank bottom monitoring installation, and each process vessel corrosion rate verification creates electrical resistance probe procurement whose commercial aggregate across global oil and gas and chemical processing infrastructure sustains the technique's dominant position.

Ultrasonic thickness measurement is the fastest-growing technique because its precision non-destructive evaluation capability for measuring remaining wall thickness in pipelines, pressure vessels, and storage tanks without process interruption creates growing adoption as digital inspection system integration improves data management and trend analysis. The technique's ability to detect localized corrosion pitting and general wall loss from external surface access, combined with permanently installed ultrasonic thickness sensor arrays whose continuous monitoring eliminates periodic manual survey requirements, creates commercial momentum that positions UTM as the technology of choice for next-generation continuous corrosion monitoring systems.

By End User, oil & gas dominates, chemical grows fastest

Oil and gas retained the dominant end-user position with approximately 32% of the corrosion monitoring market in 2025. The sector's commercial primacy reflects the extraordinary severity and breadth of its corrosion challenge, encompassing upstream production facility equipment exposed to sour crude and hydrogen sulphide, midstream pipeline networks transporting wet gas and multiphase fluids, and downstream refinery heat exchangers, towers, and pressure vessels processing complex hydrocarbon streams. Corrosion failures in oil and gas create consequences including catastrophic structural failure, environmental contamination, and loss of human life whose severity creates non-discretionary monitoring investment that regulatory mandates reinforce.

Chemical and petrochemical is the fastest-growing end-user because the industry's exposure to highly aggressive process fluids including strong acids, caustic solutions, chlorinated compounds, and reactive chemicals creates corrosion challenges that monitoring investment intensity reflects. Each chemical plant whose process fluid corrosivity requires continuous corrosion rate monitoring to prevent catastrophic equipment failure creates structured procurement whose compliance with Process Safety Management regulations under OSHA PSM 29 CFR 1910.119 sustains investment independent of commercial ROI calculation.

By Probe Type, electro-chemical dominates, electrical grows fastest

Electro-chemical probes retained the dominant probe type position with approximately 42% of the corrosion monitoring market in 2025. Their commercial primacy reflects the real-time corrosion rate quantification capability that linear polarization resistance, electrochemical impedance spectroscopy, and electrochemical noise measurement provide in conductive aqueous process environments where water chemistry changes create corrosion rate fluctuations whose timely detection enables chemical treatment programme optimization.

Electrical probes are the fastest-growing probe type because the electrical resistance probe technology's versatility across both wet and dry process environments, its established supply chain and installation infrastructure, and the growing IIoT wireless transmission capability for ER probe data collectively create above-average adoption in new facility construction and retrofit monitoring programmes. Each oil and gas production facility, pipeline monitoring station, and process plant that establishes a corrosion monitoring programme creates electrical resistance probe procurement.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Corrosion Monitoring Market Insights

North America dominated the global corrosion monitoring market in 2025, driven by its strong industrial base in oil and gas, manufacturing, and power generation sectors, substantial ageing infrastructure requiring intensive monitoring programmes, and the strong adoption of AI-enabled inspection tools and non-intrusive monitoring systems. The United States accounts for approximately 87.4% of North American revenues through Emerson Electric's Roxar systems, Honeywell, Baker Hughes, MISTRAS Group, and Cosasco’s commercial operations whose combined portfolio defines the domestic corrosion monitoring technology standard.

Canada contributes approximately 12.6% of North American revenues through its oil sands and conventional oil and gas industry’s pipeline and facility corrosion monitoring investment, the petrochemical sector's process equipment monitoring, and the aging power generation infrastructure’s integrity management programmes.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Corrosion Monitoring Market Insights

Europe is a technically sophisticated corrosion monitoring market where the North Sea oil and gas industry’s mature field integrity management requirements, the chemical industry’s process equipment monitoring compliance, and stringent EU industrial safety regulations create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its chemical and petrochemical industry’s extensive monitoring programmes, TÜV Rheinland’s corrosion risk assessment services, and the power generation sector’s boiler and heat exchanger integrity management.

The United Kingdom and Norway are significant secondary markets where the North Sea offshore oil and gas industry’s subsea pipeline and topside facility corrosion monitoring investment creates consistent above-average per-facility commercial value. Applus+ and Intertek Group’s European NDT and corrosion inspection service operations sustain European market supply from established commercial presences.

Asia Pacific Corrosion Monitoring Market Insights

Asia Pacific is the fastest-growing regional corrosion monitoring market, driven by rapid industrialization in China, India, Japan, South Korea, and Southeast Asia where oil and gas, power generation, chemicals, and construction sectors are all susceptible to corrosion and are investing in monitoring infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through its expanding petrochemical capacity, the natural gas pipeline network’s integrity management investment, and the chemical industry’s asset protection programme adoption.

India represents the most commercially dynamic emerging market within Asia Pacific where the ageing refinery infrastructure’s monitoring upgrade investment, the expanding pipeline network’s integrity management requirement, and the growing chemical industry’s safety compliance investment create above-average corrosion monitoring procurement growth.

MEA & Latin America Corrosion Monitoring Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Saudi Aramco’s world-class pipeline and facility corrosion monitoring programmes, the Gulf petrochemical industry’s process equipment integrity management, and ADNOC’s offshore platform and subsea pipeline monitoring investment. The UAE’s growing industrial facilities and desalination plant infrastructure create additional corrosion monitoring demand across the Gulf. Brazil leads Latin American revenues at approximately 44.2% through Petrobras’ offshore deepwater platform corrosion monitoring, the refining sector’s integrity management investment, and the expanding pipeline network’s monitoring programme. Mexico’s oil and gas sector and Chile’s mining industry collectively sustain growing regional engagement.

Market Dynamics

Growth Drivers: Ageing oil and gas infrastructure and regulatory asset integrity mandates creating non-discretionary monitoring investment

Ageing oil and gas infrastructure is the corrosion monitoring market’s most commercially certain structural growth driver. The United States’ approximately 3.3 million miles of pipeline network whose average age exceeds 40 years, the North Sea’s mature offshore oil and gas fields, and the Middle East’s legacy refinery infrastructure collectively create intensive corrosion monitoring requirements whose investment scale grows proportionally with asset age and remaining service life extension objectives. Each decade of additional asset operation requires increasing monitoring density and frequency whose commercial impact on monitoring procurement sustains above-average market growth independent of new facility construction investment cycles.

Regulatory asset integrity mandates including PHMSA’s Pipeline Integrity Management Rule, OSHA’s PSM standard, and API 510, API 570, and API 653 pressure vessel, piping, and storage tank inspection standards collectively create legally mandated corrosion monitoring investment whose compliance motivation sustains procurement through economic cycles. Each regulatory inspection interval and each threshold corrosion rate that triggers mandatory remediation creates structured corrosion monitoring programme investment that operators cannot defer without regulatory non-compliance risk.

Restraints: High installation cost in remote and offshore environments and skilled corrosion engineer shortage

Corrosion monitoring system installation cost in remote pipeline environments, offshore platforms, and subsea applications creates procurement barriers whose engineering access, installation infrastructure, and environmental protection requirements create total system cost substantially exceeding equivalent onshore facility installation. Each offshore monitoring system installation whose diver or ROV access requirement adds engineering cost creates commercial pressure toward non-intrusive monitoring alternatives whose external sensor installation avoids the access cost penalty that intrusive probe installation creates in offshore environments.

Skilled corrosion engineering talent shortage creates a technical capability constraint that limits the pace at which organisations can design, commission, and operate advanced corrosion monitoring programmes. The specialized corrosion science, electrochemistry, and materials engineering expertise required to interpret monitoring data, diagnose corrosion mechanisms, and specify monitoring programme design creates staffing requirements that the global corrosion engineering talent pool cannot fully satisfy at current market demand growth rates.

Opportunities: Hydrogen infrastructure monitoring and IIoT wireless sensor network deployment

Hydrogen infrastructure monitoring represents the most commercially certain near-term market expansion opportunity as the global hydrogen economy’s pipeline, pressure vessel, and storage infrastructure development creates new corrosion monitoring requirements specific to hydrogen environment embrittlement, stress corrosion cracking, and diffusion-driven material degradation. Each new hydrogen pipeline commissioned, each hydrogen storage facility completed, and each electrolyzer and fuel cell system deployed creates corrosion monitoring procurement whose technical requirements create differentiated commercial opportunities for monitoring technology suppliers capable of addressing hydrogen-specific degradation mechanisms.

IIoT wireless sensor network deployment represents the most commercially transformative near-term technology opportunity whose elimination of wired infrastructure cost and installation complexity enables large-scale monitoring network deployment across extensive pipeline systems and multi-asset facility portfolios at economics that conventional wired monitoring systems cannot achieve. Each wireless corrosion sensor network deployment that monitors hundreds of pipeline monitoring points from a single data concentrator creates commercial adoption whose operational cost advantage over manual inspection programmes sustains investment in high-density monitoring infrastructure.

Recent Developments:

-

2026: MISTRAS Group expanded its digital corrosion monitoring services in 2026 by deploying advanced ultrasonic thickness monitoring and digital twin integration for continuous structural health assessment of industrial assets.

-

2025: Emerson Electric (Roxar) enhanced its corrosion monitoring systems in 2025 with upgraded IIoT-enabled wireless corrosion sensors, enabling real-time pipeline integrity data transmission and improved offshore asset monitoring efficiency.

-

2025: Baker Hughes advanced its corrosion management solutions in 2025 by integrating AI-driven predictive corrosion analytics into asset integrity platforms, improving early detection of material degradation in oil and gas infrastructure.

Corrosion Monitoring Market key players are:

-

Emerson Electric Co. (Roxar)

-

Honeywell International Inc.

-

Baker Hughes Company

-

SGS SA

-

Intertek Group plc

-

MISTRAS Group Inc.

-

Cosasco (Rohrback Cosasco Systems)

-

Rysco Corrosion Services Inc.

-

Applus+ Services SA

-

TUV Rheinland Group

-

Corr Instruments LLC

-

Matergenics Inc.

-

BAC Corrosion Control Ltd.

-

RS Corrosion Services Inc.

-

Intero Integrity Services

-

Clamp On AS

-

3X Engineering

-

Korosi Specindo

-

Metal Samples Company (Alabama Specialty Products)

-

Pepperl+Fuchs SE

Corrosion Monitoring Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 434.44 Million |

| Market Size by 2035 | USD 1,267.64 Million |

| CAGR | CAGR of 11.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Non-Intrusive Techniques, Intrusive Techniques) • By Technique (Electrical Resistance, Corrosion Coupons, Linear Polarization Resistance, Ultrasonic Thickness Measurement, Galvanic Monitoring, Hydrogen Penetration Monitoring, Biological Monitoring, Others) • By Probe Type (Electrical, Mechanical, Electro-Chemical) • By End User (Oil & Gas, Chemical & Petrochemical, Power Generation, Manufacturing, Pulp & Paper, Water & Wastewater, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Emerson Electric Co. (Roxar), Honeywell International Inc., Baker Hughes Company, SGS S.A., Intertek Group plc, MISTRAS Group Inc., Cosasco (Rohrback Cosasco Systems), Rysco Corrosion Services Inc., Applus+ Services S.A., TÜV Rheinland Group, Corr Instruments LLC, Matergenics Inc., BAC Corrosion Control Ltd., RS Corrosion Services Inc., Intero Integrity Services, ClampOn AS, 3X Engineering, Korosi Specindo, Metal Samples Company (Alabama Specialty Products), Pepperl+Fuchs SE |

Frequently Asked Questions

The Corrosion Monitoring Market is expected to grow at a CAGR of 11.24% from 2026 to 2035.

The Corrosion Monitoring Market was valued at USD 434.44 Million in 2025.

Ageing oil and gas pipeline and refinery infrastructure requiring intensified corrosion monitoring programmes to extend asset service life.

Non-Intrusive Techniques dominated the Corrosion Monitoring Market with approximately 64% share in 2025.

North America dominated the Corrosion Monitoring Market in 2025.

Get in Touch